SOJE - HTD: Well Positioned For A Recession But Struggling With The Distribution

2023-09-01 12:17:32 ET

Summary

- The John Hancock Tax-Advantaged Dividend Income Fund focuses on high-yielding dividend-paying stocks, particularly in the utility sector.

- The fund's declining share price presents an opportunity for investors, as it currently yields 8.61% and has a strong distribution track record.

- The fund's leverage and ability to cover its distribution with net investment income are concerning, and its net assets have been declining for eighteen months.

- The fund's leverage appears a bit high for the current situation, and other funds have been forced to slash their distributions due to interest costs.

- The fund is currently trading at a discount to the net asset value, so the price is very reasonable.

The John Hancock Tax-Advantaged Dividend Income Fund ( HTD ) is a closed-end fund ("CEF") that specializes in providing a high level of income for its investors without sacrificing capital gains potential. This is because the fund's strategy is investing in high-yielding dividend-paying stocks. As I stated in my last article on this fund, the fund's management has historically favored utility stocks as a source of dividends. This is something that could prove to be very advantageous right now, as utilities tend to enjoy remarkably stable cash flows over time. The Leading Economic Indicators have now been down for 16 straight months , which is historically a sign of an impending recession.

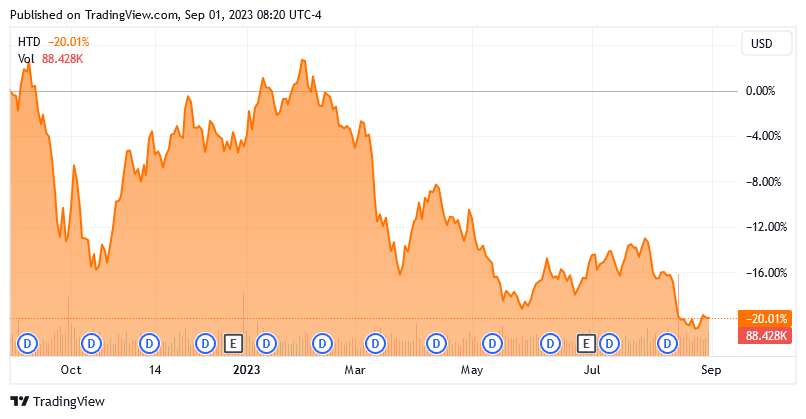

The utility sector does not suffer as much as many other sectors during a recession due to the fact that its product is typically considered to be a necessity. With that said, most dividend-paying companies tend to be financially strong companies with reliable cash flows even in recessions so most of the companies in this fund should hold up okay in the event of a recession, at least in terms of financial performance. The fact that a company's cash flows are relatively stable does not mean that the stock market will not sell it off anyway, though. We can see this in the fact that the John Hancock Tax-Advantaged Dividend Income Fund is down 20.01% over the past twelve months:

{kind=link}

This is despite the fact that the cash flows of many of the companies held by this fund have been reasonably stable. The fund's declining share price may have created an opportunity for investors though, as it currently yields 8.61% and is one of the few funds that has not cut its distribution in the past year. In fact, the fund has one of the strongest distribution track records of any closed-end fund. It has been a few months since we last discussed it, so let us revisit this fund and see if it could be a good addition to your portfolio today.

About The Fund

According to the fund's webpage , the John Hancock Tax-Advantaged Dividend Income Fund has the objective of providing its investors with a high level of after-tax total return. That is not especially surprising as the fund invests primarily in common equities. As we can see here, 64.62% of the fund's portfolio currently consists of common stock:

CEF Connect

This is a slight decrease in the fund's common stock weighting compared to the level that the fund had the last time that we discussed it. The fund increased its preferred stock and bond allocations to compensate for this change. That could be a sign that the fund's management expects that a recession may be about to hit. One of the characteristics of a recession is that common stocks decline but preferred stocks and bonds tend to hold up somewhat better. There are two reasons for this:

Corporate earnings typically decline during a recession, which causes the market to assign lower valuations to common stocks. The dividends and coupon payments paid by preferred stocks and bonds do not change, however, since these assets have no inherent link to the actual financial performance of the issuing company. The Federal Reserve usually reduces interest rates in a recession to stimulate capital investment and pull the national economy out of the recession.

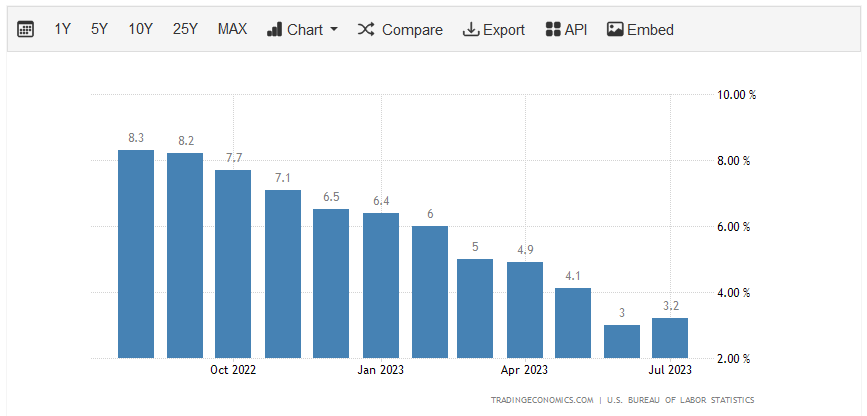

In this case, I highly doubt that the Federal Reserve will cut rates in the event of a recession. One big reason for this is that inflation still remains very high and by some measures has actually started getting worse. The most recent inflation report said that the consumer price index went up by 3.2% year-over-year compared to 3.0% in June:

{kind=link}

As crude oil price gains show no sign of a downward reversal, it is unlikely that the next inflation numbers will show any real improvement. Thus, any impending recession is likely to be an inflationary one like the one in the late 1970s and early 1980s rather than the more recent ones that the United States experienced in which deflation was a concern. Chairman Powell stated last week in his Jackson Hole speech that the Federal Reserve will not cut rates until inflation is back down to 2% consistently.

Thus, it seems unlikely that the John Hancock Tax-Advantaged Dividend Income Fund will be able to get much in the way of near-term capital gains from the fixed-income assets in its portfolio. However, preferred stocks and bonds both boast much higher yields than common stocks. The fact that the fund includes a significant allocation to these two securities gives it a higher income than it could get from an all-common stock portfolio.

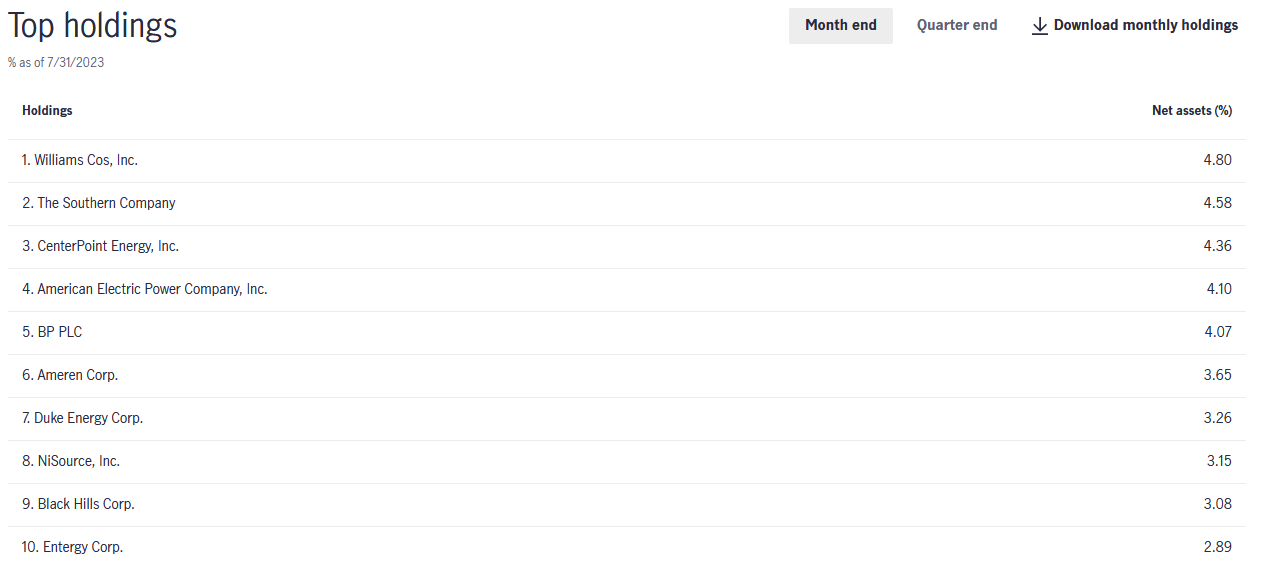

As I mentioned in the introduction to this article, the John Hancock Tax-Advantaged Dividend Income Fund invests heavily in utility companies as a source of income due to the high yields that these companies frequently possess. We can see that quite clearly by looking at the largest positions in the fund's portfolio:

{kind=link}

As many readers are likely aware, I have been discussing utilities with increasing frequency here at Seeking Alpha recently. As such, many of these companies will likely be familiar to many readers. In fact, the only company on this list that I have never explicitly discussed is The Southern Company ( SO ). The remainder of them have all been discussed in one of my previous articles at some time in the past.

There are two companies on this list that are not normally considered utilities. These are The Williams Companies ( WMB ), which is a natural gas-focused midstream company, and BP ( BP ), which is a supermajor energy. The Williams Companies has many of the same characteristics of a utility though, as its volume-based business model provides it with remarkably stable cash flows, especially considering that the majority of its customers are utilities that need natural gas for electric generation or for distribution to their customers. This chart shows The Williams Companies' operating cash flows during each of the past eleven twelve-month periods:

{kind=link}

This is about as close to the definition of stable cash flows as we can get! The company has slowly but surely grown its operating cash flows over time, regardless of any economic or commodity price changes that took place during the period. This is exactly the kind of company that we want to be invested in during difficult economic times such as what could be coming in the near future. The same can be said of the electric and natural gas utilities that comprise eight of the remaining nine positions in the above list.

The exception to the stable cash flows is BP, which will definitely be more affected by a recession than the other companies that comprise the fund's largest positions. However, as already mentioned, this recession is likely to be an inflationary one. In short, it will be a recession that is characterized by high rates of inflation. In such an environment, commodity prices tend to do pretty well. For example, let us have a look at how different asset classes performed during the 1970s:

Zero Hedge/Data from Bloomberg

As we can clearly see, commodities were the place to be for anyone looking for either a nominal or a real return. BP should do very well in such an environment as rising crude oil prices will have a positive effect on the company's financial performance.

Overall, we can conclude that the John Hancock Tax-Advantaged Dividend Income Fund is very well positioned for a near-term inflationary environment. That should be very appealing to anyone who is seeking to preserve their wealth and generate a high level of income in an uncertain economic climate characterized by inflation.

Leverage

As is the case with most closed-end funds, the John Hancock Tax-Advantaged Dividend Income Fund employs leverage in an attempt to boost its returns. I explained how this works in my last article on the fund:

"In short, the fund borrows money and then uses that borrowed money to purchase dividend-paying common and preferred stocks. As long as the interest rate that the fund pays on the borrowed money is less than the return that it receives from the purchased assets, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, so this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage, as that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason."

An additional concern right now involves interest rates. As of the time of writing, the federal funds target rate is 5.50%, so it will be difficult to borrow money at lower rates than this. That is a problem because there are very few stocks that yield above 5.50% today. Indeed, I can only think of a very small number outside of the traditional energy sector. For its part, the U.S. Utility Sector ETF ( IDU ) yields 2.66% at the current price. As such, it is going to be very difficult for the fund to generate sufficient investment returns to cover the costs of its leverage and have excess left over for shareholders. As I discussed in a recent article , this situation forced the Duff & Phelps Utility and Infrastructure Fund ( DPG ) to institute its first distribution cut in years. As such, we do not want the fund's leverage to be excessively high. However, this fund's leveraged assets currently comprise 36.50% of its portfolio. I will admit that this is above what I would really like to see, especially for a fund that is mostly invested in common equity. As such, there may be some risks here if the market declines or if rates keep going up.

Distribution Analysis

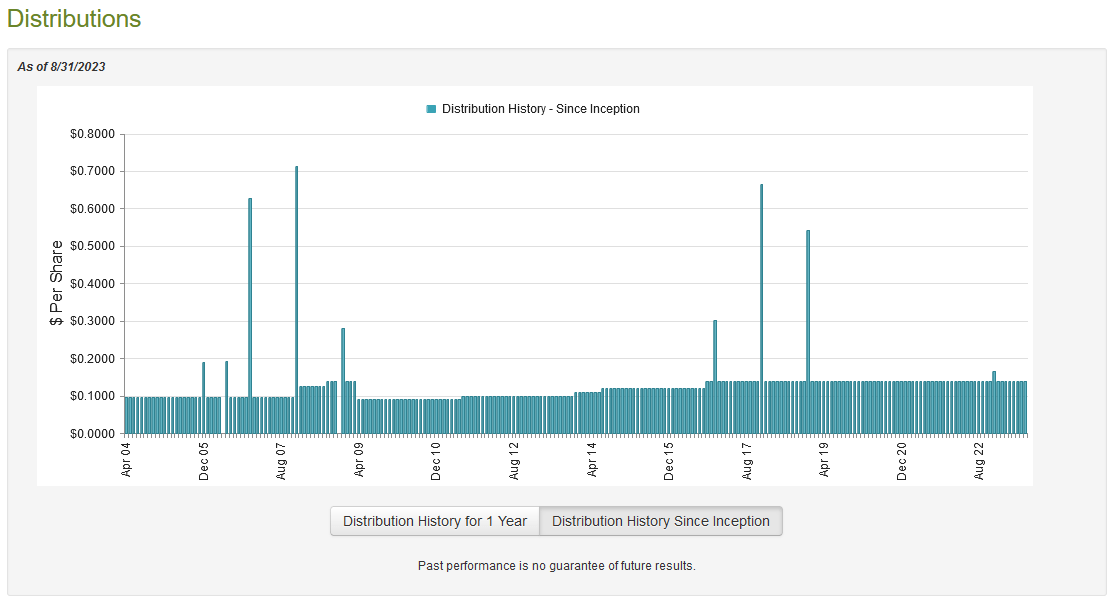

As mentioned earlier in this article, the primary objective of the John Hancock Tax-Advantaged Dividend Income Fund is to provide its investors with a high level of total return. Befitting the fund's name though, it invests primarily in dividend-paying common and preferred stocks to achieve this objective. The preferred stock will generally have a reasonably high yield. Some common stocks also have respectable yields, but these are generally lagging fixed-income securities in that area. The fund employs leverage to partially compensate for this and boost the effective yield of its portfolio. In addition, the fund aims to pay its capital gains out to the shareholders. As such, we can assume that the fund will have a fairly respectable yield itself. That is certainly the case as it pays a monthly distribution of $0.1380 per share ($1.656 per share annually), which gives it an 8.61% yield at the current price. The fund has been remarkably consistent with its distribution over time, as it has steadily increased it since 2009:

{kind=link}

This makes the John Hancock Tax-Advantaged Dividend Income Fund one of the few that has not cut its distribution in response to the challenges in the market that started last year. That will likely appeal to those investors who are seeking a safe and secure source of income to use to pay their bills and finance their lifestyles. It also fits pretty well with our thesis that this fund should be somewhat resistant to economic problems. As is always the case, it is critical to ensure that the fund can actually afford the distribution that it pays out. After all, a distribution cut would cause our income to decline and probably cause the share price to decline. Let us investigate this.

Fortunately, we have a relatively recent document that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the six-month period that ended on April 30, 2023. This is a newer report than we had available to us the last time that we discussed this fund, which is nice because it should give us a good idea of how well the fund handled the market turbulence at the end of last year. The market was pretty strong during the first few months of this year, so the fund may have been able to earn some capital gains. That will also be reflected in this report.

During the six-month period, the John Hancock Tax-Advantaged Dividend Income Fund received $23,802,724 in dividends along with $7,686,819 in interest from the assets in its portfolio. Once we net out the money that the fund had to pay in foreign withholding taxes, it had a total investment income of $31,344,633 during the period. The fund paid its expenses out of that amount, which left it with $15,741,844 available for shareholders. That was, unfortunately, nowhere near enough to cover the $30,296,719 that the fund paid out in distributions during the period. At first glance, this could be concerning as the fund clearly failed to cover its distribution with net investment income.

However, there are other ways through which the fund can obtain the money that it needs to cover its distribution. For example, it might have capital gains that could be paid out. Unfortunately, the fund generally failed at this task. It reported net realized losses of $27,273,338 which was partially offset by $26,455,493 in net unrealized gains during the period. Overall, the fund's net assets declined by $15,162,787 after accounting for all inflows and outflows during the period. This was roughly half of the distribution that is uncovered. That is certainly concerning, especially since the fund's net assets have now been declining for eighteen months. If this continues, it will be forced to cut the distribution. We need to keep an eye on this.

Valuation

As of August 31, 2023 (the most recent date for which data is available as of the time of writing), the John Hancock Tax-Advantaged Dividend Income Fund has a net asset value of $20.57 per share but the shares currently trade for $19.25 each. That gives the fund's shares a 6.42% discount on net asset value at the current price. This is a bit better than the 4.35% discount that the shares have had on average over the past month. As such, the current price appears to be a reasonable one to pay for the fund.

Conclusion

In conclusion, the John Hancock Tax-Advantaged Dividend Income Fund should be a reasonable way to protect yourself against a recession. This is due to the fact that most of the companies that the fund is invested in are non-cyclical entities that should not have their cash flows affected much by a recession. However, the fund is clearly struggling to maintain its distribution as its net investment income is not nearly enough to cover the distribution. That is likely to be the case for a while, especially as today's interest rates tend to make utilities unattractive. This could lag on the fund's performance for a while.

For further details see:

HTD: Well Positioned For A Recession, But Struggling With The Distribution