HDSN - Hudson Should Benefit From Tight Refrigerant Supply: Time To Buy The Dip

Summary

- A recent report from the U.S. Environmental Protection Agency shed some light on the supply situation for reclaimed refrigerants.

- The data hint that reclaimed refrigerants should remain at high prices.

- I explain why I am buying more of Hudson during this dip.

Introduction

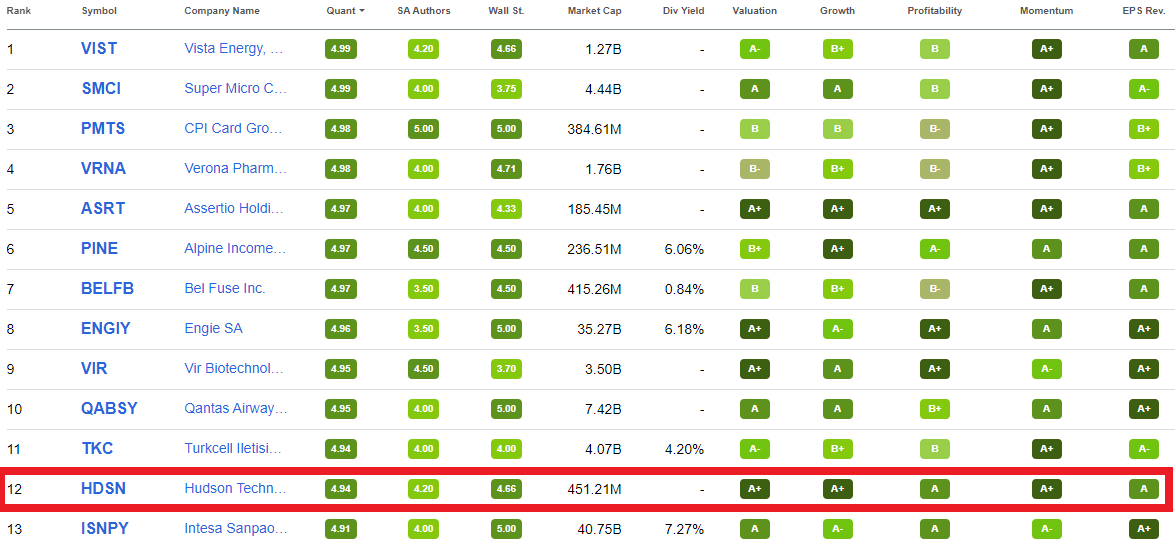

While bear markets are usually excellent times to buy stocks, they nonetheless challenge investors' patience and strategy. But even during bear markets, there are stocks that soar and not because they benefit from depressing news. Hudson Technologies ( HDSN ) has been such a stock this year, with a whopping 119.14% gain YtD. However, in the past ten days, the stock has given back around 22% of its gains, and it broke once again the $10 support. In this article, I would like to update my coverage and explain why I am buying once again a stock that is currently number 12 among the Seeking Alpha top rated stocks (by the way, Intesa Sanpaolo ( ISNPY ), a stock I cover and own, is number 13).

{kind=link}

The industry

Hudson caught my attention when it was added once again to the Russel 2002 at the end of June.

The company operates in the HVACR industry (Heating, Ventilation, Air Conditioning and Refrigeration) and it holds to spot in the supply chain. In fact, it possesses the technological know-how to reclaim old refrigerants in order to clean and recycle them so that they can be resold. Why is this important? Because, as virgin environmental-harmful refrigerants are phased down and can't be manufactured anymore, old air conditioning systems need to replace their refrigerants by buying reclaimed refrigerants. And guess what? Hudson can benefit from the fact that it is the largest reclaimer in the U.S. with a 35% market share and, as such, it is positioned to be the company people are turning to in order to find the refrigerants they need.

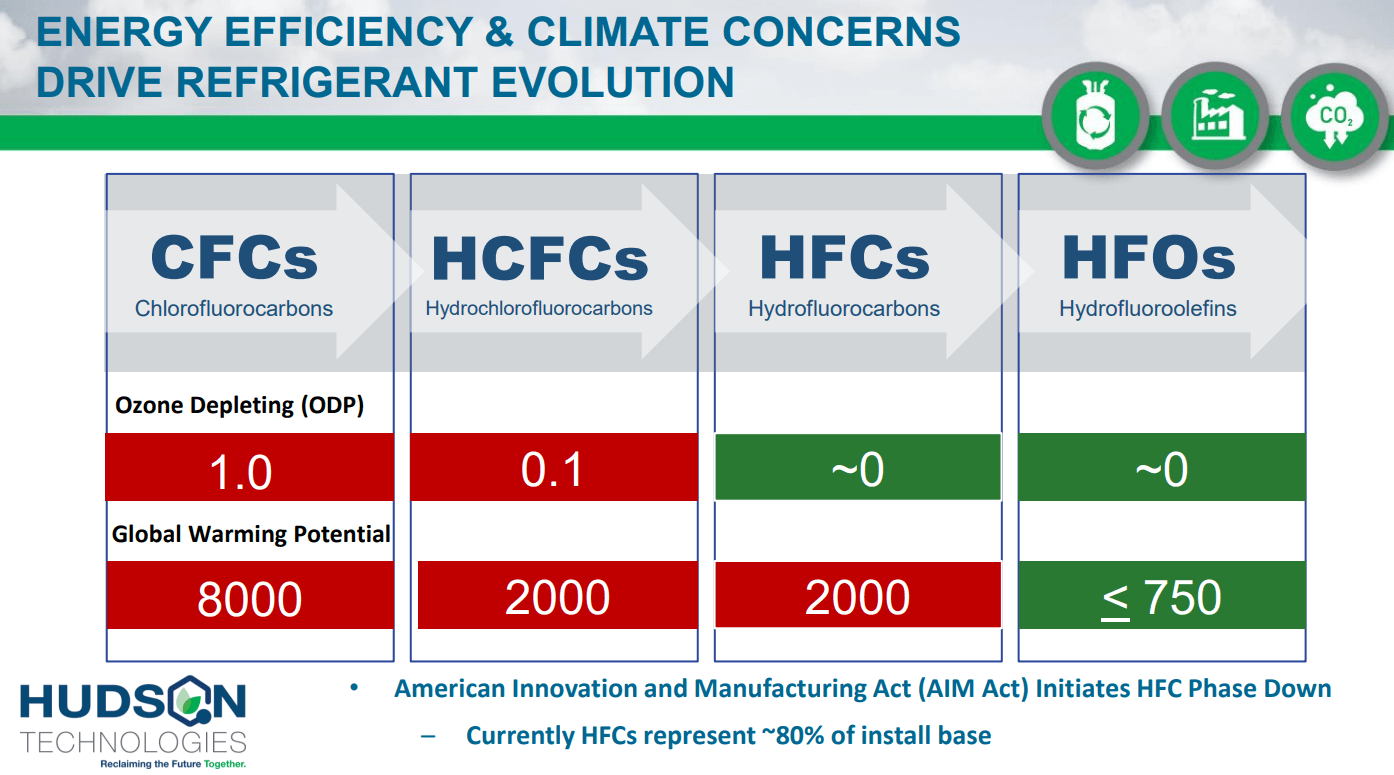

To better explain what is happening, here is a slide Hudson often shares in its presentation to explain the refrigerant evolution.

Hudson Technologies 2022 Investor Presentation

{kind=link}

As Hudson explains -

HFC refrigerants (hydrofluorocarbons) is the third generation of fluorinated refrigerants. Recognized as Ozone Depleting Potential ((ODP)) and Global Warming Potential ((GWP)), they represent a greener alternative to CFC and HCFC. Refrigerants in this group are applicable to refrigeration plants and air conditioning units designed specifically for their use. In addition, they can serve as drop-in replacements for older CFCs and HCFCs. Freons or hydrofluorocarbons ((HFC)) are the most widespread refrigerant gases in the market today. They have replaced chlorofluorocarbons ((CFC)) and hydrochlorofluorocarbons (HCFC), which damage the ozone layer. Since they can be utilized for more effective cooling and heating than other refrigerants, HFCs are a common choice for refrigerants. Because HFCs don't include chlorine, they have a smaller effect on the ozone layer. HFCs are also utilized in the manufacture of polymer foams as blowing agents, for fire protection, as solvents in cleaning goods, and for plasma etching in the creation of semiconductors. HFCs also break down very fast once they are released into the atmosphere, causing less harm to the atmospheric layers as a result. These crucial elements are anticipated to boost the demand for HFCs and support future market revenue growth.

Now, all air conditioners built before 2010 use HCFC-22, also known as R-22. Hudson is able to reclaim this refrigerant and, since in 2020 R-22 production ceased, there is now a supply issue for owners of R-22 air conditioning systems that are still functioning and don't need to be replaced yet. The situation is easy to understand: high demand and tight supply. The consequence is clear: as supplies of virgin refrigerants dwindle, reclaimed refrigerants will become more and more important, creating upward pricing pressure. Who benefits from this? Hudson and its margins.

Then in 2020, the American Congress approved the AIM act , that ruled the phasedown of virgin HFC production in the next 15 years. In particular, the Act mandates a 10% step down of HFCs production for 2023 and 2028, with a 40% reduction. This offers big tailwinds for Hudson that will be among the big players that can fill the lack of supply. If we consider that summers are becoming warmer and warmer, the need for refrigerants has another big tailwind.

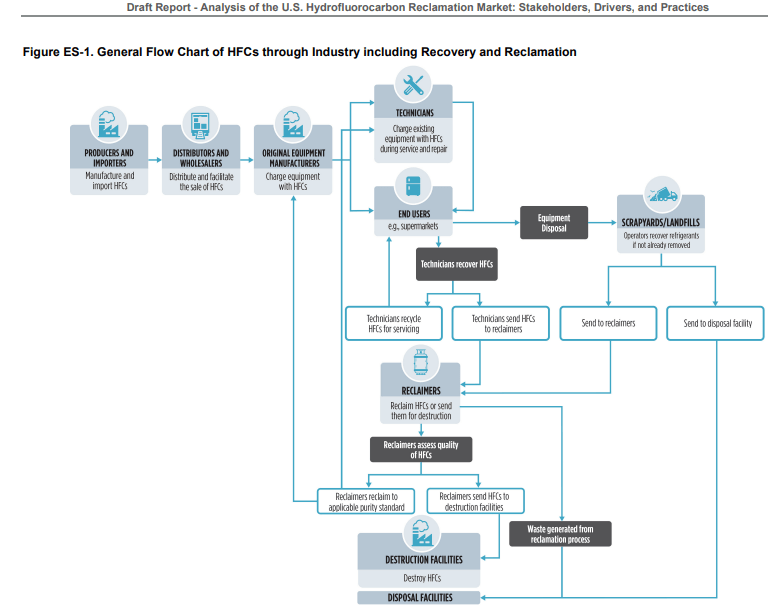

Here is a flow chart that shows the whole HFC cycle. We can see how reclaimers, such as Hudson, have a core role in this cycle as they are the ones that keep it going instead of sending all used refrigerants to disposal facilities.

U.S. Environmental Protection Agency

{kind=link}

Supply issues

As old refrigerants are phased down, there can be a big supply issue for customers who want and need them. This is why the EPA encourages reclamation. In fact, the Agency writes that

by bolstering the current supply of HFCs with refrigerants from existing systems, reclamation supports a smooth transition to alternatives. In addition, reclamation can minimize disruption of the current capital stock of equipment by allowing its continued use with existing refrigerant supplies

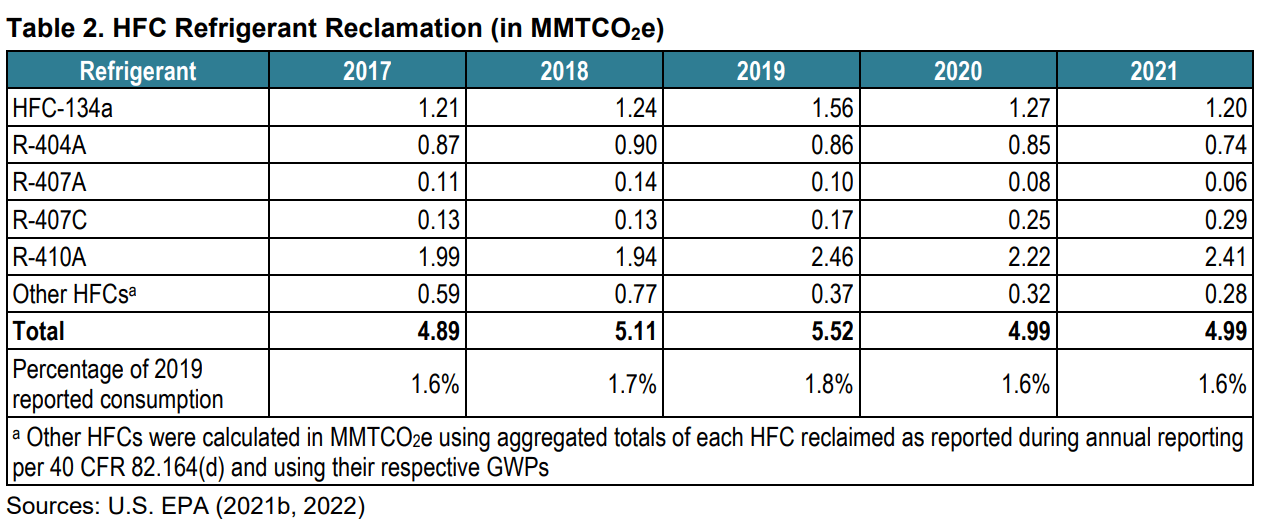

The big problem the industry is facing is that the quantity of refrigerants being recovered is not enough to meet demand. In fact, the EPA has collected data that show how, since 2017, the reclamation rate of HFCs (green columns) has increased only 6% as we can see in the graph below.

epa.gov

Over the next ten years, the EPA estimate predicts that under the HFC phasedown, reclaimed HFCs will increase in sales by $0.8 billion. However, the following table reports some data that highlight the fact that the refrigerant reclamation presents the total estimated reclaimed HFC refrigerants in MMTCO2e. EPA data indicate that the reclamation market is below 2 percent of the total.

{kind=link}

This situation can be understood as a strong tailwind for Hudson for the years to come. In fact, we see that a lot of used refrigerants are still not being reclaimed. On the other hand, we see that reclaimed refrigerant supplies are tight. Hudson can leverage its infrastructure of facilities and stocking points all over the country. In addition, Hudson owns reclamation facilities and AHRI certified laboratories that empower the company to carry out on its own the whole reclamation process.

{kind=link}

Hudson has thus two areas where it can perform well: encouraging people to sell back their used refrigerants and selling reclaimed refrigerants at high prices due to a foreseeable strengthening of demand for reclaimed old refrigerants.

Hudson: past results and future guidance

In Q1, the company saw a 149% revenue growth YoY. At half year revenues were up 72% with gross margins at 55% and operating income up 245% YoY coming in at $49.8 million. Though Hudson had cautioned investors to expect gross margins in the low 30s, even in the past quarter Hudson released a 49% result, way above expectations. All of this was due to the fact that reclaimed refrigerants' prices are increasing without a material appreciation in the cost basis of the refrigerants sold. After nine months, revenues are up 100% to $277.8 million and net income was up 278% to $98.7 million with EPS up to 275%. No wonder the stock soared. I think that the company will easily reach $300 million in revenue this year with a gross margin above 40%. Furthermore, the 2025 goal of $400 million in revenue can easily be achieved given the tailwinds we have already spoken of.

In fact, if the forecast is that this market will grow to a size of $800 million just for HFCs sales, and we assume that Hudson will maintain its 35% market share, just from this kind of reclamation Hudson should earn a $280 million in revenue, which is equal to what it made in the first nine months of this year from all its different reclaimed refrigerants. Unfortunately, the company doesn't break down its revenue by refrigerant type, nor do we know how the inventory the company carries is built up and at what average price (I actually tried to contact the investor relations office to ask these questions, but I haven't received a reply yet).

Valuation and conclusion

Hudson trades at a fwd P/E of 4.5. The fwd EV/EBITDA is a 3.5. If we look at price/cash flow, we see a very decent 8.5 and its free cash flow yield is currently a 10%. All these metrics show that the company is quite cheap. The discounted cash flow models I shared in my previous articles hint that we may be before a potential multibagger. By being conservative and slashing any kind of forecast by 50%, I still reach that the target price for the stock should be above $20. This is why I put aside some money to buy this recent dip.

For further details see:

Hudson Should Benefit From Tight Refrigerant Supply: Time To Buy The Dip