HHS - Hudson Technologies And Harte Hanks: 2 Swing Buys Detected

2023-03-30 04:00:35 ET

Summary

- While executing my long-only strategy screening, I noticed 2 buy signals for HDSN and HHS - both buy-rated [by myself] stocks from 2 different industries.

- Both companies are fundamentally sound and technically oversold, in my view.

- By placing a stop-loss order of -15%, you'll see the backtested return for HHS will drop, but for HDSN it will increase. In both cases, you'd outperform the underlying.

- I recommend considering both HDSN and HHS for a medium-term swing buy.

Note: This article has been published on my Beyond the Wall Investing marketplace on Thursday, March 29th [7:24 AM].

Thesis

While executing my long-only strategy screening, I came across two promising buy signals for two different companies, Hudson Technologies, Inc. ( HDSN ) and Harte Hanks, Inc. ( HHS ), both of which are stocks that I personally rated as "buy" previously. Despite operating in distinct industries, both companies show significant potential for growth appreciation in the short run based on the technical setups detected.

The Strategy Description

I have been thinking for a long time about how to combine a trend-following strategy and a trend-reversal strategy in such a way that a) the win rate is high and b) the exit from positions is automated and does not turn out to be premature. All investors, of course, have their own preferences as to the risk they are willing to take. As you will see in the following description, the strategy I have developed does not provide for strict risk management and is more suitable for those who understand the underlying [the business of the analyzed stock] and focus on fundamental metrics in addition to the buy signal itself.

I should clarify what I mean by combining a trend-following strategy and a trend-reversal strategy because the very idea sounds contradictory - how can you combine 2 trading strategies that are opposite in spirit? When I talk about consolidation, I primarily mean the ability to catch a reversal [trend reversal] and then automatically follow the recovery growth by entering and exiting positions on drawdowns [trend following]. I chose the long-only approach because it is so easy to backtest.

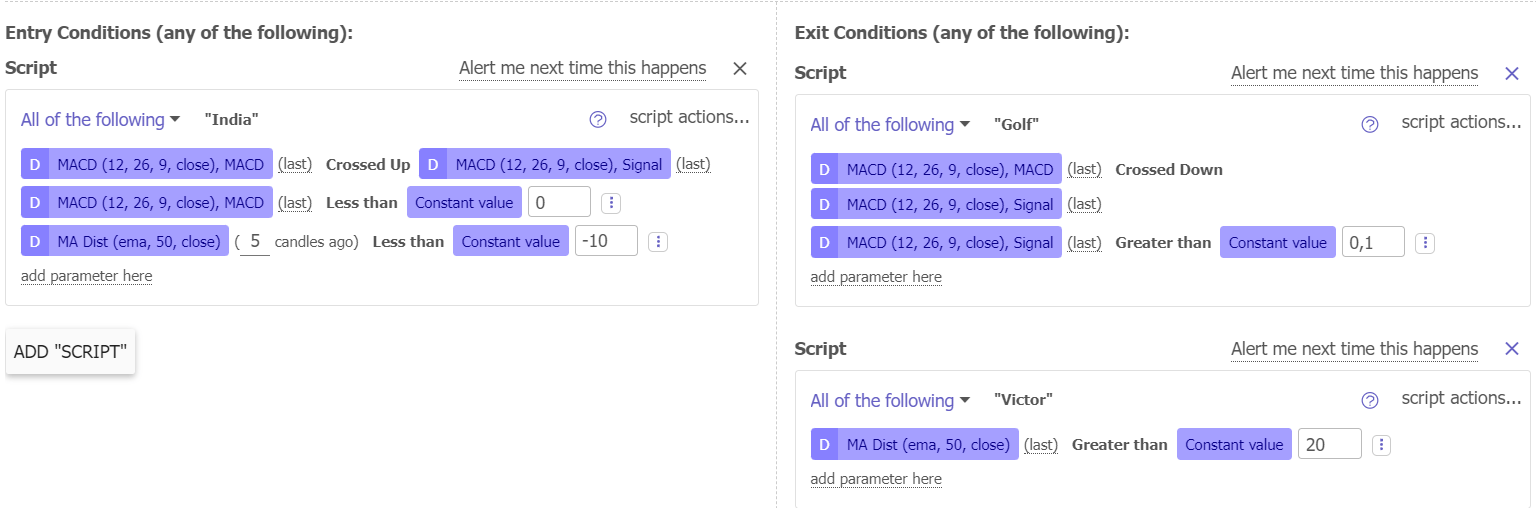

When searching for a reversal, I typically examine the MACD ( Moving Average Convergence Divergence ) indicator using the default settings [12, 26, 9]. Specifically, I look for the [blue] MACD line to cross above the [red] Signal line in negative territory (<0), which signals a potential buy opportunity. However, relying solely on this standard-setting may limit our ability to identify profitable trades, as many other traders are also using a similar thing. Therefore, it's important to explore alternative settings and customization options to increase our chances of success.

To increase the chance of detecting a true reversal, I think it is necessary to look at the amount of drawdown. To do this, I decided to focus on the distance of the moving average [MA Dist.] - enter a position only if the price was 10% below the moving average 5 days ago. That is, there was a drop below the MA [I use the 50-day EMA], indicating the recent dominance of sellers in the market; and against this background, the MACD begins to cross the signal line, indicating the return of the power of buyers. The potentially true reversal is thus confirmed. I use the EMA instead of the classic MA because of its faster speed - the price does not have to fall too low to get 10% below the EMA.

As exit settings I use 2 conditions, which can be executed independently in contrast to the entry settings:

- the intersection of the MACD line with the signal line from top to bottom in the upper part of the chart [> 0.1];

- price deviation of the stock 20% above the 50-day EMA.

Thus, I try to catch overheating and "jump out" of the position in time (as far as possible).

Here is what I got as entry/exit conditions:

TrendSpider Software, author's inputs

{kind=link}

As I wrote above, the stocks one selects must be of fundamental quality - you need to get away from simple technical indicators and conditions and dive into each individual company to gain fundamental insights. Well, let's start with that.

About Hudson Technologies Stock And Its Prospects

Hudson Technologies, Inc. is a refrigerant services company in the United States with a market capitalization of approximately $360 million. It offers innovative solutions to recurring problems in the refrigeration industry and has established a reputation for excellence in the market.

I have written about this company several times since late 2021 and have concluded each time that it is undervalued and has significant growth potential over the medium term (1-3 years). The fact is that the company is a leader in its niche with a 35% share and the industry itself is subject to heavy environmental regulation [a clear barrier to entry]. One of the most recent pieces of legislation in this area is the Aim Act, which mandates a phase-down of HFCs to combat climate change. By 2024, EPA mandates a 40% reduction in the supply of virgin refrigerants. This means that in less than 2 years we will be facing a significant HFC shortage, considering that HFCs make up 80% of the install base, writes Luca Socci in his latest great article on HDSN.

According to the latest EPA data on reclaimed ODS and HFC refrigerants, HFC recovery rates are still relatively low - which could indicate a supply shortage in the coming years. As the largest market representative, Hudson will likely be the first on the list to make up for this shortage. But the company already has excellent margins on both gross margin and EBITDA - demand for refrigerants is already there and will likely continue to grow for the foreseeable future, allowing the company to pass on rising costs to consumers and grow out of its low valuation.

The company is currently trading at ~3x its EBITDA and the market is pricing forwarding EV/EBITDA multiple at 4.582x, which is 56% below the Industrials sector median [based on Seeking Alpha Premium data ].

The key here is the question of refrigerant prices - how sustainable are they at their current, historically high levels? Management believes there are opportunities for higher prices, especially if people start to become aware or think more about what the shortage might be in 2024 when the 40 percent reduction and the virgin allowances start then.

Last year, the company more than halved its debt on the balance sheet [from $95 million at year-end 2021 to $47 million at year-end 2022] - interest payments should be lower going forward, leading to higher EPS numbers. This raises the question: How much do the prices for products sold have to fall for current EPS forecasts to come true? It seems to me that it's many times more than is possible - new earnings beats are very likely ahead, after which HDSN stock has historically flown hundreds of basis points higher in a matter of trading sessions.

Seeking Alpha, HDSN's Earnings Estimates, author's notes

{kind=link}

As for the valuation of the company, assuming only 4.2% revenue growth in FY2024, as forecasted by analysts, and assuming the EBITDA margin for the year falls to 27%, which I think is very pessimistic, the company should be worth $423.2 million at the targeted EV/EBITDA multiple of 5x - which is about 8.9% higher than it's worth to date . Given my conservative calculations, HDSN seems reasonably valued for a continuation of the stock rally - and Morningstar Premium's system agrees with me here, drawing an upside potential to the fair value of over +68.5%:

{kind=link}

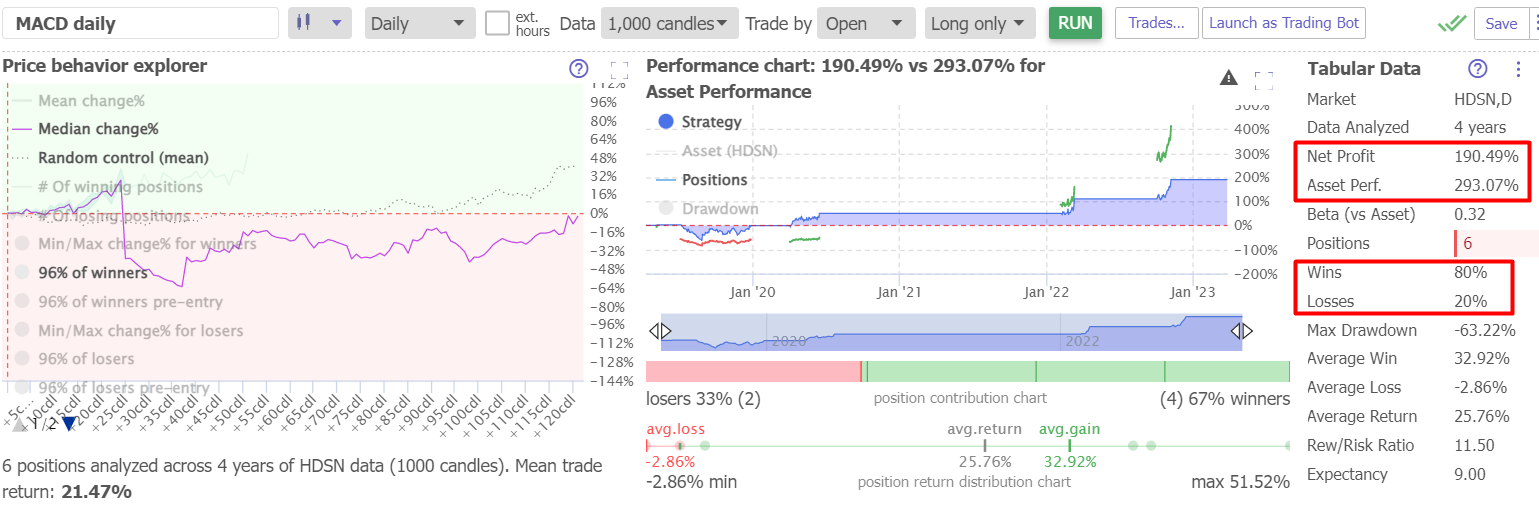

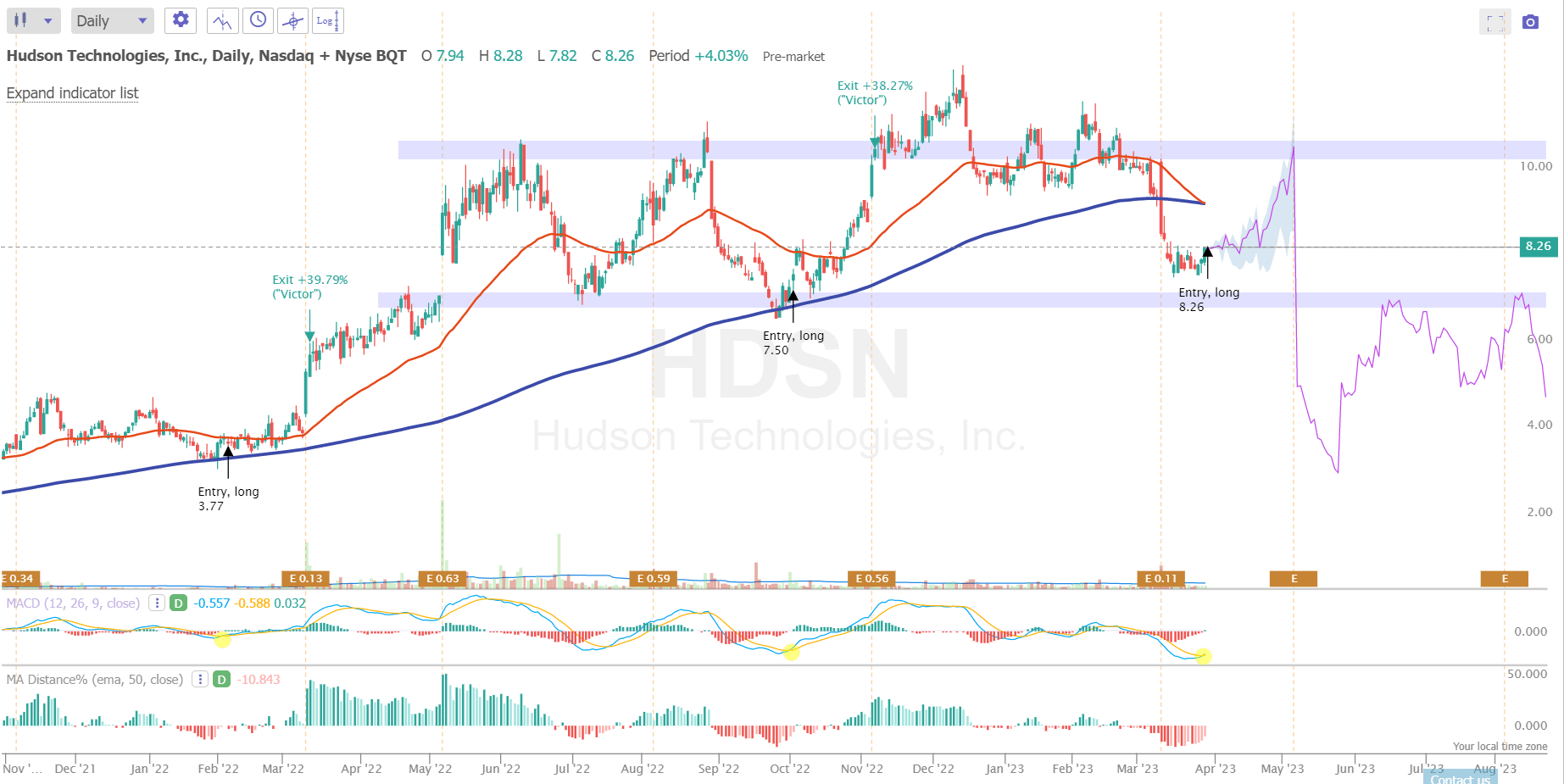

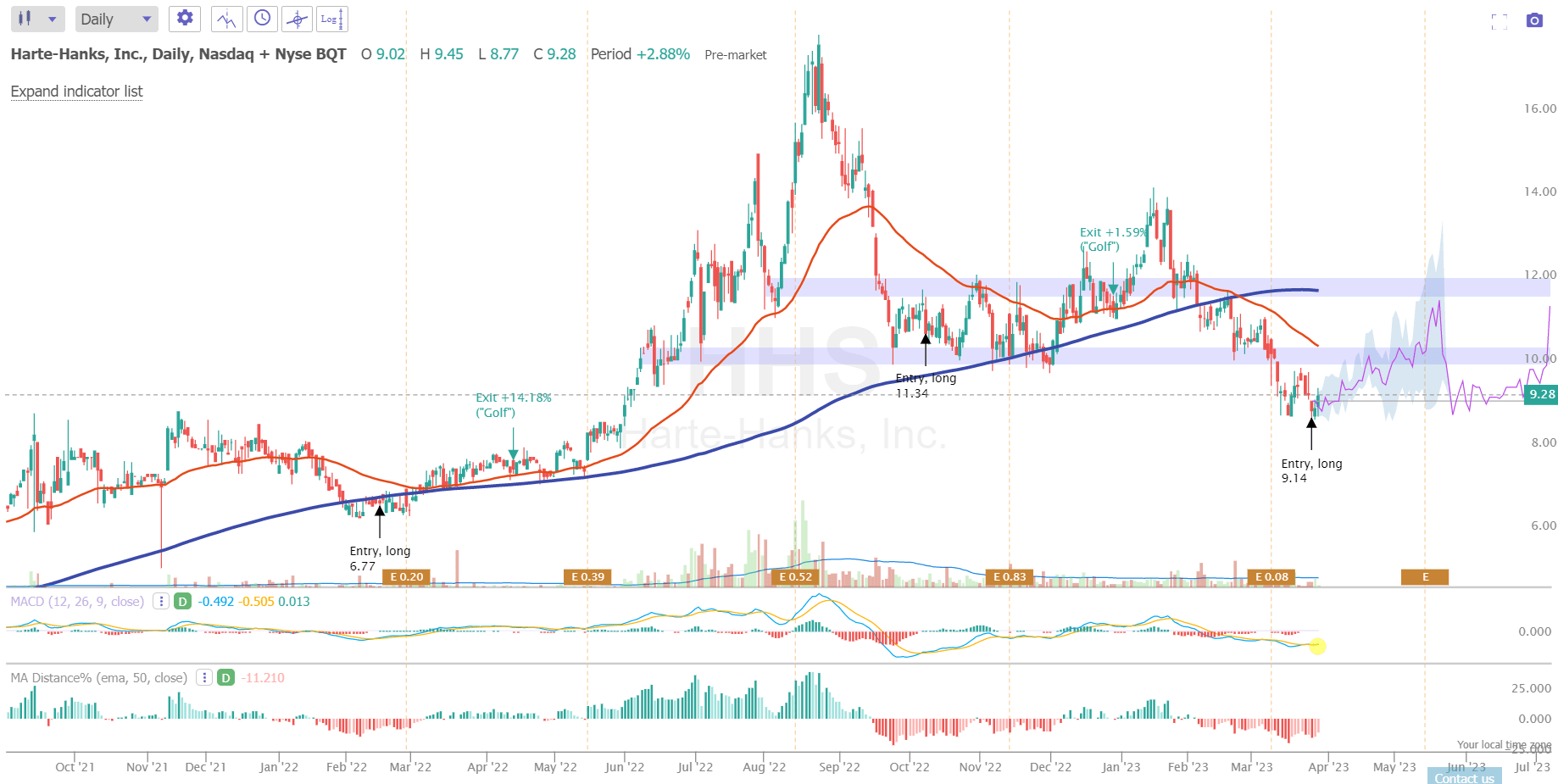

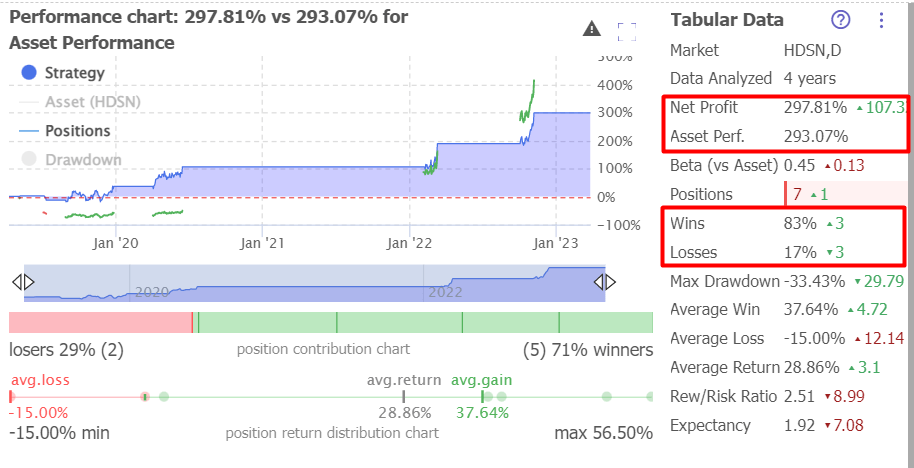

The results of backtesting the strategy described above may surprise you: There were 6 positions in the last 4 years with a mean trade of +21.47%:

TrendSpider Software, author's inputs

{kind=link}

Yes, there are not enough trades for a statistically significant conclusion. But what is striking is the high accuracy - the 80% win rate with a reward-to-risk ratio of 11.5, that's a lot. The total return would not allow us to beat the performance of HDSN itself, but it is the return per trade that counts for us, and it looks very good in this particular case. The last 2 buy recommendations are very similar to the current situation - the algorithm recommends buying now against a backdrop of active accumulation ahead of the early May 2023 report:

TrendSpider Software, author's inputs

{kind=link}

Therefore, I believe that HDSN could repeat its rise to $10 per share shortly before or a few days after the announcement of its quarterly results, which will probably exceed the Street's expectations for the 8th consecutive quarter.

About Harte Hanks Stock And Its Prospects

Harte Hanks, Inc. is a customer experience company that operates in marketing, customer care, and logistics business areas in the United States and internationally. With a market capitalization of just $64 million, the company has a diverse portfolio and a proven track record of delivering excellent customer service across various industries after it started to turn around its business operations back in 2018.

Like HDSN, I have covered Harte Hanks several times, but only since July 2022, when the stock was ranked by the Seeking Alpha Quant System as one of the best stocks at the time.

The company went through a period of decline, after which new management came in and gradually resolved all of the critical problems - most notably a heavy debt load.

As David Zanoni - another Seeking Alpha contributor - writes in his recent article , Harte Hanks has plenty of room for expansion in its home markets, which will continue to grow and develop in 2023 despite recession risks. For instance, the market growth projections are 14% annually for marketing and analytics software, 4.5% annually for customer care services, and 9.5% annually for e-commerce fulfillment, with the latter projected to reach $198.6 billion by 2030.

Even though the company operates in the field of communication services and 2023 is a challenging year for the entire advertising industry , management expects annual revenue and EBITDA growth in the high single digits, based on the recent earnings call transcript . The company experienced a total top-line growth of 5.4% for the final quarter of 2022 [and 6% for the full year], with the Fulfillment & Logistics segment contributing significantly to the quarter's growth due to a large logistics client. Despite a revenue decline of 12.9% YoY in the Customer Care segment, improved operating efficiency resulted in a 24.4% increase in EBITDA for the quarter. The strategic shift to an asset-light business model that Harte Hanks has been trying to master over the past few quarters is finally starting to pay off.

In December 2022, Harte Hanks acquired InsideOut Solutions for $7.5 million. InsideOut is known for helping large companies build and optimize inside sales initiatives, making the acquisition a strategic move for Harte Hanks to better serve its clients and enhance their sales and marketing programs, potentially driving their growth in the future. The transaction proved to be immediately accretive pulling down the valuation multiples, which also play a very important role in this whole story.

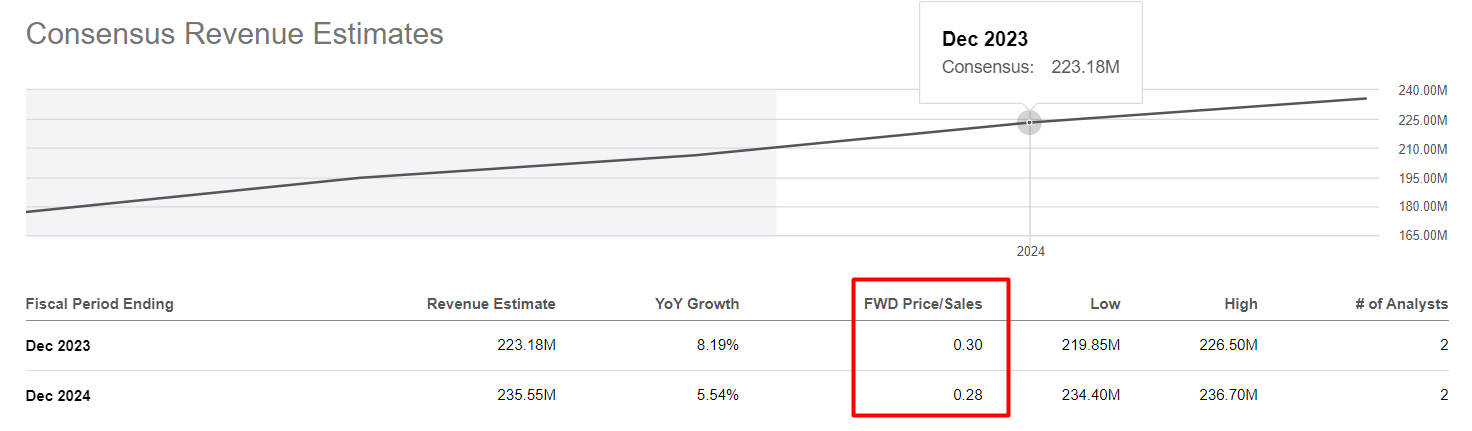

At the time of this writing the stock is valued at 0.28x of the forwarding [FY2024] price-to-sales ratio, which is extremely low compared to the sector 's median figure of 1.19x.

Seeking Alpha, HHS's Earnings Estimates, author's notes

{kind=link}

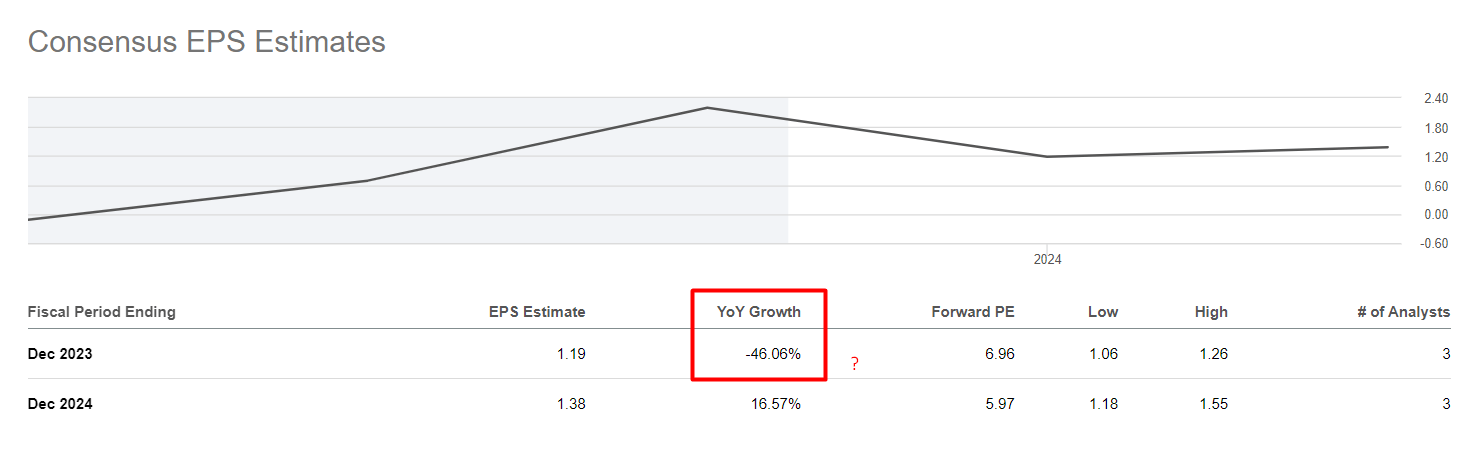

And at the same time, 2 analysts predict HHS's EPS figure to drop over 66% this year [YoY] and grow slightly over 12% in FY2024:

Seeking Alpha, HHS's Earnings Estimates, author's notes

{kind=link}

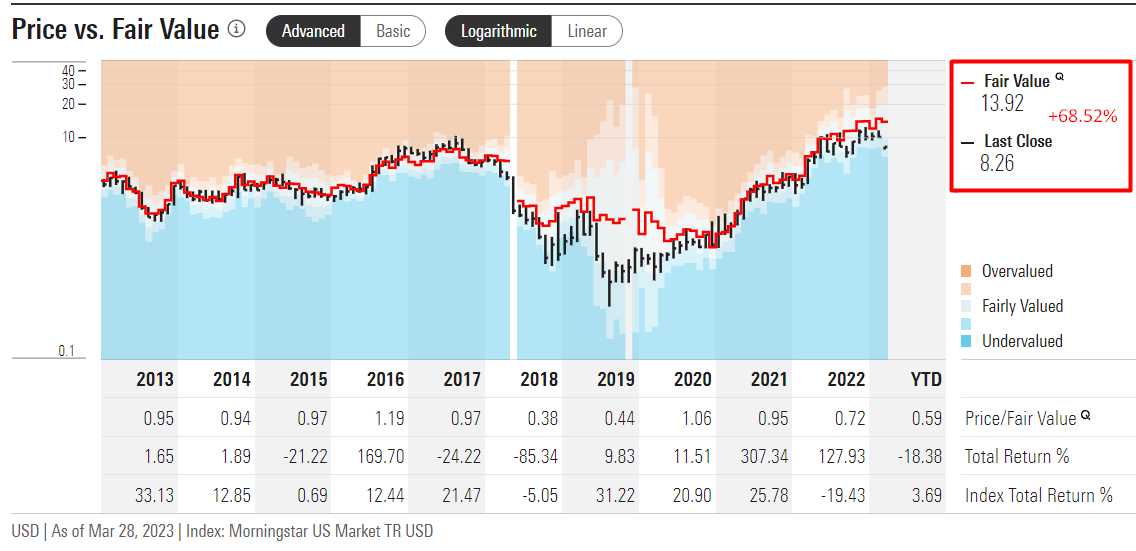

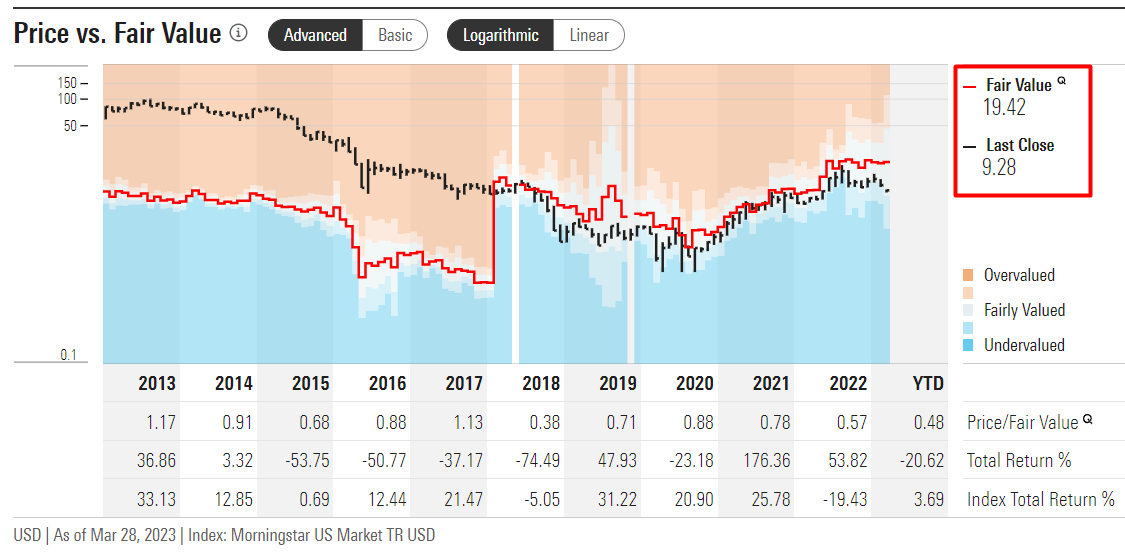

As you can see from the multiples, this is still very low. If the company beats these expectations even slightly, the implied P/E ratio should be so low that micro-cap value seekers could rush to buy the stock immediately. Morningstar Premium's system concurs with my undervaluation finding, showing a huge discrepancy between the fair value and the last close price of HHS stock:

{kind=link}

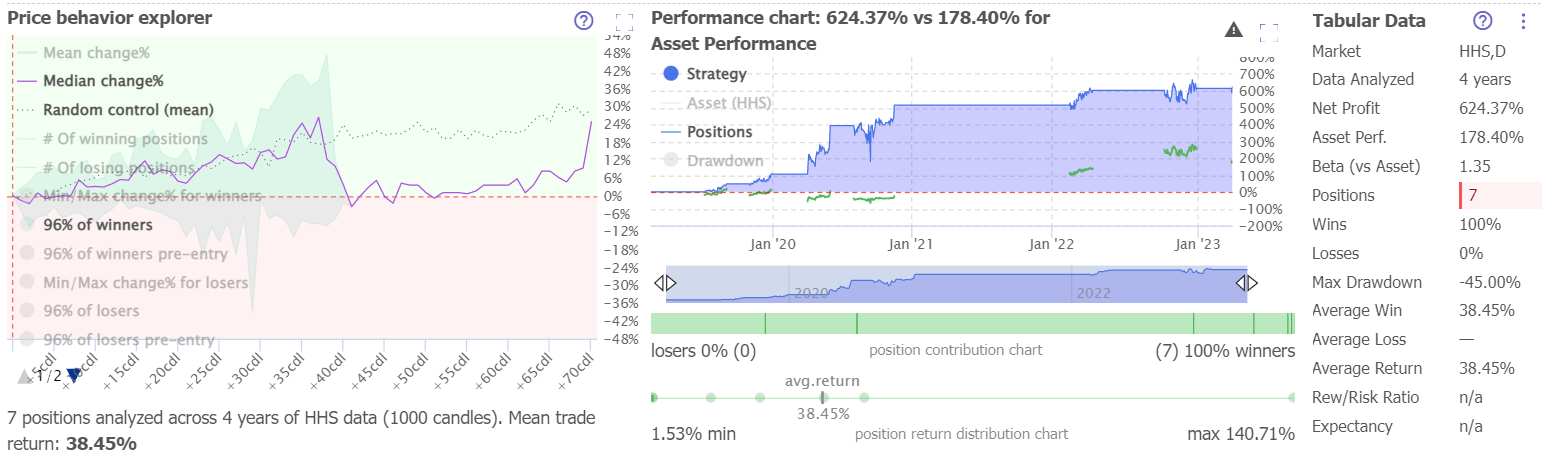

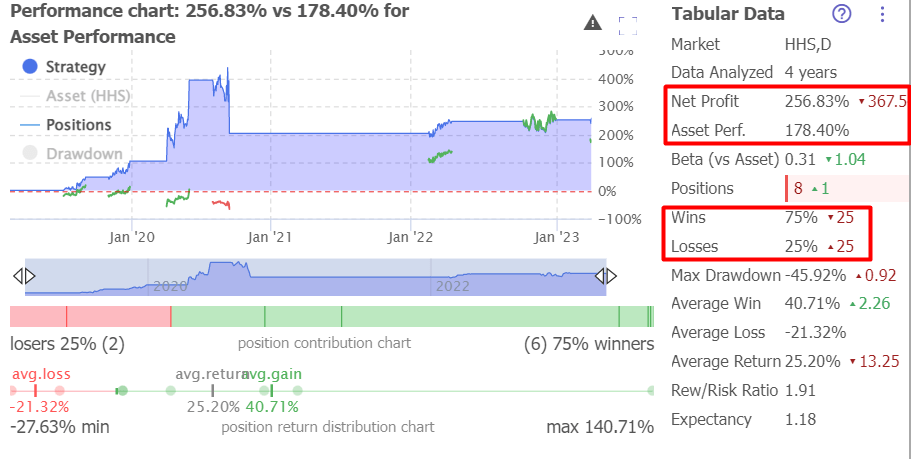

Now to my investment strategy: in the last 4 years, 7 transactions were made with an average return of 38.58%. HHS has grown significantly in those 4 years - by 178.4%. But the strategy would return the potential investor 624.37%, without a single negative trade:

TrendSpider Software, author's inputs

{kind=link}

A few days ago, the system issued another buy recommendation - since then, the price of HHS has not moved, which gives all investors with low-risk-aversion time to load up the truck.

TrendSpider Software, author's inputs

{kind=link}

Bottom Line

The main risk of the entire thesis is the peculiarity of the presented trading system, which is the lack of a stop loss.

Taking HDSN and HSS as an example, we see that despite the very high [almost perfect] win rates, both stocks had large maximum drawdowns of -63.22% and -45%, respectively. That's quite a lot. However, if you want to minimize your drawdown, e.g. by placing a stop-loss order of -15%, the backtested return for HHS will drop significantly, but for HDSN it will actually increase - and in both cases, the investor would outperform the underlying:

TrendSpider Software, author's inputs TrendSpider Software, author's inputs

{kind=link}

{kind=link}

Although I like both companies in principle, I feel compelled to warn you that both will come under increasing selling pressure in the event of a recession in the U.S., which is likely to occur in some form this year.

Anyway, HDSN and HHS are both quite interesting swing ideas in my opinion - this is not just a conclusion drawn from a finger based on technical analysis. I have been watching these stocks for a long time and was surprised to see buy signals on both of them almost simultaneously [which are generally rare]. These events coincided perfectly with the behavior of the prices of these stocks - in both cases they fell quite sharply, but not to the point where it could be called a trend reversal [from bullish to bearish]. At the same time, their valuation multiples compressed significantly in recent months - both companies are quite undervalued by Mr. Market against the backdrop of their idiosyncratic prospects for the next few years.

Therefore, I recommend considering both HDSN and HHS as medium-term swing buys.

As always, your comments are welcome! Thanks for reading!

For further details see:

Hudson Technologies And Harte Hanks: 2 Swing Buys Detected