HDSN - Hudson Technologies: Certain As Refrigerators And Air Conditioning

2023-06-11 09:11:18 ET

Summary

- Hudson Technologies is a buy due to its low valuation, strong growth, industry leadership, and large total addressable market in the refrigerant wholesale and recycling industry.

- The company is poised to capitalize on the Aims Act, which aims to phase out harmful HFCs and spur new refrigeration technologies, benefiting Hudson's recycling business.

- Risks include a lack of a deep moat, potential further dilution of shares outstanding, and volatility in margins and earnings.

Thesis

Food is as old as mankind and the economics are thus very efficient. Refrigeration, however, is a relatively new technology when considering the full length of human existence and has become integral in the production, distribution, retail, and consumption of many kinds of temperature sensitive food. Hudson Technologies ( HDSN ) serves even more than the food industry. It serves the entire HVACR industry, including air conditioning, wholesaling what it claims is the largest selection of refrigerant in the U.S. and selling wraparound solutions, including its piece de resistance in refrigerant recycling. I rate Hudson technologies a buy, as this company meets all my criteria for an investment: a low valuation, strong growth, industry leadership, and a large total addressable market with the bonus of being ESG friendly.

Operations

Hudson technologies has several operations from which it earns revenue. I cover their wholesale refrigerant trading business, their refrigerant recycling business, as well as their other services.

Refrigerant Wholesale

The primary business of Hudson Technologies is the wholesale of refrigerants. As wholesaler, it makes the market between refrigerant manufacturers like DuPont ( DD ) and Honeywell ( HON ) and HVACR manufacturers and technicians who work with refrigerant on the products we know and use daily. A number of factors such the degree to which an environment needs to be cooled and the mechanics of the underlying cooling system dictate the relevant refrigerant product. As an industry leader, it is able to profitably carry the widest array of refrigerants from Freon, the classic brand of the The Chemours Company, and catch all term for the chemical compound that powers air conditioners by evaporating and liquifying itself again and again to remove energy from the oxygen around it, to refrigerants for unique cooling systems.

Refrigerant Recycling

At the core of Hudson's strategic advantage is refrigerant recycling. By recycling and reselling old refrigerants, they are taking revenue from legacy refrigerant manufacturers and further developing economical relationships with key players downstream on the refrigerant supply chain by buying back their old refrigerant and therefore crediting their new refrigerant purchase.

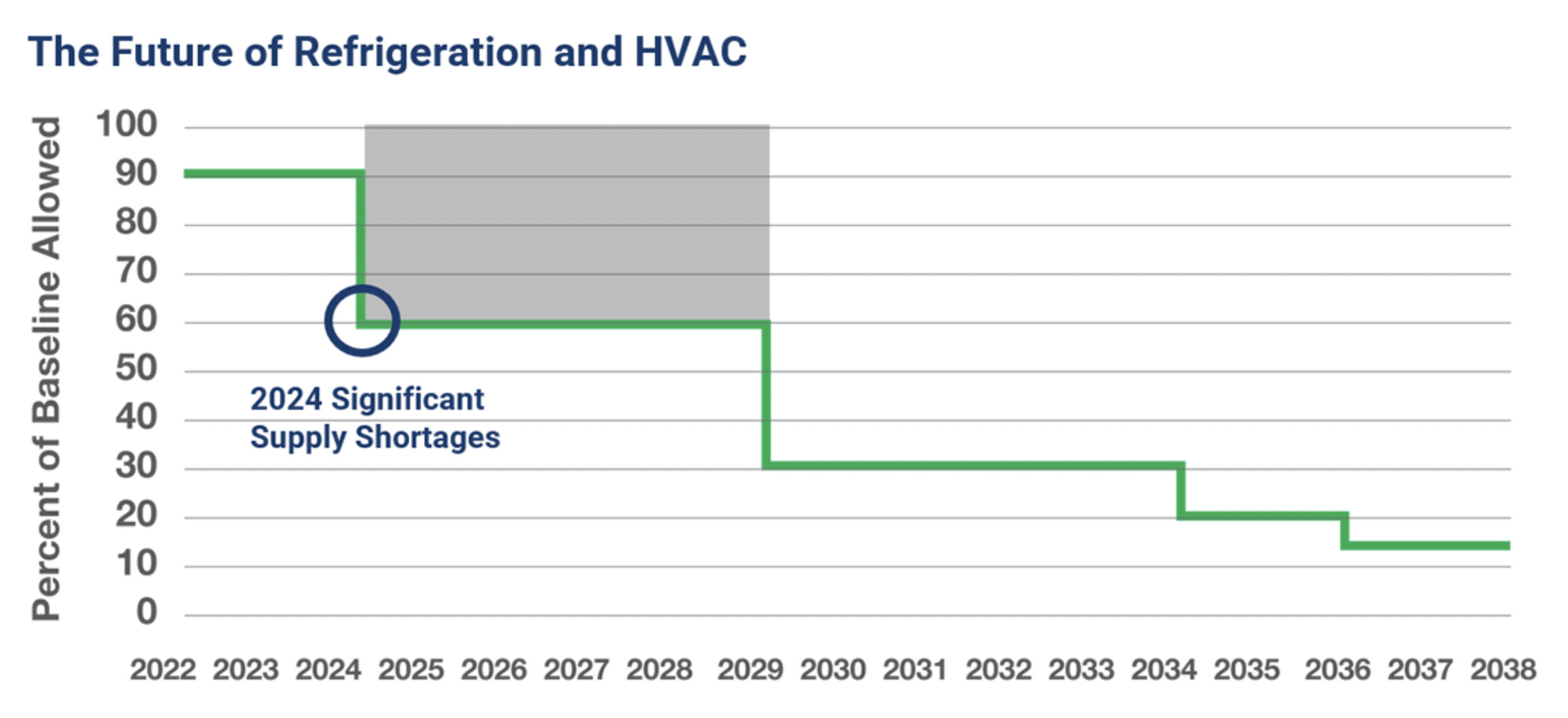

Passed in 2020 by Congress, a piece of legislation called the Aims Act empowers the Environmental Protection Agency to regulate a certain type of refrigerant called HFCs, or hydrofluorocarbons, which are an extremely potent greenhouse gas thousands of times more harmful than the carbon dioxide gas powered vehicles emit. These substances are released into the atmosphere when refrigerant is produced, when handled by consumers, and when refrigeration systems leak. The goal of the regulation is to phase out HFCs by decreasing the production each year, as shown below, and spur new technologies.

{kind=link}

The problem is that many legacy cooling and refrigeration systems still depend on HFCs. By recycling these HFCs, and offering other services to optimize their lifecycle in systems, Hudson Technologies stands to facilitate the transition to greener technologies. As an accomplished wholesaler experienced in selling a wide variety of refrigerants, the company is further poised to capitalize on the legislation as new refrigerants and new systems come onto the market. Hudson Technologies has invested millions in its recycling assets, having PP&E of $65.5 million. There are competitors in this space, some of whom include National Refrigerants, a competitor in wholesale operations as well, Airgas, A-Gas, and Chemours (CC), the only publicly traded competitor. Hudson Technologies, while it doesn't have a moat, is considered the industry leader in refrigerant recycling as the largest operator in the U.S.

Other Services

As a foot in the door to selling and recycling refrigerants, Hudson Technologies also cross sells refrigeration system maintenance services through On-Site R-Side. It is one of the only refrigerant recycling companies that will go to the customer, and it has patented technologies such as its ZugiBeast to streamline service to save time and money while increasing the longevity of the refrigerants in the system. They moreover help prevent leaks that are financially costly and harmful to the environment. From the company description, "It also offers SmartEnergy OPS service, a web-based real time continuous monitoring service for facility's refrigeration systems and other energy systems; and Chiller Chemistry and Chill Smart services." From the company website, "ChillSMART® includes both Chiller Chemistry® and Performance Evaluation in one unique package. This state-of-the-art evaluation is based on chiller operating data plus a fluid (refrigerant, oil and water) chemical analysis. Together, this approach optimizes your packaged chiller systems and keeps your units operating efficiently."

Financials

Hudson Technologies has grown revenue at a three year CAGR of around 31%. Its margins are equally excellent. TTM, Gross profit margin is 46.34%, EBITDA margin is 38.25%, and net income margin is 28.22%. Over the years, margins have been quite volatile, with profit margin ranging from lower than -30% during the pandemic to recent highs over the current levels. This volatility is somewhat concerning, as investors should look for stable margins. However, margins have been climbing up in recent years, despite a dip in the most recent report and stand to benefit from the Aims Act.

The chart below shows PP&E plotted with cash and equivalents, debt, and inventory. In 2017, Hudson Technologies borrowed in excess of $150 million in part to finance an expansion of PP&E for its refrigerant recycling facilities and in part to build up inventories. It has since paid down that debt by selling off inventory and at the last report has just $43.23 million in debt, notably less than its gross PP&E. Inventories have risen while the debt has been paid down and the cash position is a bit low at $5.295 million, but it has grown since the pandemic and accounts receivable amount to $38.8 million. Inventory is currently worth $137 million. The leverage, although a bit excessive for the capital investments that actually took place, is secured by current assets and cash flow is not affected by debt service, as levered free cash flow margin is high at 13.67%.

Shares outstanding on a fully diluted basis have grown over the years, and there have been no stock buybacks despite strong cash flow and earnings. This is something that I don't love here, especially combined with a decent amount of long term debt. It's unclear why Hudson technologies is raising capital through equity offerings. It hasn't had short term debt since December of 2021, so it appears that rather than utilizing a credit facility, Hudson Technologies is selling stock to finance operations and taking advantage of recent rallies in share prices. That sort of opportunism is not a shareholder friendly mechanism of financing to say the least.

Valuation

Seeking Alpha Quant Gives Hudson Technologies a grade A valuation. It trades at or below the industrials sector median ratio for all but one measure, where it is slightly above the median. The Price/Earnings ratio is just 5.98 compared to a sector median of 16.78. Based on my analysis so far, I see no reason why this stock should be so far below the sector median ratio. In my opinion, it is at least the median company in terms of its business model, profitability, and outlook.

Given that Hudson Technologies is largely a refrigerant recycling company, I'm not sure that the relevant sector is industrials. The closest competitor, in my opinion, is Chemours, which is classified as a materials company. Chemours receives a C+ valuation grade from Seeking Alpha Quant due to a high Price/Book value. Materials companies have lower multiples overall, but even assuming that Hudson Technologies is a materials company, it still looks undervalued compared to the sector median.

Risks

The main risk I see here is that Hudson Technologies doesn't have a very deep moat. Any player can make the capital investments into refrigerant recycling that Hudson has made. They do however have a leadership position and strong existing relationships in the industry. They are one of the only refrigerant recyclers that goes on site to reclaim materials, and they are currently the largest operation in the U.S. Another competitive risk to their business model is that many smaller players, without access to recycling plants, get in front of the used refrigerant supply and flip the refrigerant, taking margin from the back-integrated companies like Hudson Technologies. Other risks include further dilution of the shares outstanding and volatility in margins and earnings. There is likely a seasonality component to earnings and margins volatility, as during the warmer months of the year in temperate climates there is naturally more demand for refrigerant. Other than these issues, I see Hudson Technologies as a solid investment.

Conclusions

Refrigeration and air conditioning are mainstays of modern society. There is a very large total addressable market, and the importance of refrigerant recycling is emphasized by the Aims Act. Hudson Technologies has a nice mix of business, trades at cheap multiples, and is highly profitable. In my opinion, the shareholders must demand that these profits be distributed in the form of a dividend or share buybacks, or at least go toward paying down debt. Revenue growth expectations are quite low, compared to the rate at which revenue has grown. Similarly, earnings are not forecast to grow much into 2023. Hudson Technologies historically almost always beats these expectations, so earnings rallies may be a bit unlikely, however share prices should appreciate to at least sector medians in the near term as investors discover this hidden gem. I reiterate that Hudson Technologies is a buy and look forward to reading your comments.

For further details see:

Hudson Technologies: Certain As Refrigerators And Air Conditioning