HDSN - Hudson Technologies Is Optimizing Operations For Long-Term Sustainability

2023-10-03 13:52:29 ET

Summary

- Hudson Technologies' short-term expectations have moderated, leading to a downgraded HOLD recommendation with a near-term price target of $13.90/share.

- The company is well-positioned for the future circular economy with its ability to produce and sell rehabilitated refrigerant as FDA regulations on virgin HFC use become stricter.

- Hudson experienced a decline in revenue and gross profit, but management is optimizing operations by deleveraging the balance sheet and improving inventory management.

This article is an update to a previously published article on Hudson Technologies ( HDSN ). HDSN has returned ~56% since my initial publication on Seeking Alpha. I have since made a few updates to my model and though the overarching thesis hasn’t changed, my short-term expectations have moderated. My recommendation at this time is downgraded to a HOLD with an updated near-term price target of $13.90/share given the slowdown in revenue growth and margin compression over the last two quarters. Though long-term I believe HDSN shares have the ability to become a $25 stock, I don’t believe this will take place until the FDA’s regulation to phase out virgin HFC takes place beginning in 2024, making Hudson’s rehabilitated HFC more heavily demanded.

Starting with the positive notes, Hudson is set up for the future circular economy. One of the best aspects of the firm that I found appealing is their ability to produce and sell rehabilitated refrigerant as regulation becomes more stringent on virgin HFC use. For example, management’s comments in their August q2’23 earnings call denotes that back in July 2023:

The EPA issued a final rule for allowances for the 2024 to ’28 period, mandating a 40% baseline reduction in the virgin HFC production and consumption allowances. As we previously discussed, we believe the current phasedown schedule represents a tremendous opportunity for our business as the supply of virgin HFCs becomes limited and our reclaimed refrigerants will be needed to meet the demand for the large installed base of more than 125 million HFC units.

This coincides with my original thesis in that as more virgin refrigerant usage is phased out, the opportunity for Hudson to sell their rehabilitated refrigerant at a premium becomes more prominent. Though regulation provides a cushion for the duration of 2023, the ramp-up periods through 2028 will provide Hudson the opportunity to upsell their rehabilitated refrigerant and take advantage of the supply/demand dispersion.

Financials

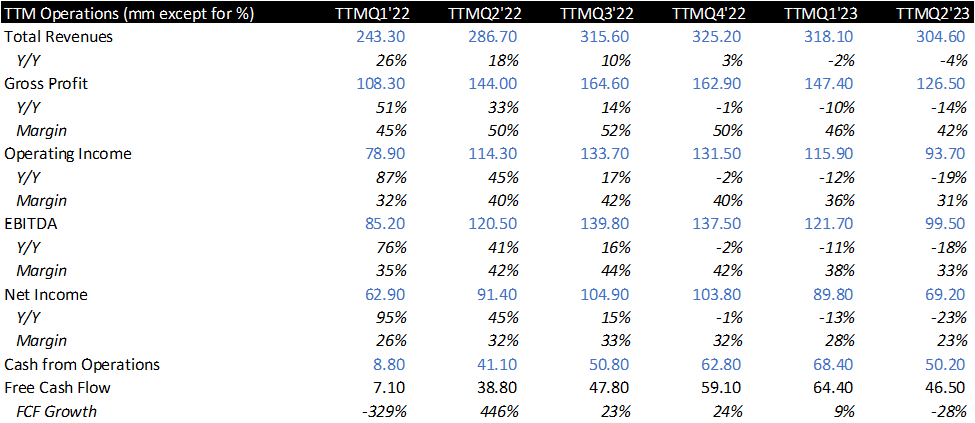

Hudson experienced a -4% decline in revenue on a TTM basis, or -13% when isolating q2’23. Though Hudson experienced two consecutive quarters of declining revenue generation, I don’t believe this is indicative of any stress on the company’s operations given the expected decline after a banner year. Gross profit also faced a significant decline of -14% using TTM figures for q2’23. Though this is a large jump, management has maintained a high profit margin of 42%.

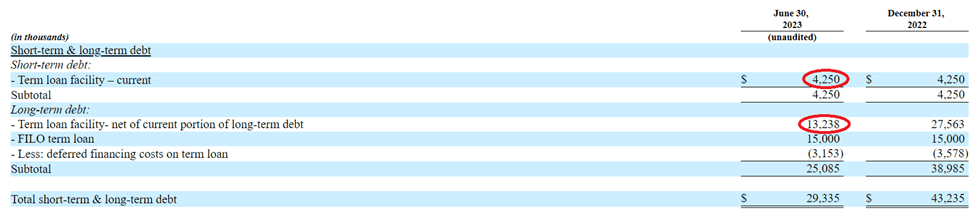

Management is continuing to optimize operations by deleveraging the balance sheet. Management extinguished $11mm alone in the second quarter of 2023 and more recently extinguished the remaining $17mm of the term loan with TCW Asset Management Company resulting in a debt load of ~$11.85mm for a debt/EBITDA multiple of 0.12x, granting management more flexibility to focus on generating cash.

{kind=link}

To add some perspective, the $17mm extinguishment resulted in a 60% decrease in their total debt load. Though free cash flow declined by 28% on a TTM Y/Y basis, management has the ability to cover the remaining debt load of $11.85mm with free cash flow alone. I believe this strength will be a huge asset for Hudson as the broader economy slows down.

{kind=link}

Considering the cash conversion lifecycle, management has reduced their days from 305 in the previous quarter to 298 days. Though this doesn’t appear to be significant, much of the reduction was a result of inventory management, a -6% decline in days inventory using TTM figures. This improvement in inventory management will allow management to potentially lower their carry costs of refrigerant and provide more flexibility to opportunistically purchase inventory at a lower cost.

{kind=link}

Valuation Update

Hudson’s valuation still remains in value territory at 9.5x trailing earnings. Though this next year won’t be a high-flying year following their outstanding FY22 performance, I believe management has taken the steps to set up Hudson for long-term success. This includes significantly deleveraging the balance sheet, focusing on their long-term goal relating to rehabilitated refrigerant, and optimizing cash flow as a self-financing entity. At this time I provide HDSN a HOLD rating with a price target of $13.90/share.

For further details see:

Hudson Technologies Is Optimizing Operations For Long-Term Sustainability