HDSN - Hudson Technologies Keeps Being One Of The Best Small-Cap Stock

2023-11-11 04:03:55 ET

Summary

- Hudson Technologies is a small-cap refrigerant services company with good operational growth prospects.

- The company faced challenges in Q3 2023 due to a challenging pricing environment and lower sales volume.

- Despite the challenges, Hudson Technologies remains well-positioned for the industry shift and has a strong long-term gross margin target.

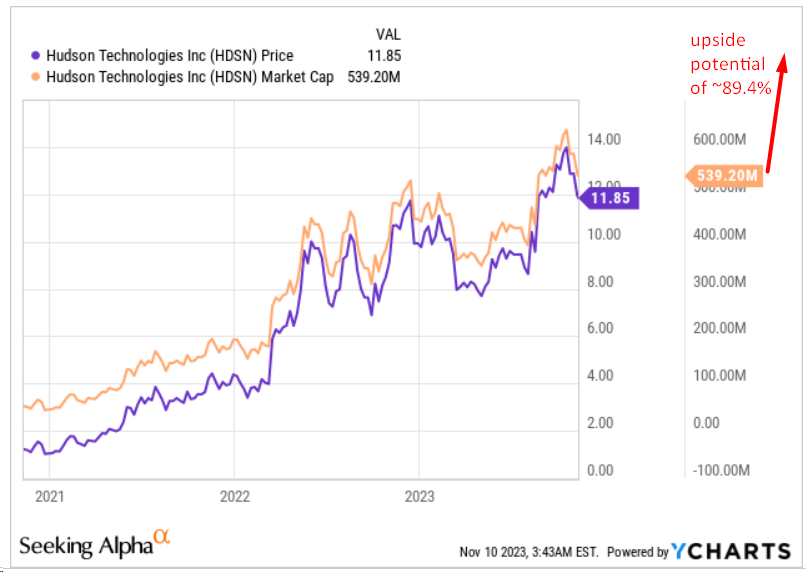

- My valuation calculations lead me to conclude that HDSN has an upside potential of ~89.4% in the medium term.

- Despite HDSN's increased multiple over the past year, the company remains comparatively more attractive than other industry players with higher leverage and weaker margins.

Introduction

I started covering Hudson Technologies ( HDSN ) stock in late 2021 when one share was trading at around $4. Since then, I've written about HDSN several times , and each time I've updated my thesis, I've come to similar conclusions that the company is undervalued and has good operational growth prospects. These calls were perhaps one of the most successful in my short career as an analyst.

{kind=link}

It's been more than six months since I last reported on the company, and in that time Hudson Technologies has managed to do a lot. How has my thesis changed? Let's figure it out together .

Financials And Prospects

Hudson Technologies is a $540-million refrigerant services company that provides solutions to recurring problems within the refrigeration industry primarily in the United States.

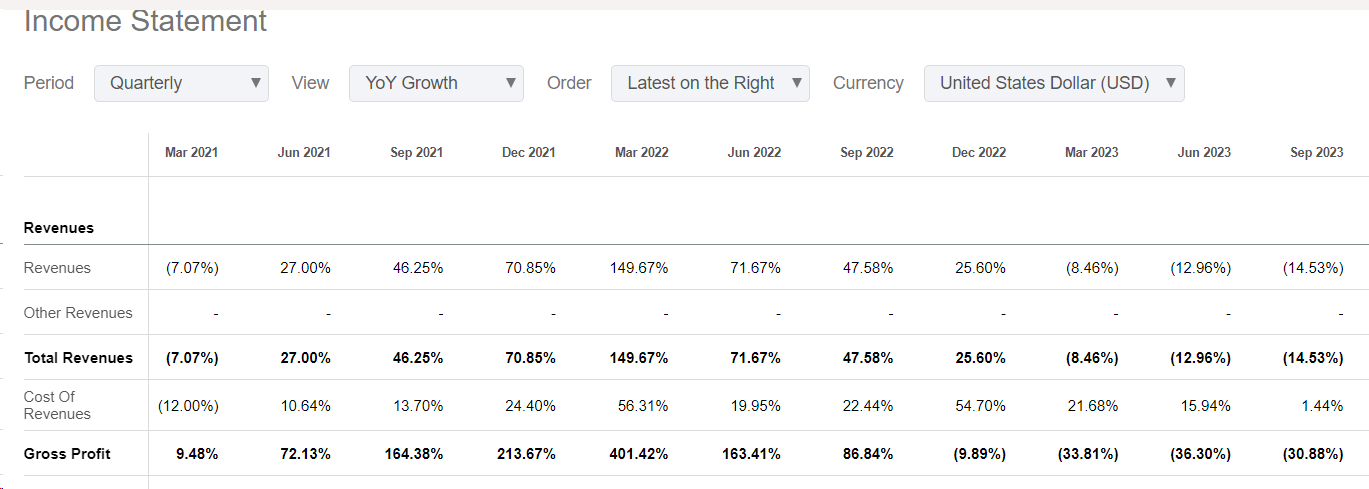

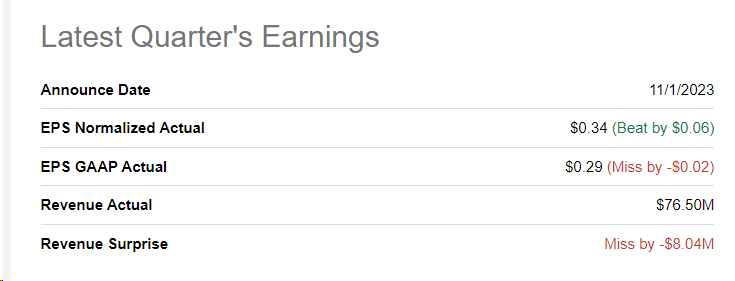

In Q3 2023 , HDSN recorded revenues of $76.5 million, a ~15% decrease compared to the same period in FY2022, primarily due to lower selling prices for certain refrigerants (-27% YoY). The gross margin was 40%, down from 49% in Q3 2022.

{kind=link}

The cooling season in 2023 faced a challenging pricing environment and lower sales volume, contributing to a 17% decline in the sale price of certain refrigerants over the nine-month period. However, HDSN achieved a gross margin of 40%, slightly higher than its long-term targeted gross margin levels, the management team noted during the recent earnings call. The company's gross margins were positively impacted by higher-margin carbon sales and the DLA contract. Excluding these contributions, gross margins would have been closer to 38%.

The company's operating income for Q3 2023 was $23.1 million, compared to $36.3 million in Q3 2022, and net income was $13.6 million or $0.30 per basic and $0.29 per diluted share, down from $29.4 million or $0.65 per basic and $0.62 per diluted share in Q3 2022. The company's results failed to beat consensus estimates for GAAP EPS and revenue, which is why the shares reacted post-earnings with a decline , which developed into a (not yet strong) correction.

{kind=link}

{kind=link}

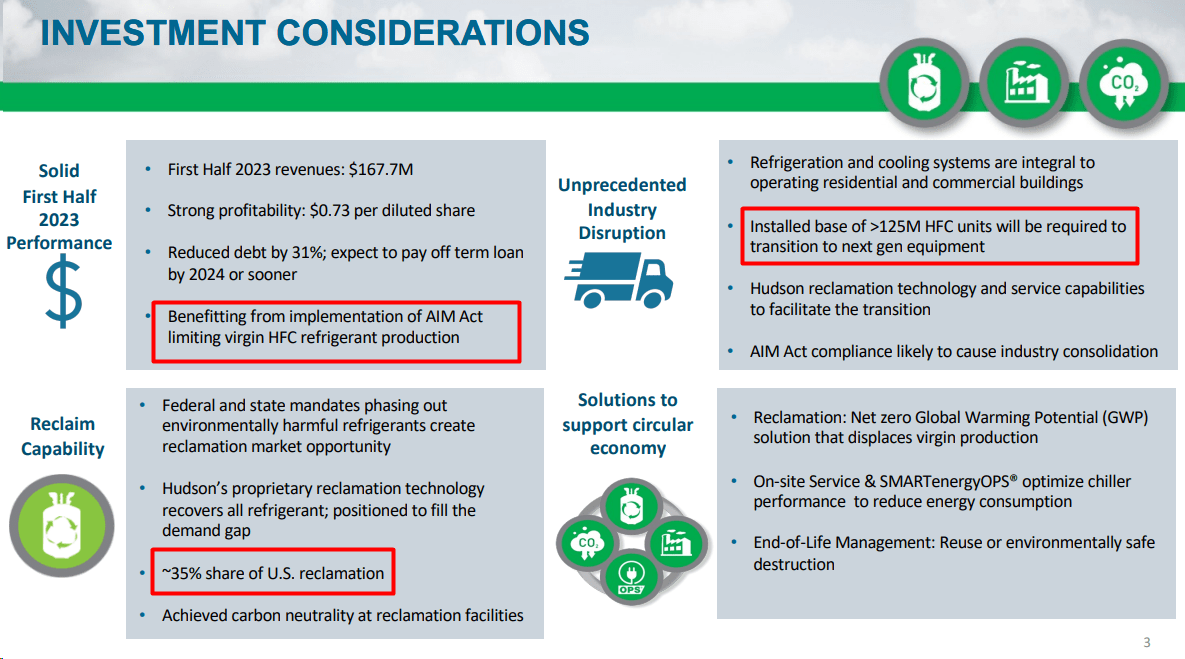

HDSN aggressively paid down its debt, culminating in the full repayment of its term loan ahead of the March 2027 maturity date. Today, HDSN's debt-to-equity ratio is almost zero thanks to the remaining minor liabilities on the balance sheet, which significantly reduces the company's credit risk.

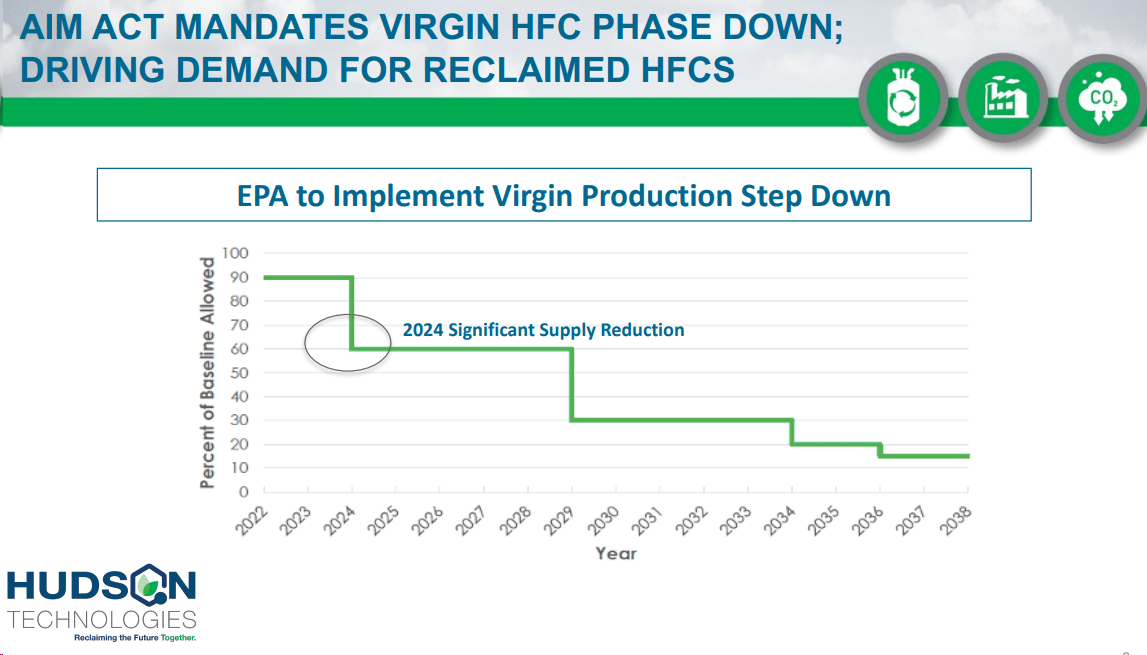

The company sees the upcoming 40% baseline reduction in virgin HFC production and consumption allowances as a significant opportunity for its business. Generally speaking, HDSN still looks to be well-positioned for the industry shift, emphasizing its proprietary reclamation technology and commitment to the circular economy for refrigerants.

{kind=link}

Despite the pricing challenges in recent quarters, the company is confident in its long-range gross margin target of 35%. Apparently, market conditions favor the company in achieving its goal. As another Seeking Alpha analyst, Blake Downer , noted in his recently published brilliant analysis , the global refrigerant market is projected to grow with a CAGR of 7.4% to 7.98% until 2030, and the refrigerant recycling market is expected to see a CAGR of 10.5% through 2028. Long-term trends indicate increasing demand in the HVACR industry due to shifts in the global equilibrium temperature. With a share of around 35% of the total market, I believe HDSN is well-positioned to curb the growing demand in the market.

Based on what the management said, HDSN remains focused on sustainable and responsible refrigerant management and anticipates an inflection point for the HFC market in 2024. The company sees its reclamation technology as a key asset in meeting the growing demand for environmentally friendly cooling and refrigeration solutions.

Looking at the results of past quarters, I am personally inclined to trust the management of HDSN: Their actions have truly turned the company around, which had certain problems with its debt back in 2019, and today, none of the past threats is a serious risk factor for the company. Another measure of the management's success is the shareholders' return since the turnaround. So when HDSN executives say they're betting on 2024, I believe them. In fact, a sharp drop in virgin production is planned for 2024 , which should boost the company's sales.

{kind=link}

And what about HDSN's valuation?

HDSN's Valuation And Wall Street's Expectations

When I last wrote about Hudson Technologies, the stock was trading at an EV/EBITDA of ~3x, making it very cheap. As HDSN has grown (+40% since my bullish call), valuation multiples have also risen:

But here it is very important to understand that the valuation of a stock does not take place in a vacuum: It takes into account the risks of investing in the company and the state of the market as a whole. 2023 was far from the best year for small caps, so it is unlikely that the increase in HDSN's EV/EBITDA can be explained by the market's move. Most likely it’s about deleveraging: the market remembered that the company had problems 4 years ago, and in 2023 the market was finally convinced that this is no longer a significant risk factor, so it started to give HDSN a higher multiple. At least that's how I see it.

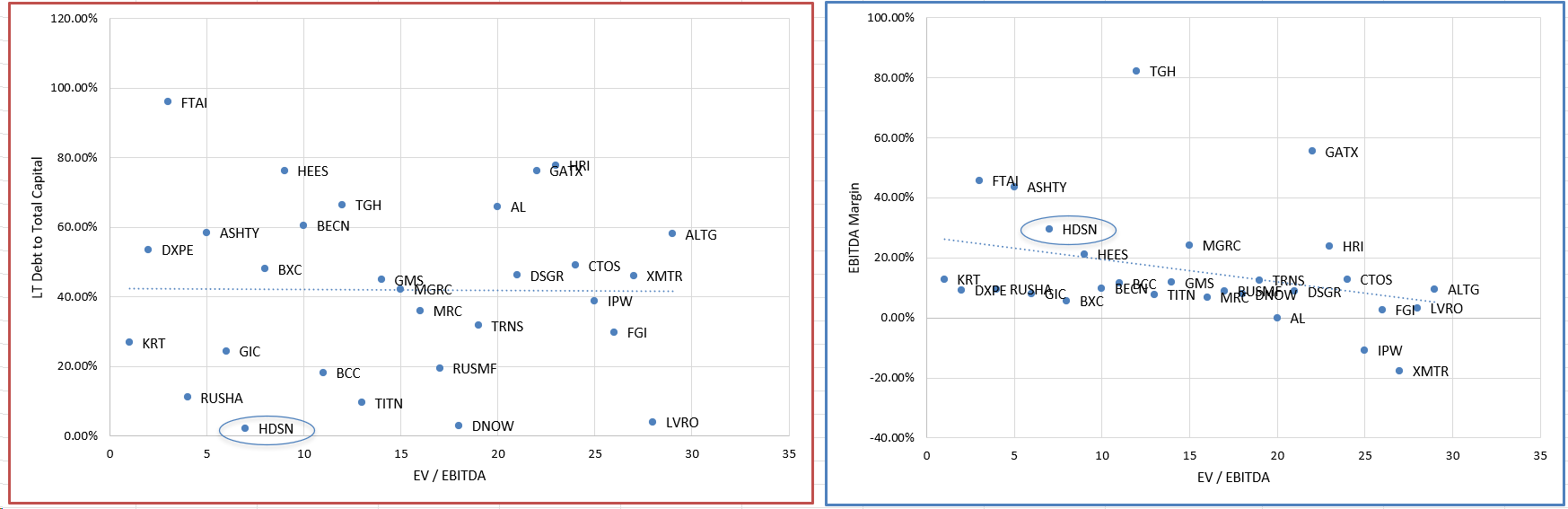

If I understand this correctly, then the fairness of the valuation of the company should be based on its marginality (compared to other companies). And here we have a problem because HDSN’s niche is quite specific and narrow. Think for yourself: A company with a capitalization of $560 million is a player in its industry with a 35% market share. But if we stay in the broader industry - Trading Companies and distributors - then HDSN is unbeatable with its current EV/EBITDA ratio given its debt and marginality levels:

{kind=link}

The company with its minimal debt burden trades at a discount of 29% to the broad industry median, while its EBITDA margin ((TTM)) is several times higher than the median value.

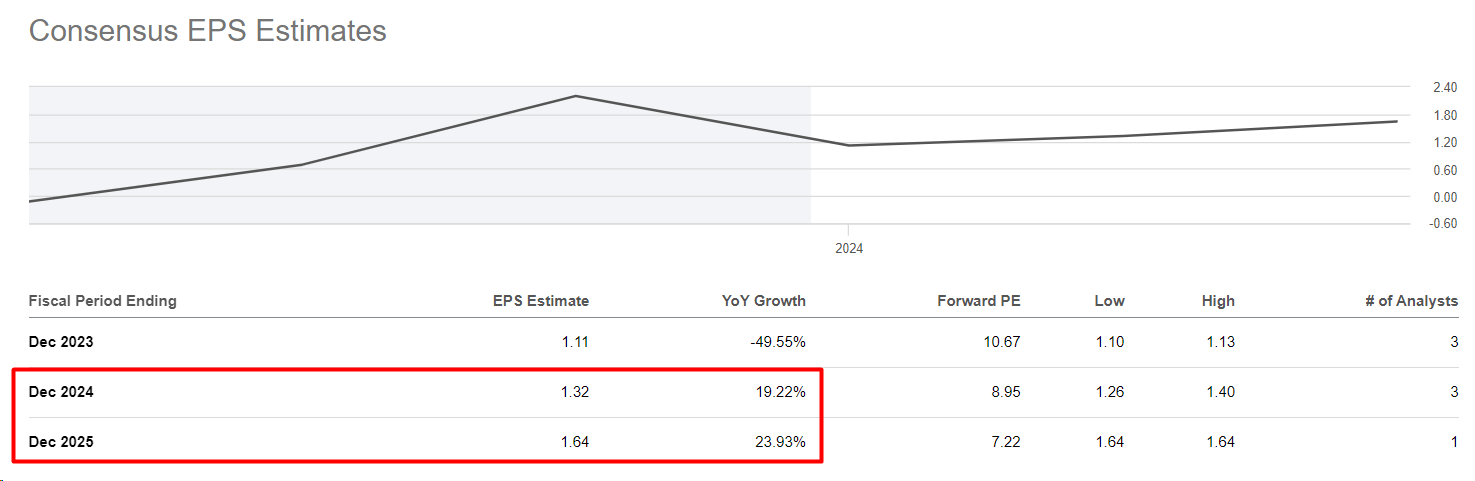

The market expects that we will see a recovery in the company's EPS again in 2024.

{kind=link}

Taking into account the consensus estimate for HDSN's FY2024 revenue of $321.7 million, an EBITDA margin of 40% (slightly lower than FY2022) results in a forecast EBITDA of ~$128.7 million. If the EV/EBITDA multiple rises to at least 8x, which seems a fair condition given the current post-deleveraging period, we get an enterprise value of ~$1.029 billion. Hudson's net debt is only $8.4 million, so the equity value of the company should be $1.021 billion, which is 89.4% higher than what I see on the screen today:

{kind=link}

The Bottom Line

As it always comes with investing in stocks, HDSN has plenty of different risk factors in the competitive claims management industry that should be taken into account. First off, the company faces the challenges of economic downturns impacting demand, regulatory changes affecting operations, and potential strain from catastrophic events leading to a surge in claims. Technology risks, integration challenges from historical acquisitions, dependence on a few major clients, and pricing pressure from cost-conscious insurers are additional concerns. The labor shortage in the industry and the potential for reputational damage further contribute to the risk profile. Specific to HDSN, its relatively small size, vulnerability to new entrants, and reliance on a limited set of products and services pose additional risks that investors should carefully consider before making investment decisions.

But despite the relatively high risk, the reward side of the equation seems much more attractive to me. Yes, HDSN's multiple has risen quite a bit over the past year, but still, the company has become even more attractive compared to other more leveraged and less marginal players in the industry.

Based on what I see today, HDSN is still a 'Buy' even at its current prices.

Thanks for reading!

For further details see:

Hudson Technologies Keeps Being One Of The Best Small-Cap Stock