HDSN - Hudson Technologies: Yet Another Tailwind As El Niño Kicks In

2023-07-03 12:26:07 ET

Summary

- The arrival of El Niño, a climate pattern that generally brings warmer weather, could benefit Hudson Technologies, a company whose demand for reclaimed refrigerants for air conditioning systems increases with rising temperatures.

- Despite weather-related risks, Hudson Technologies reported a good Q1 with a gross margin of 39%. The NOAA's prediction of a warmer than normal summer could further boost the company's performance.

- The Aim Act, which mandates a phased reduction of greenhouse gases used in coolants, refrigerators, and AC systems, is also expected to provide a tailwind for Hudson Technologies, a leader in refrigerant reclamation in the U.S.

Introduction

We have some significant news for a company such as Hudson Technologies ( HDSN ). We are entering into the warm phase of a well-known climate pattern. In other words, El Niño is here as all the conditions required to determine if it is present or not have been met.

Hudson Technologies is a company greatly affected by weather patterns. When temperatures rise, so does the demand for reclaimed refrigerants for air conditioning systems. When the weather is cooler, this demand is weaker and Hudson doesn't perform as well.

What El Niño is

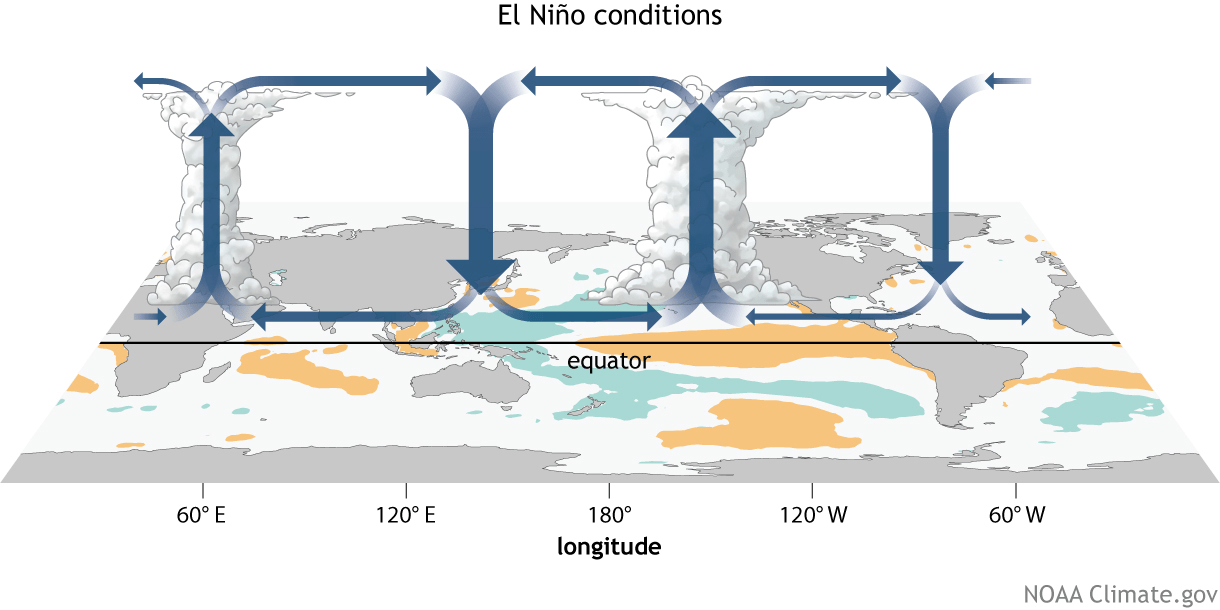

We can see El Niño explained through an info-graphic of the National Ocean and Atmospheric Administration (NOAA) which I share here with the caption the agency provides.

Generalized Walker Circulation (December-February) anomaly during El Niño events, overlaid on map of average sea surface temperature anomalies. Anomalous ocean warming in the central and eastern Pacific (orange) help to shift a rising branch of the Walker Circulation to east of 180°, while sinking branches shift to over the Maritime continent and northern South America. NOAA Climate.gov drawing by Fiona Martin. (NOAA Climate.gov)

{kind=link}

As the NOAA states,

During El Niño, the surface winds across the entire tropical Pacific are weaker than usual. Ocean temperatures in the central and eastern tropical Pacific Ocean are warmer than average, and rainfall is below average over Indonesia and above average over the central or eastern Pacific.

Rising air motion (which is linked to storms and rainfall) increases over the central or eastern Pacific, and surface pressure there tends to be lower than average. Meanwhile, an increase in sinking air motion over Indonesia leads to higher surface pressure and dryness.

But what exactly happens in North America during this phase?

Usually El Niño brings cooler and wetter weather to the southern states, while the Pacific Northwest experience drier weather. In particular, the winter season is warmer pretty much around the whole continent.

Now, what matters most is that the years when El Niño happens are usually years of records for warmth , even though overall during the summer cooler conditions may take place.

But what matters for Hudson investors is not summer temperature as much as when the usually cold season ends. In fact, in the summer a difference of a couple of Fahrenheit is not really what drives people to use their AC. Much more important is to understand when the cold season gives place to warmer temperatures which make people turn their heating systems off and turn their AC on. Therefore, El Niño could provide a strong catalyst for Hudson as it may be that hot temperatures will last longer than expected after summer is over.

Weather: Headwind or Tailwind?

One of the major risks with Hudson is the weather.

Now, we already know the results Hudson reported in Q1 when large portions of the U.S. faced a cold winter. Yet, Hudson reported a good quarter with gross margin still at 39%.

What matters most for us is to understand what could have happened in the second quarter. How has weather been in the U.S.? While April saw temperatures in line with the average, in May temperatures around most of the country were above average , especially in the Central Plains and the West.

{kind=link}

In many states the average temperature was already above 70° F which means ACs are on.

The three-month outlook given by the NOAA for this summer shows a for most of the country a 33% or greater likelihood of a warmer than normal summer.

Lastly, if past data can tell us something about heat cycles, according to the U.S. Environmental Protection Agency , in the past 10 years, the peak in refrigerant reclaimed pounds was reached exactly in 2016, when El Niño drove temperatures up.

The Aim Act: Tailwind No Matter What

There is also a tailwind that can't be easily wiped out: the AIM Act.

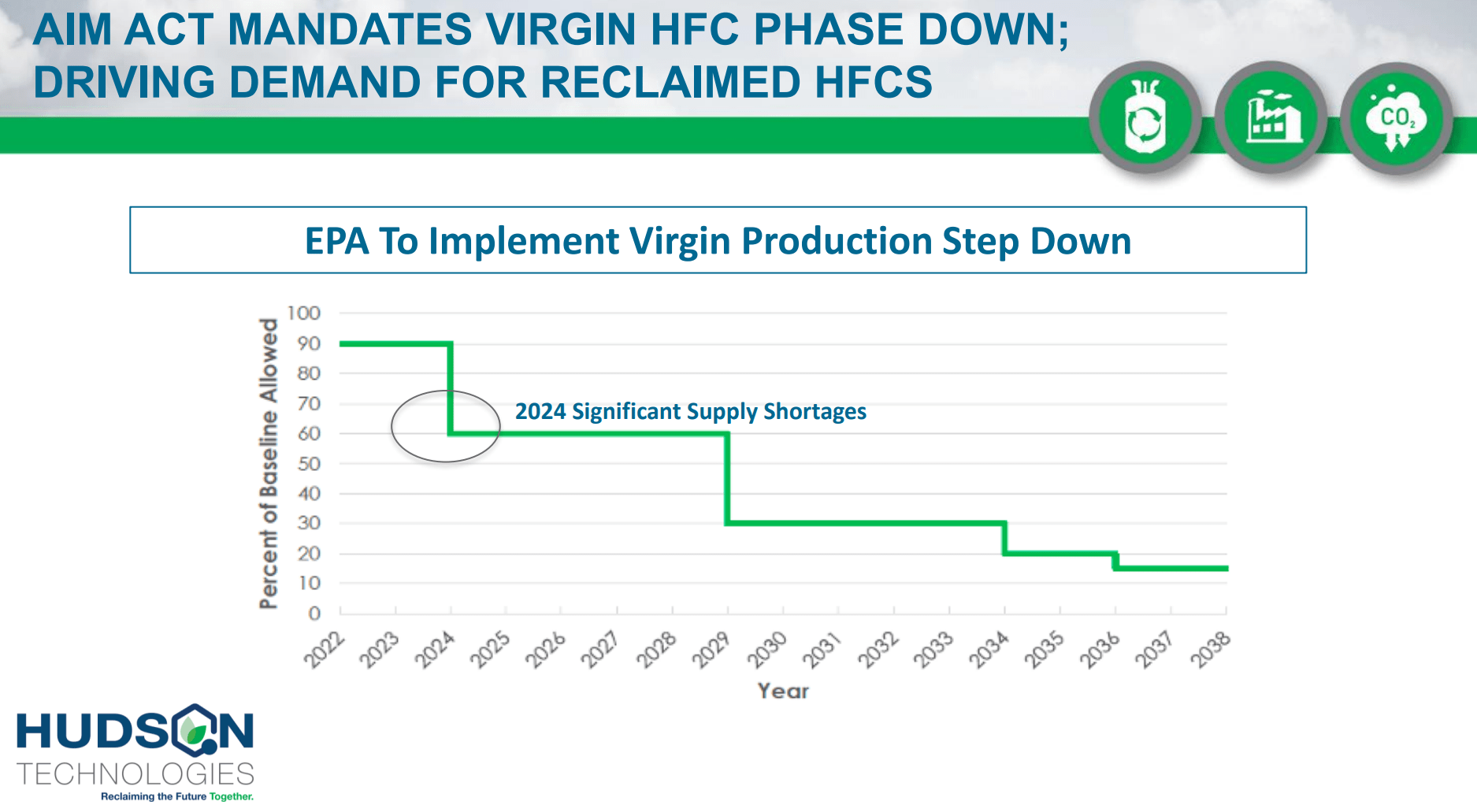

This law asks for an 85% phasedown of the production and consumption of HFCs by 2035. In fact, these are greenhouse gases used in coolants, refrigerators and AC systems. At the beginning of 2024, the law will require a 40% reduction of virgin HFC use. Right now, we are in the first step which is requiring a 10% reduction compared to the baseline.

Hudson 2023 Investor Presentation

{kind=link}

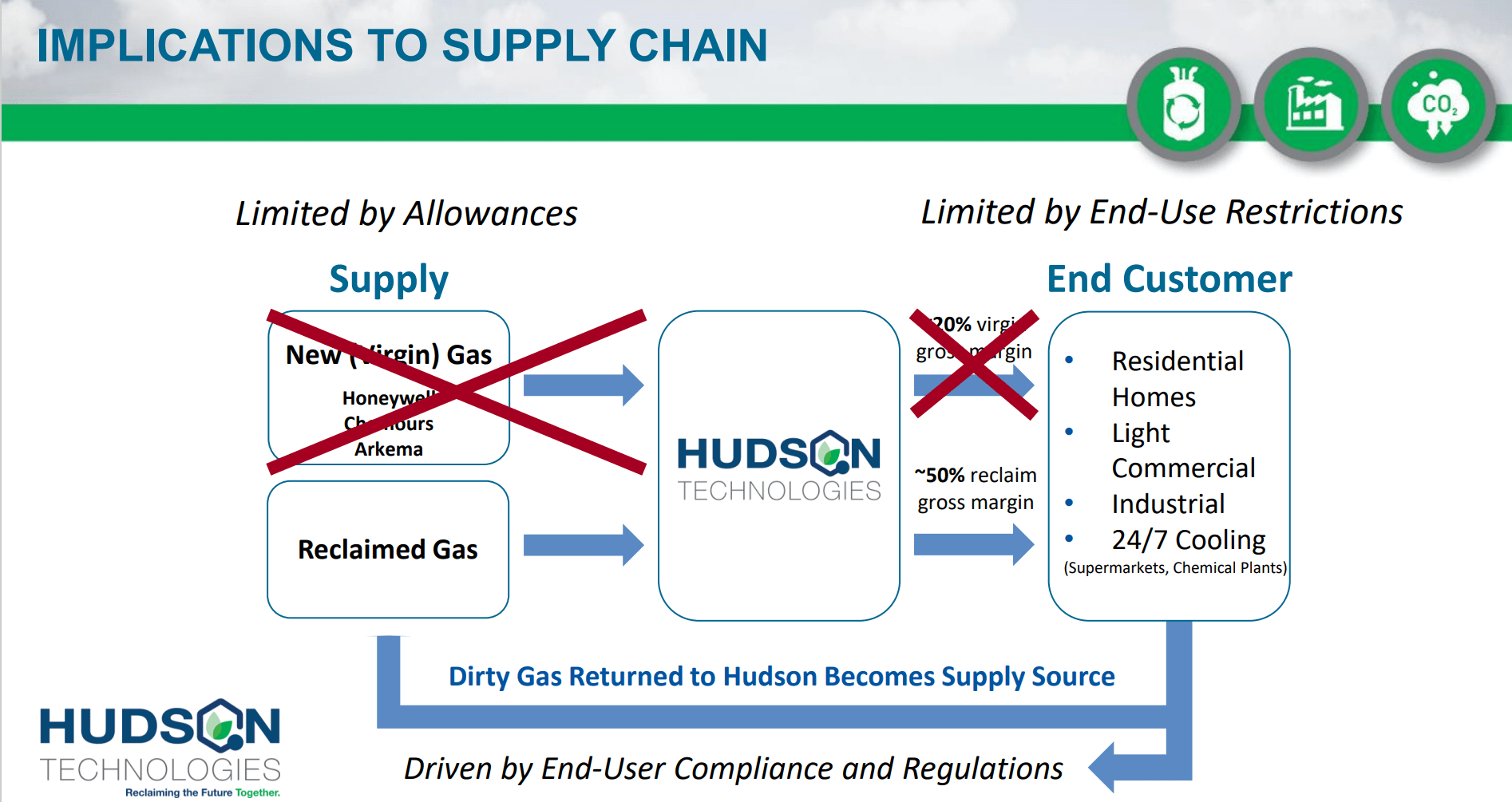

I believe this is a sure tailwind for Hudson, since the company is a leader in the U.S. in refrigerant reclamation. It has the necessary know-how to reclaim old refrigerants and sell them once again to an estimated install base of more than 125 million HFC units. Currently, Hudson holds a 35% share of the U.S. reclamation market. In particular, the spot Hudson holds in the supply chain is crucial. With virgin refrigerants being phased down, Hudson plays a unique role in making sure dirty gas is reclaimed and sold back to the end-customer still needing HFCs for its needs.

Hudson 2023 Investor Presentation

{kind=link}

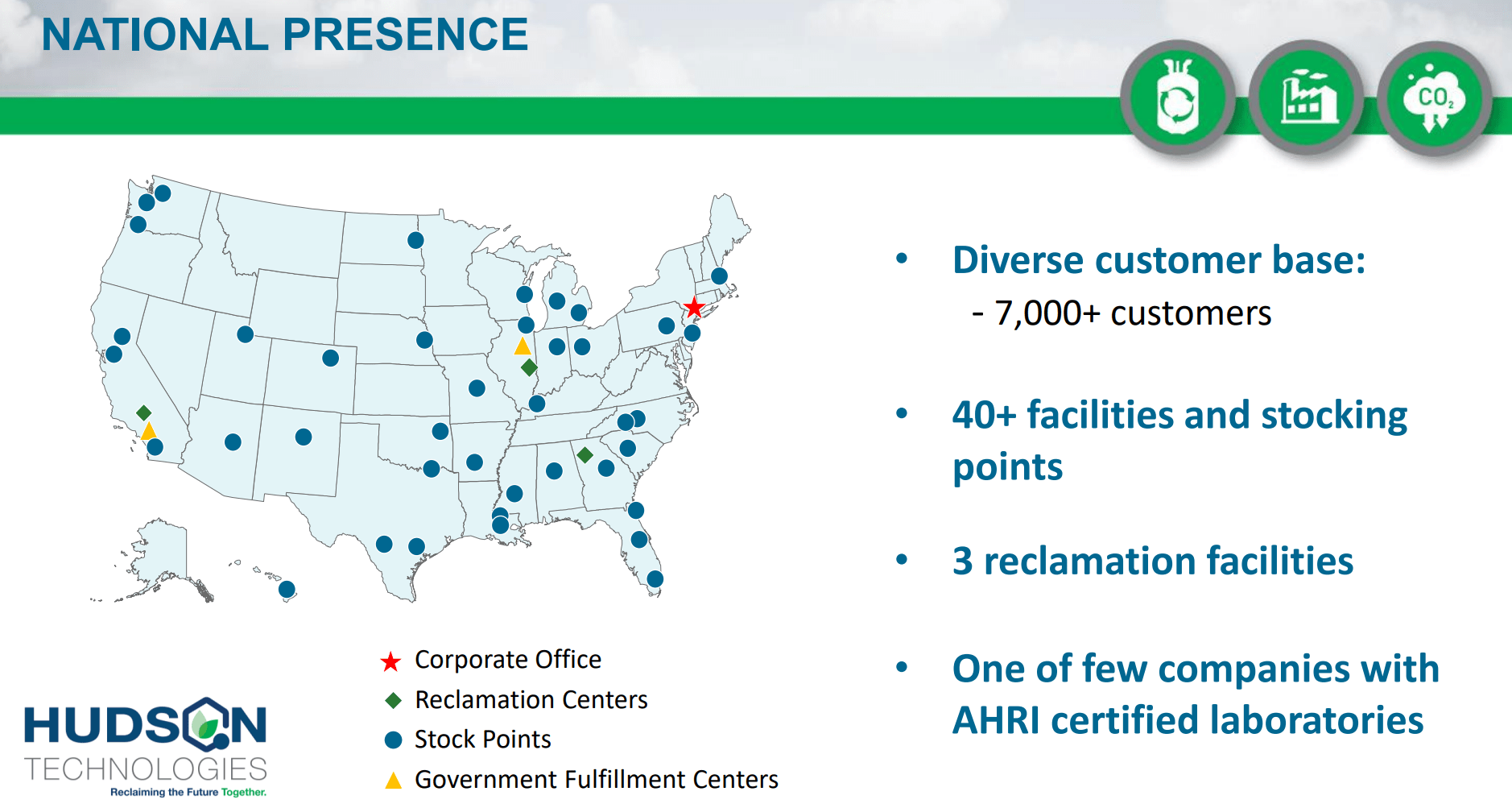

Moreover, Hudson has built in the past three decades a unique infrastructure supporting its activities. This creates a certain moat protecting its activities. In fact, it has 40+ stocking points around the country and its most densely-populated areas. Hudson owns three reclamation facilities and 2 AHRI certified laboratories out of the 4 the country currently has.

Hudson 2023 Investor Presentation

{kind=link}

In short, it seems like Hudson's story is already written as it heads towards success.

Risks: Virgin Refrigerant Flood and Inventory

As always, no investment comes without risk. Aside from unpredictable catastrophes such as wars, there are intrinsic risks in every business, and Hudson is no exception.

We have already seen how weather can be a variable. However, in a globally warming world, though a season or two may see cooler weather, Hudson is generally insulated from this issue.

However, the real issue has to do with inventory. In fact, if Hudson happens to carry reclaimed refrigerants in its inventory at a price that is above the current market price for them, then it can run into trouble as it is gradually forced to sell its refrigerants at a price lower than the price Hudson purchased the refrigerants to be reclaimed. This is exactly what happened in 2017, when a severe supply and demand imbalance almost threw Hudson out of business. Back then the market was flooded by Chinese suppliers' HFCs that needed to be discarded. This caused refrigerant prices to plunge, undercutting in price reclaimed refrigerants. It is not very difficult for this situation to replicate.

Still, this must make us cautious when considering how Hudson manages its inventory. In particular, we need to be aware of how FIFO and LIFO work (for those who are unfamiliar with the subject, I suggest reading this ).

Hudson uses the FIFO method, meaning it sells the oldest available item in its inventory first. FIFO has the advantage of reporting a better valuation of the current value of the inventory, as under this method we find on the balance sheet the cost of the most recent purchases which we assume to be closer to the current market value.

We know how in 2022 refrigerant prices, as well as many other commodities, skyrocketed. Since Hudson was carrying an inventory built before this price surge, we can easily understand why gross margins went higher too and reached 50%.

But now we need to forecast if the average refrigerant reclamation price will stay high or not. For sure, the AIM Act pushes toward this direction. Since Hudson uses FIFO, we can look at the current inventory level on the balance sheet and, assuming a similar quantity to be present, we can infer more or less where prices are going.

In Q1 2023, on Hudson's balance sheet, inventory went a bit down compared to the prior quarter. While it was $145 million at the end of December 2022, it is now $137 million. However, compared to the same quarter of the prior year, it went up since in Q1 2022 it was $101 million. This means that during the year refrigerant prices increased but that in the last few months they came down a bit.

Finally, during the last earnings call, Hudson reported R22 prices are still strong at more than $30/lb, while prices for HFCs are in the $10/lb range, down from the peaks seen in 2022.

Hudson's Balance Sheet is Strengthening

Since in 2017 Hudson risked going bankrupt, the company seems now very careful with its balance sheet. In fact, it is taking advantage of the current situation to deploy a lot of its free cash flow to aggressively pay down its debt. Last year, for example, the company generated $59.2 million in FCF (out of a $325.2 million revenue) and reduced its debt by $48.1 million. This is why the company reduced its debt by 56% brining it down to only $43.6 million at the end of Q1. We can be sure to see this number come down again when Hudson releases its Q2 report in my view.

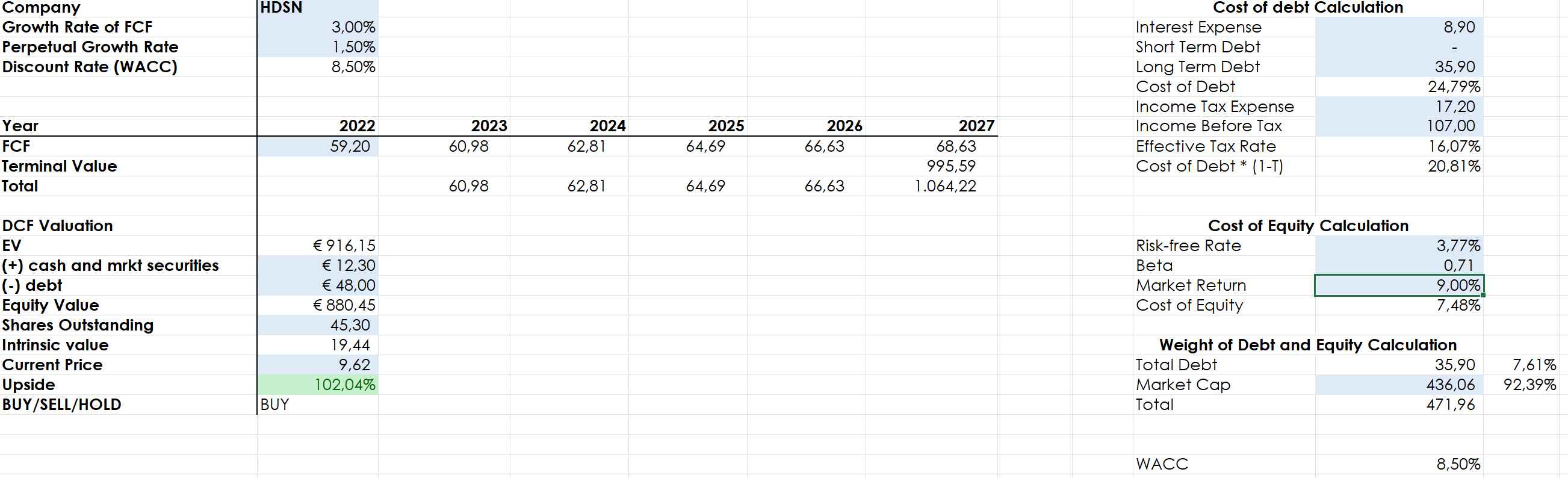

Hudson Valuation

I would like to share my discounted cash flow model for Hudson. Even though I am being quite conservative, assuming a FCF of only 3% per year for 5 years and then a perpetual FCF growth rate of 1.5%.

{kind=link}

The numbers don't leave much room for any kind of objection: Hudson is undervalued and, as long as it achieves minimum growth, still presents itself at a very interesting entry point in terms of price.

Expecting revenues to reach $400 and gross margin to come down to 35% (which could make the net income down be around 22%), we are before a company trading a 2024 fwd P/sales barely above a 1, while from a fwd 2024 PE perspective the stock is trading at a 5. Now, considering the niche and the competitive advantage Hudson has, I believe the market still needs to award a certain premium to this stock.

Conclusion

I am long Hudson both because of the strong tailwinds it will benefit from and because of the way it is currently managed. I also believe its full potential still needs to be unleashed and that, until 2024, the company won't fall under many investors' radars. I rate it a buy, considering the 100% upside to be realistic.

For further details see:

Hudson Technologies: Yet Another Tailwind As El Niño Kicks In