BOSSY - Hugo Boss: Reiterate Buy Rating As Turnaround Situation Progresses Well

2023-11-24 07:29:58 ET

Summary

- BOSSY's turnaround situation is progressing positively, with the ability to raise prices and a strong order book indicating strong growth ahead.

- In 3Q23, BOSSY saw 15% organic sales growth and 10% growth on a reported basis, with growth across regions.

- The inventory situation is normalizing, and gross margin is expected to expand in 4Q23.

Summary

Readers may find my previous coverage via this link . My previous rating was a buy as I believed the Hugo Boss (BOSSY) turnaround situation was on track, and I was positive that 3Q23 was going to be a good quarter. I am reiterating my buy rating as the BOSSY turnaround situation has progressed positively. It has reached a stage where it is able to raise prices by low double digits, and the order book has grown strongly, both pointing to strong growth ahead.

Financials/Valuation

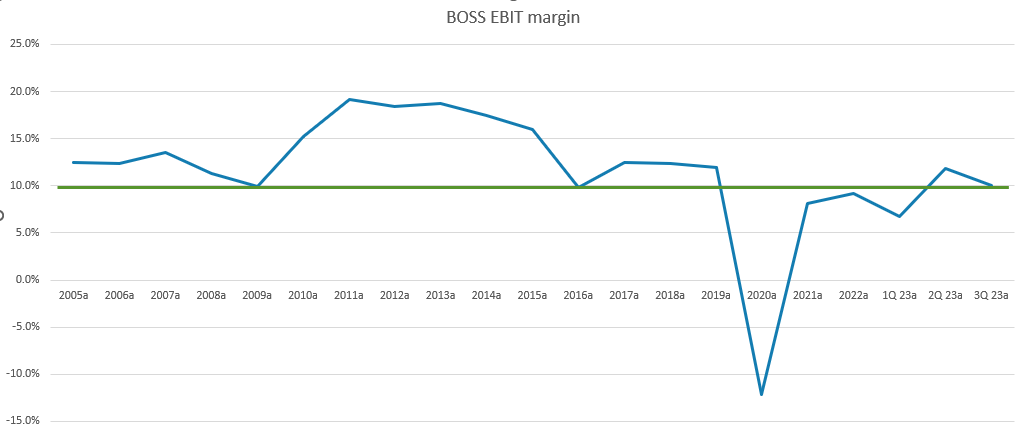

BOSSY saw 15% organic sales growth and 10% growth on a reported basis in 3Q23. By region, EMEA saw 12% growth, the Americas saw 22% growth (the US saw 20%, which suggests that growth was strong ex-US as well), and APAC saw 21% growth (China grew 17%). Gross margin was reported at 60.6% flat against 3Q22, and EBIT grew ~$11 million to $103.3 million at a 10.1% margin. On the balance sheet side of things, inventories grew 2% sequentially and 32% annually to EUR1.154 billion and ended the quarter with $93 million in cash and ~$1.2 billion in debt.

Based on author's own math

Based on my view of the business, BOSSY should grow 13.7% in FY23 (management guidance) and continue to see low-teen growth for FY24 and FY25. I did not make any changes to my growth assumption as the turnaround remains on track and I do not see any issues with BOSSY continuing the current low-teen growth momentum. However, I did adjust my FY23 earnings to $267 million as I believe BOSSY is able to achieve management FY23 EBIT guidance (based on the EBIT margin expansion, inventory issue stabilising, and pricing growth seen in 3Q23). I derived earnings using the BOSSY historical EBIT to net income conversion rate. Accordingly, I increased FY24 and FY25 assumptions by the same magnitude (10 bps). I also continue to believe that BOSS should trade back to its historical average as it continues to show progress in its turnaround, which so far has been going on really well. I re-note to readers that BOSS has historically grown at ~6% CAGR from FY05 to FY19. Now that growth has the potential to stay in the low teens for the near term and the EBIT margin to expand further, I think it deserves to trade at its historical average.

Based on author's own math

Comments

My previous upgrade to a buy rating appears to be too early. The stock fell after my upgrade to $55, which was a painful ride. However, on the positive end, I was right that 3Q23 is going to be positive, as the trend suggested back in 2Q23. True enough, BOSSY delivered a solid performance in 3Q23, and I expect growth to remain strong in the near term as BOSSY continues to see a solid order book. During the call, management expressed optimism about the progress made in the wholesale order book. In particular, order book increases remained robust in the Americas and Europe. From a quantitative standpoint, two other data points also give confidence that order demand remains healthy. Firstly, Hugo Blue, a new brand line, saw initial orders way above expectations. This tells me that management has made the right fix to its marketing strategy (I talked about it in my update ) and that the product suits BOSSY target consumers' preferences. Both elements are key to a successful product launch. Second, the solid 21% growth in the brick-and-mortar wholesale channel was highlighted by management. The more promising data lies within this 21%, where ¾ of that 21% growth was on a like-for-like basis. This again proves the point that BOSSY is launching products that suit consumers' preferences.

If you look at Q1, we make only a kind of qualitative statement, but I can assure you that the order books have been pretty strong across the board. I mean, Asia is more or less neglectable, but in Europe and in the Americas, we still have seen a very strong order book.

And if it comes to Hugo Blue, the first orders have been actually above our own expectations, so we are actually quite happy how the order books developed for the summer season. Source: 2Q23 earnings

Along with volume, I am optimistic about the trajectory of pricing growth. The 15% organic growth in 3Q23 was driven, in part, by volumes, according to management. When asked about the price increases during the call, management said that they were in the mid-single digits for this fall season, which, on top of the pricing growth seen in FY/W22, sums up to a total of low-double digit pricing growth. I believe the way BOSSY is able to increase prices (as much as low double digits) is an amazing indicator of BOSSY's product in the market and how it has positioned its product to show its price-value proposition.

If we come to the retail performance, I think it's worth mentioning that we have now two price increases as well in our books, and those price increases are helping us in terms of the average ticket that we are selling.

and regarding pricing, you're right. We did at the end, we did two price increases. One was for winter 2022, and another mid-single and now for fall. So we have a combined rate, which is like low double digits. This is where we are standing. I think, and this is why I always highlight this.

Besides that, we also further strengthened the 24-7 lifestyle images of Boss and Hugo while always putting strong emphasis on our superior price-value proposition. Source: 2Q23 earnings

Regarding inventories, I believe the situation has taken a further step in normalizing as the growth in inventory (32%) is a big step down from the 2Q23 53% growth and 1Q23 66% growth. Moving forward, the management anticipated a more noticeable gradual normalization of inventory as well. As such, I believe the path to achieving inventory as a percentage of sales below 20% by 2025 is plausible. Now that we are pretty sure that inventories are on a path to normalization, it should dismiss any concern that a high inventory stock count will pressure gross margins. In fact, gross margins have been pretty stable, and management anticipates gross margin expansion in 4Q23. Given the freight cost situation , reduced product cost, and pricing growth, I believe gross margin should expand as guided.

Returning to the topic of margins, I see the fact that EBIT margin stayed above 10% as encouraging, even though it did not grow sequentially. Productivity drove a 19bps improvement on a year-over-year basis for BOSSY, with revenue per square metre increasing 7% to EUR12.4k. You may remember that BOSSY is currently revamping its store concepts, with the goal of updating 40% of stores by 2023's end and approximately 80% by 2025's end. As such, I expect EBIT margin to continue to improve as these refreshed stores open and mature over time. An important point to note is that the 7% increase in store productivity is outpacing the 3% annual increase that is already part of the company's multi-year guidance. Which means there is chance that BOSSY will raise its guidance which could be a catalyst to driving the share price up.

{kind=link}

Risk & Conclusion

While BOSSY is not facing any inventory issue, this is not the same for the industry. Due to the high levels of inventory in the industry right now, management has warned that they may witness increased promotional activity from competitors during the end-of-year discounting periods. Since more budget-conscious shoppers may flock to these sale items, this might slow growth in the short term.

In conclusion, BOSSY turnaround is progressing really well, which made me reiterate my buy rating. Growth ahead should remain positive, supported by pricing growth and order book visibility. Additionally, the inventory situation has proven not to weigh on gross margin, giving comfort that EBIT margin will not be impacted.

For further details see:

Hugo Boss: Reiterate Buy Rating As Turnaround Situation Progresses Well