SWGNF - Hugo Boss: Wait For Further Price Correction

2023-11-23 23:35:32 ET

Summary

- Hugo Boss' performance continues to be strong, with its ongoing five-year investment programme paying off in both revenue growth and margin expansion.

- Strikingly, BOSSY has reported double-digit sales growth across geographies in contrast with other luxury brands, but in line with the affordable luxury segment.

- Its market multiples look improved since the past few months too, though they still aren't low enough to be competitive.

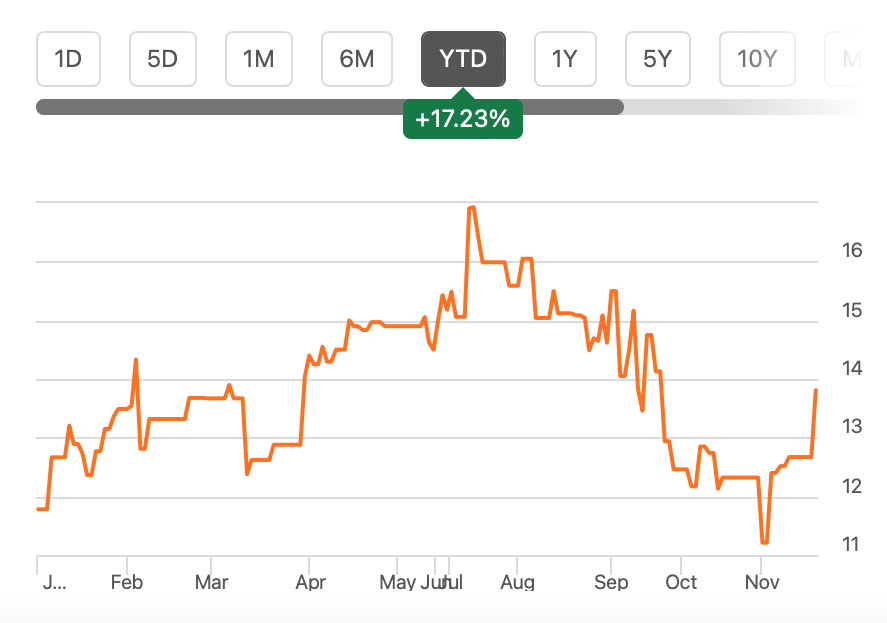

Since I last wrote about the fashion and accessories brand Hugo Boss (BOSSY) in early May, its price has declined by almost 7%. The article was titled "Good Performance, High P/E", so it comes as no surprise that the price declined since, though it's still up year-to-date [YTD].

Price Chart (Source: Seeking Alpha)

{kind=link}

Yet, at the time, I had gone with a Hold rating going on good top-line growth and the medium-term prospects from its ongoing investment programme , a five-year programme that aims to drive growth and profits. The programme has already contributed to improved EBIT margins and they are expected to see further improvement in the next years.

With a price decline in the past six months, however, its forward price-to-earnings (P/E) ratio looks far more attractive, which is discussed in greater detail later on here. The question now is as follows. Has the P/E declined enough to make Hugo Boss a Buy now? Or have there been developments in the interim that justify the price fall?

The latest results

The key development for the company is the results for the nine months of 2023 (9M 2023) released earlier this month, which aren't bad at all. Let's look at them in detail.

Sales growth is still good

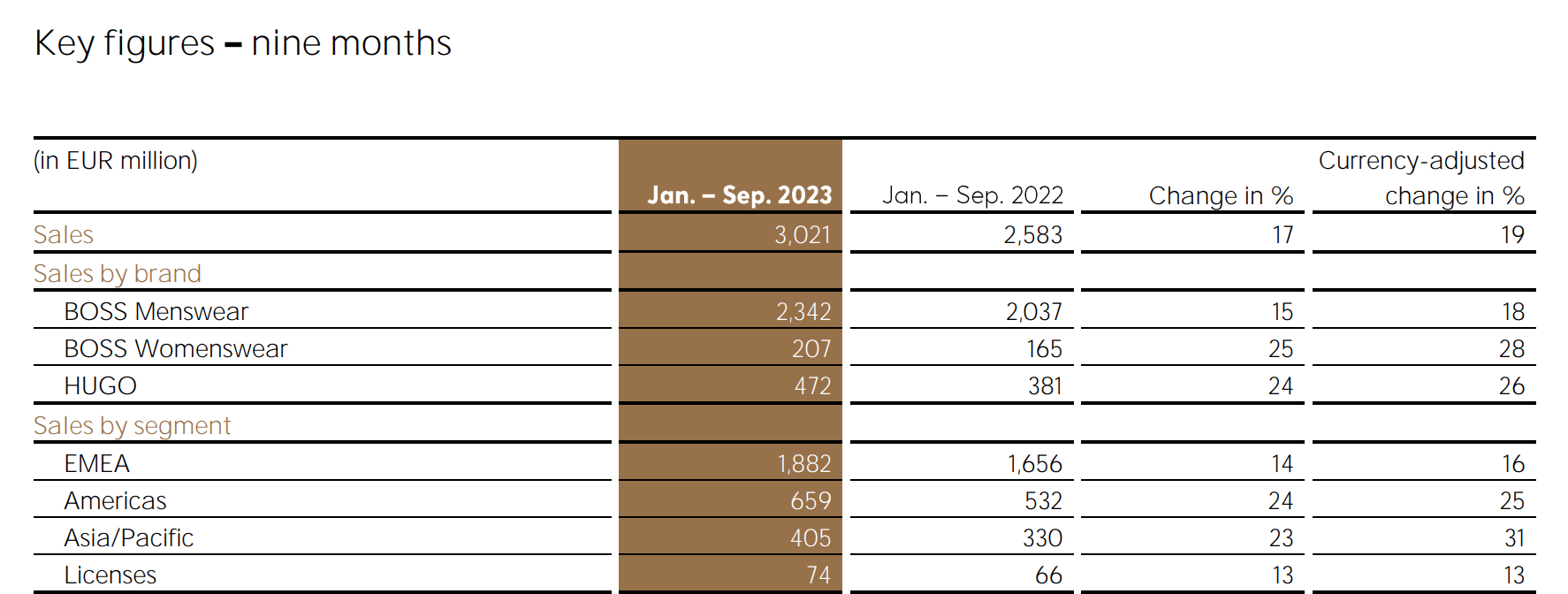

For 9M 2023, the company's sales growth is still rather positive at 19% year-on-year (YoY) on a currency adjusted basis and at 17% at actual exchange rates, even though it has been cooling off with each succeeding quarter. Its growth across geographies is particularly notable, with all its key markets of EMEA, the Americas and Asia Pacific showing double-digit growth in both currency adjusted terms and at market exchange rates (see table below).

{kind=link}

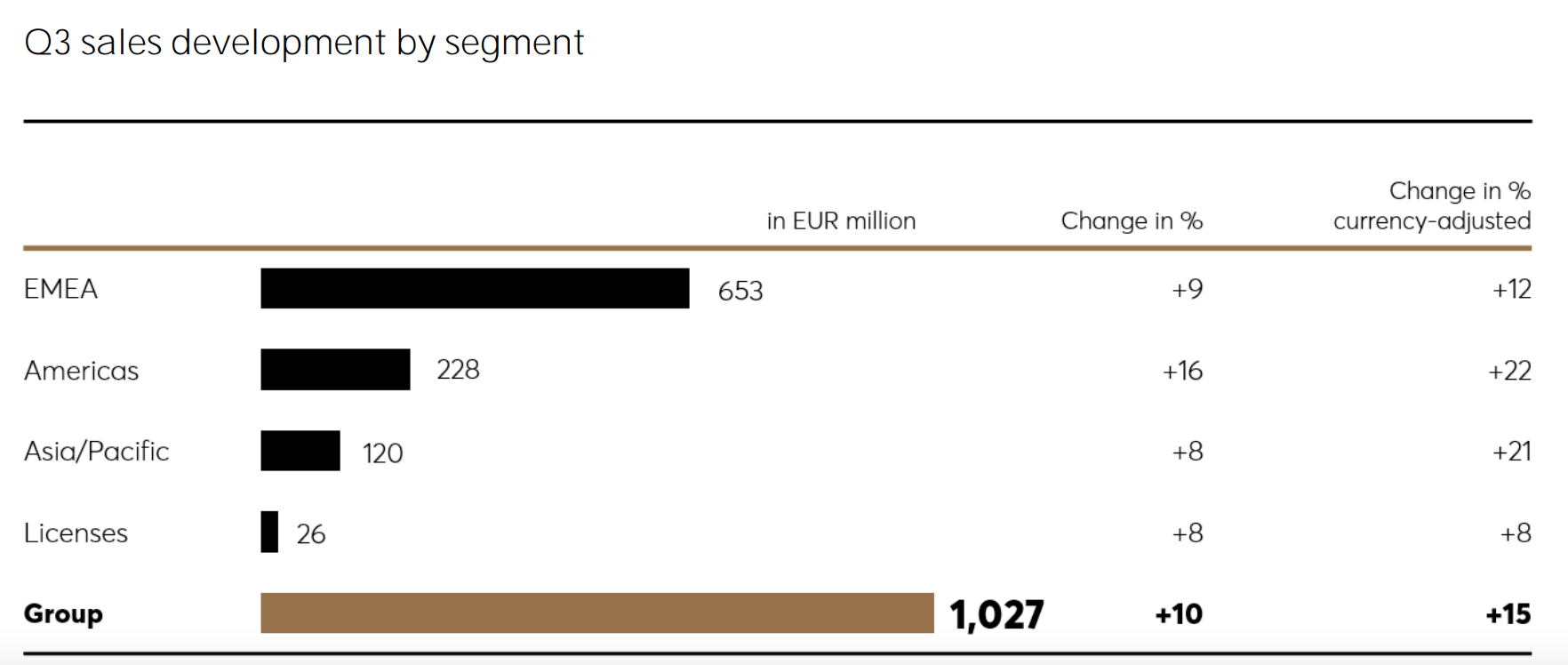

In the third quarter (Q3 2023), there has been some softening in sales growth to 15% at constant currency and at 10% at actuals, essentially indicating that it's the exchange rates that have played spoilsport more than anything else in the latest quarter. At constant currency, once again, all key geographies have seen double-digit growth (see chart below).

The growth across markets is a real highlight here considering that other luxury brands have reported significant softening in sales, especially in the US market. However, it's not entirely surprising. A few months ago, the Longines owner Swatch Group (SWGAY) had also confirmed that its sales were strong "particularly in the lower and medium price segments, with high double-digit growth rates". In other words, while premium luxury is seeing a softening, affordable luxury is still thriving.

{kind=link}

Sustained margins

The company's profit picture looks good too, with operating income and net income attributable to shareholders seeing strong growth of 25% and 24% respectively. The margins were largely sustained too, with the gross margin at 61.5%, just a shade lower than the 62% seen for 9M 2022. The operating and net margins came in at 9.6% (9M 2022: 9%) and 5.7% (9M 2022: 5.4%). In Q3 2023, the net income margin was particularly improved, rising to 6.1%.

Positive outlook

With this as the result, it's no wonder that the company has left its outlook unchanged for the full year 2023 after twice revising it upwards earlier. It now expects the following:

- Sales growth of 12-15% on an actual basis, which amounts to EUR 4.1-4.2 billion. This compares positively with the initial expectation of a "mid-single-digit-percentage-rate", though it is still a decline of 31% from growth in 2022.

- EBIT growth of 20-25% to EUR 400-420 million, which would result in an operating margin of 9.9% at the midpoint of both the revenue and EBIT ranges. This is higher than the 9.2% for 2022 and a significant increase from the initial target of 5-12% growth.

- Net income growth of 20-25%, which would result in a 6.56% net income margin assuming it comes in at the midpoint of the range. This is up from 6.08% in 2022.

The market multiples are still a bit high

The absolute net income number would come to EUR 256 million, with the above assumptions. If the ratio of net attributable income to shareholders to net income remains constant at 94%, as seen in 2022, the forward P/E for 2023 comes to 16.1x, a definite correction from the 20.9x levels at the time I last checked.

My estimates are a tad higher than other analysts, at 15.45x, which is almost in line with the 15.34x for the consumer discretionary sector. But it needs to be noted that the gap between my estimates and those of the sector has narrowed significantly too, since the sector was trading at 14x when I last checked. Still, it is a bit higher. The same is true for the trailing twelve months [TTM] P/E at 17.5x compared to the sector at 15.6x.

Source: Seeking Alpha, Author's Estimates

Some premium on the stock is justifiable, though, as an affordable luxury brand. These brands tend to trade at relatively higher market multiples. And on a TTM basis, BOSSY is indeed trading at a lower P/E compared with peers like Tommy Hilfiger and Calvin Klein owner PVH Corp. ( PVH ), Michael Kors and Jimmy Choo owner Capri Holdings ( CPRI ) (see chart above). However, its forward P/E is actually higher. As a result, this comparison reveals that considering the average of the two multiples, Hugo Boss is due for some further correction for now.

What next?

I think Boss would start looking interesting again if its price drops below USD 13 from the present level of USD 13.8. It clearly has a lot going for it in terms of improving its sales growth from the compounded annual growth rate [CAGR] of 5.52% over the past decade. Its margins are also sustained and it's set to increase profits in double digits in 2023.

However, the price is still slightly higher than desirable. This is especially so when considering its peers' forward P/E ratios. Right now, it's best to continue to Hold, but keep it on the watchlist for now. It could be a rewarding stock over the medium term.

For further details see:

Hugo Boss: Wait For Further Price Correction