TCN - I Am Buying These REITs During This Correction

2023-04-11 08:05:00 ET

Summary

- There are lots of opportunities following the recent correction.

- Many REITs are priced at exceptionally low valuations.

- We discuss 2 REITs that we have been buying lately.

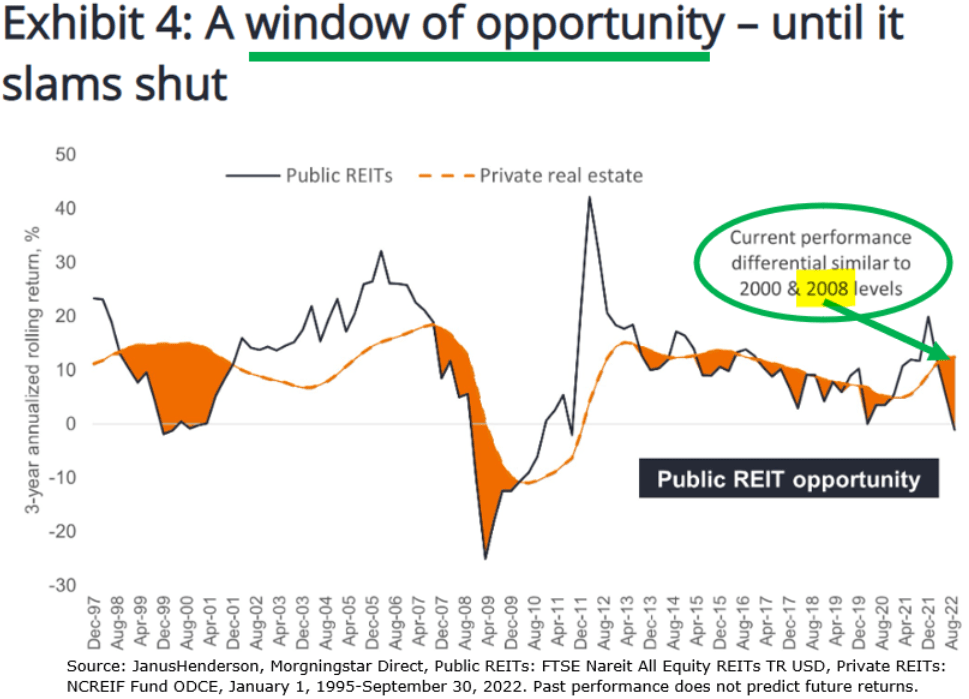

Real estate investment trusts, or REITs, are currently the cheapest they have been since the great financial crisis, according to a study by Janus Henderson. They are priced at a 28% discount on average, which essentially means that you get to buy real estate at 72 cents on the dollar:

{kind=link}

And that's just the average of the sector.

Quite a few REITs are even cheaper than that, trading at 30, 40, or even 50% discounts relative to the value of the real estate they own.

Some REITs, of course, deserve to be discounted. Just think about office REITs like Boston Properties, Inc. ( BXP ) or overleveraged REITs like Industrial Logistics Properties Trust ( ILPT ).

But there are also a lot of REITs that dropped just in association with others and they are now undervalued.

That's what we are buying at High Yield Landlord.

We look for high-quality REITs that are temporarily priced at a large discount. Currently, our Core Portfolio holdings are priced at a 38% discount on average:

High Yield Landlord

It does not take a genius to understand that buying real estate at a huge discount is likely to be a good investment in the long run.

Sure... there are some near-term headwinds, but this is more than reflected in the price, and eventually, headwinds will again turn to tailwinds and valuations will again expand.

In today's article, we want to highlight a few examples that we are today accumulating for our Portfolio:

Tricon Residential Inc. ( TCN , TCN:CA)

TCN is one of just three companies that focus on single-family housing:

They all performed very well in 2020 and 2021 as home prices surged, but then they collapsed in 2022 as interest rates rose and investors began to fear that the housing market could crash:

Tricon Residential

This is a fair concern. Housing affordability has rarely been worse, and very few transactions are happening today.

But as you probably know: the best time to invest is when everybody is fearful, and there are few other sectors that are impacted by greater fear than single-family housing at the moment.

As a result, these companies are now priced at exceptionally low valuations with steep discounts on their net asset values.

The values of their properties may decline in the near term, but the discounts are so large that this should be largely priced in.

We are bullish on AMH and TCN, but I am the most interested in TCN because of its valuation and its asset management business.

Valuation

Tricon Residential is priced at the lowest valuation in its peer group with an estimated 40% discount to its net asset value, providing great margin of safety if property prices begin to decline and significant upside potential if and when interest rates return to lower levels.

TCN is a Canadian company (with a U.S. listing), and so it needs to provide NAV estimates based on property appraisals. The management believes that its current NAV estimate is conservative given that they have been able to sell properties at a 10%+ premium to it.

Moreover, we think that the values of these properties should be somewhat more resilient because 90% of them are located in strong sunbelt markets, and these are mainly affordable properties with a $1,700 monthly rent on average. The management also thinks that their current rents are about 20% below market.

Here is what the CEO said on a recent conference call :

"All of this to say that we have a lot of faith and a reported net asset value of $13.74 per share or CAD18.83 and believe the pullback in our stock is far over done."

This, of course, does not mean that its NAV won't decline at all, but it should limit the downside as its properties remain in high and growing demand and its rents keep growing at a rapid pace.

Asset Management Business

Unlike its peers, TCN is not just a traditional landlord.

It also has an asset management business that allows it to earn fee income by managing capital for others.

That's how the company owns $17.6 billion in assets, despite only having a $2.3 billion market cap.

This makes it less dependent on public capital markets because it does not need to raise new equity to buy additional properties. This wouldn't be possible at today's prices anyway.

Instead, it can raise capital in private markets from other investors to buy additional properties and it earns growing fee income as it grows its assets under management.

Before the recent surge in interest rates, they were targeting 15% annual FFO (funds from operations) per share growth over the next 3 years. They then recently scaled back their growth plans because they don't think that it would be prudent to aggressively purchase new properties in today's uncertain environment.

But it shows you that they have access to ample private capital and could grow significantly in the coming years as the market eventually stabilizes. Even Blackstone's BREIT formed a $300 million partnership with TCN to acquire single-family properties and many other leading institutions are interested to work with Tricon. It speaks highly for their management.

In 2023, we think that the company's FFO per share will be more or less intact because its strong organic growth will go into higher interest expense. One downside of TCN today is that it has a lot of variable-rate debt, but this is priced into the stock, and it should serve as a significant catalyst if and when interest rates begin to decline.

Its close peer AMH recently released strong results with 5-7% same-property revenue growth and a 22% dividend hike.

American Homes 4 Rent

TCN's yield is relatively low at ~3%, but this is a growth story with the bulk of the returns expected to come from future upside as the company returns to rapid growth and its discount to NAV eventually closes down.

In short, you get to buy an interest in a diversified portfolio of professionally-managed Sunbelt single-family homes at 60 cents on the dollar and then get to participate in the long-term growth of their asset management on top of it.

Whitestone REIT ( WSR )

WSR is also a heavily discounted REIT that focuses on rapidly growing sunbelt markets.

But its thesis is quite a lot simpler because this is a real REIT that's structured in the USA and it does not have an asset management business. It is also relatively small in size, which makes it easier to analyze its assets.

WSR specializes in retail strip centers, and we estimate that it is currently priced at a 40% discount to its NAV.

Whitestone REIT

Whitestone REIT

We suspect that it is so cheap because it is categorized as a "retail investment" and retail is today out of favor.

But here's what the market is missing:

Recession-resistant: These properties are mostly recession-resistant because they focus on essential services like grocery, barbershops, fitness, restaurants, etc.

E-commerce resistant: Again, because these are essential services, you cannot easily get them on Amazon.com, Inc. ( AMZN ) or elsewhere. No online grocer is today profitable, and most people prefer to work out at a gym than at home using stuff like Peloton Interactive, Inc. ( PTON ).

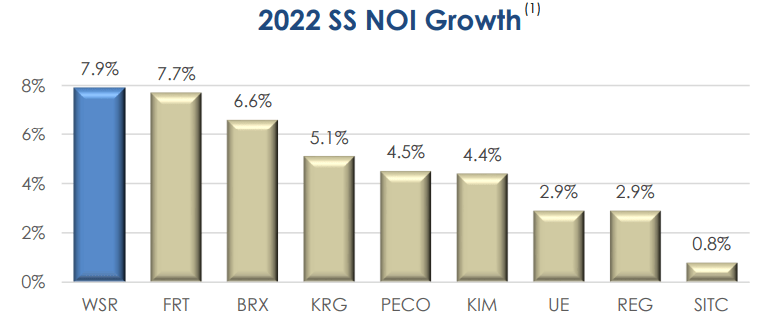

Rapidly growing markets: These service-oriented strip centers are located in rapidly growing sunbelt markets like Austin, Texas, and Phoenix, Arizona. As a result, there is growing demand for them and this is reflected in rapidly growing rents. In fact, its rents have been growing even faster than those of Federal Realty Investment Trust ( FRT ), Regency Centers Corporation ( REG ), and other blue-chip REITs:

{kind=link}

Whitestone REIT

Therefore, we think that it is unfair to discount WSR by so much and believe that it is now undervalued.

The market also appears to worry about the REIT's balance sheet because it has historically used more leverage than average, but the market appears to have also overlooked the significant improvements that they have made on this front.

Their leverage has come significantly already, and the CEO recently told us in an exclusive interview at High Yield Landlord that they expect their Debt/EBITDA to be below 7x within a year.

All in all, you get to buy good retail real estate with growing rents at 60 cents on the dollar.

Not a bad deal in my opinion.

You also earn an 11% cash flow yield while you wait. Half of that is paid in dividends and the rest is reinvested in growth/deleveraging.

Bottom Line

On average, REITs have earned an 89% total return in the next three years after being priced at a 20% or greater discount to NAV:

Janus Henderson

Each time, there were reasons why REITs were so heavily discounted.

But eventually, headwinds turn into tailwinds, narratives change, and REITs recover.

We think that this time, again, investors who buy the right REITs at these levels will make a little fortune in the coming years.

For further details see:

I Am Buying These REITs During This Correction