ABNB - I'll Avoid These Sectors In 2023

Summary

- I wrote an article about which sectors I intend to focus on for this year, with a number of example picks for each sector. In this article, it's the opposite.

- I will show you what sectors I will try to avoid, given volatility or negative potential for these sectors.

- However, as we know clearly, it's all about valuation and there are exceptions - I will show you exceptions for each sector.

Dear subscribers,

In my previous article, I made a general case for why I am investing in certain, key sectors that I view as having a solid upside for the coming year. This is in spite of any recession risk or potential volatility that I believe the market will face in this year.

Cost inflation and general inflation aren't going anywhere. Unemployment will be coming up higher, given the massive amounts of tech layoffs that we're seeing across the globe. Ukraine is still a powderkeg of military activity with an active war going on in full, and there's plenty of tense geopolitical macro in the west and Asia even without considering that.

It's a mess, dear subscribers. A mess.

However - the volatility that some people and investors shy away from, that's where value investors thrive - provided we're as well-rounded, well-read, and well-informed as we think we are.

Why?

Because our knowledge and our degree of macro and valuation expertise mean that we can cherry-pick the investment opportunities that we see will/could outperform. We're not perfect, but I would argue that looking over time, you'll see that DK/iREIT contributors have a success rate that's above the average in the long term.

Equally important to see what we invest in, is what we don't invest in.

That's what this article is going to be about.

What sectors not to invest in, and what sectors I, with some exceptions, won't be touching all that much this year for long-term investment.

Some Disclaimers

First off, some disclaimers.

Just because a sector is unattractive, doesn't mean that there aren't singular opportunities in that sector. I believe/"know" that every sector has the sort of companies that will not only survive, but they will also thrive. That's why there are companies that still manufacture telephones, after all.

Heck, despite the car being around for over 130 years , there are still companies that manufacture horse-drawn carriages and do so with profit. Or, we've had computers for over 50 years, but there are still companies that build manual typewriters. It's all about excelling in your field, whatever that field may be.

And no matter which field I look at here, there will always be companies that see outperformance, just as there will be companies that fail to perform well, despite being in a tailwind-heavy sector. If we look hard enough, we'll even find some tech companies that managed to not garner positive RoR despite the tech-frenzy in 2020-2021.

So, perhaps we should view this as a list of sectors where you need to be extra careful prior to put money to work, as opposed to saying "NOPE, that's X sector - Wolf report said to avoid it."

So, here are the sectors I would avoid - again, in no particular order.

1. Energy

Not utilities, but Energy. The energy sector is coming off a blockbuster 2022 which was characterized by tight supplies and rising demand due to massive energy price increases and trouble across the world, not just in crude, but also gas and even coal.

Given the risk of recession, I believe that energy prices will not rise much further beyond the levels we saw last year. I'm a bit of a lone wolf in this, I'll admit because most analysts I follow actually view Energy as a pretty "safe" sector going into next year - so take what I say here with a bit of salt, and shop around a bit for other opinions.

Me, I believe the combination of continued renewable capacities and the already high prices for energy will make seeing any further increase here somewhat hard.

More importantly, I think you will all agree that the macro outlook for 2023 is a bit of a "Wild card", and the volatile energy sector isn't a sector I want to be overexposed in after an outperformance. Why?

Because historically speaking, the drop back down from energy tops has been mutually assured (value) destruction for investors, over time.

Just consider for a moment that Russia and Ukraine reach a truce. The war is over. This could result in energy price declines as Russian capacities are routed back across the existing infrastructure. Is it likely? Maybe not - but it's a possibility.

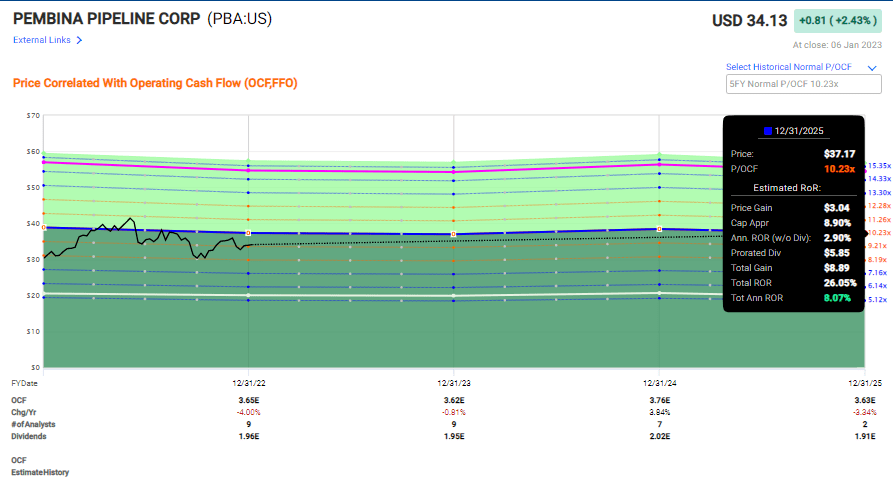

So, be extra careful with Energy. I view upstream as the subsector having the most risk, and would view downstream and midstream as the more favorable plays - or energy plays with a mix of renewables. But most companies have been winding down their expectations. Just look at what Pembina Pipeline could generate, based on normalized forecasts.

{kind=link}

Pembina Valuation (F.A.S.T graphs)

Same thing with Enbridge, at around 9% (which granted, is better, but not great) That's why, last year, I sold my shares of Pembina at just around $40/share, at a nice, tidy profit. Enbridge is gone too, for me.

Remember, and I say this with love, analysts have a tendency of being the last people in the game of musical chairs when the music stops.

Just look at how long it took them to down-wind some of their PTs in tech.

Still, two names I would be interested in looking closer at here:

Both of these haven't seen as much growth, both investment-grade rated, and both are what I would view as solid. Other than those, or similar ones, I'll be very cautious about energy.

Moving on.

2. IT/Tech

This is probably the broadest one yet, and you could even make a valid argument that some companies I would consider Tech are actually communications companies instead.

The main thing is, I don't see an easy 2023 for Tech or IT here. Yes, there are plenty of drivers here for the bullish camp - cloud computing, artificial intelligence, and the growth of the 5G wireless network are all factors that play into growth, though I choose to get part of that growth by simply investing in Telcos which may be viewed as ancillary.

The opportunities in the sector, in the form of semiconductors, are massive. But the sector also holds companies that I view as unlikely to go anywhere. This includes Apple ( AAPL ), where the next 3-4 years of results are forecasted to bring about average returns of less than 4-5%, at a 20x+ P/E despite dropping significantly. And Apple is, without a doubt, one of the best companies in this space.

However, the combination of increased interest rates, many of the tech "darlings" being unprofitable, SBC-heavy collections of dubious value (Kind wording, less kind being "trash") that have never or rarely actually turned a profit, ever, (I'm looking at you, Roku ( ROKU ), Palantir ( PLTR ), Airbnb ( ABNB ), Blue Apron ( APRN ), Dropbox ( DBX ), Lyft ( LYFT ), Peloton ( PTON ), Pinterest (PINS), Snap ( SNAP ), Uber ( UBER ) and Zillow ( Z ) to name only a few), means that I must admit to feeling somewhat vindicated compared to last year.

Why?

Because it seemed quite popular to take anyone who questioned the ridiculous valuations of some of these "companies" ( A company without consistent profit isn't a real business, it's a hobby, sorry. ) and simply call them outdated, or not understanding the "new paradigm".

Well, the old paradigm is back - reality .

And reality isn't kind to wishful thinkers who honestly thought you could power a business long-term using a combination of hope, caffeine, and debt.

Such as the idea of slapping an iPad on an exercise bike, charging $2,000+ for it, not to mention a $12.99 membership fee per month, and advertising it as a realistic alternative to a $10-$15/gym membership and then seriously making the case that a $160+ share price is valid for such a business.

Almost none of the companies mentioned above are "new" businesses - the excuse that it's never profitable in the beginning is to one that works if your business has a 6-8+ year history.

I believe 2023 will be just as harsh and a wake-up call to many of these businesses, even the ones that actually turn a profit, like Salesforce ( CRM ), a solid business with A+ credit. Many of these companies have never experienced the actual cost of capital, and it's dubious if their business model (not Salesforce, but others) can even survive such an environment.

It's going to be a trying time, and I have no desire to be a Guinea Pig by investing in it, nor should you.

Anyway, IT/tech - what should you be investing in?

I would say that opportunity will be found in quality plays that operate the outer or core segments of the semiconductor, or non-optional software sectors, such as:

- Qualcomm ( QCOM )

- Skyworks Solutions ( SWKS )

- Global Payments ( GPN )

- Cisco ( CSCO ) (only slight upside at this point)

So, those are some examples of companies in the sector I wouldn't call "bad" investments at this time. In fact, even Microsoft ( MSFT ) is looking decent.

3. Healthcare/Pharma

This one isn't as much an "avoid", as you can't just pick any undervalued name any longer. Healthcare/Pharma came out strong in 2022 due to the defensive nature of the entire sector. I remain invested in favorites, such as Bristol-Myers ( BMY ) and Merck ( MRK ) as well as Novartis ( NVS ). But I've left behind plays I view as more problematic - not because they're not quality companies, but because I'm not sure how they can adapt to company-specific trends.

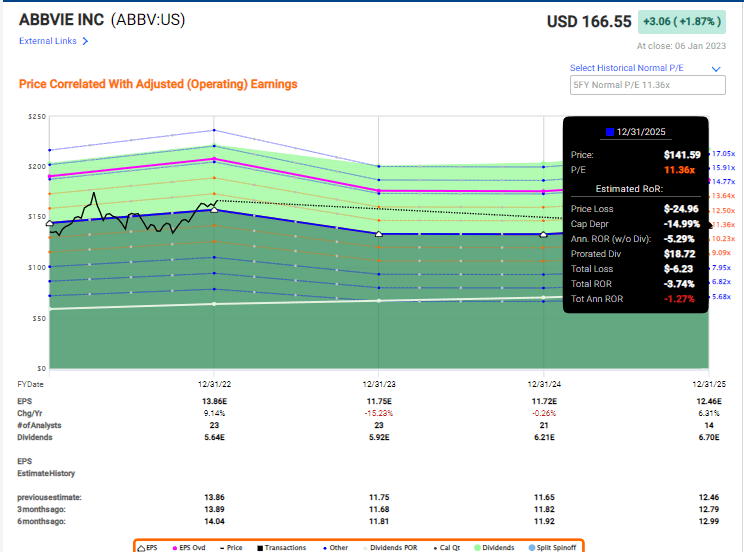

A good example of this is AbbVie ( ABBV ). AbbVie is in no way a bad company, but I sold what remained of my stake at over $165. Remember, my cost basis for this stock was below $70/share. That's when it was time to buy AbbVie.

Now?

{kind=link}

AbbVie forecasts (F.A.S.T graphs)

Not so much, as I see it. Even if the company manages the Humira decline better than expected, you're still looking at some pretty sobering circumstances for outperforming the market. At 3.55% yield, I believe you're literally better off by just doing a 50/50 into BMY and MRK - less yield, but better growth potential and broader spectrum.

What I'm pointing to here is that the last 3 years have meant that healthcare and pharma, for large parts, have performed very well - but fundamentals now matter to a greater degree than they did in 2022.

This sector is defensive, and defensive plays are good, but the sector is going into 2023 much more soberly valued than in 2022. I believe the outperformance potential for this one is actually fairly low here.

But, as always, there are solid plays despite what I view as conservative views for the sector.

Here are two I am going for.

4. (Most) Basic Materials

Basic Materials and chemicals may have a rough year. These companies and the sector are inherently cyclical, meaning their downside potential in a recession and downcycle is significant.

Combine this with a slowdown in China which is influencing the markets for many base metals and commodities, and you may see why I'm fairly neutral on the entire sector, with certain qualitative exceptions. I like companies that tilt specifically toward the rebuilding of Ukraine, for instance. That's a sector I believe is going to be gangbusters, and why I'm heavily invested and positioned in key companies that my research shows will benefit significantly from the upcycle there.

There are also plays on EVs - chemicals or materials used by these companies will mostly weather any sort of downturn rather well, I believe.

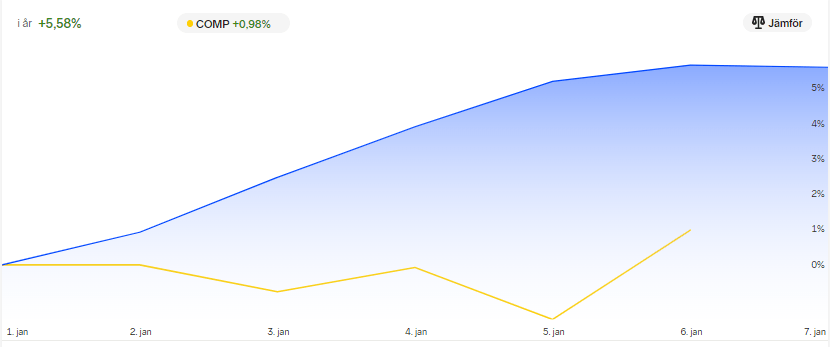

Materials and Chemicals actually outperformed, and I've started my investment year extremely strong in no small part due to my exposure to these companies bought at very good prices, or in some cases, actually trough lows. Here's a snapshot of my YTD investment performance for the first week.

{kind=link}

Nordnet Author Portfolio Performance YTD (Nordnet)

And there are a lot of basic materials like BASF ( OTCQX:BASFY ), HeidelbergCement ( OTCPK:HDELY ), Yara International ( OTCPK:YARIY ) and others in that outperformance. Pretty decent, if I do say so myself.

But, overall, I think it's a bad sector to be overexposed or go too heavily into unless you know very closely what you're doing.

However, two potentials I see and view as potential attractive here, based on the way the current industry is moving - copper and fertilizer.

So, because of that, I'm watching:

- Freeport-McMoran ( FCX )

- Yara International ( OTCPK:YARIY )

Aside from those, I'm going to be very, very selective of my exposure here.

5. (Almost All) Consumer Discretionary

Yeah, this is the sector I'm probably least in, with the exception of quality, timeless luxury plays like LVMH ( OTCPK:LVMUY ) and Kering ( OTCPK:PPRUY ). The sector has vastly underperformed over the past few years, and while I have been able to make timely gains, RoR and exits with companies like Whirlpool ( WHR ), the consumer discretionary sector together with Energy, is my least invested sector going into 2023.

The sector was down 31.35% in 2022 - and I got my share of that decline with key exposures during the year as well.

The reason for this massive outperformance was high rates of inflation - both input and wage, higher energy prices, less money for consumers, logistics, supply chain bottlenecks out the wazoo (particularly in 1H22), and massive price increases above inflation , passing along costs - and more - to consumers.

This was certainly a recipe for disaster, and only the absolute best and strongest survive here. So when consumer demand began to fall in 2H22 in response to recession fears, it wasn't odd to see this sector even further out of favor than it was going into the year.

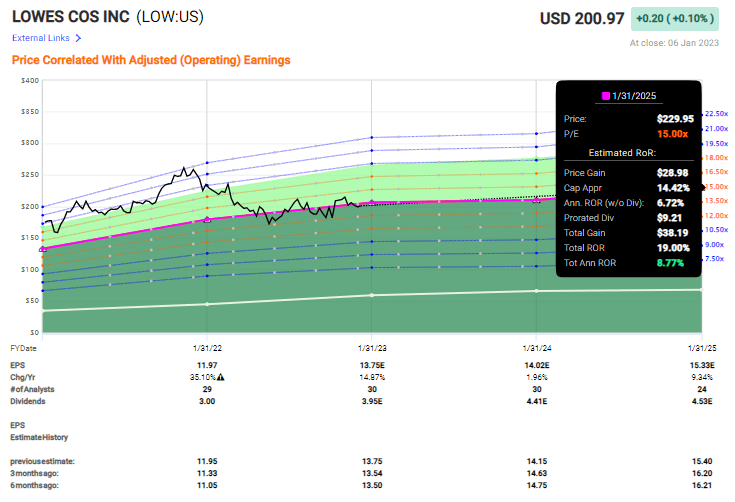

Consumer discretionary is in a very tough spot. I wouldn't touch many of the companies that others are working with here - such as Tesla ( TSLA ) or Amazon ( AMZN ). I know that differs me from even from some of our other very talented/expert contributors. I'm also very careful with anything from this sector that was once touted as "cheap if it's ever not premium", like Lowe's ( LOW ). Lowe's as an example has spent a longer time normalized at 15x P/E than it has at its premium for the past year.

{kind=link}

Lowe's Valuation (F.A.S.T graphs)

And to be clear, I own shares in Lowe's. It's decently attractive here, as I see it.

The one thing speaking for investing in discretionaries is the substantially low valuations we're currently seeing in the sector. I cherry-pick the best of the mass, and leave the rest out, to see what happens with them.

As of now, the only "clear" opportunity I see lies within the Home improvement sector as well as footwear, with recovery finally taking place. So much of this part of the index (of most funds) is Amazon, and that's a company I'm not investing in.

So, for now:

- Lowe's ( LOW )

Wrapping Up

Don't view this as a list of forbidden sectors - view it, rather as a list of sectors where I believe we need to be extra careful. Keep in mind that, at heart, I'm a contrarian.

When everyone says a company is cheap, sometimes that's the case - and when it is, I'll agree.

But "everyone saying X" usually gives me pause, it doesn't make me enthused in the least. I try to search the outer circumferences of the market for quality companies that are overlooked , not something that everyone suddenly says is good.

When everyone says "Company X is lost", that tends to make me pretty interested.

Sometimes my strategy leads me to taking positions too early. It happens - but more often than not, statistically speaking, it has led to triple-digit annualized or actual RoR outperformance.

Let's do an example.

Right now many people are saying that Office properties and as a result, the REITs that hold them, are trash. There's going to be massive declines in occupancy, reorganizing of space into multi-use or even residential, etc., etc., etc. We've heard it. When something like this is said, and its specifically exemplified by one area (in this case the west coast), this negativity often spills over into other companies and geographies of that sector.

This leads to massive valuation disconnects. And that's what I look for.

I believe both residential REITs, with certain key examples, and office REITs are very good examples of this. And that is why I push money to work here currently, expecting significant outperformance.

It's certainly a market to be careful in - but it's also one where we should not ignore outperformance potential if a sector or a company has been punished.

So, what I want to leave you with going into this year from a macro level is to:

- Stay alert.

- Allocate according to your strategy - whatever it may be.

- Don't invest in a "bad business", regardless of valuation - it's not viable.

- Don't let uncertainty or exuberance be more important than hard data and facts

- Don't put yourself into situations you know will be uncomfortable for you, risk or finance-wise.

- Don't alter your approach just because of a crash. If you believe in the company, realize that the market is unpredictable, illogical and overreactive.

And above all, stay grounded. If you're a part of iREIT on Alpha, Dividend Kings or any service where you feel safeguarded, you're certainly not alone.

All the best for this year - and let me know any questions you might have!

For further details see:

I'll Avoid These Sectors In 2023