AMX - I'm Waiting For América Móvil's Margin Expansion

2024-01-06 04:45:14 ET

Summary

- América Móvil's Q3 2023 earnings show strength in volume drivers at the expense of rate.

- The company is facing headwinds with volatility in FX and macroeconomic factors impacting its performance.

- While the stock price has decreased, concerns about long-term value and the need for margin expansion remain, leading to a hold rating.

I am following up on my Q1 2023 thesis for América Móvil (AMX) in light of JV changes and in advance of year-end earnings.

I previously rated América Móvil a hold for the following reasons:

- Performance across countries was inconsistent, with strength in Brazil and Mexico partially offset by rate and volume challenges in other areas

- The company was facing headwinds in the Latin America telecom market as well as its own scale.

- Favorable valuation multiples reflected non-operating noise from FX.

- The stock price had steadily climbed across five years, putting it at what I believed was a fair price.

Since my last analysis, America Movil is down more than 14%, returning to the same level from 1 year ago, while the S&P 500 was up more than 6%.

AMX Price Trend (Seeking Alpha)

{kind=link}

While the lower price made me more optimistic about the stock, and America Movil certainly isn't going anywhere, I continue to have concerns about its long-term value. The Chile Joint Venture with Liberty Latin America is an unnecessary distraction and a drain on cash flow. Performance, especially on net ads, is improving but is still inconsistent, especially outside of core consumer wireless. In addition, volatility in FX and below-the-line items continue to show that America Movil is overexposed to macroeconomic factors. Lastly, DCF shows that price growth is dependent on margin expansion, which has yet to actualize.

With all of the above in mind, I continue to rate America Movil a hold as the price target of $16-20 is a balanced risk-reward to today's pricing.

Chile JV An Unnecessary Distraction

On December 23rd, America Movil and Liberty Latin America announced additional funding for their struggling JV in Chile. Without the cash inflow, the JV would have been unable to pay down its current debt. This certainly helped the Chilean entity and its bondholders , but it doesn't help America Movil's shareholders.

According to recent reports , Chile has the most mature telecom industry in Latin America. There is little to no organic growth in the wireless segment, which is reflected in the struggles of the JV. Chile has a forward growth rate expectation of 1.9%, a percentage point below overall Latin America. Voice services are expected to continue declining, offset by data

{kind=link}

ARPU Continues To Be A Concern

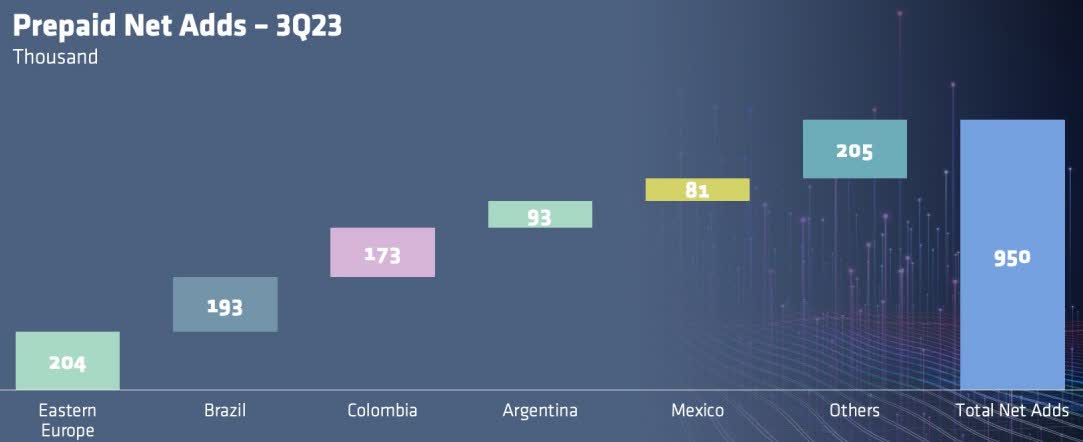

In my previous analysis, I had concerns on both the rate and volume side of the core wireless business. The good news is that volume has improved with every region showing growth in postpaid and prepaid.

Q3 Postpaid Net Adds (AMX Investor Relations) Q3 Prepaid Net Adds (AMX Investor Relations)

{kind=link}

{kind=link}

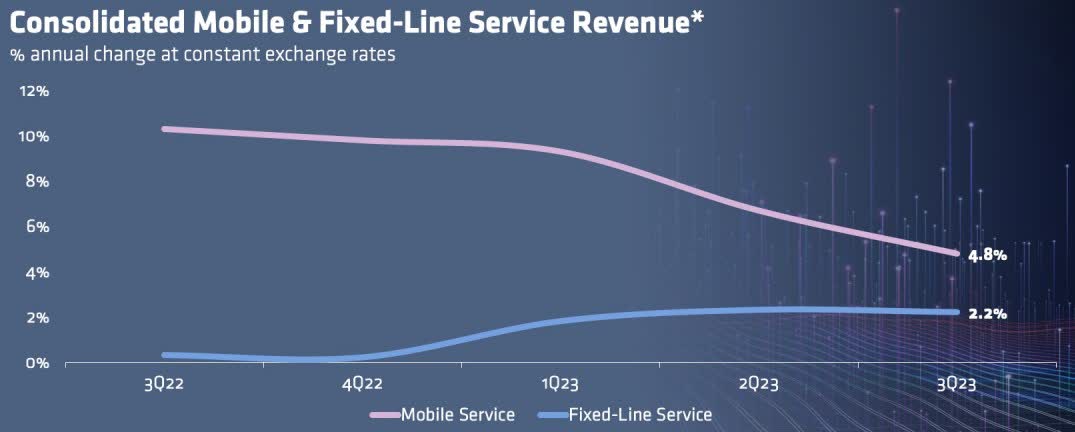

Unfortunately, total revenue declined 3.3% on the back of FX, and service revenue growth adjusted for FX decelerated across the business.

Service Revenue Growth (AMX Investor Relations)

{kind=link}

A couple of reasons for revenue slowdown are causes for long-term concern.

First, results on the rate side continue to be mixed as ARPU growth was challenged in every region but Brazil, with inflation outpacing pricing attainment. This signals that strong volume growth is being driven on the back of discounting and slower pricing growth.

ARPU vs Inflation (Worldbank)

In addition to ARPU, businesses outside of core services showed signs of weakness. Corporate services in Mexico were called out in the earnings call as an area of underperformance. In addition, the earnings release showed that Brazil actually declined by nearly 5% in corporate services. This is usually a longer-term, higher-margin area for telecoms and I always get nervous about struggles in B2B.

Cash Flow Overexposed To Macro Factors

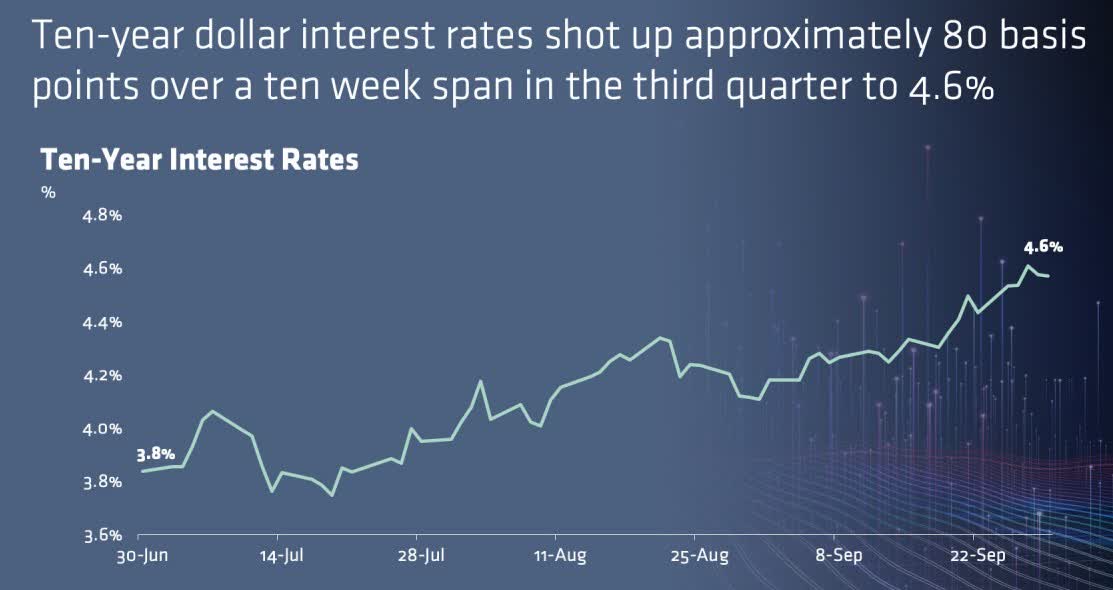

2023 performance continues to highlight just how exposed cash flow is to macro factors.

The Q3 earnings presentation opened not with a slide on financials but with a slide on USD interest rates, showing this as a top concern for management. Keep in mind that America Movil is a highly leveraged Mexican company with over 60% of its debt denominated in USD, EUR, and GBP.

Interest Rate Impact (AMX Investor Relations)

{kind=link}

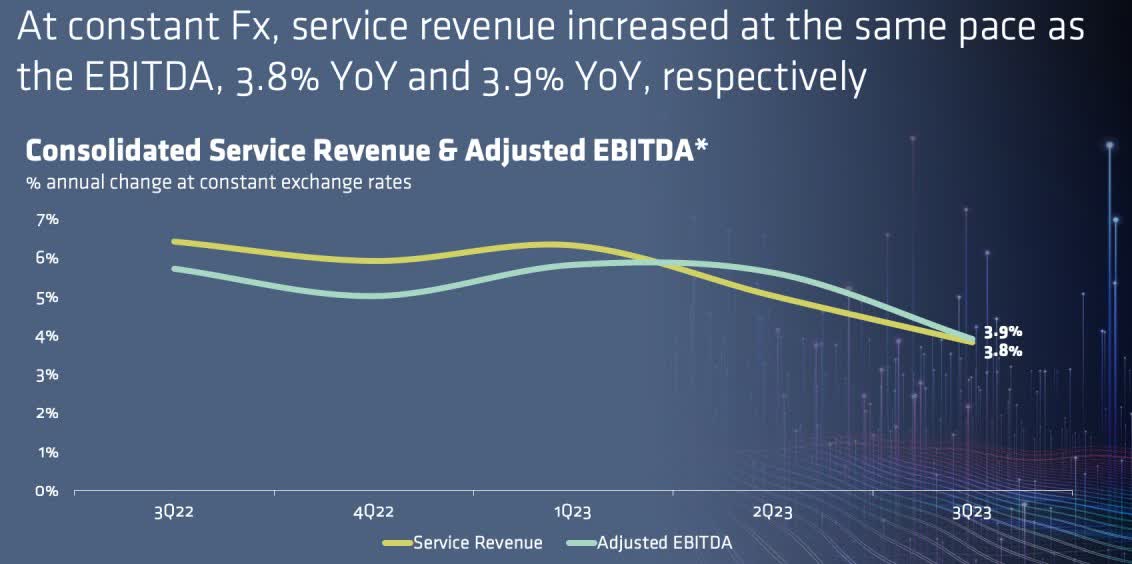

Beyond debt, the overall business is heavily exposed to FX. On the CapEx side, the majority of the $7 billion is spent in other countries. As far as operations go, as reported in Mexican Pesos, the business declined 3.3% overall and 4.3% in service revenue. In constant currency terms, service revenue grew 3.8% or an 8.1 percentage point spread. While FX doesn't speak to the underlying strength of the business, it still impacts cash flow for US investors.

The USD to MXN conversion has been very volatile throughout the year, and I have found no indication of stabilizing.

Price Growth Depends On Margin Expansion

Analysts spent a lot of time on the earnings call around margin expansion. Management guidance has EBITDA growing at a faster rate than revenue through efficiencies and cost control. However, revenue and EBITDA continue to pace in line with each other.

Revenue vs EBITDA (AMX Investor Relations)

{kind=link}

This is critical in setting a target price. I ran DCFs, one with margin expansion and one without. I made the following assumptions:

- Near-term revenue growth of 4% based on current trends, management guidance, and industry long-term growth expectations

- Long-term growth of 3% based on industry CAGR forecast

- Discount rate of 10% as a lower-risk large cap in telecom

With one percentage point of margin expansion, DCF generated a price target of $20, a 10% upside from today's pricing.

DCF With Margin Expansion (Data: SA; Analysis: Author)

{kind=link}

Without margin expansion, DCF generated a price target of $16, 12% downside from today's pricing.

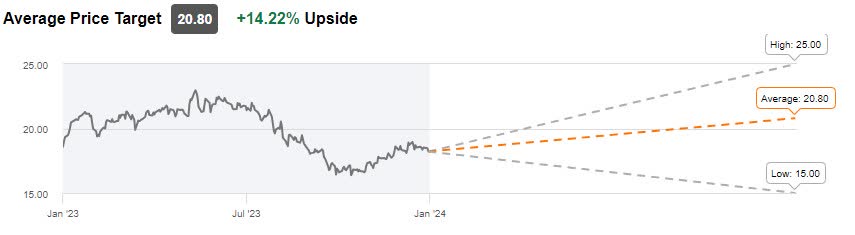

Wall Street has a slightly higher target at $20.80, with a range from $15-25; however, we are still largely in line with risk/reward in the range.

AMX Wall Street Rating (Seeking Alpha)

{kind=link}

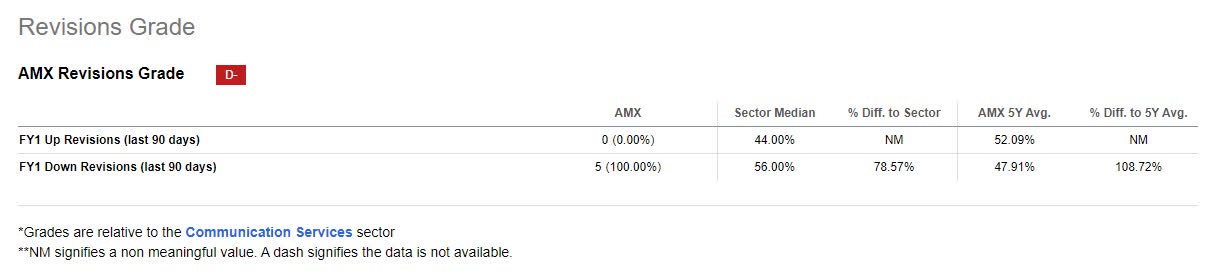

The quant rating is a hold driven by profitability challenges and downward revisions. These are similar concerns I have with margin expansion and decelerating growth.

Earnings revisions are bearish, with consensus consistently revised downward for full year 2023.

{kind=link}

Verdict

America Movil continues to have mixed performance across the business, especially on the rate side. In addition, volatility in interest rates and FX, along with a struggling JV, continue to increase risk to cash flow. With a price target range of $16-20 and a current price in the $18 range, I recommend investors hold current positions. Future success hinges on maintaining revenue growth, increasing margin, and better hedging macro risk. I will be closely watching future quarters for signs of margin expansion or contraction, as well as a turnaround in ARPU.

For further details see:

I'm Waiting For América Móvil's Margin Expansion