ICAP - ICAP: Too Volatile For Income Oriented Investors We Prefer DIVO

2023-03-20 06:52:56 ET

Summary

- Just like JEPI and DIVO, ICAP uses a covered call strategy.

- Such a strategy results in a low beta profile.

- Strangely enough ICAP also uses leverage which results in a high beta profile.

- Unlike JEPI and DIVO, ICAP doesn’t outperform when stock markets go down.

The Amplify CWP Enhanced Dividend Income ETF ( DIVO ) and the JPMorgan Equity Premium Income ETF ( JEPI ) are two popular ETFs for income oriented investors.

Some Seeking Alpha contributors prefer the InfraCap Equity Income Fund ETF ( ICAP ) above JEPI. Do we agree? Does ICAP deserve a spot in the sunlight besides these two giants?

For us, the answer is no. ICAP has no clear strategy, a higher expense ratio, it doesn’t create alpha and, unlike JEPI and DIVO, it underperforms when the equity market falls.

InfraCap Equity Income Fund ETF

Just like JEPI and DIVO, ICAP invest in high yielding equities and uses a covered call strategy on top of that. But ICAP utilizes this option strategy on only 30% of its portfolio. This translates on the one hand in less income, but on the other hand the upside is less capped compared to e.g. JEPI.

In the prospectus is mentioned that the portfolio managers “may purchase and write put and call options in an effort to generate additional income and reduce volatility in the portfolio”. Currently there are only written call options.

Unlike JEPI and DIVO, ICAP also invest in preferred stocks. This makes sense. Like a covered call strategy itself, preferred stocks are lower beta, have less upside potential and offer more income. The portfolio managers claim themselves also that they “opportunistically select preferred securities for inclusion in an attempt to boost yield and reduce ICAP’s portfolio beta”.

About one fifth of ICAP’s portfolio is invested in preferred stocks.

Figure 1: Instrument type (InfraCap)

Preferred stocks are popular among financial companies because it help them meet the regulatory requirements regarding their capital structure. As a result, almost one third of ICAP’s portfolio is invested in financial stocks.

Figure 2: Sector allocation (InfraCap)

The portfolio managers want ICAP’s portfolio of equities to be a diversified selection of securities, including a broad cross-section of sectors and sub-sectors, such as REITs, Utilities, Industrials, pipelines, and financials.

Figure 3: Top 10 holdings (InfraCap)

But more importantly, unlike JEPI and DIVO, ICAP uses leverage (currently 20%)! We do not really understand why one would use leverage in what’s basically a low beta strategy like covered call writing. The leverage will allow ICAP to participate more in the stock market’s upside. This participation was already higher because ICAP limits the use of covered calls. The limited the use of covered calls also leads to less downside protection. And leverage makes things only worse when stocks fall. In down markets there might be no downside protection at all. Leverage leads to a higher beta, both on the upside and on the downside. How many income oriented investors are interested in an ETF that almost “promises” to underperform when the equity markets go down? Looking at ICAP’s asset under management not that many.

Probably due to the use of leverage the expense ratio of ICAP (0.8%) is higher than those of JEPI (0.35%) and DIVO (0.55%).

Performance

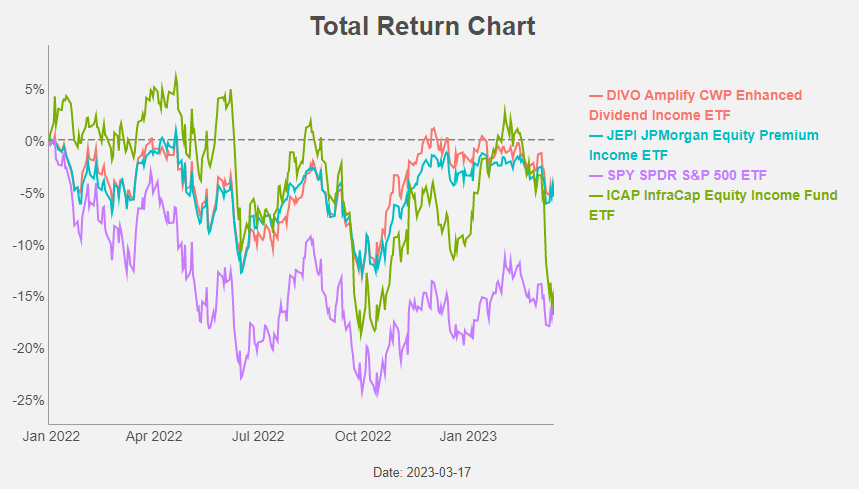

The performance of ICAP since inception is in line with that of the S&P 500. Both are down almost 17%.

{kind=link}

DIVO and JEPI perform much better in this down market. The reason is twofold: they earn more option income and their security selection creates alpha on top of that. Or, in other words: their (coherent) strategy is working.

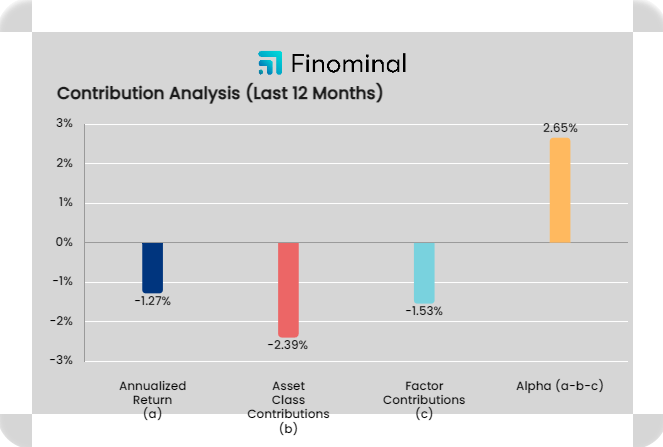

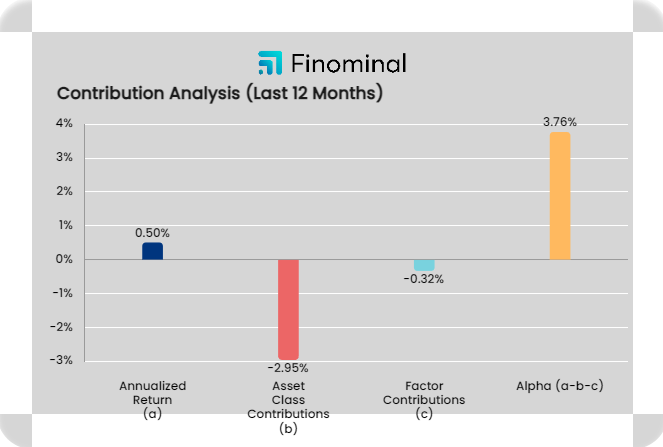

Over the last 12 months, JEPI and DIVO delivered 2.65% and 3.76% alpha.

{kind=link}

{kind=link}

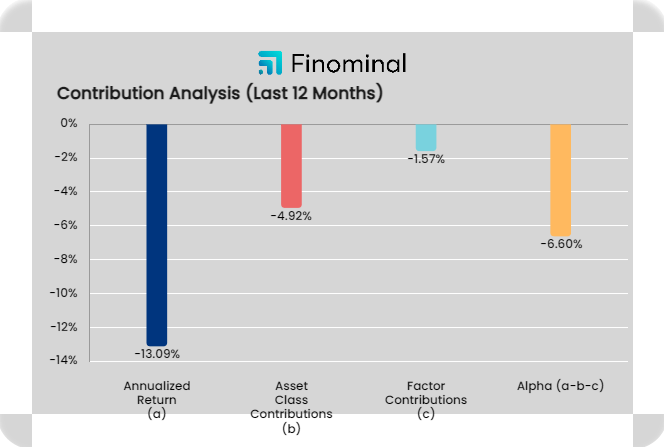

ICAP on the other hand, delivered an alpha of minus 6.6%.

{kind=link}

Not unexpectedly, Figure 4 also makes clear that ICAP is much more volatile than JEPI and DIVO. The latter have a beta in the range of 0.6 to 0.7, while ICAP has a beta of 1.1.

Banking crisis

ICAP’s underperformance can be explained by

- the leverage that amplifies the negative stock returns

- the more limited option premium income

- the security selection in general and the overweight in Financials in particular.

Preferred stocks are popular among financial companies because it help them meet the regulatory requirements regarding their capital structure. As a result, almost one third of ICAP’s portfolio is invested in financial stocks. The weight of Financials is much less in both JEPI and DIVO. This is good news for both JEPI and DIVO the moment a financial crisis happens, as is currently the case.

Figure 8: Sector allocation comparison (ETFResearch) Figure 9: Sector allocation comparison (ETFResearch)

ICAP also has a higher allocation to Real Estate and Utilities. All three sectors are in a long term downtrend.

{kind=link}

But, not only ICAP might feel the negative impact of the banking crisis. JEPI uses an options overlay that implements written out-of-the-money S&P 500 Index call options to generate distributable monthly income. It does this through so-called equity-linked notes (ELNs). These are derivative instruments that are specially designed to combine the economic characteristics of the S&P 500 Index and written call options in a single note form and are not traded on an exchange. This approach exposes JEPI to counterparty risk if any of the counterparties would go bankrupt. The counterparties mentioned in the prospectus are diversified and well-known names like Barclays, BNP Paribas, Citigroup, Credit Suisse, Goldman Sachs and Royal Bank of Canada.

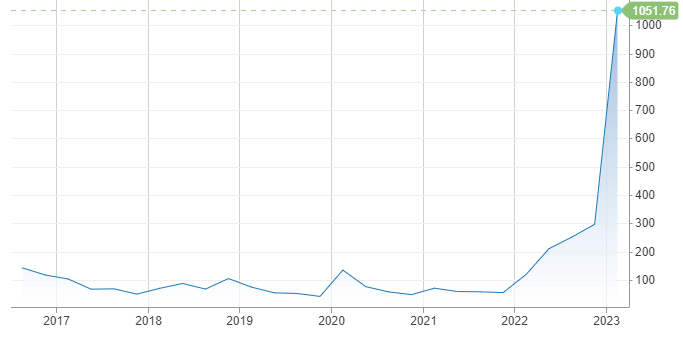

Especially at Credit Suisse the situation looks problematic. The price of the 5 year credit default swap (that insures you against a Credit Suisse default) is skyrocketing.

{kind=link}

We don’t know if JEPI currently has any ELNs outstanding with Credit Suisse as a counterparty. We do know that the counterparty risk is higher than it was say two weeks ago.

For DIVO, the impact of the banking crisis seems limited to the impact on the stock market in general and that impact is rather muted for the time being.

Outlook for covered call ETFs

The banking crisis has also a silver lining for covered calls ETFs: the higher volatility as a result of the crisis translates into higher option premiums and hence higher option income.

Figure 12: VIX Index (CBOE)

Covered call writing is a defensive, low(er) beta, strategy. When the markets rise, you get a nice return. That return will probably lower than the return of the equity markets itself, but that’s something you know in advance.

When the equity markets fall, you outperform thanks to the collected option premiums. Of course, when the market really tanks, you will still have a negative return. That’s why we prefer not to invest in such a strategy when the equity market is in a long term down trend.

{kind=link}

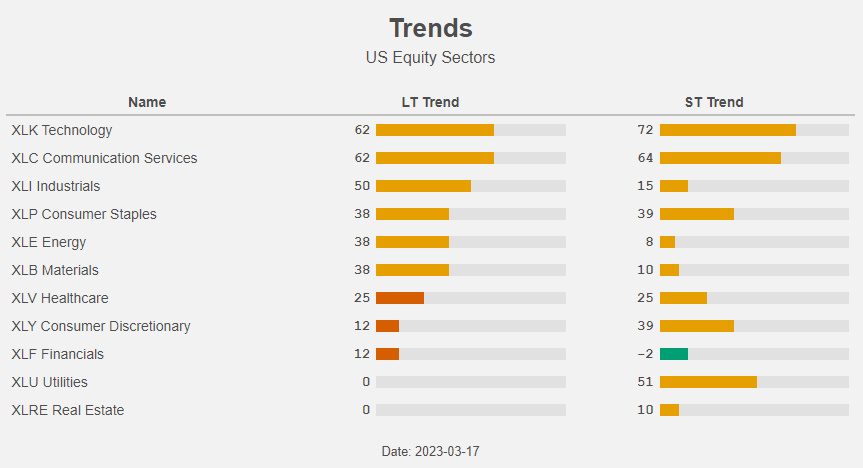

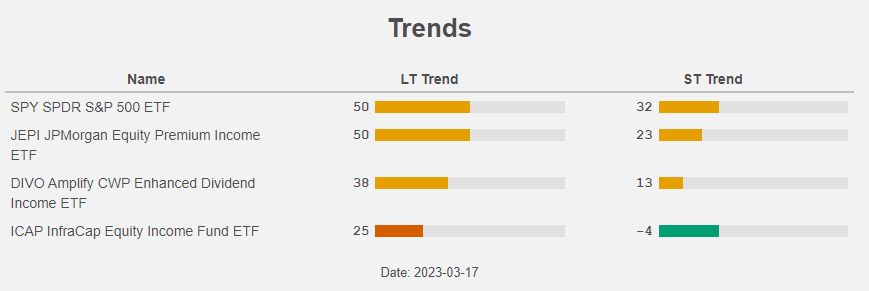

This is currently not the case. The S&P 500 is in a neutral long term trend, as is the case for both JEPI and DIVO. ICAP on the other hand is in a long term down trend.

The current environment with stocks not in a long term downtrend and high volatility is a good backdrop for (genuine) covered call ETFs.

Conclusion

ICAP is much smaller compared to DIVO and JEPI (who themselves are rather “young” ETFs) and we can understand why this is the case. High beta investors are looking for upside potential (and not yield), while income oriented investors prefer a lower beta strategy with high yields. ICAP wants to be both high yield and high beta.

So, no clear strategy, a negative alpha, underperformance when markets are down, high fees: too much negatives to be positive about ICAP. I recommend income oriented ICAP-shareholders to switch to DIVO (or JEPI if you don’t care about the heightened ELN-linked counterparty risk).

DIVO combines the best of both ICAP and JEPI while avoiding the negative points like JEPI’s use of ELNs and ICAPs use of leverage.

For further details see:

ICAP: Too Volatile For Income Oriented Investors, We Prefer DIVO