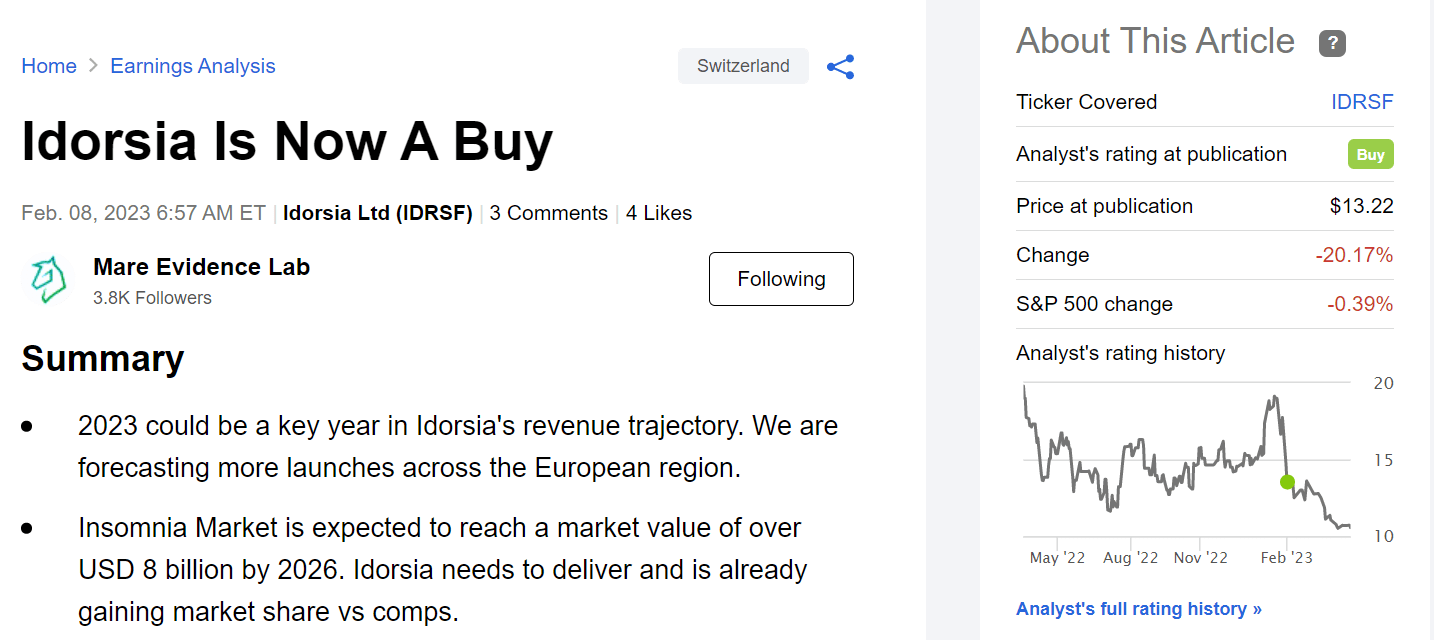

IDRSF - Idorsia: A Trough Year But Long-Term Potential

2023-04-26 11:35:44 ET

Summary

- Idorsia missed top-line sales estimates.

- Only a quarter of liquidity, there was no funding news, and this increased the risk of equity dilution.

- Idorsia confirmed its 2025 financial targets but is lagging behind 2023 sales.

Idorsia ( IDRSF ) just released its Q1 numbers and is down by more than 13%. Since our initial buy rating which was released in early February, the company's stock price is at -20%, and today, we decided to provide a deep-dive.

Mare Evidence Lab's Previous Publication

{kind=link}

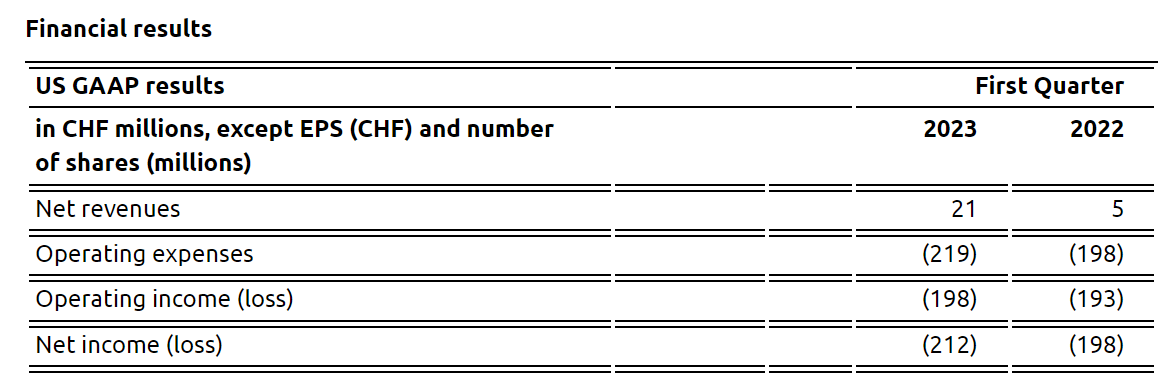

Cross-checking Wall Street analyst expectations, Q1 top-line sales missed consensus by 37%, with key misses for Idorsia's core product (Pivlaz and Quviviq).

Going into detail, Quviviq's turnover was at CHF4.3 million and signed a minus 60% versus the average equity research analysts' expectations. More important to note is the no-growth on a quarterly basis. Indeed, as a reminder, Q4 2022 sales stood at CHF4.2 million. Looking at the detail, US growth continued to be driven by high levels of co-pay assistance, while the other region (such as Italy and Germany) had a slow first-quarter start. On a negative note, given the limited net turnover growth, it will be key to assess how the company's management expects to switch patients from free programs to reimbursed customers. Idorsia petitioned for DORA-class drugs to be eliminated from the Drug Enforcement Administration substances list and this could accelerate sales; however, the timing is unknown.

Related to Pivlaz Q1 sales, the company delivered CHF13.5 million with an average miss of 36%. Turnover declined sequentially on a quarterly basis; however, the management noted that it was due to de-stocking activities. On a positive note, Pivlaz is gaining market share in Japan with 27% of aSAH patients treated in March compared to the 25% cured in December.

Idorsia Financials in a Snap (Idorsia Q1 Press Release)

{kind=link}

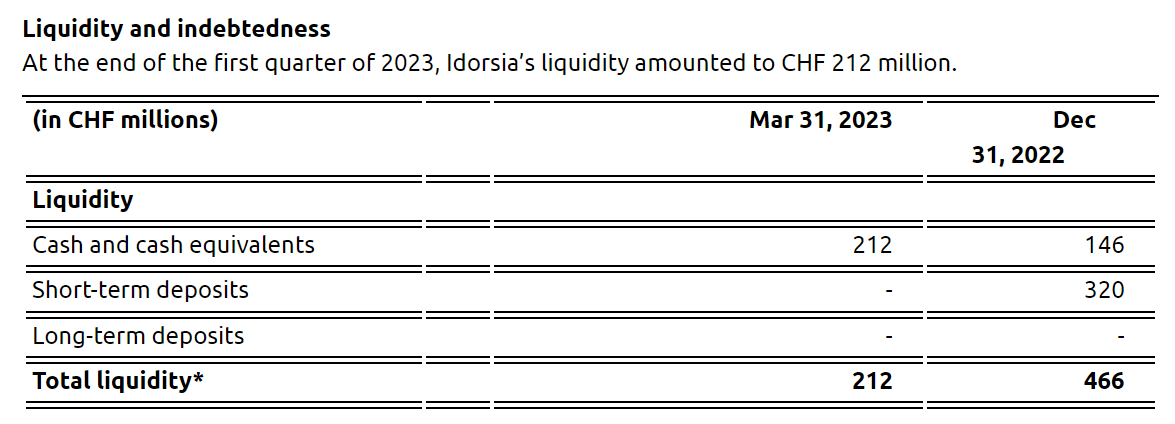

In our initiation of coverage, here at the Lab, we highlighted how our FY 2023 operating loss was set at a minus CHF650 million, and on a quarterly basis, the company was burning approximately CHF200 million. The company's main negative catalyst will be Idorsia future financing options. At December end, cash & cash equivalents stood at CHF466 million and according to our internal estimates, Idorsia had circa three-quarters of liquidity. As a reminder, in January 2023, the company " created 10 million new shares at a nominal value of CHF0.05. This could be used for SBC and fundraising opportunities ".

{kind=link}

In Q1, there was no funding announcement and this increased the risk of equity dilution. With only CHF212 million in liquidity at March-end, there is only a quarter of cash, and in our view, there is some urgency to raise fresh capital. Idorsia confirmed that is continuing to explore non-equity dilutive options and/or equity fundraising. However, we should report that Idorsia actively looked for royalty monetization and/or product out-licensing deals and with these imminent needs, an equity raise looks more likely. Here at the Lab, we assume CHF1.1 billion of funding support before 2026 profitability. Looking at Idorsia's cost, the company's expenses were pretty much in line with our forecast.

Conclusion and Valuation

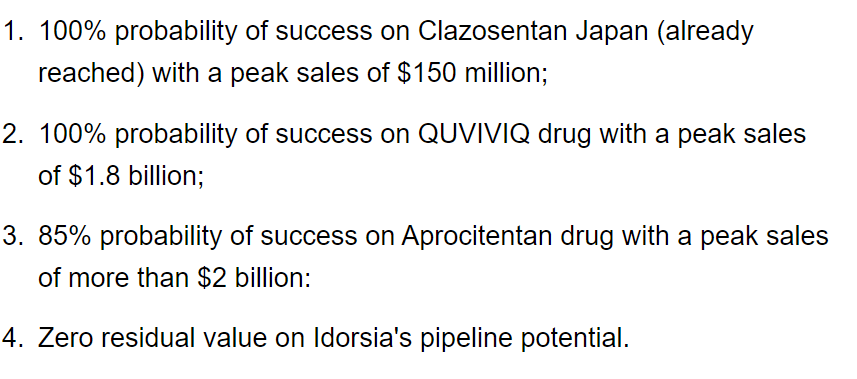

The company reiterated its Fiscal Year 2023 operating loss guidance; however, Idorsia stepped away from its previous top-line sales outlook set at CHF230 million. Despite that, the company continues to emphasize its 2025 financial target (revenue > CHF1 billion and profitability). Cross-checking 2025 consensus estimates, sales are set at CHF719 million. Idorsia is now trading at a depressed valuation, and we still see a solid upside based on the global insomnia market estimated at USD8 billion by 2026 (CAGR of 9%). Quviviq is in a ramp-up phase with more launches across the EU area and is now time for the Swiss region and the UK (after Italy and Germany). As a reminder, Idorsia's CEO has important skin in the game with a 25% equity stake coupled with debt facilities. This is another buy case that supports our investment thesis. Mare Evidence Lab's target price is adjusted with a probability scenario and derived a valuation of CHF15.5 per share. We slightly decreased our previous estimate to reflect slower growth in Idorsia's 2023 revenue. In detail, our price is supported by:

Mare Estimates on Idorsia's Pipeline

{kind=link}

Material (funding) uncertainty continues to be an ongoing concern. As already mentioned, Idorsia's stock price negatively reflects the need for new funding, even if equity dilution is a clear downside risk. On a positive note, the Aprocitentan PDUFA date has been set for the 19th of December 2023.

For further details see:

Idorsia: A Trough Year, But Long-Term Potential