IDRSF - Idorsia: Dilution Risk Causes Downgrade To Hold

2023-06-10 09:22:00 ET

Summary

- Idorsia missed sales expectations by 47% and is urgently seeking funding to avoid equity issuance.

- We have cut our Quviviq sales expectations and pushed out the timeline to profitability to 2026.

- We downgrade Idorsia to neutral with a 12-month target price of CHF7.2 due to time pressure on funding.

Since our latest Q1 update , Idorsia's stock price lost an additional 5.2% ( IDRSF ). As a reminder, the company missed Wall Street expectations for Quviviq's top-line sales by approximately 47%. In addition, as already emphasized in our initiation of coverage, we reported how Fiscal Year 2023 operating loss forecast was set at a minus CHF650 million with a quarterly basis cash burn of circa CHF200 million. Idorsia's " main negative catalyst was its future financing options " and unfortunately the sword of Damocles is still above the company's head.

Mare Ev. Lab previous analysis

{kind=link}

With our publication titled " A Trough Year, But Long-Term Potential ," we suggest holding your investments, and over this week, the company announced key supportive news. Even if, these latest developments are positive, we are incorporating a new base case scenario that is related to the company's quarterly cash burn estimates.

- Following the lower-than-expected revenue generation, Idorsia decided to replace its Chief Commercial Officer. Therefore, Simon Jose will step down and Otto Schwarz will be the new commercial head starting in July 2023. Otto has 35 years of experience in pharma sales and is well-known by Johnson & Johnson and Clozel Family (the two major Idorsia shareholders);

- More important to report is the exclusive negotiations with an undisclosed company on its business activities in APAC (excluding the China region). Looking at the press release, Idorsia will sell its product license in selective territories for a total value of approximately CHF400 million. André C. Muller Idorsia's CFO mentioned that " this prospective transaction would allow the company to realize the significant value and I would expect the completion by July ". This is also subject to regulatory approvals and appropriate due diligence; however, if the deal goes through, this would extend Idorsia's cash runway for almost two additional quarters. This transaction is still pending and as already mentioned by the company, further announcements will be communicated as appropriate. Despite that, at March-end, the company had only CHF212 million in cash so even if the transaction will be concluded, Idorsia still needs to raise new capital. In our calculation, the company will have sufficient liquidity to cover its ongoing expenses by 2023 Q3-end;

- Looking at the company's Annual General Meeting, Idorsia authorized 100 million more shares in equity issuance. As reported by the management team, this is the last resort; however, we should now include this dilution optionality in our calculation. Even if the management continues to prioritize licensing and royalty monetization for financing, we are now assuming dilution from 100 million new stocks at a 10% discount to the current price (CHF8). If this happens, as a worst-case scenario, we would assume an equity raise of CHF800 million and cut our 12-month target price to CHF7.2 per share.

Change in our Estimates

During the AGM, Idorsia pulled back its 2023 top-line sales guidance, confirming the operating loss and reaffirming its 2025 profitability target. In our forecast, we lowered:

- Quviviq sales from CHF95 million to CHF65 million. This is due to lower Q1 sales. Despite subsidies, the US ramp-up is continuing, but Idorsia needs to outperform the branded insomnia market (and is unlikely with the changes in the Chief Commercial Officer). Therefore, we are reducing US and EU sales;

- The company should work on cutting operating expenses. However, we make limited changes in the 2023 net loss. In our estimates, our profitability targets are now set for 2026 and our cash burn to profitability moved from CHF1.1 billion to CHF1.5 billion;

- Still related to point 2) we now assume 10 million lower non-GAAP SG&A cost at CHF500 million and CHF40 million savings in R&D at 325 million. For this reason, we have an operating loss in 2024 and 2025. Here at the Lab, we still do not forecast Non-GAAP operating profitability until 2026;

-

Related to point one, beyond 2023, we also forecast a reduction of approximately 25% for Pivlaz and Quviviq's top-sales trajectory.

Conclusion and Valuation

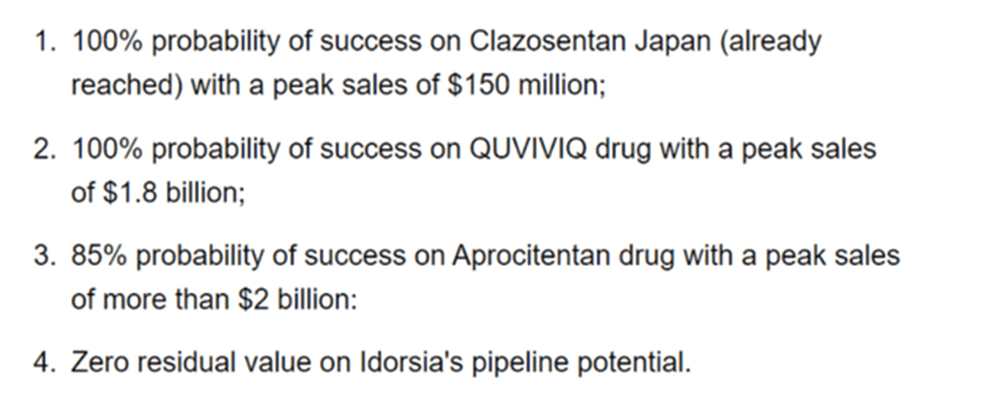

Here at the Lab, assuming a dilution risk, in our base case scenario, we are still supportive of the Idorsia drug portfolio and its future net present value on the company's late-stage assets (Fig below).

This is already taking into consideration lower pick-up in sales (given Q1 performance) and a lower cost basis. However, our Quviviq sales reduction is only partly offset by cutting OpEx. Therefore, our target price falls to CHF7.2 per share.

Mare Estimates on Idorsia's Pipeline

{kind=link}

As a consequence, on a twelve-month estimate, we decided to move our rate from Overperfom to Neutral given Quviviq's sales lack and time pressure on funding. Despite that, management remains confident in the long-term prospect, and they do have a solid track record with skin in the game (both at the equity level as well as at the debt level). Whilst Idorsia's recent licensing monetization news was limited, we believe that Pivlaz would be approximately valued at a multiplier of 5/6x on 2023 sales. This provided the necessary support for Idordia's asset quality. However, clarity on funding with royalty monetization and licensing agreements poses serious risks. Therefore, we suggest to remain neutral on the short-term horizon.

Downside risks to consider are clinical trial failures, higher marketing expenses, higher R&D costs, and lower sales trajectory with commercialization challenges. In addition, the company may struggle to gain reimbursement. On the upside, 1) Quviviq could exceed our base-case sales forecast thanks also to strong reimbursement negotiations, 2) a new license monetization that might extend Idorsia's cash burn beyond Fiscal Year 2023, and 3) other pipeline success.

For further details see:

Idorsia: Dilution Risk Causes Downgrade To Hold