IDRSF - Idorsia Is Now A Buy

Summary

- 2023 could be a key year in Idorsia's revenue trajectory. We are forecasting more launches across the European region.

- Insomnia Market is expected to reach a market value of over USD 8 billion by 2026. Idorsia needs to deliver and is already gaining market share vs comps.

- Idorsia's pipeline is not priced in. With the late-stage pipeline coupled with Idorsia's revenue stream, Wall Street is too much discounting the Swiss player.

Here at the Lab, we decided to initiate coverage of Idorsia ( IDRSF ) with a buy rating and CHF 16 target price. The Swiss company is a clinical-stage biotech player specializing in small molecule development with state-of-the-art facilities, experienced management teams with a solid track record, and a pipeline not fully priced in. Recently, Idorsia was penalized by the market for Clazosentan P3 clinical failure in a study called REACT, as well as by the recent announcement on the Fiscal Year 2022 release.

Starting with the negative news, here are our main key takeaways:

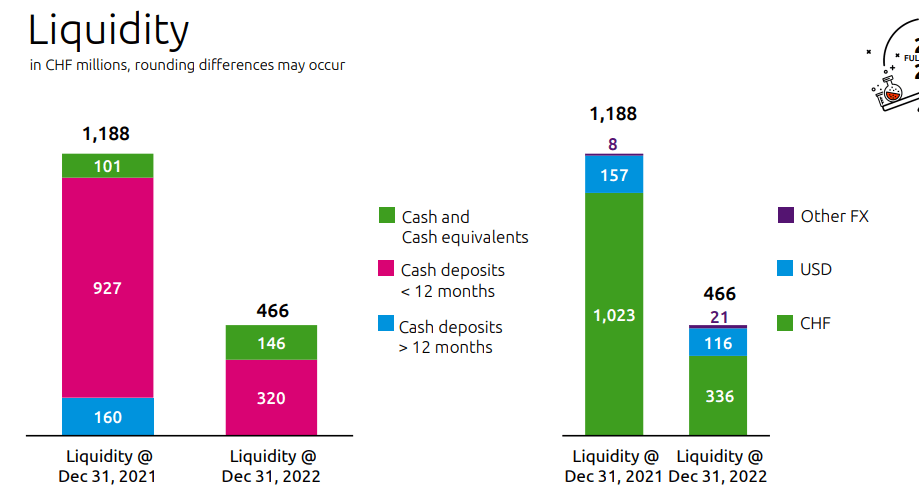

- The company cash & cash equivalent was at CHF 466 million, compared to CHF 695 million at September end. As a reminder, last year, Idorsia's cash position was over CHF 1 billion (Fig 1). According to our internal estimates, this is not coming as a surprise; indeed, even in the current fiscal year, we are expecting an operating loss of CHF 650 million, which is very much in line with management's latest indication. What we didn't like was the latest CEO indication on capital raise, he specifically said that Idorsia continues " to carefully weigh our funding options, including non-equity dilutive opportunities ". During 2022, Idorsia previously declared that non-equity dilutive opportunities were not an optionality. This change in communication was not very well appreciated by the market and Idorsia's stock price is down by almost 9% at the time of writing. Here at the Lab, considering the expected operating loss, we were already guiding for near-term funding. During the Q&A, we should note that the CEO reported

non-equity dilutive remains the company's preference optionality;

- Still related to equity dilutive opportunities , in January, Idorsia created 10 million new shares at a nominal value of CHF 0.05. This could be used for SBC, but also for fundraising opportunities, confirming the above negative comment;

-

As anticipated, yesterday, the company released a follow-up note on Clazosentan P3 clinical failure. This news is coming as a negative surprise; however, our internal estimates have always been very minimal on Idorsia numbers. In detail, we were forecasting a 70% chance of success with a sales peak of $125 million in sales (and a value of CHF 0.5 per share). Here at the Lab, we do not expect a meaningful impairment on Clazosentan; what is interesting is the fact that the drug was already approved in Japan to treat delayed cerebral ischemia (in March 2022). However, the regulators required an additional important endpoint and Clazosentan failed. Based on our indication, there is a limited implication for Clazosentan ex-Japan. As already mentioned by the company, Idorsia " will fully analyze the efficacy and safety data to understand this unexpected result";

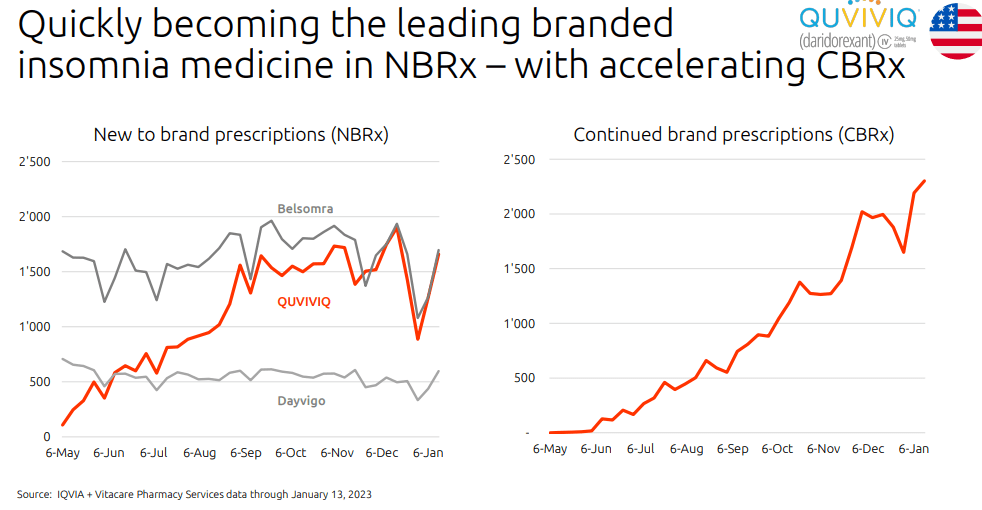

- Going to the P&L analysis, Quviviq sales continue to lag. Q4 turnover was below Wall Street analyst expectations; however, this was negatively influenced by 30 days of treatment free for new patients. Idorsia reported CHF 4.2 million, while consensus was forecasting CHF 7.7 million;

- Stock-based compensation was the main driver of the discrepancy between GAAP and Non-GAAP results. In the Q&A, we understood that this will be limited in the current Fiscal Year 2023.

{kind=link}

Source: Idorsia Q4 and FY 2022 results presentation

Our supportive investment thesis is based on the following:

- Starting with some interesting data, the global insomnia market is expected to grow significantly over the next years, driven by factors such as the increasing prevalence of insomnia, raising awareness about the disease, and advancements in the field of sleep disorders management. In 2020, the global insomnia market was valued at approximately USD 4.3 billion and is expected to reach a market value of over USD 8 billion by 2026, growing at a CAGR of around 9% during the forecast period. Europe and North America are expected to hold a significant share of the market, while the Asia-Pacific region is projected to witness the highest growth rate;

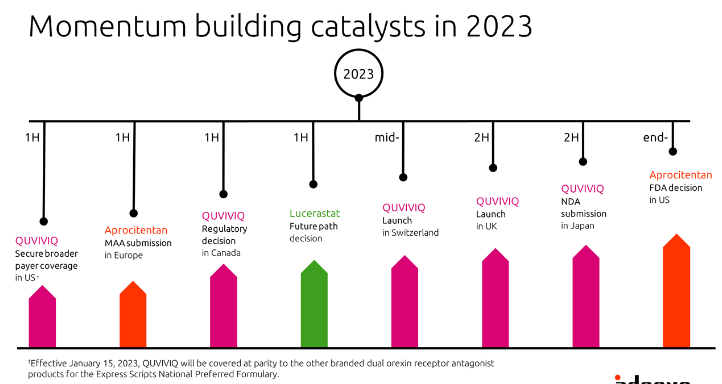

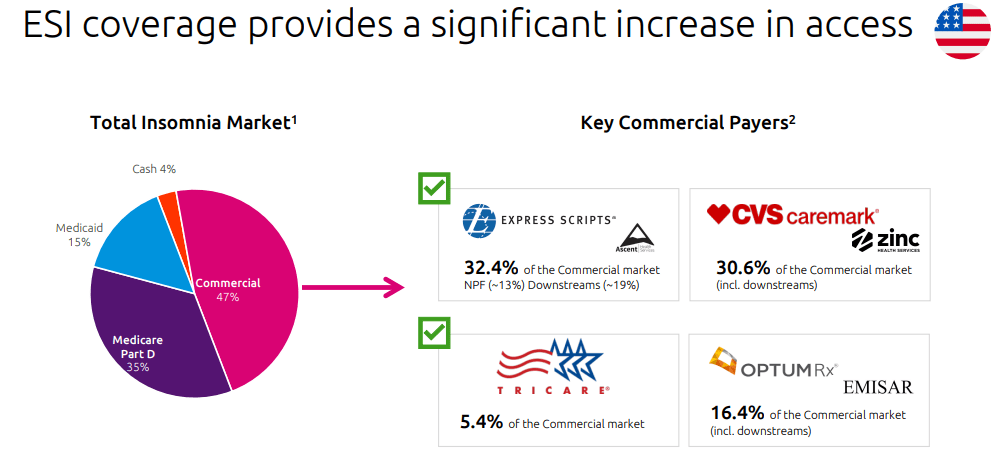

- Related to point 1), thanks to QUVIVIQ, since May 2022 Idorsia reached net sales of CHF 6.5 million, started its commercial activities in Italy and Germany, and prepared more launches across the European region (Fig 1). In detail, the Swiss market is expected to start in mid-2023, followed by the UK in the 2023 second half, and then France and Spain. Aside from the great sales starts, it is key to emphasize the ESI reimbursement deal signed in January 2023 (Fig 2) that will boost its sales trajectory;

- All in all, Q4 2022 top-line sales reached CHF 54 million, beating consensus estimates by more than 40% at the aggregate level. However, this positive outcome was primarily delivered by Hainan Simcere's new contract. In detail, Idorsia reached a licensing agreement for the Chinese market by signing a contract worth CHF 28 million. Despite that, excluding this positive one-off, sales were above CHF 5 million versus Wall Street estimates;

- Still related to our sales analysis, Pivlaz drug continues to see a strong market penetration. Pivlaz sales were broadly in line with consensus, with 95% of target accounts having ordered Pivlaz by 2022 end;

- Going down to the P&L, operating expenses stood at CHF 234 million and were lower than the consensus at CHF 263 million. In 2022, on the human resources total headcount, Idorsia created 185 new positions from 1.176 to 1.361;

- More important to report is the fact that Idorsia guided 2023 net revenue at CHF 230 million and adj (non-GAAP) operating loss at CHF -650 million. In addition, the company left unchanged its 2025 financial targets, expecting to reach >CHF 1 billion in global sales supported by a sustainable profit. Cross-checking the Wall Street forecast, here at the Lab, we note that the average consensus is forecasting a net loss of more than CHF 250 million in 2025.

QUVIVIQ launches across the EU

{kind=link}

Fig 1

{kind=link}

Fig 2

Idorsia is gaining market share vs comps

{kind=link}

Fig 3

Conclusion and Valuation

Regarding the company's valuation, we decide to derive our target price based on the sum-of-the-parts Net Present Value of the company's late-stage assets, adjusting our consideration with a probability scenario. Our valuation is derived from a DCF model with a 10% discount rate. In detail, our price is supported by:

- 100% probability of success on Clazosentan Japan (already reached) with a peak sales of $150 million;

- 100% probability of success on QUVIVIQ drug with a peak sales of $1.8 billion;

- 85% probability of success on Aprocitentan drug with a peak sales of more than $2 billion:

- Zero residual value on Idorsia's pipeline potential.

For further details see:

Idorsia Is Now A Buy