IDRSF - Idorsia: The Market Has Overreacted

Summary

- Idorsia reported the yearly results for 2022 with some very positive developments, while also discussing important risk factors.

- Clazosentan will not see the US and the EU market but could be allowed in other Asian countries.

- QUVIVIQ continues to penetrate the commercial market in the US and had a good start in Europe, while 2023 will likely see a ramp-up in sales.

- Idorsia’s liquidity problem will be solved soon and the management continues to prefer non-dilutive options while not excluding partial equity funding.

- My very conservative valuation model is now considering the extreme case of the additional liquidity fully sourced by dilutive equity funding, which is still leading me to rank Idorsia as a buy.

A quick look at the recent events

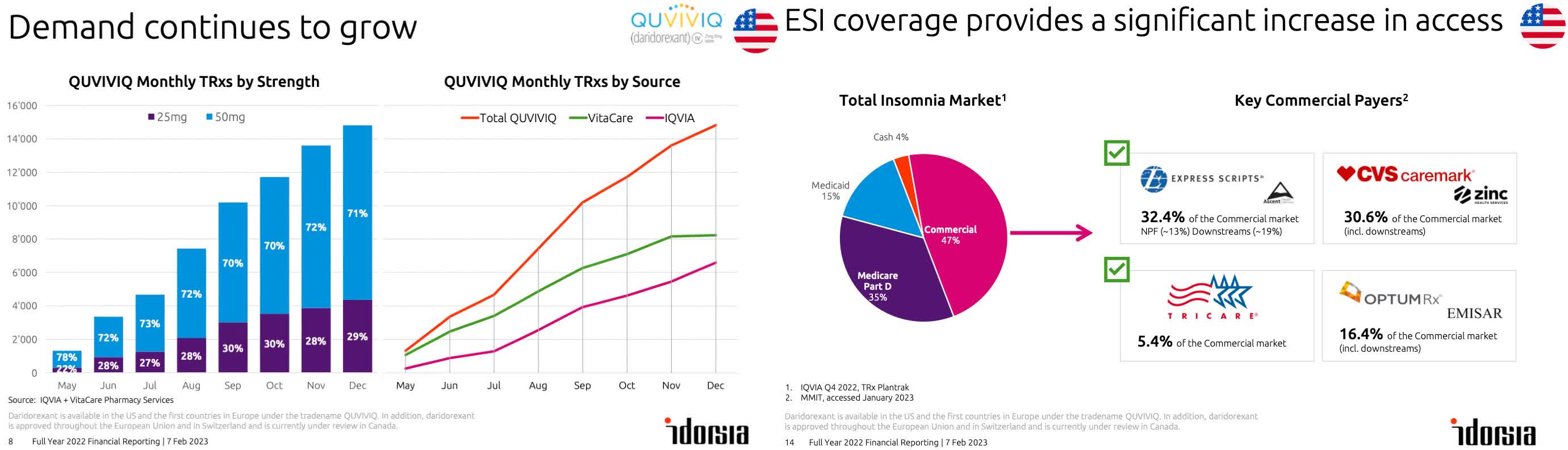

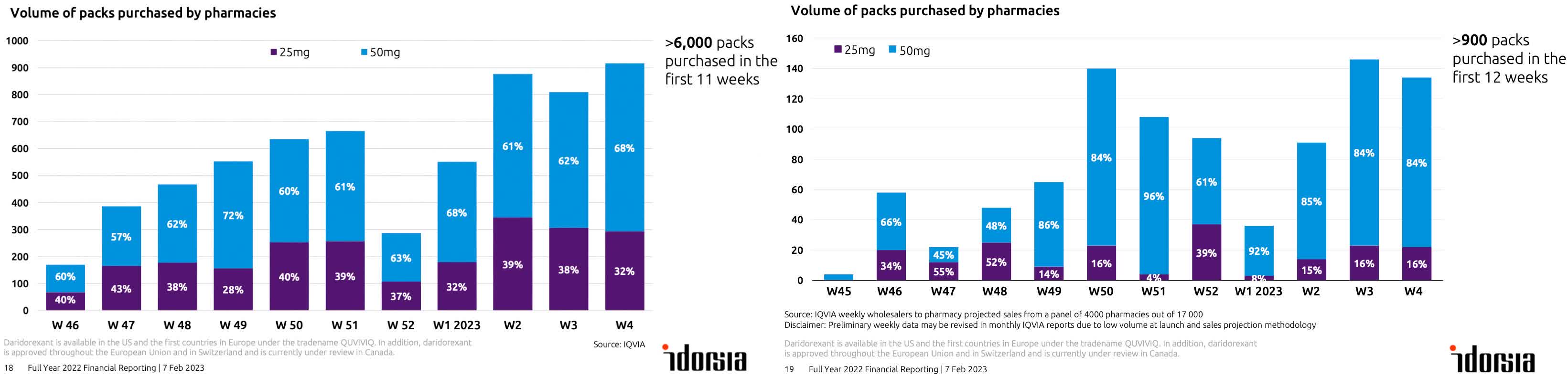

On February 6, 2023, Idorsia Pharmaceuticals Ltd (IDRSF) reported the failure in the Phase 3 study REACT for its promising compound Clazosentan. The study did not meet the primary endpoint. A big disappointment that resulted in the abandonment of the commercial plans for this compound in the USA and Europe. The next day, the company announced the financial results for 2022. Clazosentan, which is sold under the name PIVLAZ in Japan, was able to achieve sales of CHF 44M since its launch in April 2022, while only about 25% of aneurysmal subarachnoid hemorrhage [aSAH] patients are treated with it until now. QUVIVIQ generated CHF 6.5M in net sales since its launch in May 2022 in the US, and since November in Germany and Italy. Although the sales of QUVIVIQ could seem disappointing, the data isn't reflecting the real dispensed volume in the US, due to running coupon and co-pay programs. On January 15, 2023, QUVIVIQ has been added to the Express Scripts National Preferred Formulary, gaining access to approximately 22M people, representing around 13% of the potential commercial market, while the company is negotiating the terms with other important commercial actors, to gain a broad commercial coverage in the US.

{kind=link}

In Europe, the drug has been reportedly off to a good start in Germany and Italy, and Idorsia is preparing the launch in other countries this year.

{kind=link}

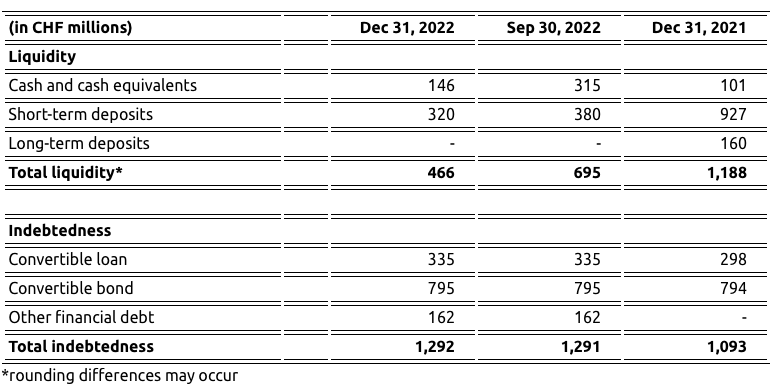

The company disclosed its guidance for 2023 with non-GAAP net revenue of CHF 230M and a declining operating loss of approximately CHF 650M while confirming its commitment to reach sustainable profitability in 2025, with global revenue above CHF 1B. But the big question mark remains around its financing plan for the coming years, as the company reported CHF466M in liquidity at the end of the last fiscal year, and is projected to consume CHF 880M in operating expenses during the current year.

{kind=link}

Overall the full-year results have exceeded the company's guidance while the company was able to reduce its estimated operating expenses. The start of QUVIVIQ may seem disappointing, but I am confident once the commercial channels are ready, sales will experience a very positive momentum in the US and sequentially also in Europe.

Valuation

Following the recent events and the continuous developments, I updated the street estimation set, my projections, as well as the respective valuation models.

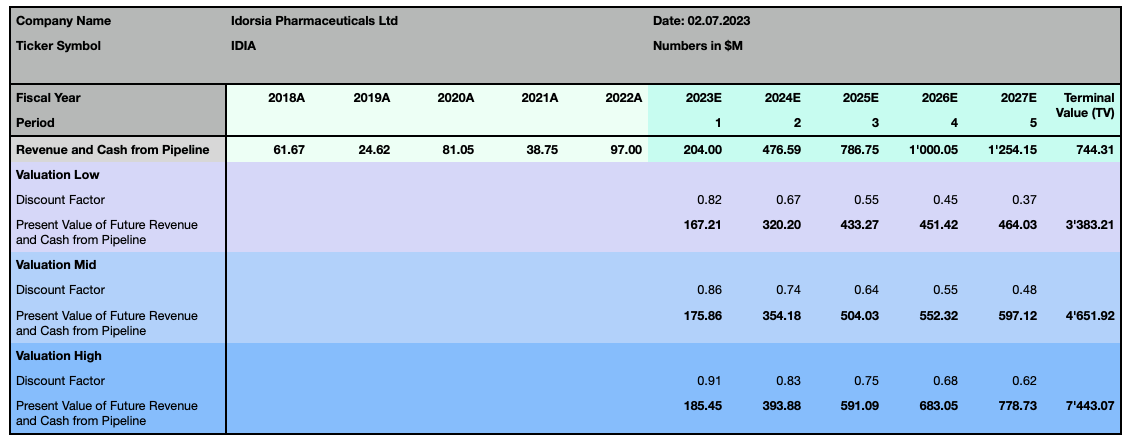

Author, using own estimations and data from S&P Capital IQ

Both estimation sets are now significantly lower than those discussed in my former valuation , published on August 24, 2022; reflecting the slower sales ramp-up with QUVIVIQ, and excluding Clazosentan from the rest of the world, while also adjusting its sales projections in Japan. Although PIVLAZ could likely be allowed in other markets in Asia, based on the Japanese Phase 3 study results, I don't consider it in my projections.

It's important to note that both estimation sets are more pessimistic than the company's target for 2025, while still probably seeing the company breaking even during that year, but not reaching the CHF 1B mark in sales until 2026. My estimations continue to be significantly more cautious than those reflecting the street consensus, although some analysts could further adjust their targets in the coming weeks. I also underscore that my revenue estimations include milestones and royalties payments, and for reducing the complexity of the modelization, I assume them to be spread over the years in a way that may not reflect reality and this can lead to anticipated or postponed revenue streams over the years of my estimations.

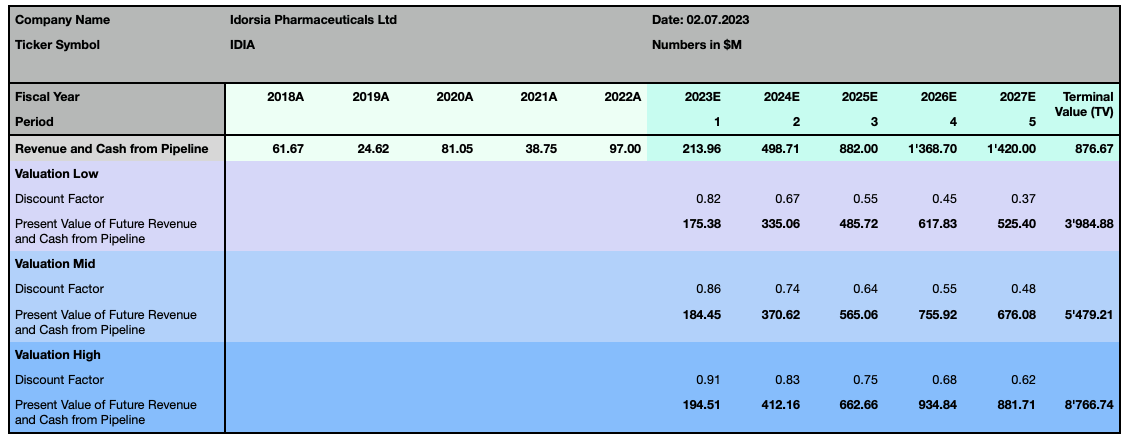

Bearing in mind the complexity of Idorsia's pipeline with 11 compounds in different development stages as well as its partnership agreements, I chose to reduce this complexity and provide a Discounted Cash Flow [DCF] valuation based on very basic assumptions and avoid further distortions, considering the already low visibility.

{kind=link}

In the latest webcast, the management confirmed preferring non-dilutive funding options, while not excluding equity dilutive funding and underscoring convertible bonds being highly unlikely in the actual market conditions. Considering the actual liquidity, the projected income, and operating expenses, I estimate the company's additional liquidity needs to be around CHF 700M through 2025. To be even more cautious in my valuation approach, compared to the method used in my last articles, I now consider not only the full potentially issued shares as the base for the fair stock price calculation, but I even consider the additional liquidity fully sourced by equity dilutive funding, which I quantify roughly with 25% increase in total shares considered in my valuation model.

I value different scenarios based on the estimated likelihood and the discount rate commonly applied in biotechnology or pharmaceutical DCF valuations for companies with mid-stage pipelines. I also assume zero perpetual growth rate as this is in my opinion more reasonable for Idorsia at this stage.

Author

I proceed by substituting my forecasted estimations with the average market estimations in my valuation model by maintaining the same model assumptions.

Author, using data from S&P Capital IQ Author

{kind=link}

Considering the likelihood of the different scenarios, the valuation based on my estimations is still over 16% more conservative than the valuation based on the forecasted street consensus, with a price target of CHF 19.08 or $20.61 for my estimation set, and of CHF 22.86 or $24.69 when considering the data of the analyst's consensus. However, both models underscore how significantly Idorsia's stock price is undervalued, even when considering an equity dilutive funding of CHF 700M. This valuation is pricing in the full dilution of the share price through the exercise of equity derivatives and equity instruments reported at the end of 2022, which is, in my opinion, rather unlikely, but gives an insight into a very conservative approach in terms of fair valuation of the stock price.

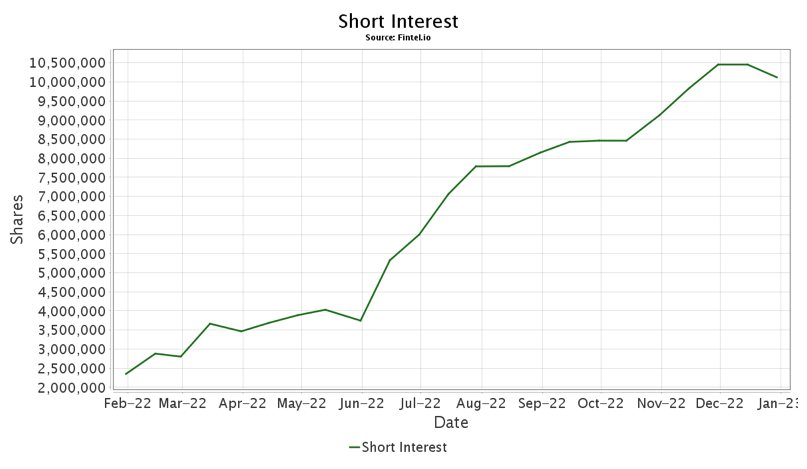

The short interest in the stock listed in the US has reached new record levels with over 10M shares sold short, exponentially increasing during the past year.

{kind=link}

The most recent sell-off has pushed back the stock to price levels not seen since September 2022. While the recent negative events may have led many investors to lose patience and sell their positions, it's worth mentioning that the pressure from short selling has been consistently strong and that this may lead to an overreaction on negative days, such as the last few market sessions, while the stock could significantly recover as soon as the short-selling pressure decreases.

The bottom line

Idorsia's pullback has been triggered by the failure of Clazosentan's Phase 3 study, the rather slower start of QUVIVIQ's sales, and further pressure coming from the uncertainty around the company's funding for reaching its profitability target in 2025. My adjusted valuation model considers all those negative elements and goes even further by assuming a very unlikely fully equity dilutive financing option. The stock has been oversold and is now hovering at levels reflecting panic selling and high uncertainty. At this price the stock offers massive upside potential, even when considering my very conservative assumptions, leading me to continue ranking Idorsia as a buy position based on the discussed fundamental data.

For further details see:

Idorsia: The Market Has Overreacted