URTH - IGA: Trading At A Discount For A Very Good Reason

2024-01-01 06:33:12 ET

Summary

- Voya Global Advantage and Premium Opportunity Fund offers a high level of income through its portfolio of equities and dividend-paying stocks.

- The fund's recent performance has been disappointing, with a declining share price over the past three and five years.

- The fund's distribution history shows declining distributions and net assets, raising concerns about its ability to sustain its current yield.

- The fund might perform reasonably well in a weak market due to the options strategy, but there is no guarantee that will be the case in 2024.

- The fund is trading at a massive discount on net asset value, but the fact that net asset value has been declining for eighteen months explains this.

The Voya Global Advantage and Premium Opportunity Fund ( IGA ) is a closed-end fund that can be employed by investors who are seeking to earn a very high level of income from the assets that are contained in their portfolio. The fund's current 9.25% yield is a testament to its general success in the provision of income, although this is not nearly as high as some of the other closed-end funds that are currently available on the market. In particular, some of the better fixed-income funds can beat this one in terms of yield. However, investing in fixed-income generally requires investors to sacrifice much of the upside potential of equities, since equities theoretically can appreciate indefinitely but fixed-income securities cannot go up to the point where their yield-to-maturity goes below zero since nobody will ever buy such a security. The Voya Global Advantage and Premium Opportunity Fund invests in equities, so investors still have exposure to some of the upside potential, although this fund's strategy does require the conversion of some of the upside potential into current income. That may reduce the fund's appeal in the eyes of some investors.

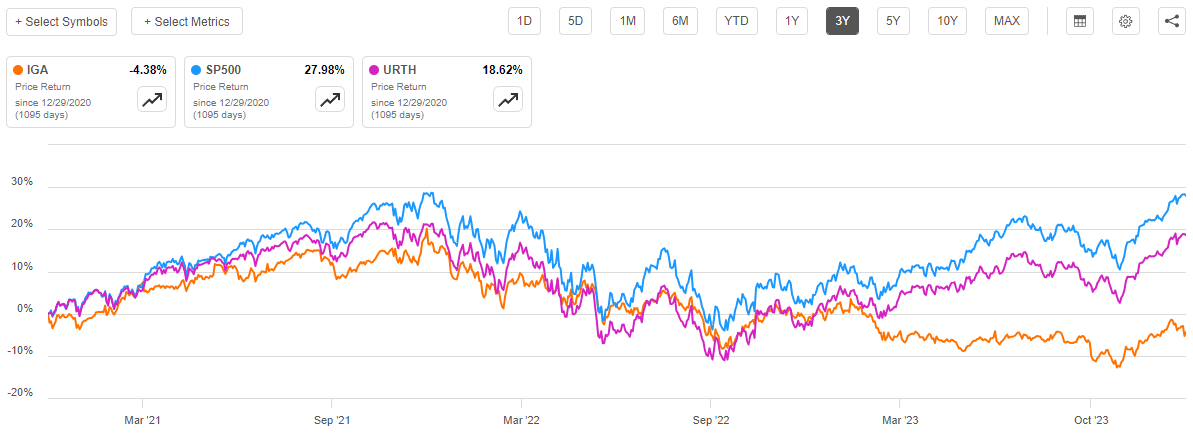

Unfortunately, the recent performance of the Voya Global Advantage and Premium Opportunity Fund has not been particularly impressive. Over the past three years, shares of the fund are down 4.38%. This is much worse than the 27.98% return of the S&P 500 Index ( SP500 ) or the 18.62% return of the MSCI World Index ( URTH ):

{kind=link}

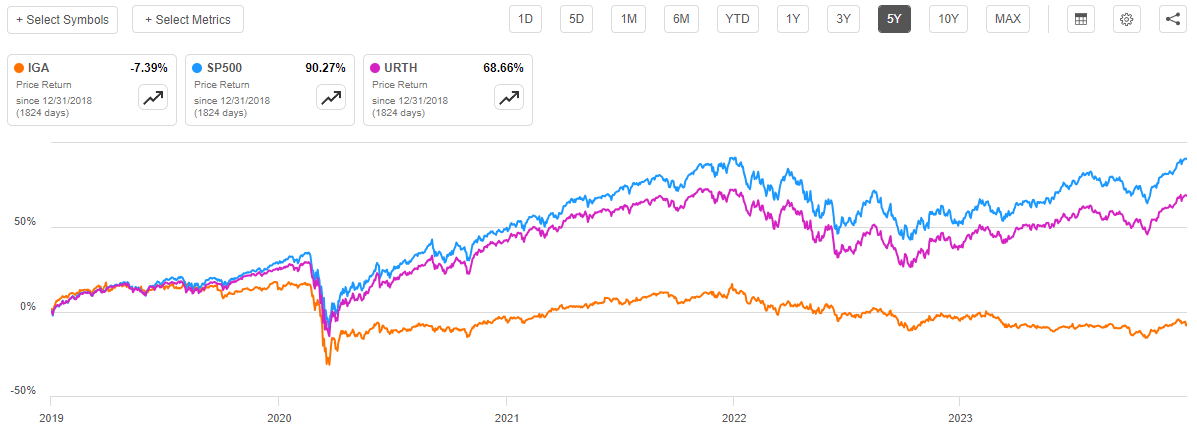

Things do not get any better for the fund when we look at its performance over a longer period of time. The fund's share price is down 7.39% over the past five years, which compares very poorly with either of the indices:

{kind=link}

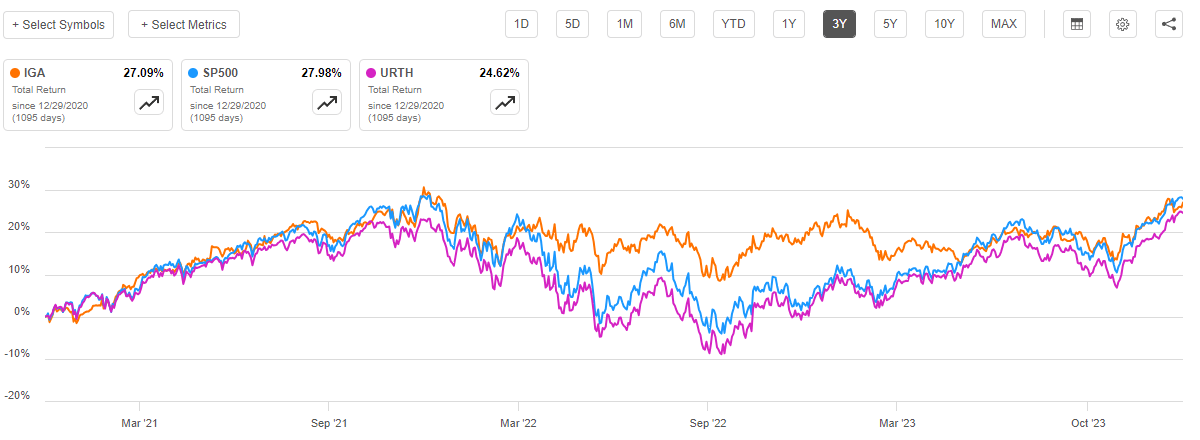

However, as I have pointed out in numerous previous articles, the basic business model of closed-end funds is to pay out the majority of their investment income to the shareholders. This typically results in the fund having a much higher yield than most broad-market indices. This is certainly the case with the index, as neither the S&P 500 Index nor the MSCI World Index yields anywhere close to 9.25%. As such, it is prudent to include the fund's distribution in any analysis of its results. When we do this, the Voya Global Advantage and Premium Opportunity Fund delivered a total return that was almost identical to the S&P 500 Index over the past three years:

{kind=link}

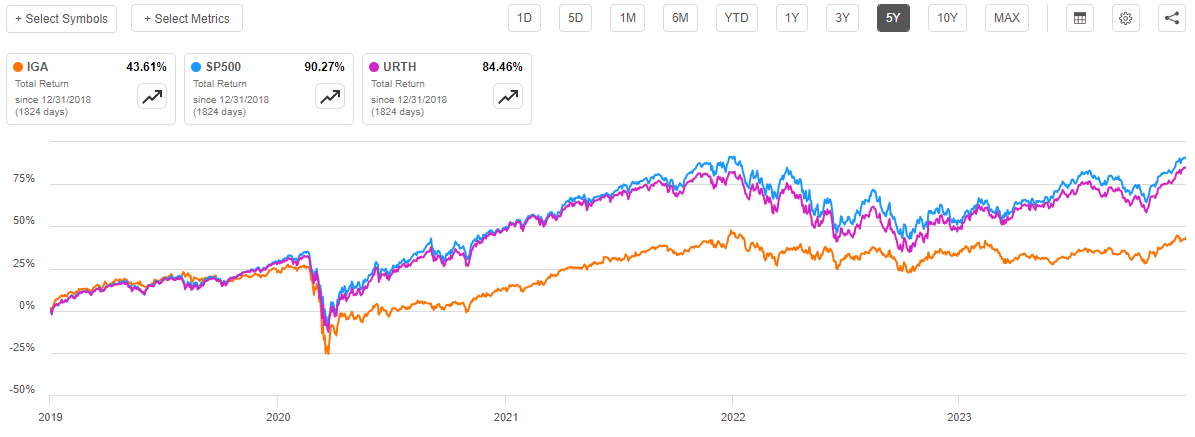

The fund managed to accomplish this very similar performance with considerably less volatility than either of the two indices. Unfortunately, it falls far short of the indices over the trailing five-year period:

{kind=link}

This could suggest that the Voya Global Advantage and Premium Opportunity Fund is a good holding if you are concerned about market volatility or even a near-term decline in equities. However, it will underperform during very strong bull markets. This is exactly what we would expect given the fund's basic strategy, and as such, any decision about whether or not to add it to your portfolio depends on your views of the forward-looking direction of the market and your overall goals.

About The Fund

According to the fund's webpage , the primary objective of the Voya Global Advantage and Premium Opportunity Fund is to provide its investors with a very high level of current income. This is a bit strange, considering that this fund invests primarily in common equities. As we can see here, fully 97.47% of the fund's assets are invested in common equities. The only other type of securities in the portfolio is a small allocation to cash, which is presumably invested in a money market fund:

CEF Connect

The reason why the fund's focus on current income is a bit strange is that equity securities tend to be very poor at the provision of income. As of the time of writing, the S&P 500 Index ( SPY ) only yields 1.40% and the MSCI World Index yields 1.70%. That means that a $1 million investment in either index will yield less than $20,000 annually. That is certainly nothing to write home about, and it is certainly nothing to brag about at a holiday meal. The fund could theoretically sell a bit of its stock every year to provide its investors with a substantial distribution yield, but that is still considered realized gains and it is very unreliable. After all, the stock market does not always go up.

In a recent article , I pointed out that there are some equities that do pay higher yields. There are certainly some that have yields above the current 5.5% or so that can be obtained by simply putting your money into a money market fund. However, these stocks are generally going to be in one of a handful of sectors (typically energy or industrials) and they have much smaller market caps than the mega-cap technology stocks that dominate both the S&P 500 Index and the MSCI World Index. Those mega-cap technology stocks drag down the yield of the broad market indices. This is easy to see simply by looking at the yields of some of the single-sector index funds relative to the S&P 500 Index. In short, though, this fund could be attempting to earn some income by focusing its attention on these individual high-yielding stocks as opposed to simply buying the same handful of stocks that every other closed-end fund buys.

A look at this fund's holdings does indeed reveal that it is certainly doing this to a degree:

Voya

Here are the yields of each of these securities:

| Company |

| Current Yield |

| Johnson & Johnson ( JNJ ) |

| 3.04% |

| Merck & Co. ( MRK ) |

| 2.83% |

| AbbVie ( ABBV ) |

| 4.00% |

| PepsiCo ( PEP ) |

| 2.98% |

| Procter & Gamble ( PG ) |

| 2.57% |

| iShares Russell 1000 Value ETF ( IWD ) |

| 2.02% |

| Cisco Systems ( CSCO ) |

| 3.09% |

| Verizon Communications ( VZ ) |

| 7.06% |

| Amgen ( AMGN ) |

| 3.12% |

| Philip Morris International ( PM ) |

| 5.53% |

As we can clearly see, each of these stocks has a significantly higher yield than either of the two primary broad-market indices that we have been using to track this fund. I will admit that this is not exactly what I expected to see, as it is difficult to see any real difference between this fund and the Voya Global Equity Dividend and Premium Opportunity Fund ( IGD ) that we discussed last week. This is surprising because this fund does not specifically state that it invests in dividend-paying equities like its sister fund states. From the fund's website:

Vota

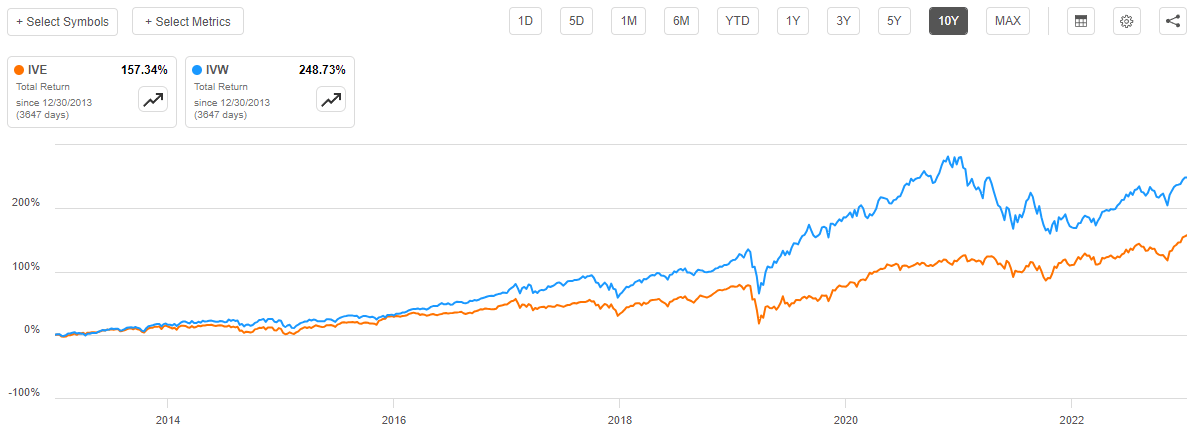

This one does not specifically state that it invests in dividend-paying stocks. However, it still writes index call options. As such, I would have expected to see significant exposure to the "Magnificent 7" stocks that have accounted for much of the total return of the S&P 500 Index over the past decade. After all, if the fund is writing index options without actually holding the index, then it is asking for trouble if the underlying portfolio does not deliver a similar performance to the index. As everyone reading this is likely aware, dividend-paying value stocks have generally underperformed the S&P 500 Index by a lot over the past ten years. For example, here is the total return performance of the iShares S&P 500 Value ETF ( IVE ) against the iShares S&P 500 Growth ETF ( IVW ) over the past ten years:

{kind=link}

As we can see, growth stocks substantially outperformed value stocks over the period. Thus, if the fund is writing options against the major indices, it seems quite possible that the portfolio will not be able to keep up sufficiently to avoid having call options exercised against it and exposing the fund to losses.

With that said, this fund is not writing options on the S&P 500 Index or the MSCI World Index. The fund's semi-annual report lists the following option contracts written as of the end of August:

{kind=link}

A few of these are broad-market indices, such as the FTSE 100 or the Nikkei 225. These are only single-country indices though, and they are not often followed by American investors. We also see Consumer Staples and Industrials index options here. These are both value indices, as nearly every company in one of those two sectors is a value stock. This actually makes the fund's portfolio start to make a lot more sense, as its holdings should at least exhibit similar movements to these options and help offset the fact that the fund is not actually holding the indices.

This is something that sets this fund apart from Eaton Vance's option-income funds which tend to be fairly popular holdings among investors who are looking for a closed-end fund that employs options. Those funds generally write options against the S&P 500 Index and their holdings tend to reflect that. In particular, the Eaton Vance funds have substantial exposure to the "Magnificent 7" stocks and the other large American companies that we tend to find among the largest positions of any domestic equity fund, or indeed even most global funds that do not specifically exclude the United States. The Voya Global Advantage and Premium Opportunity Fund is holding very different holdings from many other similar funds from other fund houses, and this could be appealing to those investors who are looking to improve the diversification of their portfolios. After all, if every fund in our portfolios is invested in the same dozen stocks or so, all of which come from the technology sector, we do not really have much diversification at all even if there are twenty funds in our portfolios.

As I have pointed out in numerous previous articles, one of the biggest problems that most American investors have today is that they are overly exposed to the United States. This is an especially big problem for Americans because their income is also exposed to the American economy, so a domestic problem could both reduce their savings due to a stock market decline and wipe out their incomes. Thus, it is important to have a certain amount of international diversification in a portfolio to reduce your exposure to any individual nation.

As we saw earlier, the Voya Global Advantage and Premium Opportunity Fund specifically states on its webpage that it invests in stocks from around the world. The fund's name suggests the same thing. However, the fund is very heavily weighted towards the United States:

Voya

The United States accounts for just under a quarter of the global gross domestic product. As such, this fund is substantially overweighted to this country based on its actual productive output. However, that is not just a problem with this fund, as the MSCI World Index has a 69.70% weighting to the United States. This is actually a pretty big reason why so many investors are going to be overweight to this nation, as the United States markets have substantially outperformed those of any other nation since the Great Financial Crisis and the 2009 recession. As such, any investor who was not actively taking their profits and investing overseas is now going to be substantially overweight to this nation.

This is somewhat disappointing, as this is a sign that the fund may not be as good at reducing American exposure as we might like to see. The fund's focus on value stocks might still be advantageous for those investors who have overexposure to growth right now, but this fund cannot serve as a "one-stop shop" for obtaining the necessary international exposure to protect you against regime risk or domestic economic problems. For that, it is important to pair this fund with one that specifically excludes the United States.

Distribution Analysis

As mentioned earlier in this article, the Voya Global Advantage and Premium Opportunity Fund has the primary objective of providing its investors with a very high level of current income. In order to achieve this objective, the fund invests in a portfolio that consists of dividend-paying stocks from around the world. The fund then writes call options against indices and index exchange-traded funds with the objective of receiving the premium from the option sale and then having the option expire worthlessly. This can result in fairly respectable synthetic dividends from the indices against which options are being written if the fund is reasonably successful at ensuring that it does not get too many options exercised against it. The dividend-paying stocks that are held by the fund have higher yields than the major indices, which provides an additional source of income for the fund. Finally, the fund has the ability to realize capital gains if the stocks in the portfolio appreciate in a friendly market. The fund pockets all of the money that it obtains through these operations and then pays it out to the shareholders, net of its own expenses. We can expect that this will give the fund a fairly respectable yield.

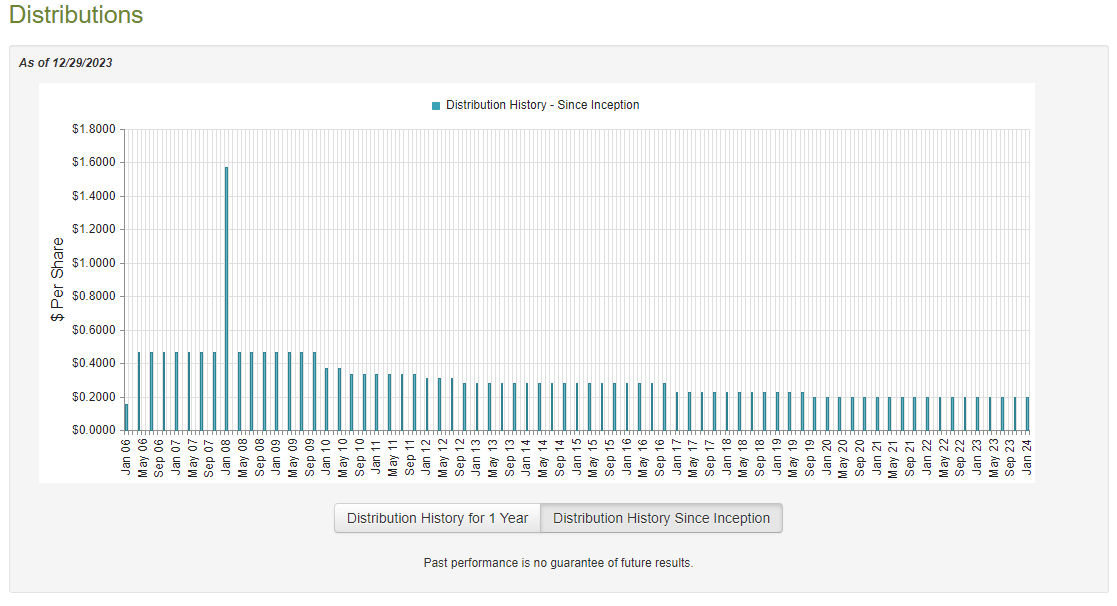

This is indeed the case, as this fund pays a quarterly distribution of $0.1970 per share ($0.7880 per share annually), which gives it a 9.25% yield at the current price. The fund has unfortunately not been particularly consistent with respect to this distribution over the years:

{kind=link}

As we can see, the fund has generally experienced a declining distribution over the years. This is very disappointing, as it is the exact opposite of what most income investors want due to the fact that inflation tends to reduce the purchasing power of the distribution over time. As such, investors who depend on the fund's distribution to pay their bills or finance their lifestyles have seen increasing difficulty accomplishing these tasks over the years. This is almost certainly going to be a major turn-off for any investor who is seeking to earn a safe and consistent income from the assets in their portfolios.

With that said, the fund's distribution history is not necessarily the most important thing for any investor who is considering purchasing the fund's shares today. After all, anyone who purchases the fund's shares today will receive the current distribution at the current yield. This individual will not be affected by any actions that the fund took in the past. As such, the most important thing for any buyer today is how well the fund can sustain its current distribution going forward. Let us investigate this.

Fortunately, we have a relatively recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on August 31, 2023. This document was linked to earlier in this article. This is one of the most recent financial reports currently available for any closed-end fund, as most have financial reports that are at least six or seven months old at this point. This one is newer, which should give us a better understanding of how well the fund has performed recently. In particular, the market was incredibly strong during the first half of this year, which should have given the fund the opportunity to earn some capital gains on the stocks in its portfolio. The market did turn during the last two months of the reporting period though, which could have handed the fund some fairly large unrealized losses.

During the six-month period, the Voya Global Advantage and Premium Opportunity Fund received $3,228,221 in dividends along with $8,197 in interest from the assets in the portfolio. When combined with a small amount of income from other sources, the fund reported a total investment income of $3,236,932 during the period. The fund paid its expenses out of this amount, which left it with $2,467,748 available for shareholders. Obviously, this was nowhere close to enough to cover the distributions that the fund paid out during the period. During the six-month period, the fund paid out a total of $6,168,978 in distributions. At first glance, this might be concerning, as the fund clearly did not have sufficient income to completely cover its distributions over the period.

However, a fund like this does have other methods through which it can obtain the money that it needs to cover the distributions. For example, it might have been able to pocket some of the premiums that it received from the options strategy. The fund also might have been able to realize capital gains from stocks going up in value during the first part of the reporting period. Unfortunately, the fund did not have sufficient success to cover the distributions during the period. It reported net realized gains of $662,942 but this was partially offset by $433,395 net unrealized losses. Overall, the fund's net assets went down by $6,162,192 after accounting for all inflows and outflows during the period. Those outflows did include a $2,690,509 share repurchase program, but the fund clearly failed to fully cover its distributions either way. This is quite disappointing, especially since the fund also failed to cover the distributions during the preceding full-year period. Thus, over the eighteen-month period that ended on August 31, 2023, the Voya Global Advantage and Premium Opportunity Fund failed to fully cover its distributions. This is concerning, as it may suggest that the fund will be forced to cut the payment.

Valuation

As of December 28, 2023 (the most recent date for which data is currently available), the Voya Global Advantage and Premium Opportunity Fund has a net asset value of $9.91 per share but the shares currently trade for $8.52 each. This gives the fund's shares a 14.02% discount on net asset value at the current price. This is a more attractive price than the 13.45% discount that the shares have had on average over the past month. As such, the current entry price appears to be reasonable.

Conclusion

In conclusion, the Voya Global Advantage and Premium Opportunity Fund provides a reasonable way to obtain a high yield without sacrificing the upside potential of an equity investment. The fund appears to exhibit somewhat lower volatility than ordinary common equities, which actually should position it to deliver fairly strong performance if you believe that the markets are overvalued and could decline in 2024. While there are reasons to believe that the stock market is overvalued, I am hesitant to predict a near-term decline. The fact that this fund has failed to cover its distribution over the past eighteen months is a major strike against it, as is the fact that the distribution has been repeatedly cut over its lifetime. As such, it appears that it is trading at a huge discount for a reason.

For further details see:

IGA: Trading At A Discount For A Very Good Reason