IHRTB - iHeartMedia: A Hold For Now Even Though Management Sounded Optimistic

2023-06-02 07:23:59 ET

Summary

- iHeartMedia's Q1 results show a decline in revenues, EBITDA and FCF - causing concerns about the company's ability to handle its debt load.

- Management remains optimistic about the future, expecting a recovery in ad spending and positive free cash flow in each of the three remaining quarters of 2023.

- Management should focus on repurchasing their bonds, trading at deep discounts to par, and positioning the company to achieve the net leverage ratio goal of 4x.

We have been working our way through various earnings reports and conference calls over the last few weeks and have gotten behind as we are having to spend more time analyzing comments from management and looking up historical reporting data to compare and contrast current results to previous quarters. iHeartMedia (IHRT) is one report that we keep circling back to as we are having trouble reconciling the market's reaction to the actual numbers and even management's comments.

So to be clear, we were wrong on iHeartMedia a few months back. Our belief was that the tailwinds of certain key demographics returning to the ad market would be stronger than the overall slowdown in ad spending that could occur with worries about the economy. While auto has returned locally and is quite strong, that has not been able to slow the decline in revenues and the even greater decline in EBITDA and FCF. Sure, Q1 is a weak quarter for the company due to seasonality issues and such, but we think the market was taken aback by the operating leverage iHeartMedia enjoys for EBITDA/FCF generation and just how quickly (and to the extent) that it worked against them this quarter.

So taking a careful look at everything brought us to a few conclusions and forced us to add some topics to our watchlist moving forward.

Market Pessimism

Our big takeaway from this quarter is perception that is derived from perspective (what one believes to be true based on what they are seeing). It is clear to us that management has a perspective that differs greatly from that of the market and clearly a gulf now exists between the two camps. This gulf between the two perspectives has created a perception (among some in the market) that iHeartMedia's business might not be so great after all and it might get bad enough that they end up having cash flow and, ultimately, debt problems.

As investors in this space, we did not see the ad spending slowdown occurring this quickly, but it did and the initial results for many in the industry have not been good. There is no denying this. However, iHeartMedia's management team did not seem pessimistic about the business going forward and seemed to indicate that their belief was that this was going to be a small pullback in ad spending in 2023 before getting political ad spend coming in at the end of the year and into, and through, 2024. Bob Pittman, the company's CEO, said that "the advertising market was a bit stronger in the quarter than we had initially anticipated" in his opening remarks on the conference call and mentioned an advertising recovery a couple of times as well. So if management was pleased with the fact that this quarter came in better than expected, there seems to be a disconnect with market expectations because the reception to the release was not great and the stock has been in a downtrend for a while now. If all of that was good news, the market certainly did not get the message - as the below chart will attest to.

EBITDA And FCF Generation

We have seen more and more talk among investors about iHeartMedia and whether it can make it through a recession with the debt load. We thought it was possible before the latest quarter and believe that it is still possible...and to be clear, we do not think that it is highly probable that the company defaults, or even comes close, assuming that the Fed is nearing the end of their rising interest rate cycle and that any potential recession does not cut too deep.

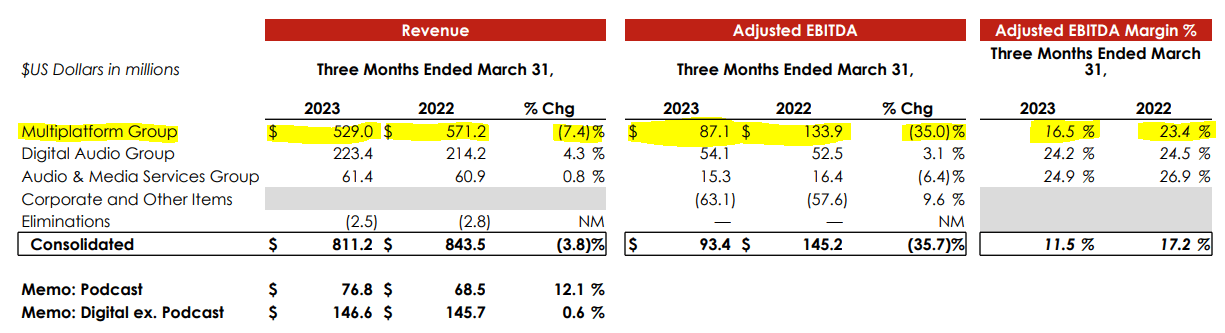

What many miss is that media companies are highly levered to the advertising market and have pretty high costs that they cannot take out of the business...the fixed costs can be pretty brutal even in the best of times and in tough times their impact is amplified upon results. So the fluctuations in revenues are key to what these types of businesses can generate in regards to EBITDA and FCF. This was on display in iHeartMedia's Q1, as the company reported revenues of $811 million and Adjusted EBITDA of $93 million. In Q1 of 2022, iHeartMedia reported revenues of $843 million and Adjusted EBITDA of $145 million. These differences highlight the difference between a quarter with a healthy advertising background and one with uncertainty, but it also shows the relationship with revenues and how above a certain level a large portion of that hits Adjusted EBITDA.

The Multiplatform Group, which includes the broadcast radio assets, shows perfectly the operating leverage at work. (iHeartMedia Q1 2023 Investor Presentation)

{kind=link}

A better example might be to look at Q4 2022 with Q1 2023. Both quarters had a weakening ad market and expenses (other than the run-off from a bad program the company ran in late 2022) would be similar from one quarter to the next. Looking at Q4 revenue of $1.126 billion and Adjusted EBITDA of $316 million with FCF of $165 million, you can see what iHeartMedia is capable of in their best quarter of the year (which is their strongest ad demand season). So revenues quarter-over-quarter decline $315 million and Adjusted EBITDA declines $223 million on the same basis. FCF also declines by $298 million on that basis, further highlighting the operating leverage.

Management indicated that this will be the only quarter that they do not report positive FCF, as Bob Pittman stated, "we will generate positive free cash flow in each of the remaining quarters in 2023." This was repeated by Rich Bressler (iHeartMedia's COO and CFO) in his prepared comments as well. Based on the numbers, we think that it will take the company until Q3 to be FCF positive on a fiscal year-to-date basis due to this big hole they are starting out in. So as bad as this quarter was for the metrics that really matter, it certainly looks like the company will generate plenty of FCF to pay down debt and/or build up cash on the balance sheet.

Debt

We were pleased to see that management paid down another $20 million in debt by buying back some of their bonds below par. This cost the company $15.4 million in cash, and although the company stated that it is "expected to generate approximately $2 million of annualized interest savings" in their Executive Summary of the conference call presentation PowerPoint, we think that the number is closer to $1.5 million (the actual we think is $1.675 million). While that is splitting hairs, we think it is important to note because it is a compelling return on cash when looking at the interest savings and even better when factoring in the total return due to repurchasing these bonds below par (the current yield-to-maturity, or YTM, is around 25%).

iHeartMedia's Form 10-Q provides more detailed figures for their debt repurchases in the quarter. (iHeartMedia 10-Q, SEC)

{kind=link}

If management was able to repurchase $20 million in a quarter in which the company had negative $133 million in FCF, we would hope that they could repurchase a good bit more next quarter when they should generate somewhere between $50 million and $100 million. With revenues and Adjusted EBITDA falling in 2023, so long as the company can remain FCF positive in a meaningful way, management should be incentivized to continue to repurchase bonds, especially the 8.375% coupon bond maturing in May 2027 since it has been trading below 60 cents on the dollar the last few weeks, as the repurchases amplify their ability to drive down their net leverage ratio (this is due to the steep discount to par the bonds trade at). In short, instead of $100 million cash sitting on the balance sheet later in the year and being netted out against the company debt balance (which is carried at par), management might be able to repurchase roughly $166.7 million of that particular bond over the course of the year (assuming it continues to trade around $0.60 on the dollar) which gives them an additional $66.7 million benefit in the calculation of net leverage. This is what will most likely have to be done in an environment where EBITDA is going to be declining.

Our Takeaway

Look, this was not a great quarter and caught some people by surprise with how far EBITDA and FCF fell. While management is more optimistic than we are, we still like the industry overall and believe that digital is going to be what companies are forced to embrace. Before the transition to digital can play out with the market choosing winners and losers, we think that all players in the industry will have to adjust their focus to their respective balance sheets to address their debt -something many were not even thinking would be a major headache 12-18 months ago. iHeartMedia has approximately 40% of their debt structured as floating, so they have already been impacted by the rise in interest rates and expect to pay about $390 million in interest expense this year. If interest rates are cut, that would provide a nice tailwind for the company as their annual interest expense would decrease dramatically.

This story has gotten more complicated with the headwinds in the media space, and more specifically with the weakness in the ad market, but if management is correct in their guidance and outlook (specifically with 2024 looking better than 2023, and 2023 not looking as bad as some had feared) then we think that 2023 might be the year that sets the stock up for a move higher later. Management should focus on plowing FCF into buying back their deeply discounted bonds in 2023 and 2024 and then look to extend their loans that mature in 2026 in the first half of 2025 to signal to the market their intentions (while also getting it out of the way in order to focus on the bonds they have maturing in 2026).

How We Are Playing The Stock

We currently have this name rated a 'Hold' on our Watchlists. With the stock down big we have only recently resumed purchases in order to maintain our target allocations, however we are not sellers on gradual moves higher as these purchases are used to lower cost basis and enable us to de-risk on larger moves higher over time. We remain confident that the company will not have debt issues, assuming the economy does not seriously deteriorate, but want to wait another quarter before we get aggressive with the name. If management's guidance for Q2 turns out to be accurate and their guidance on Q3 is in-line with what they alluded to on this quarter's conference call, then at that time we might turn bullish once again.

While we recognize that this may very well be a name that can rise dramatically when the ad market recovers, we do wonder if more conservative investors might not be better served looking at the bonds. With offerings by brokers of the May 2027 maturity that has the 8.375% coupon offering yields to maturity between 23% to 26% and current yields between roughly 13.50% and 14.70% they look tempting. Currently we are only holders of the equity in personal and client accounts, but we do see some situations where the bonds could serve a legitimate purpose.

For further details see:

iHeartMedia: A Hold For Now, Even Though Management Sounded Optimistic