ITW - Illinois Tool Works: A Dividend King Near All-Time Highs

2023-06-09 07:06:14 ET

Summary

- Illinois Tool Works is performing well despite being close to a manufacturing recession, with shares up 8% year-to-date and 37% above their 52-week low.

- The company continues to report organic growth and offset inflationary headwinds through its pricing power, maintaining a positive outlook despite economic challenges.

- ITW's success makes it an attractive option for dividend growth investors, as it has more than 50 consecutive annual dividend hikes and is considered one of the best dividend kings.

Introduction

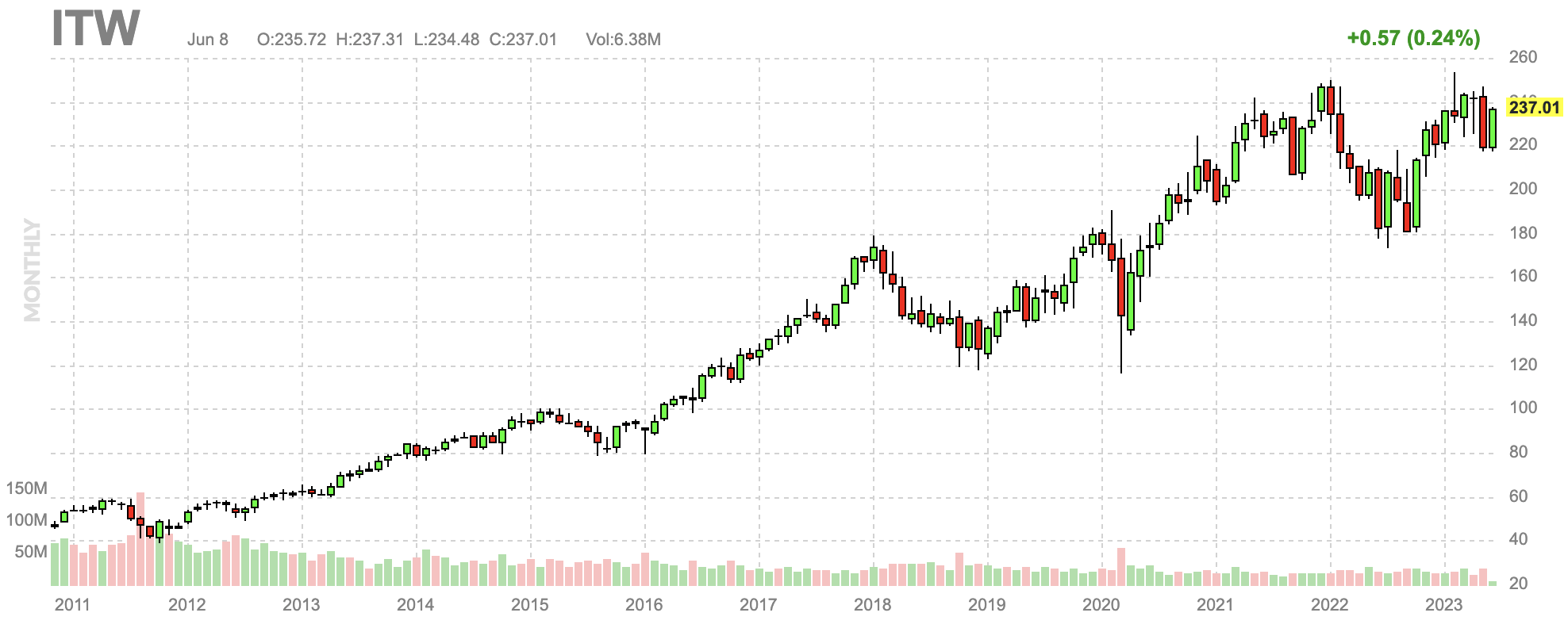

Someone, please tell Illinois Tool Works (ITW) we're very close to a manufacturing recession. This Illinois-based industrial stock clearly hasn't gotten the memo.

Shares of ITW are trading roughly 5% below their all-time high. They are up almost 8% year-to-date and 37% above their 52-week low.

{kind=link}

What's so interesting is that this cyclical dividend king, with more than 50 consecutive annual dividend hikes, is doing just fine. The company continues to report positive organic growth, it's offsetting inflationary headwinds by using its pricing power, and it has a good outlook, despite economic challenges.

This is great news for dividend (growth) investors who continue to bet on the right horse. While cyclical headwinds aren't unlikely to provide us with better buying opportunities down the road, ITW is proving, once again, that it's one of the best dividend kings money can buy.

In this article, I'll elaborate on all of this.

So, let's get to it!

A Dividend King That Comes With An Excellent Business Model

Let's start by mentioning that Illinois Tool Works is a dividend king. This means the company has hiked its dividend for at least 50 consecutive years. As I wrote in my January ITW article , this means at least three things:

- A company needs to be able to pay a dividend in the first place. Meaning it needs to be profitable.

- That company needs to be profitable on a long-term basis and maintain strong capital discipline.

- It needs to consistently grow its net income and free cash flow to pay a steadily rising dividend.

Hence, when dealing with a dividend king, we can assume that we're dealing with a superior company. After all, no company can fake 50 years of consecutive dividend growth - meaning borrowing money to distribute a dividend.

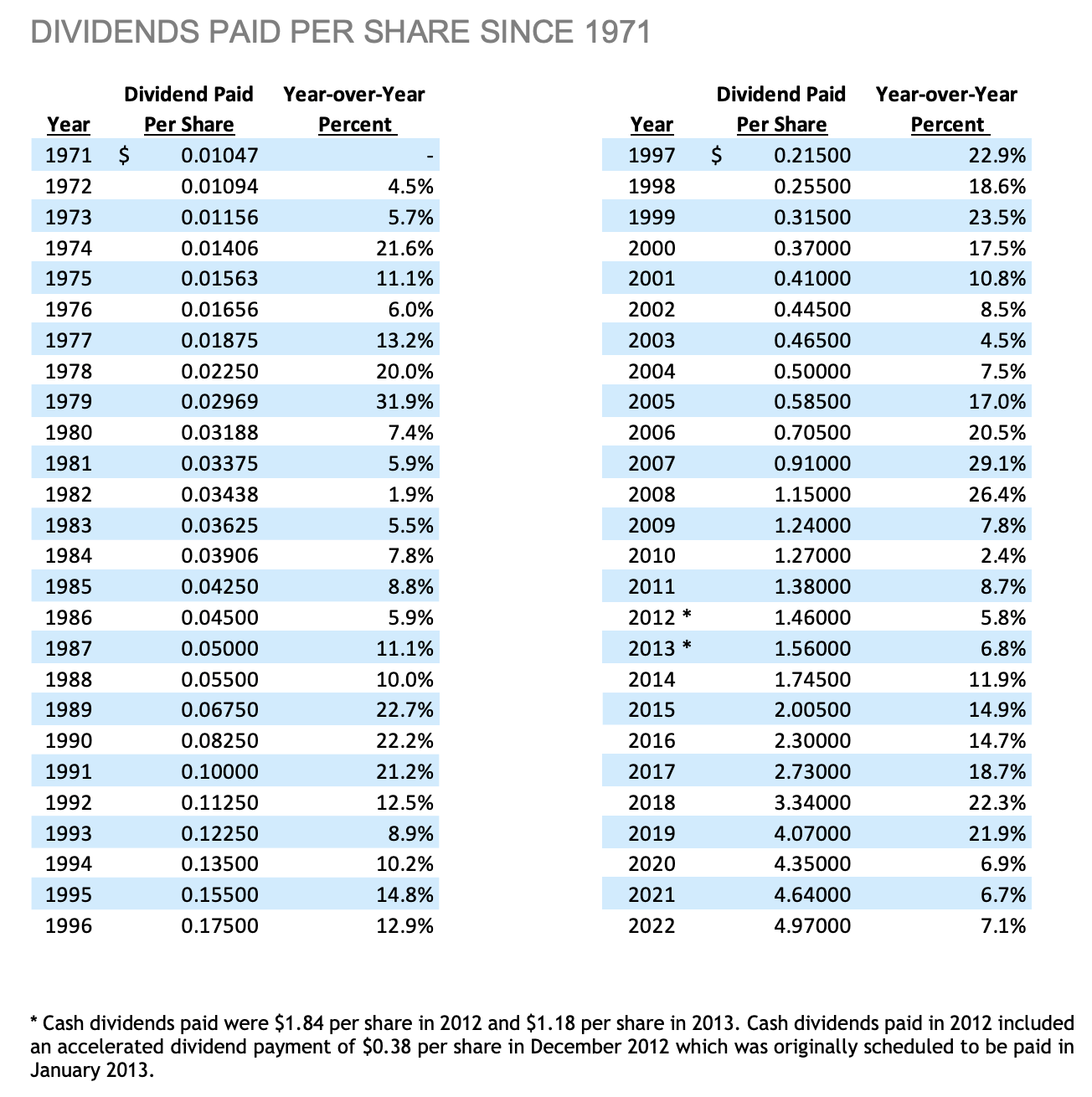

Last year, the company hiked its dividend by 7.1%, which marked the 50th consecutive dividend hike.

{kind=link}

The company currently yields 2.2%, which is based on a $1.31 per share per quarter dividend.

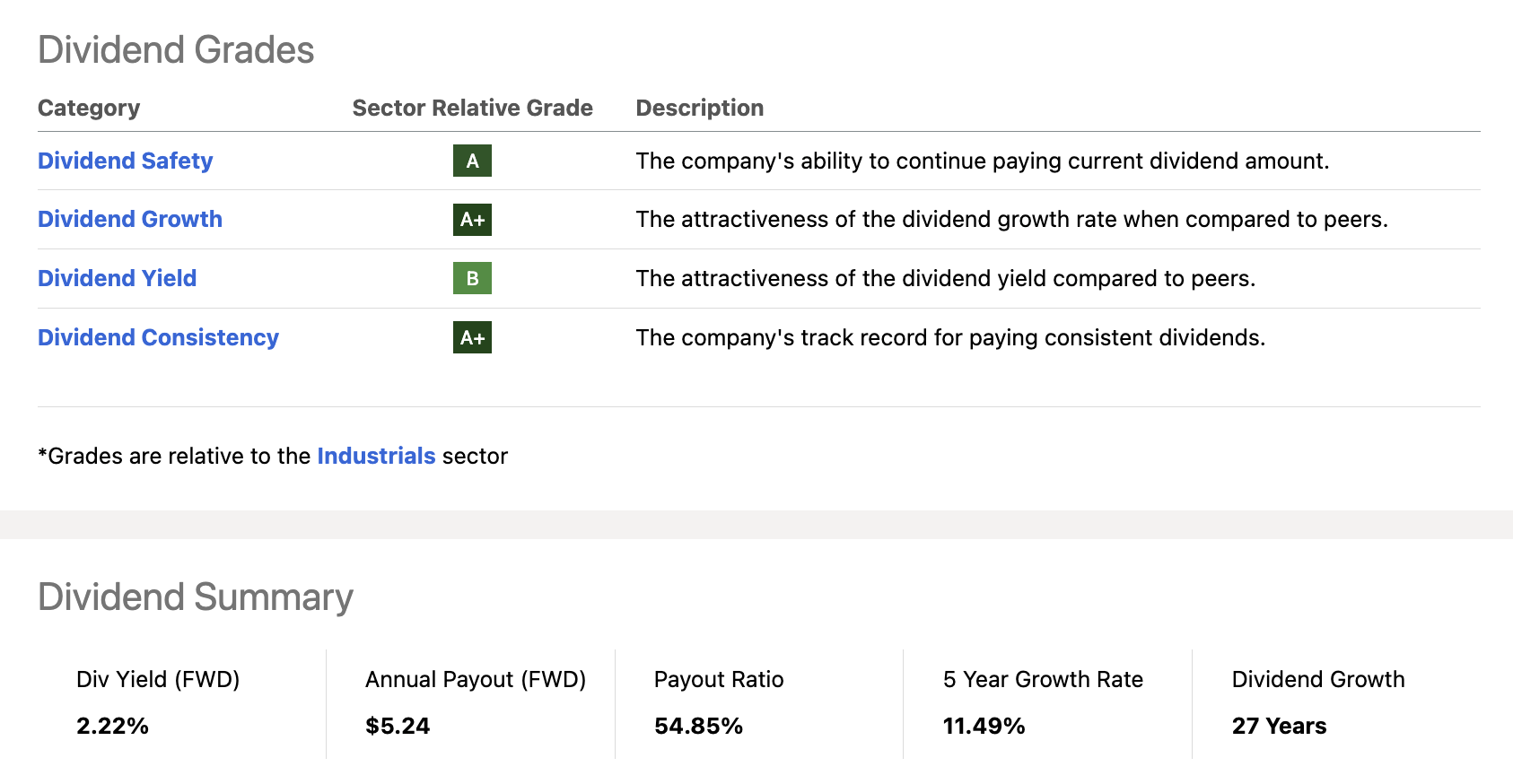

This dividend comes with an impressive dividend scorecard (please ignore the dividend growth number of 27 years).

- On average, ITW has hiked its dividend by 11.5% per year over the past five years.

- The company maintains a healthy 55% payout ratio.

{kind=link}

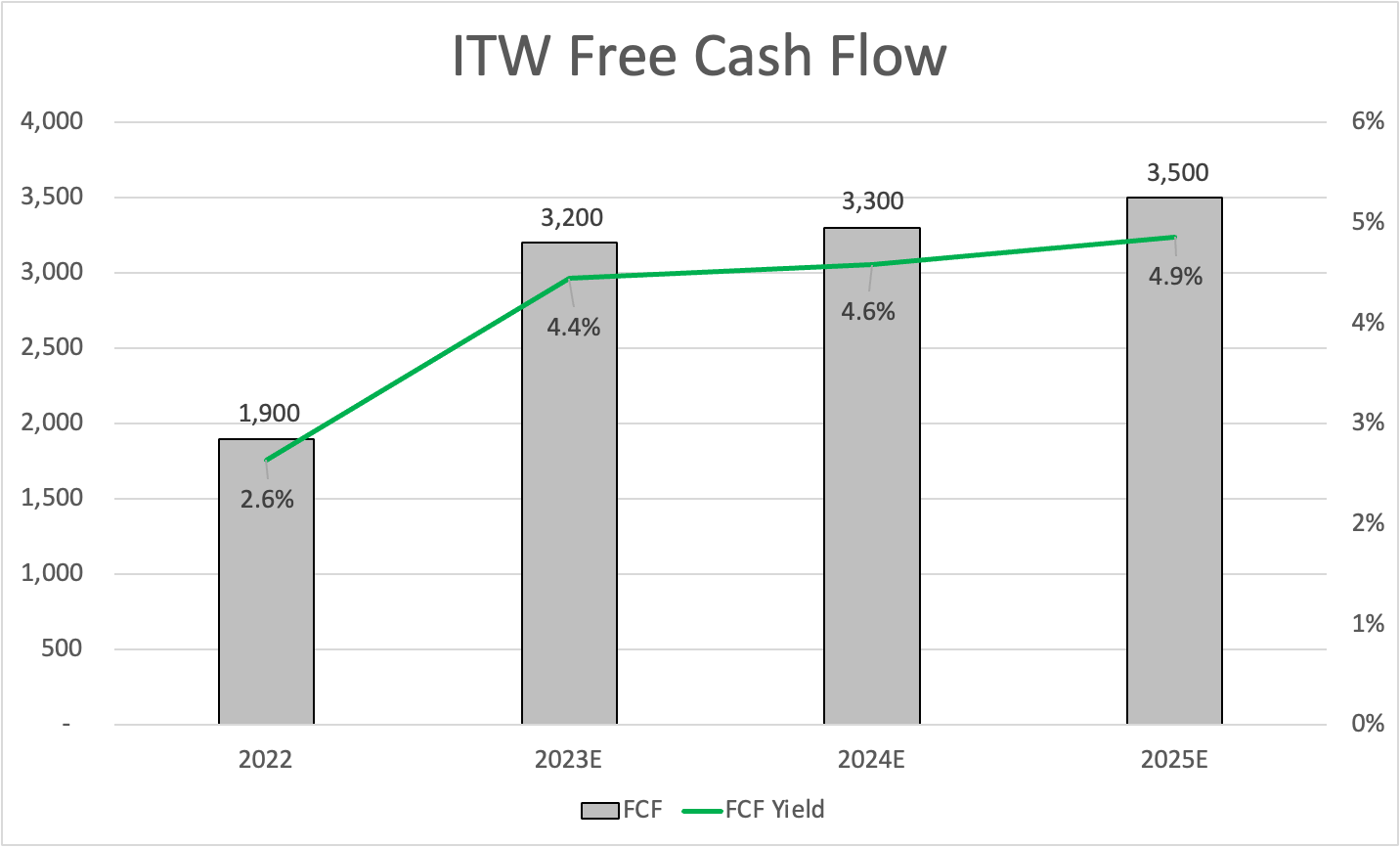

Furthermore, after a number of tough pandemic years with broken supply chains, the cash payout ratio is expected to drop from the 80% range to less than 50% in 2024.

{kind=link}

This is good news for long-term dividend growth and buybacks, which is something the company also does. After all, it has a 2023E net leverage ratio of 1.6x EBITDA and an A+ credit rating, which means it does not have to prioritize debtholders over shareholders.

Hence, over the past ten years, ITW has bought back roughly a third of its shares.

This is one of the reasons why the company is consistently outperforming the market and its industrial sector peers.

With that said, let's dive a bit deeper, as the company's business model and growth plans reveal a lot about the odds of prolonged satisfying dividend growth, buybacks, and potential outperformance.

ITW Is Mature, But Not Slow

There are fantastic reasons to buy proven businesses in the dividend king and aristocrat segments. However, one downside is that these businesses are often very mature, which tends to come with slow growth.

ITW isn't a fast-growing business, as the chart below shows. However, it's expected to ramp up its growth rates. Also, the company is increasingly efficient, as shown by the consistent - yet volatile - long-term uptrend in free cash flow.

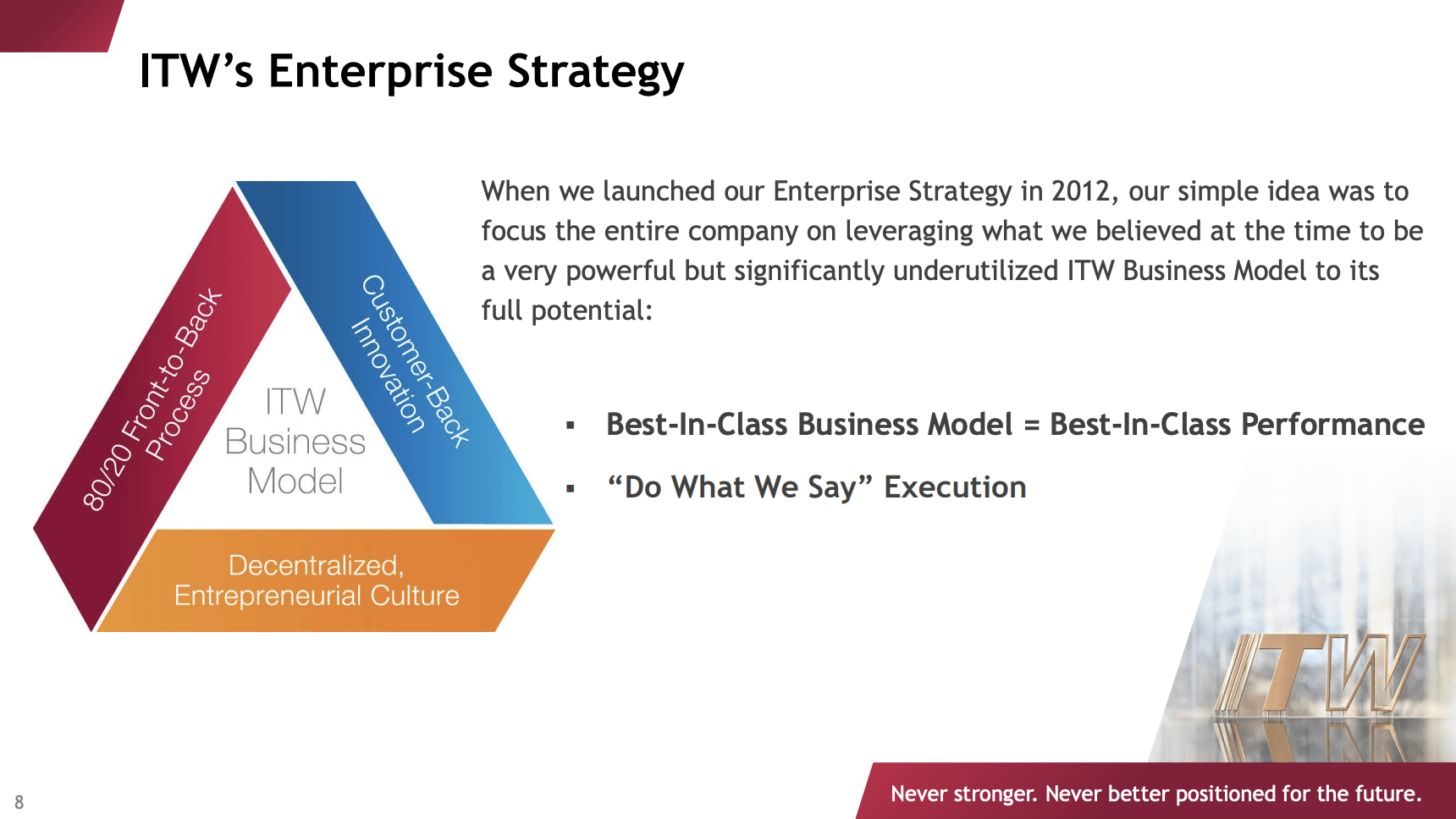

With all of this in mind, ITS has a very smart business model. The company follows its 80/20 model. This means that ITW focuses on the best 80% of business opportunities, cutting costs and complexity in the least promising 20% of its projects. This allows the company to remain innovative without becoming a company with too much dead weight.

This is based on an enterprise strategy that began in 2012 and focuses on organic growth as the primary engine for financial performance.

{kind=link}

The strategy involves narrowing the business portfolio, simplifying the business structure, and establishing strategic sourcing capabilities.

Related to my revenue and free cash flow chart, in its May investor presentation, the company highlighted the benefits of its enterprise strategy. Since 2012:

- Total revenue has declined by 11%.

- Operating margins have improved by 790 basis points.

- Earnings per share have tripled.

- Dividends have gone from $1.48 to $5.06.

- The market cap has tripled as well.

That's pretty good for a company with negative 11% revenue growth.

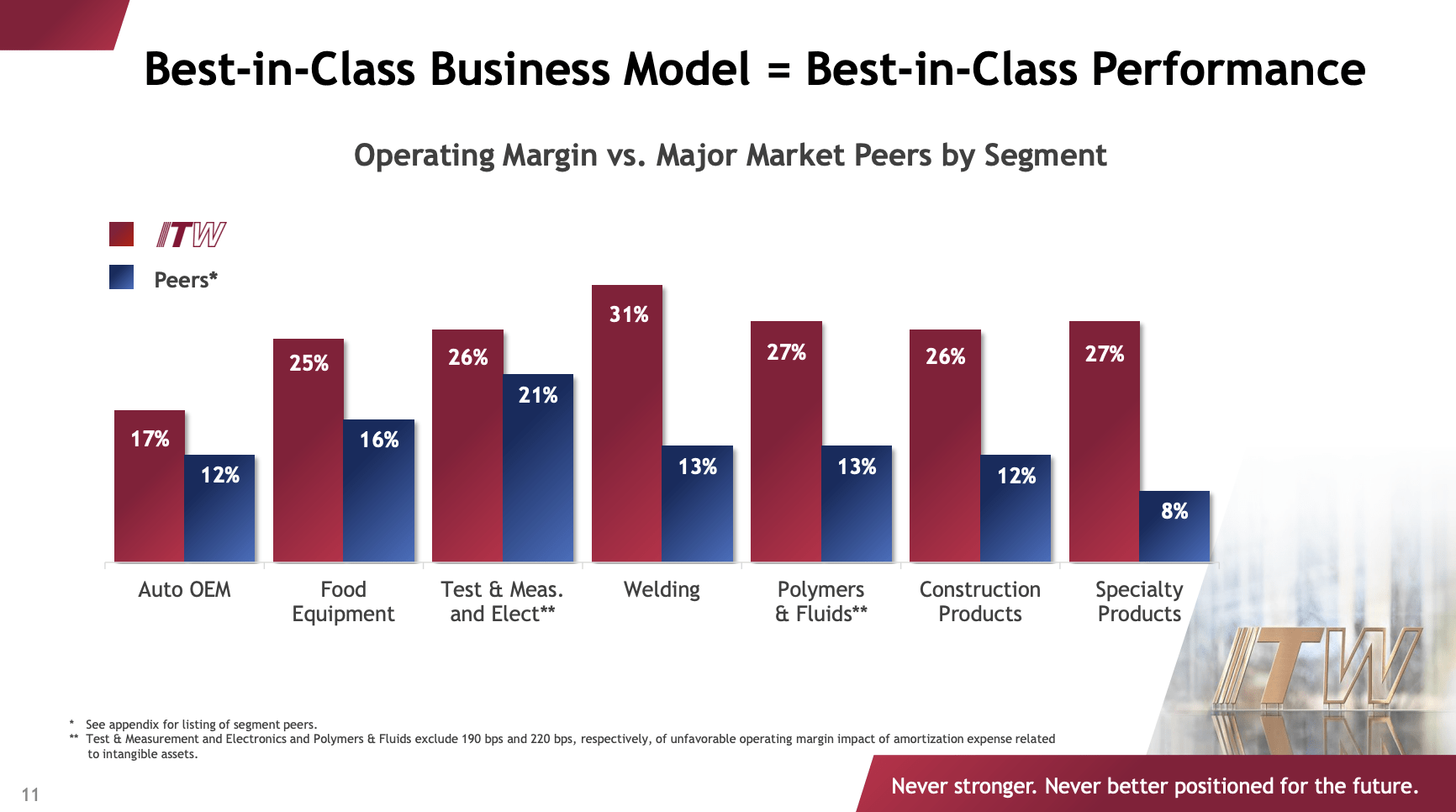

Additionally, the company has peer-leading margins in every single one of its segments.

{kind=link}

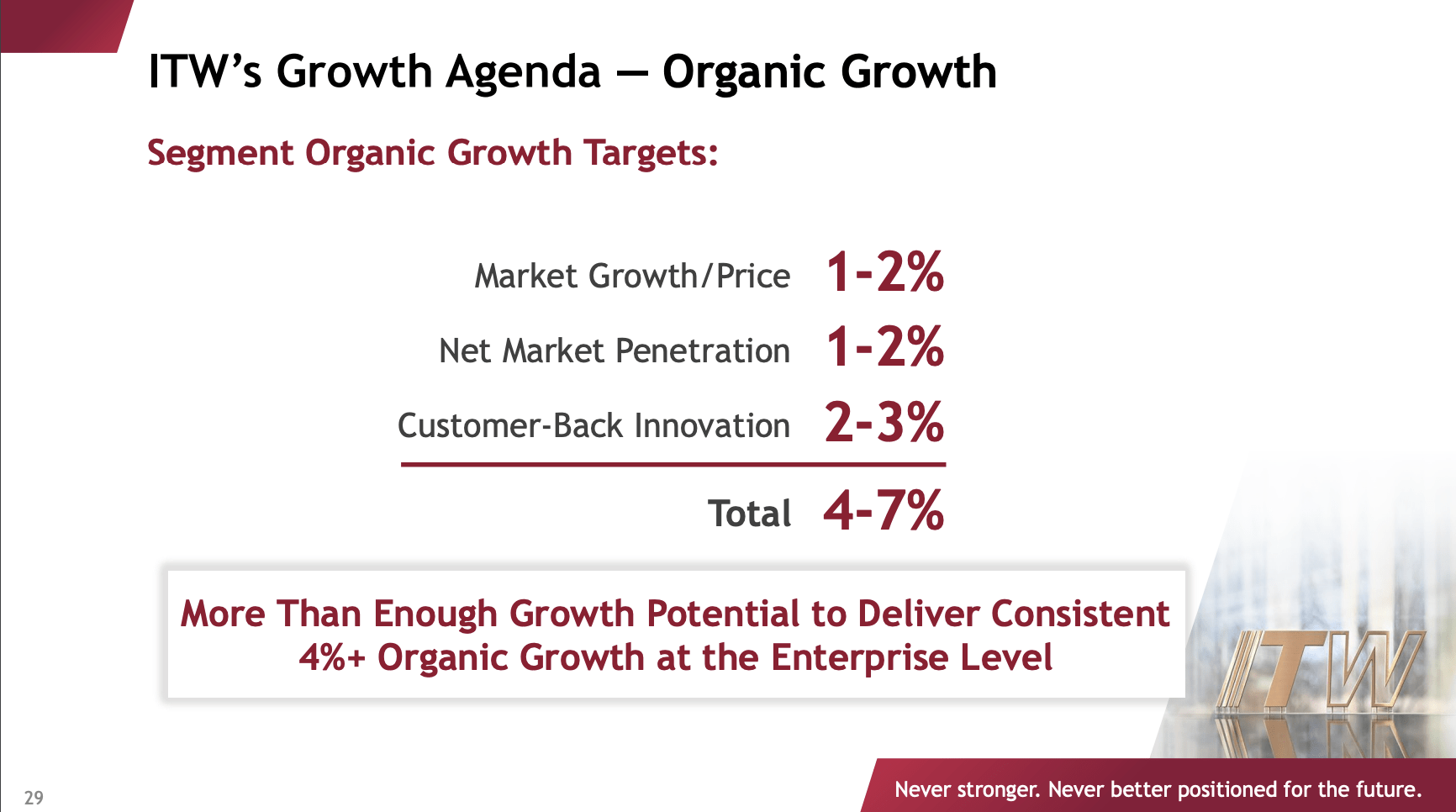

The good news is that ITW is now shifting its focus to organic growth, as it targets 4% to 7% organic growth through the cycle in its 2030 plan. This is expected to be caused by pricing, market share benefits, and innovation.

{kind=link}

Furthermore, the company is proven to be extremely resilient in the current market.

There are plenty of indicators that point to a steep manufacturing recession. One of them is the ISM Manufacturing Index. The chart below shows the new orders component of that index. Even during the 2015/2016 manufacturing recession, that number was higher.

Bloomberg

Despite that this slowing trend has been going on since 2021, ITW is doing just fine - as suggested by its stock price.

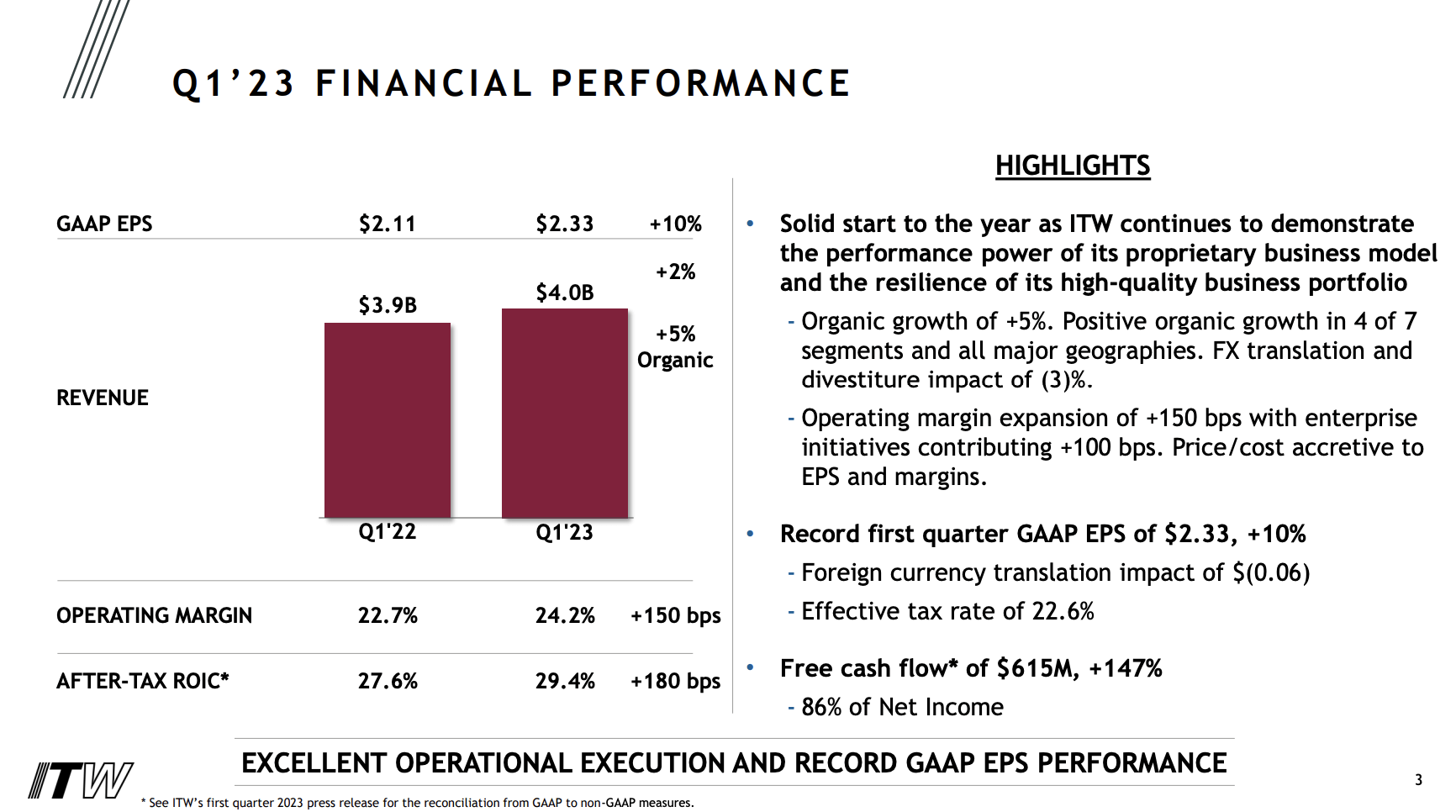

In the first quarter, the company achieved 5% organic growth, with four out of seven segments delivering positive organic growth. Food equipment led the way with 16% growth, followed by Welding with 10%, Automotive OEM with 8%, and Test & Measurement and Electronics with 6%. Polymers & Fluids was flat, Construction was down 1%, and Specialty was down 5%.

{kind=link}

Despite higher wage and benefit costs, operating margins expanded by 150 basis points to 24.2%, driven by the aforementioned enterprise initiatives. GAAP earnings per share increased by 10% to $2.33, setting a new Q1 record.

Illinois Tool Works expects to recover about half of the 250 basis points of margin dilution experienced over the last two years. However, the company mentioned that investments in organic growth and workforce may offset some of the margin gains.

The free cash flow conversion rate was 86% of net income, in line with or slightly above normal Q1 levels.

With regard to the slowing trend in economic growth, the company mentioned that around 25% of the company's revenues were slowing down, specifically in residential construction, commercial welding, automotive aftermarket, appliance components, Specialty Products, and the Test & Measurement segment. These businesses experienced varying degrees of decline in Q1, but their performance was in line with the company's expectations.

The company also emphasized that the business environment is uncertain, but based on current knowledge, the company remains well-positioned to achieve its goals.

This was also reflected in its outlook.

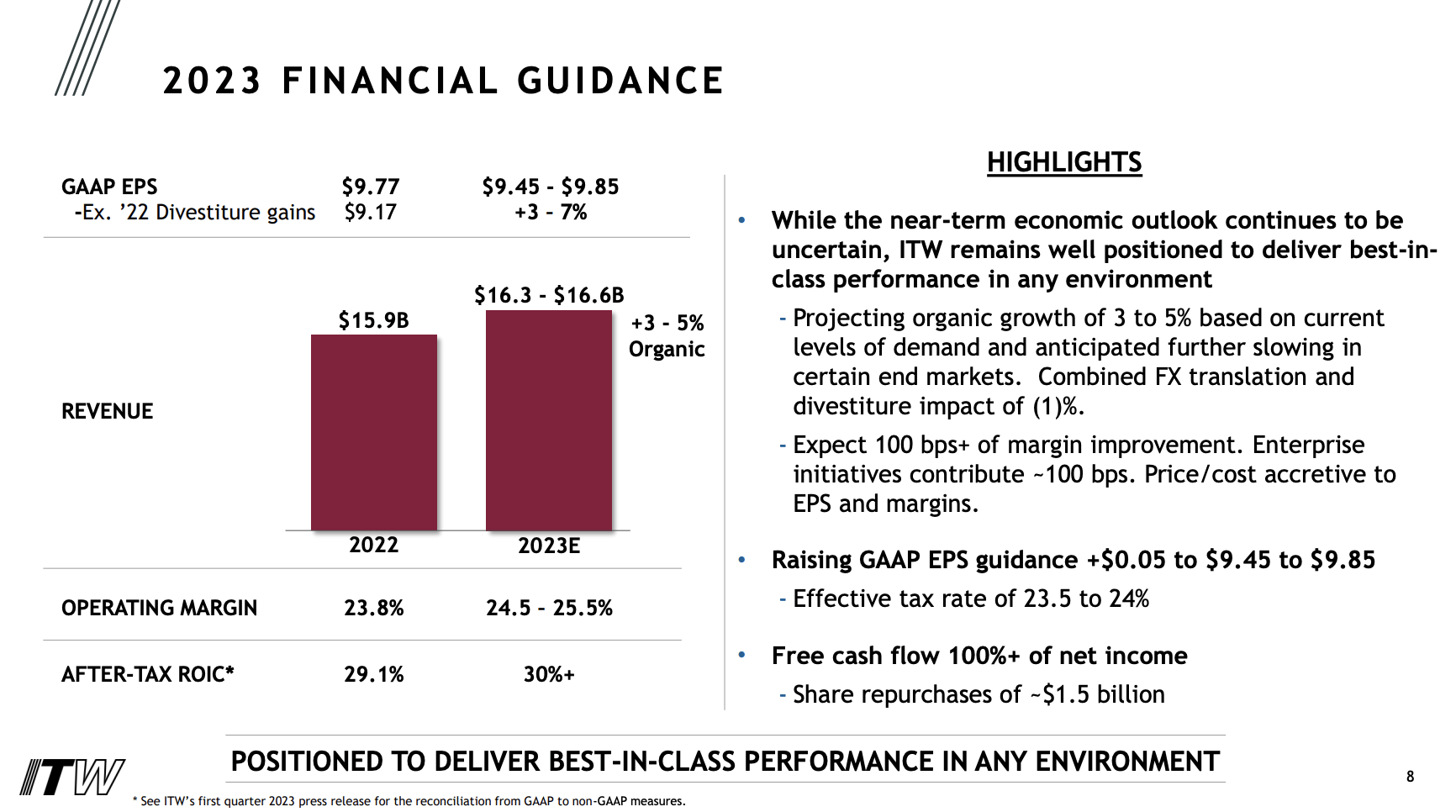

The company provided updated guidance for the full year 2023, raising the GAAP EPS guidance by $0.05 to a range of $9.45 to $9.85. The organic growth projection is set at 3% to 5%, accounting for the current levels of demand and potential risks in certain end markets.

{kind=link}

Operating margins are expected to expand by more than 100 basis points, including contributions from enterprise initiatives and positive price/cost margin impact.

While I do not expect that ITW's stock price can continue a smooth uptrend, these numbers and developments support its extreme resilience in tough markets.

Valuation

When valuing ITW, it is important to assess free cash flow. Since the pandemic, the valuation has increased steadily. Currently, ITW is trading at 32x LTM free cash flow, which seems absurd.

However, free cash flow is expected to rebound quite significantly, as shown in the free cash flow chart earlier in this article.

ITW is trading at 22x 2024 free cash flow, which brings the valuation back to pre-pandemic levels. However, we're using 2024 expectations, which means a bit part of future growth has already been priced in.

The current consensus price target is $237, which is a dollar above the current price. I agree with that, as I dislike the risk/reward at current levels.

While I believe that the stock price surge is warranted, thanks to its terrific business performance and a good outlook, I would not be a buyer at current levels, as there are high chances that the outlook might be revised lower in the 2Q23 earnings call. After all, economic headwinds are becoming stronger, which is not yet priced in.

If you're in the market for ITW shares, I would monitor the stock for an opportunity close to $200. I believe that the $180 to $200 range offers buying opportunities.

In that case, I would be a gradual buyer to have a chance at averaging down if the stock falls further. That is how I have dealt with every single investment since the economic growth peak of 2021.

Takeaway

Illinois Tool Works stands out as a resilient and reliable dividend king, defying the looming manufacturing recession. Despite the cyclical headwinds, ITW continues to report strong organic growth, mitigate inflationary pressures through pricing power, and maintain a positive outlook.

Its impressive dividend scorecard, robust financials, and strategic focus on organic growth position it as a top choice for dividend (growth) investors.

ITW's 80/20 model and enterprise strategy have contributed to improved margins, tripled earnings per share, and a significant increase in dividends.

While the company isn't a fast-growing business, it is expected to ramp up growth rates and maintain its peer-leading margins.

However, considering the current economic uncertainties, cautious investors may wait for a potential buying opportunity within the $180 to $200 range.

Overall, ITW's exceptional performance and prudent business approach make it a compelling dividend king to watch closely.

For further details see:

Illinois Tool Works: A Dividend King Near All-Time Highs