ITW - Illinois Tool Works: A Good Buy At Current Levels

2023-10-30 14:21:52 ET

Summary

- Illinois Tools Works' revenue growth is expected to benefit from strength in end markets like Automotive OEM and Food and Equipment.

- The company's margins are expected to benefit from recent price increases and cost reduction initiatives.

- ITW stock is considered a good buy due to its growth prospects, attractive dividend yield, and reasonable valuation.

Investment Thesis

Illinois Tools Work’s ( ITW ) revenue growth should benefit from strength in its end markets like Automotive OEM and Food and Equipment, the Chinese economy reopening gaining momentum, new product innovation, and market share gains which should more than offset the weakness in end markets like Semiconductors and Welding. Beyond 2023, the company’s revenue is poised to benefit as the semiconductor end-market bottoms and inventory destocking at its customers ends by mid-2024.

In terms of margins, the carryover impact of recent price increases and cost reduction initiatives should continue to benefit margins in the near term. In the long run, benefits from volume leverage and enterprise initiatives should help margins. The valuation is also lower than historical levels. Given good growth prospects and a reasonable valuation, I believe the ITW stock is a good buy at the current levels.

Revenue Analysis and Outlook

I previously covered ITW in September. The stock price declined mid-single digits since then as the concerns around the United Auto Workers ("UAW") strike at big three automakers Ford ( F ), General Motors ( GM ), and Stellantis ( STLA ) grew. The company also reported incremental softness in Test Measurement & Electronics, and Welding Segment orders when it reported its Q3 results last week.

In the third quarter of 2023, ITW reported a 0.5% increase in revenue to $4.031 billion attributed to a 0.2% increase in organic sales and a 1.5 percentage point favorable impact of FX translation which was partially offset by a 1.2 percentage point adverse impact of divestiture activity. However, one should note that Q3 this year had one less shipping day compared to Q3 last year. On an equal-day basis, organic growth was up 2% Y/Y.

Organic revenue was largely flat Y/Y, as organic growth of 3.8% Y/Y in the Automotive OEM, 6.3% Y/Y in the Food Equipment, and 3.4% Y/Y in the Polymers & Fluids segments was offset by a decline in organic sales of 3.9% Y/Y in Test & Measurement and Electronics, 2.4% Y/Y in Welding, 2.1% Y/Y in Construction Products, and 5.6% Y/Y in Specialty Products. Additionally, product line simplification activities reduced organic revenue by 40 basis points in the third quarter.

ITW’s Historical Revenue Growth (Company Data, GS Analytics Research)

Looking forward, I am optimistic about the company’s medium to long-term growth prospects. The near-term prospects have also improved over the last few days as UAW and two automakers have agreed on tentative deals. The company guided for a 12 cents impact on its Q4 EPS, assuming the production level at automakers remains similar to what it was seeing at the timing of its earnings call. However, with the strikes ending given the recent agreements between UAW and Ford , and UAW and STLA, the actual impact can be less and the results better.

While there has been some weakness in the Welding and Semiconductor market, I am not too worried about it. For Semiconductor, industry experts were expecting a reacceleration of demand in the second half of this year. However, this recovery seems to have been deferred to next year. So, while this is a near-term headwind, it should eventually dissipate next year which coupled with easy comparisons due to a significant decline this year bodes well for growth in the medium term. Similarly, while the Welding segment is seeing an impact from cyclical showdown due to the tough macroeconomic environment in the near term, the longer-term prospects remain intact.

Further, the weakness in this market should be offset by strong demand in other markets like Automotive OEM, which continues to benefit as Automotive production continues to ramp up after the last couple of years of supply chain disruption, and the Food and Equipment business which is benefiting from reopening as well as the company's launch of new innovative products. Further, the Chinese economy reopening and improved production rates are also helping ITW.

The company is also executing well and doing a good job in terms of gaining market share. For example, last quarter, the company saw a 7% Y/Y increase within its residential renovation business of the Construction segment while the end market was essentially flat. According to management, most of this outperformance stemmed from volume and market share gain through the big box retailers. Similarly, the company’s Automotive aftermarket business grew 10% Y/Y outperforming end-market growth helped by new product launches.

Overall management has guided for 2% to 3% Y/Y growth in revenues this year as strength in end markets like Automotive OEMs, and Food and Equipment, China reopening gaining momentum, and market share gains are expected to more than offset weakness in end markets like Semiconductors and Welding. While management has not yet guided for FY24 revenue growth, I believe ITW’s growth may accelerate next year as some of the slowing end markets like Semiconductors bottom and see easier Y/Y comparisons. Further inventory destocking has been a big headwind for the company in recent quarters and, according to management, it impacted the company’s topline between 1% and 1.5%. Management anticipates the destocking to be completed by the middle of the next year and this headwind waning can itself add 1% to 1.5% to growth next year. So, I remain optimistic about the company’s medium to long-term growth prospects.

Margin Analysis and Outlook

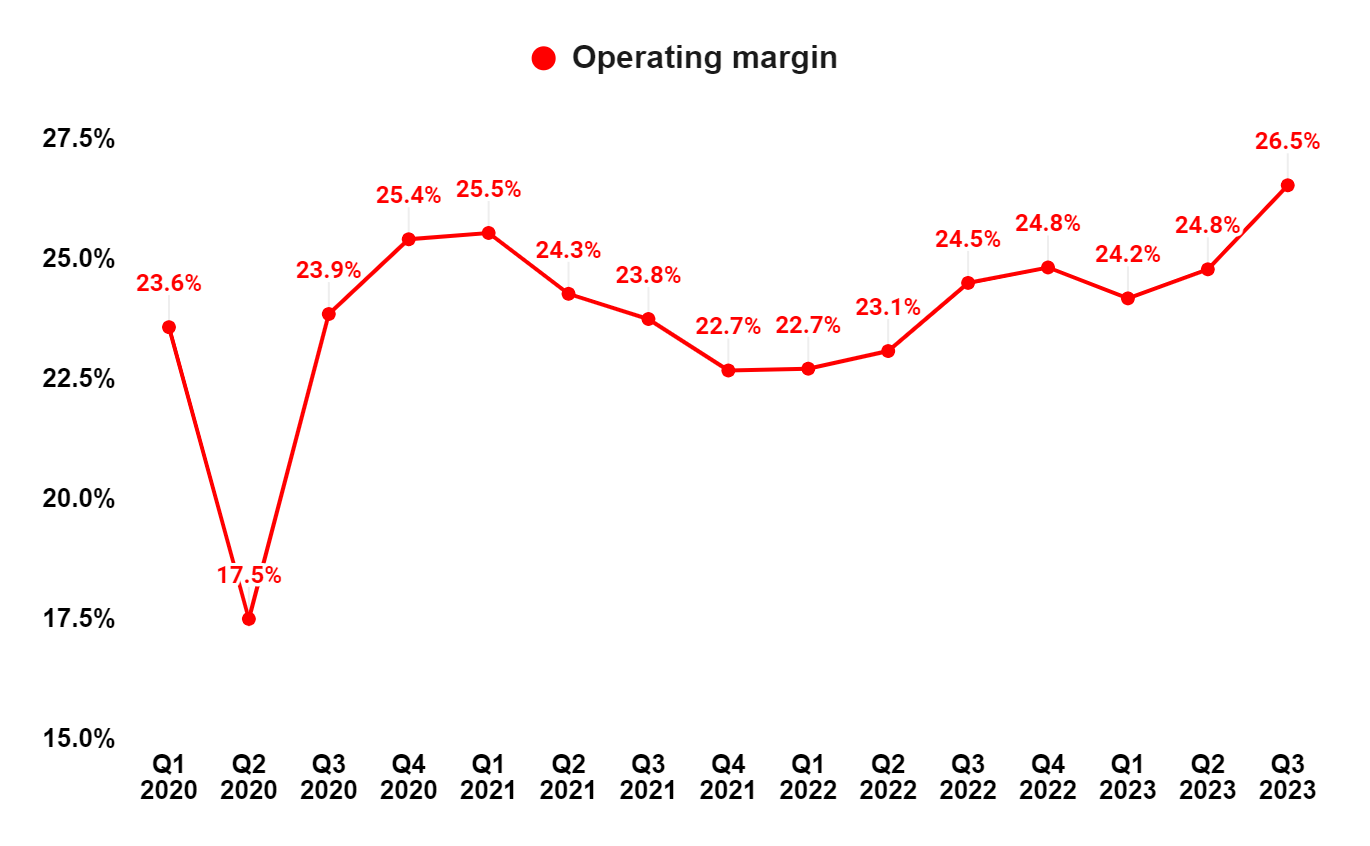

While the company’s revenue growth was modest last quarter, its margin performance was impressive and the company reported a 200 bps Y/Y improvement in operating margin to 26.5%, driven by a favorable price/cost impact of 210 bps and 140 bps contribution from cost reduction and productivity improvement actions under enterprise initiative. This more than offset the headwinds associated with higher employee-related expenses.

ITW’s Historical Operating margin (Company Data, GS Analytics Research)

{kind=link}

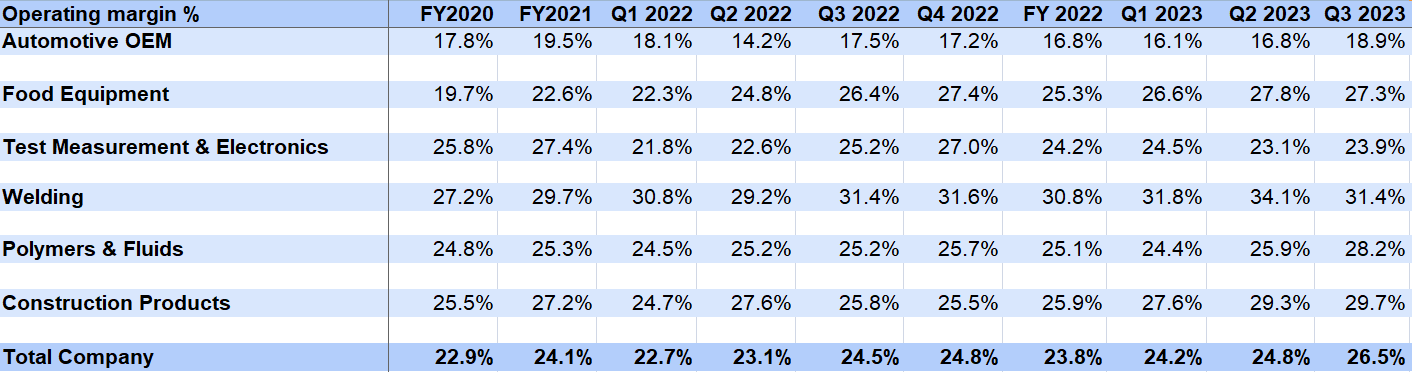

Segment Wise, the company saw an operating margin expansion of 140 bps Y/Y in Automotive OEM, 100 bps Y/Y in Food Equipment, 10 bps Y/Y in Welding, 280 bps in Polymers & Fluids, 420 bps Y/Y in Construction Products and 10 bps Y/Y in Specialty Products which effectively offset a 140 bps Y/Y decline in operating margin in Test & Measurement and Electronics segment, and resulted in Y/Y increase in total operating margin for the company.

ITW’s Segment Wise Operating margin (Company Data, GS Analytics Research)

{kind=link}

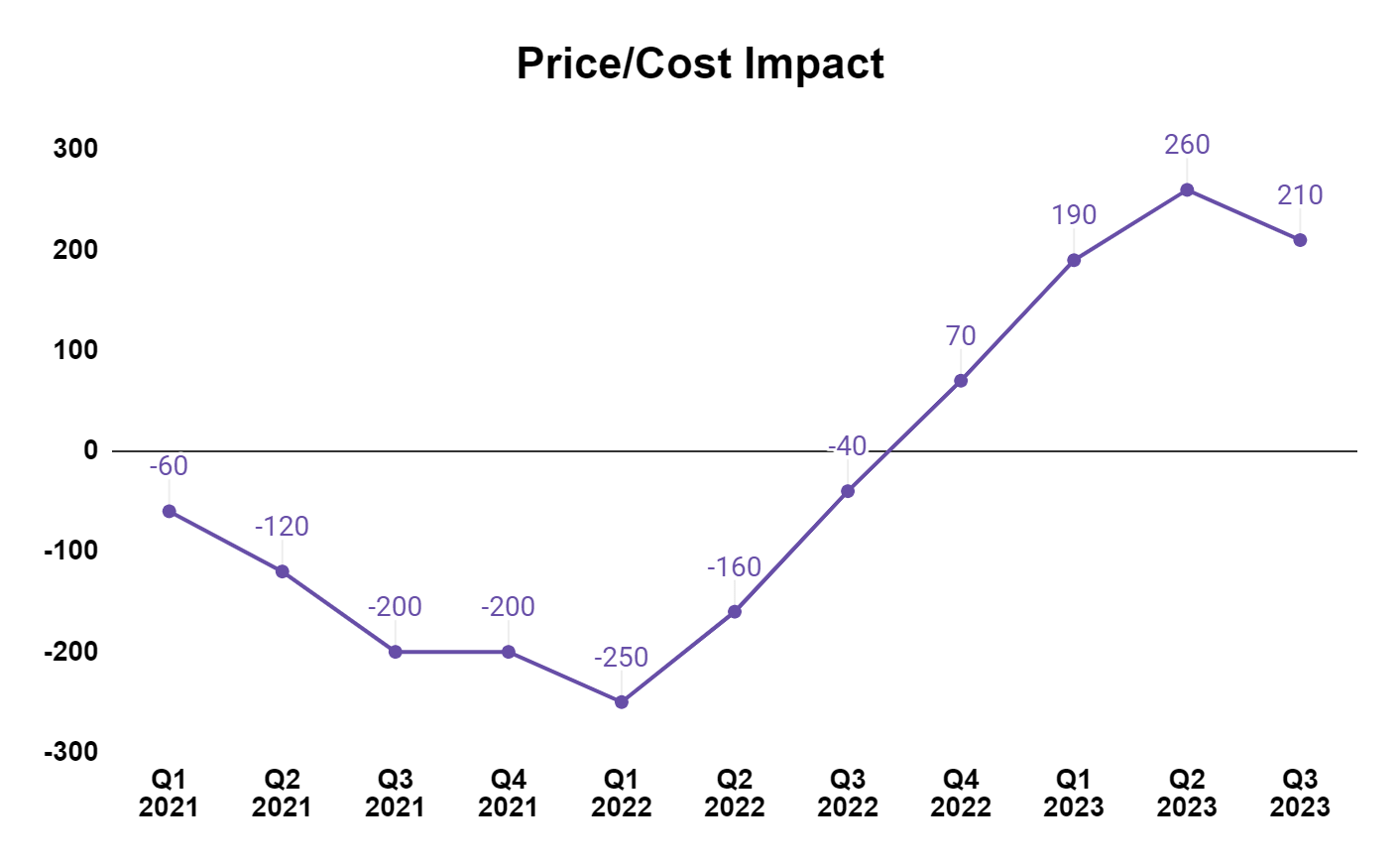

Looking forward, the carryforward impact from recent price increases as well as cost reduction initiatives should continue to help the company margins.

ITW Price Cost Impact (Company Data, GS Analytics Research)

{kind=link}

Management has a long-term target to reach an operating margin of 30% by 2030 indicating further upside as they continue to work on enterprise initiatives focused on cost reduction and productivity improvement. Further, the company typically has incremental margins in the 35% to 40% range. So, once the near-term macro headwinds fade and growth accelerates from the next year, the benefits of volume leverage should start flowing through the margin line as well. So, I am optimistic about the company’s margin growth prospects.

Valuation and Conclusion

ITW is currently trading at 22.90x FY23 consensus EPS estimates of $9.75 and 21.75x FY24 consensus EPS estimates of $10.26, which is at a discount versus the company’s 5-year average forward P/E of 24.72x. Further, the company has a good forward dividend yield of 2.51% and a good track record of increasing dividends regularly.

The company has good growth prospects benefiting from strength in the majority of its end-market, inventory destocking headwind easing by mid-2024, China reopening gaining momentum, product innovation, and increasing market share. The margins should also see gains from the carryover impact of recent price increases and cost-reduction initiatives in the near term. In the long run, benefits from the company’s enterprise initiatives along with volume leverage should aid margin growth. These promising growth prospects, combined with attractive dividend yield and reasonable valuation, make ITW stock a buy.

For further details see:

Illinois Tool Works: A Good Buy At Current Levels