XLI - Illinois Tool Works: Coasting Well But Tighten Your Seat Belts

2024-01-08 14:35:22 ET

Summary

- Illinois Tool Works stock has delivered decent mid-teens returns over the past year, outperforming the Industrial Select Sector SPDR Fund.

- The company has shown commendable financial progress, with room for further improvement on the operating margins and FCF front, which could end up improving even the dividend theme.

- Valuations are no longer attractive, particularly considering the degree of medium-term earnings growth.

- Developments on the charts signal some caution.

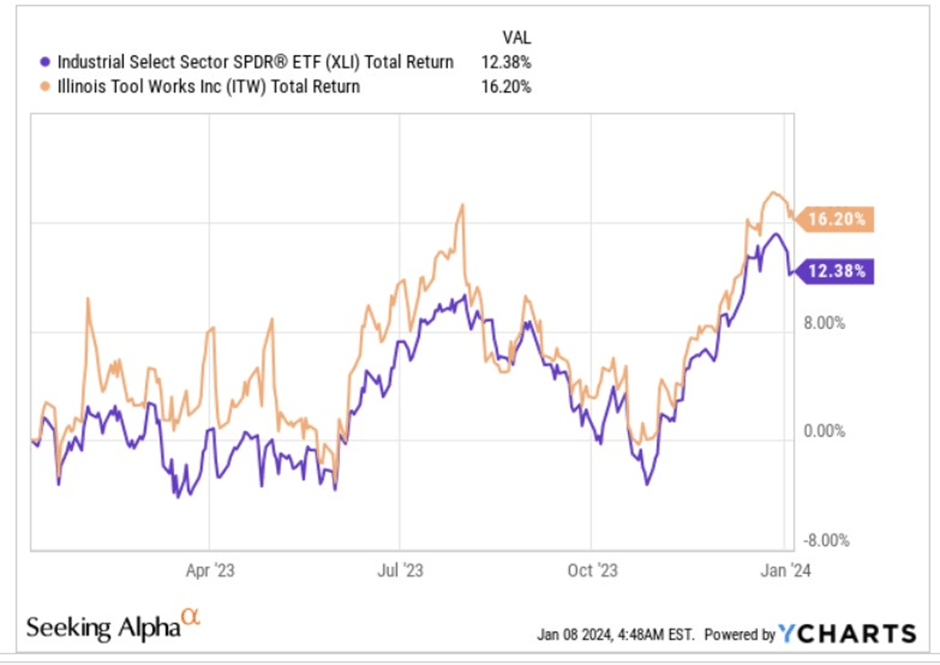

Decent Alpha Over The Past Year

The stock of Illinois Tool Works (ITW), a global manufacturer of industrial products and equipment, has done relatively well over the past year; during this period it has managed to deliver returns within the mid-teens threshold, and consequently also outperform the Industrial Select Sector SPDR Fund (XLI), a product which focuses solely on the industrial stocks of the S&P500.

{kind=link}

Commendable Financial Progress With Scope For Further Improvement

{kind=link}

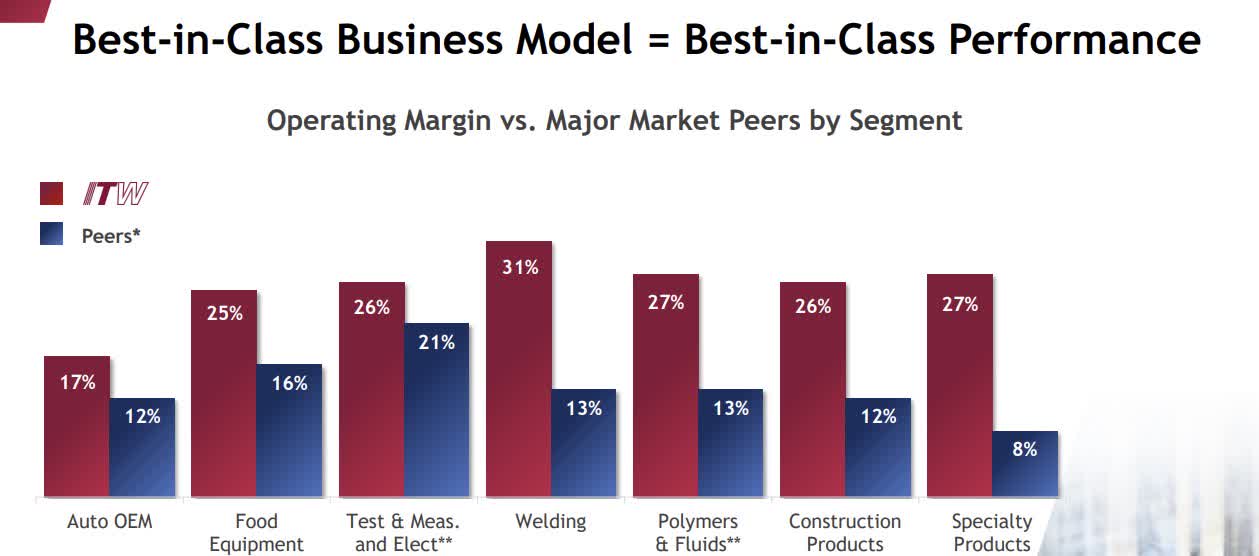

First, it's important to consider that structurally, ITW's operating margin profile across its various operating segments, is already at an elite level versus its largest peers, yet still, the company continues to show room for improvement and beat its high standards.

ITW's long-term goal (through 2030) for its operating margin is to facilitate incremental progress towards 35-40%, and as of 9M-23 we've already witnessed tremendous progress on this front, with the company delivering close to 200bps of YoY improvement (the 9M-23 EBIT margin came in at 25.1%).

The conditions here deserve special mention as the company has been able to facilitate margin progress, even though its highest-margin segment by far- Welding (31% margins and the third largest contributor to the overall group EBIT profile) has only witnessed 2.7% topline growth as of 9M-23 and most recently in Q3, organic revenue actually fell by -2% .

Overall margin progress has been abetted by ITW's ongoing enterprise strategy (for instance in Q3 this contributed 140bps of improvement, following 130bps of improvement in Q2) where management has pruned underperforming commoditized product lines, simplifying the business, doubling down on strategic sourcing, deeper innovation, and crucially accelerating organic growth by re-applying the company's proprietary 80/20 front to back process.

For the full year, management expected to deliver over 150bps of improvements (at the mid-point) with around 100bps of improvement down to the enterprise strategy alone. Besides the enterprise strategy, ITW has also been extracting some benefits from favorable price/cost dynamics as the inflationary environment ebbs, but this tailwind likely peaked in Q2-23 (216bps of improvement), and could be less of a support going forward, given the high base.

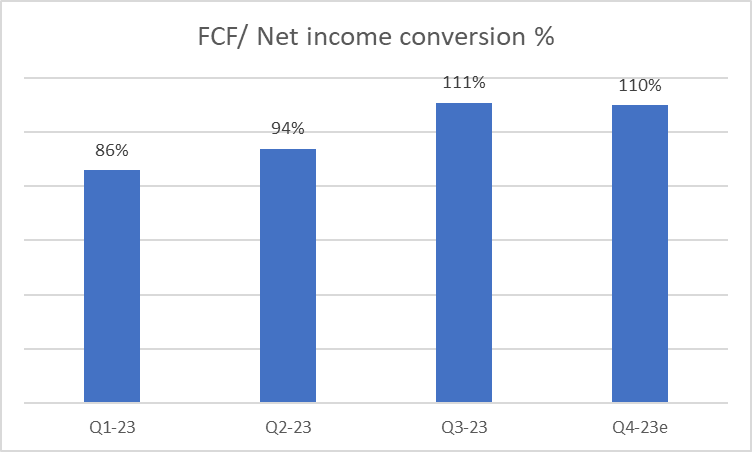

Besides margin improvements, the other key highlight is how well the company is now executing on the free cash flow front. Note that ITW's FCF per annum had been on a downward trajectory for the last two years, but within the first nine months of 2023 itself, it had already delivered a 12% improvement over last year's entire FCF total.

10K and 10Q

Besides margin improvements, there's also been a great deal of progress on the working capital front with the net income to FCF conversion improving every quarter. It stood at only 86% in Q1, but by Q3 it had come in an impressive 111%. Management suggested that the FY figure would be closer to 100% so this implies that even the Q4 conversion could be as impressive as Q3.

{kind=link}

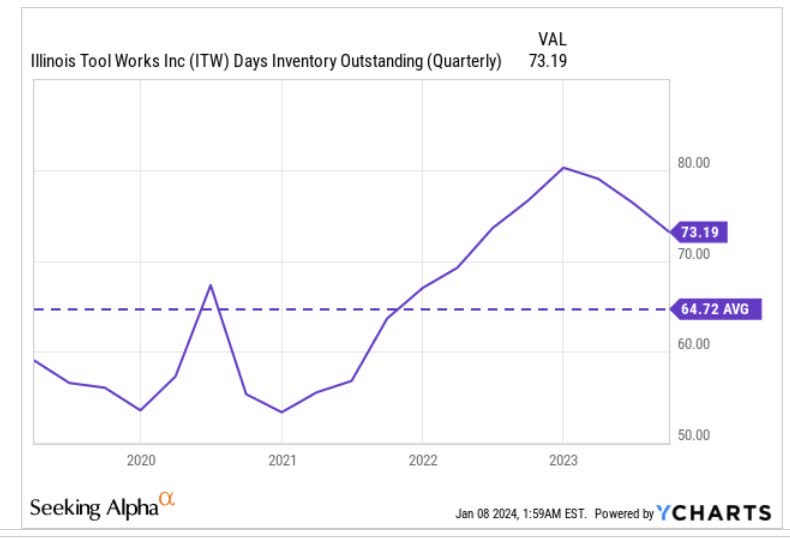

ITW's inventory buildup had been a drag on the operating cash flow for the last two years, but now over the last four quarters, it has been a useful source of cash. Now, some of you may think that these improvements have been going on for quite some time, and there's only so much one can extract, but we would point to ITW's current days in inventory position to highlight how improvements can still be made. As things stand the DIO is still quite elevated at 73 days and is still around 12% off the 5-year average of 65 days.

{kind=link}

In addition to better inventory management, we also see room to get better on the receivables front, which in fairness, is actually a bigger component of ITW's total current asset base (50% of total current assets as opposed to 28% linked to inventories). ITW's management of its receivables had been sucking out cash for six straight quarters until Q3-23 when it reversed that trend with a positive cash contribution.

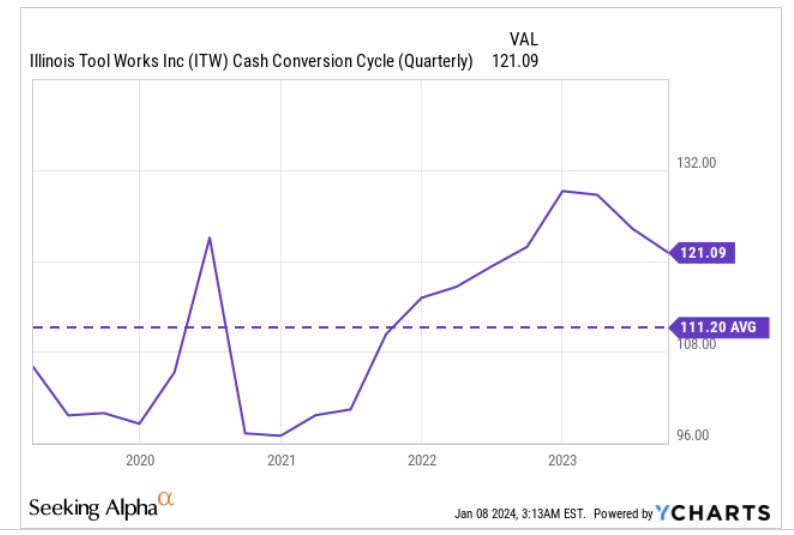

Looking ahead, investors can be hopeful of further progress on the FCF, as the overall cash conversion cycle of 121 days is still around 9% higher than its long-term average.

{kind=link}

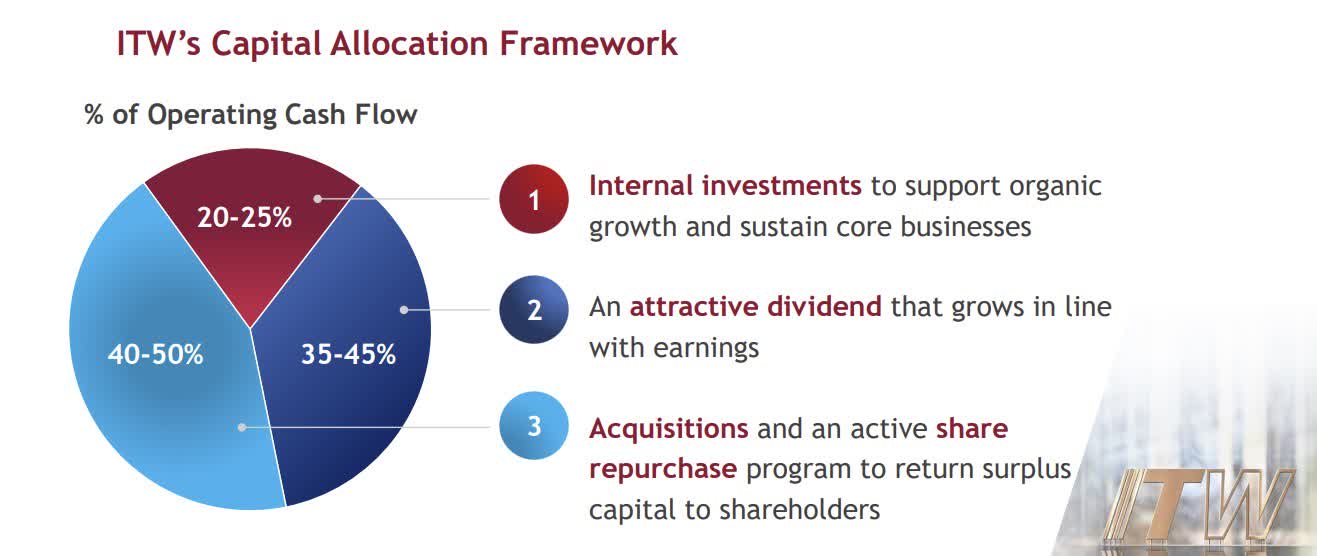

Superior cash generation means ITW's dividend profile could also be on the cusp of being enhanced even further, as it plans to divert 35-45% of its operating cash flow here.

{kind=link}

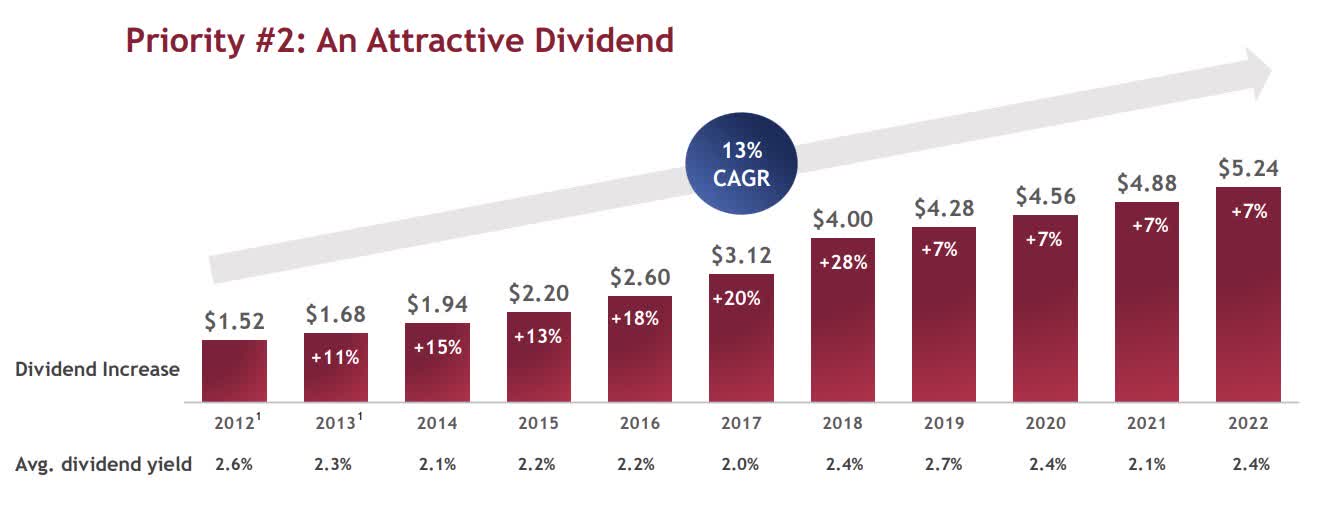

For context, ITW has a tremendous track record of raising dividends for 60 years, which accounts for nearly two-thirds of its entire history as a corporation! However, note that in recent years, the degree of annual hikes (including the most recent one in September ) has only come in at the 7% threshold, considerably well below the double-digit hikes that characterized the period from 2013 to 2018. Given the onset of superior cash generation, we "may" see a return to double-digit hikes from next year.

{kind=link}

Closing Thoughts- Not A Great Buy At These Levels

Despite the ongoing execution, we would be hesitant to lap up ITW stock at current levels, as we don't believe it offers great value for the earnings potential.

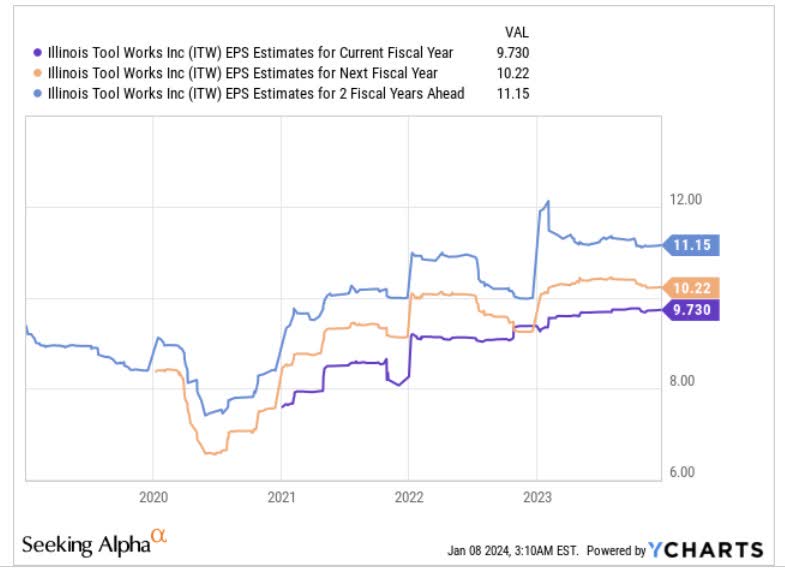

If one looks at how consensus estimates are positioned over the next two years (through FY25) the takeaway is that this is a 7% earnings CAGR business.

{kind=link}

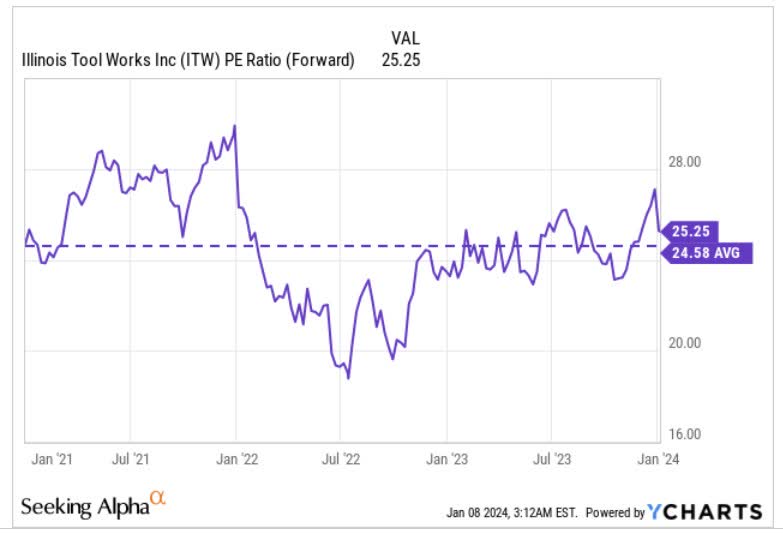

For that degree of earnings growth, it feels a bit much for this business to be priced at over 25x forward P/E, which translates to a 3% premium over the stock's 5-year average.

{kind=link}

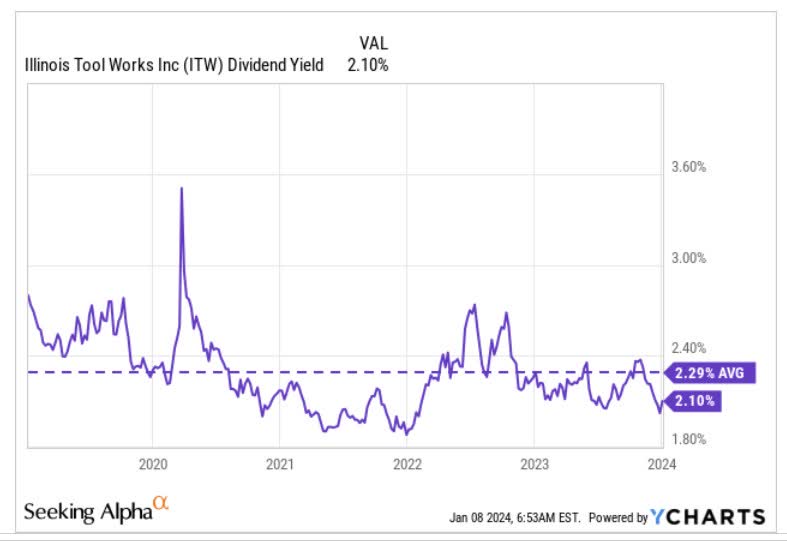

Then, we can appreciate that a lot of investors gravitate to ITW solely for its dividends, but at the current price, the yield also looks sub-par at only 2.1%, around 19bps lower than its 5-year average.

{kind=link}

The chart below highlights how ITW's stock is positioned relative to other dividend aristocrats of the S&P 500. As things stand, ITW looks relatively overbought (the relative strength ratio is now at levels last seen in Q4-21 from where there was a reversal) and is unlikely to benefit from rotational interest from those focused solely on dividend aristocrat options.

{kind=link}

Finally, if we review ITW's weekly price imprints over the last three years, it appears that the stock has been moving in the shape of a rising wedge pattern, which is not ideal. Within the wedge, the price is also a lot closer to the upper boundary than the lower boundary, putting the reward-to-risk equation in an unfavorable spot. Compounding the issue, we've also seen the stock recently hit a double top at around the $265 level, which could point to some weakness ahead.

{kind=link}

For further details see:

Illinois Tool Works: Coasting Well, But Tighten Your Seat Belts