ITW - Illinois Tool Works: Quality Business Model But Limited Upside Potential

2023-07-12 05:27:46 ET

Summary

- Illinois Tool Works operates a unique business model, focused on innovation and entrepreneurship.

- Management is implementing a strategy to achieve consistent growth in the coming years, with scope for margin improvement.

- The company outperforms the wider machinery industry on a profitability basis while remaining resilient to economic conditions.

- ITW stock is trading at a premium to its historical average multiple, which may be justified to an extent, but does not suggest further upside.

Investment thesis

Our current investment thesis is:

- ITW operates a unique business model, which should support continued growth despite its mature position.

- We believe growth should slowly begin to improve, as will margins.

- ITW valuation implies a c.15% premium of its last 10 years, which looks about justifiable but leaves no alpha.

Company description

Illinois Tool Works Inc. ( ITW ) is a global manufacturer and seller of industrial products and equipment. The company operates through seven segments, including Automotive OEM, Food Equipment, Test & Measurement and Electronics, Welding, Polymers & Fluids, Construction Products, and Specialty Products.

Each segment focuses on specific product categories and serves different end markets. Their product offerings include components, fasteners, assemblies, equipment, consumables, and maintenance services for various industries.

Illinois Tool Works distributes its products directly to industrial manufacturers and through independent distributors.

Share price

ITW's share price has outperformed the market in the last decade, as continued robust financial results have driven value for investors. Given its nature, outsized returns are unlikely, however, the share price reflects the outcome of consistent improvement.

Financial analysis

{kind=link}

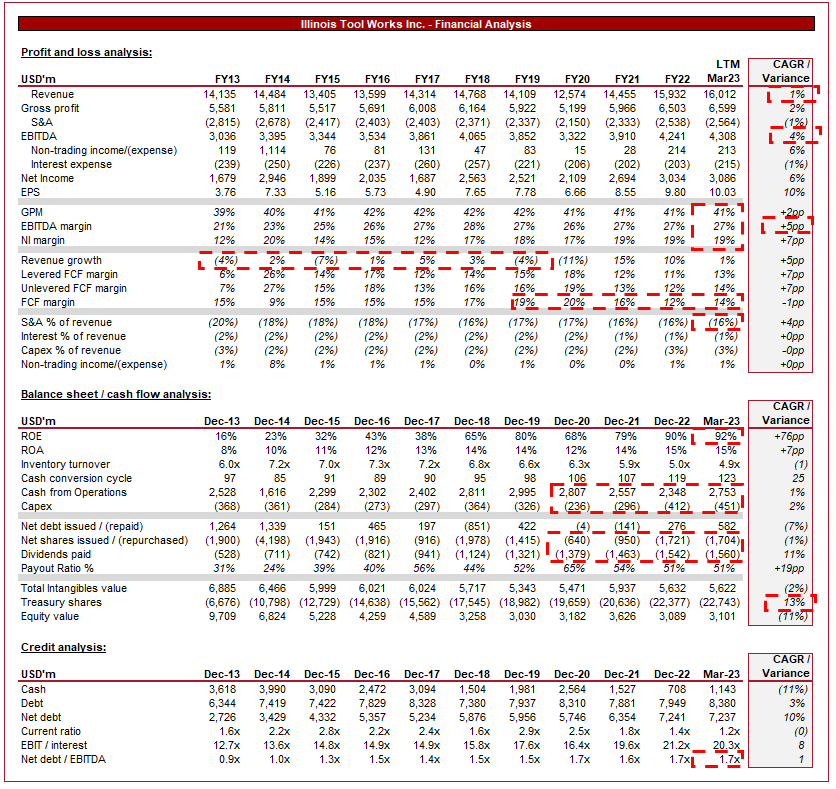

Presented above is ITW's financial performance for the last decade.

Revenue & Commercial Factors

ITW's revenue has only marginally increased over the last decade, with a CAGR of 1%. During this period, revenue has turned negative 4 times (once due to Covid-19), implying some level of weakness in the company's commercial position but also a reflection of divestitures. This said, the overarching trajectory of the business is positive, although slow.

Business Model

ITW's Management attribute much of the company's success to its unique business model, which it believes positions the company well to continue its current trajectory, despite its size and maturity.

ITW's various segments operate an "80/20 Front-to-Back" process. This is a generic efficiency tool that was developed in the 80s, however, ITW has improved and refined it. This operating system focuses on the largest and best opportunities (the "80") while eliminating cost, complexity, and distractions associated with less profitable opportunities (the "20"). The results of the system are operational excellence and innovation, which translate to financial improvement.

In conjunction with the above, ITW positions itself as the go-to problem solver for its key customers by understanding their needs and creating unique solutions. This is referred to as "Customer-back innovation". The company starts at its "80" customers and seeks to innovate away key problems its customers currently face. Customer insights gathered through the 80/20 process drive innovation and have resulted in over 18k patents.

Finally, ITW businesses have flexibility within the ITW Business Model framework to customize their approach and serve specific customer needs. This is a noticeable departure from the traditional business model, where uniformity and structure are immediately implemented as a means of simplifying control. Once again, this is orchestrated to foster an innovative culture within the business, allowing for improvements to be achieved.

We really like the business model. The company reiterates it whenever possible and it is clear why. To truly instill such a culture in an institution of its size, this must be constantly reinforced. We believe this is a primary reason for the success of the business during the historical period. This said, the company has not been perfect. Growth has clearly faltered and efficiency metrics have weakened.

Reinvigorating growth

Management has outlined numerous factors to achieve a return to consistent growth.

Firstly, (and interestingly) Management has largely divested of businesses in commoditized industries, seeking to focus on industries with scope for diversification and value-add. The belief is that growth is higher in these avenues. This looks to be a shrewd decision. The view on growth is simplistic but the impact of high competition in a commoditized industry on margins is not positive, so we like this decision.

Further, the business focused on developing the 80/20 structure among its core divisions, scaling these from the bottom up. This involved an investment in "front-office" personnel, those who can drive greater innovation and customer wins.

Finally, the business has sought to achieve operational improvement through a focus on sourcing, delivering a 1% improvement annually since 2022.

We like the company's growth strategy but similar to its business model, it noticeably lacks defined performance obligations. An improvement in culture and increased recruitment in developmental areas is a positive, however, we would prefer to see more specific action items.

Manufacturing industry

The manufacturing industry is cyclical in nature, given businesses only want to invest when the outlook is positive, and they are easily able to easily obtain financing. The general trajectory, however, is overarchingly positive. Increased global innovation and population growth will mean continued infrastructure investment is a necessity in order to support the future.

Geopolitical tensions, trade disputes, and policy changes can introduce uncertainties and affect the machinery industry's global market dynamics. This looks to be heightened in recent years, as relationships deteriorate between global powers. We suspect this will drive increased investment by US firms in domestic infrastructure.

The COVID-19 pandemic has highlighted the importance of resilient supply chains and the ability to be flexible. Many businesses were caught out by overseas production facilities, unable to ship their products to their required locations. Our view is that investment in supply chain resilience could support increased demand for a range of products ITW offers, such as Welding equipment.

Similarly to other industries, the machinery industry has experienced a trend of consolidation, with companies seeking strategic acquisitions to expand their product portfolios, geographic presence, and technological capabilities. ITW has engaged in M&A consistently across the historical period where opportunities have arisen. We believe this should be a focus for the business, as micro-M&A of niche businesses could support margins and growth.

Economic & External Consideration

Current economic conditions represent a near-term headwind. This is because the cost of financing has increased, discouraging new construction projects, as well as contributing to increased financial struggles for many businesses.

ITW's Construction Products segment, for example, has a large exposure to the home building industry, a sector that has been materially impacted by high rates.

Despite these concerns, ITW continues to grow, with Management guiding 3-5% organic growth for FY23. This is an impressive level of resilience for the business.

We believe interest rates will remain elevated for several additional quarters, as inflation continues to decline.

As a global business, ITW faces material FX risk, as overseas income is translated to dollars. This has the potential to deteriorate earns.

Margins

ITW's margins are extremely good. It has a GPM of 41%, EBITDA-M of 27%, and a NIM of 19%.

Margins have improved over the last decade, as the business has benefited from scale economies, a favorable product mix as low-margin businesses are divested, and operational investment by Management.

We expect further margin improvement in the coming years, through innovation and operational gains.

Balance sheet & Cash Flows

ITW has experienced a reduction in its inventory turnover, partially contributing to an increase in its CCC. This is an operational inefficiency that is tying up cash.

Although this is detrimental, its FCF margin has remained flat across the historical period. The level of FCF is extremely good, allowing for a consistent 2-3% Capex investment.

ITW's use of debt has only marginally increased over the historical period, with its ND/EBITDA ratio increasing to 1.7x. At this level, the company can raise further debt without being overly concerned about solvency.

Distributions have been large for several years, with both dividends and buybacks. This is owing to a combination of divestiture cash, strong cash conversion, and small debt raises. Given the depletion of cash, we suspect distributions will need to be reined in.

Outlook

{kind=link}

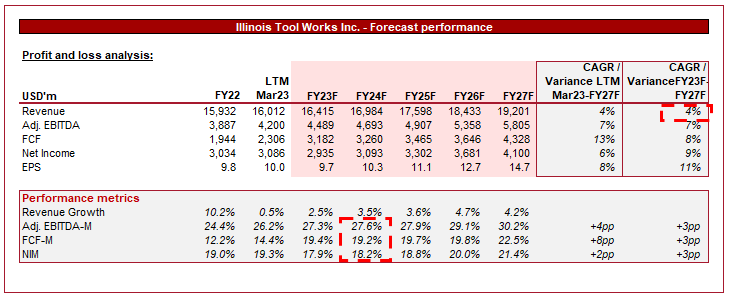

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are expected organic growth in line with Management's forecast, 4-5%, which we believe is a reasonable expectation.

Margins are forecast to materially improve. This is beyond the level we expect in this timeframe but remains a potential upside in our thesis.

Industry analysis

Machinery industry (Seeking Alpha)

{kind=link}

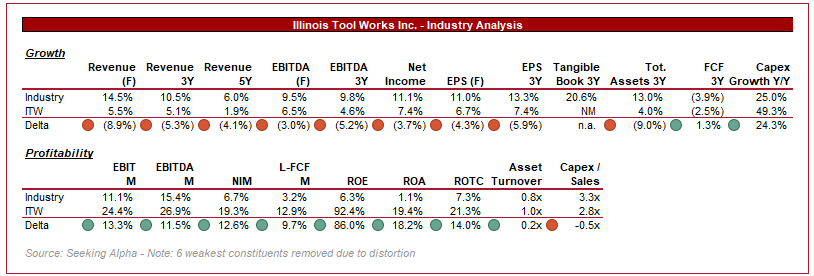

Presented above is a comparison of ITW's growth and profitability to the average of its industry, as defined by Seeking Alpha ( 68 companies).

From a growth perspective, ITW underperforms noticeably. This is an established weakness with the business currently and looks set to continue. This comparison is muddied somewhat by growing businesses (as is the profitability comparison).

ITW performs far better when comparing profitability, with an EBITDA-M 11.5% higher than the average. Given the maturity of the machinery industry, we strongly favor margins to growth.

Valuation

Valuation (Capital IQ)

ITW is trading at 19x LTM EBITDA and 18x NTM EBITDA, a c.16% premium to its 10Y historical average.

For a mature business such as this, valuation is critical. Investors are unlikely to get a discount, and equally will not be bailed out of stagnation.

We believe there is little justification for a premium beyond c.15% to its historical average multiple, given the lack of tangible development. Margin improvement, scope for better growth, and continued innovation are critical, and valued, but this is not materially different from the investment in the last decade. The resilience of the business has not changed, and unfortunately, neither has its growth trajectory.

ITW has been a great business in the last decade and remains so. Importantly, at a similar level.

Final thoughts

ITW is a fantastic business. It has a wide moat due to its level of expertise, product development, and scale. Our view is that a business such as this has the potential to be a mainstay in any portfolio, but to generate alpha, the price must be correct.

There are several positives and concerns with the business. Broadly, they negate each other in our view, with slight upside (Margin improvement and potential for slightly better growth). Based on this, a c.15% premium looks the top end of fair.

For further details see:

Illinois Tool Works: Quality Business Model, But Limited Upside Potential