XLI - Illinois Tool Works: Quality Fundamentals And Technicals But Shares Priced For Perfection

2024-01-10 07:03:59 ET

Summary

- The Industrials sector is a leader in the market away from the tech space, offering hope for those concerned about narrow leadership.

- I have a hold rating on Illinois Tool Works due to its premium and high valuation and somewhat sluggish EPS growth.

- ITW is a diversified industrial conglomerate with strong margins, but some macro headwinds could pressure profits.

- While its technical picture is constructive, I highlight important price levels to monitor ahead of Q4 results due out in early February.

The Industrials sector has helped lead the market over the past year. Now, you might scoff at such a comment, but aside from the glamour growth areas of Information Technology, Communication Services, and Consumer Discretionary, Industrials is the leader. Many stocks in the group can benefit from key investment packages put through by Congress over the past few years while the diverse group offers a ray of hope to those concerned about the market's purported narrow leadership in recent years.

I have a hold rating on Illinois Tool Works (ITW). The stock has a mid-20s P/E, and given somewhat sluggish EPS growth over the coming quarters, it is priced for near-perfection while ITW's technicals and momentum are generally bright spots.

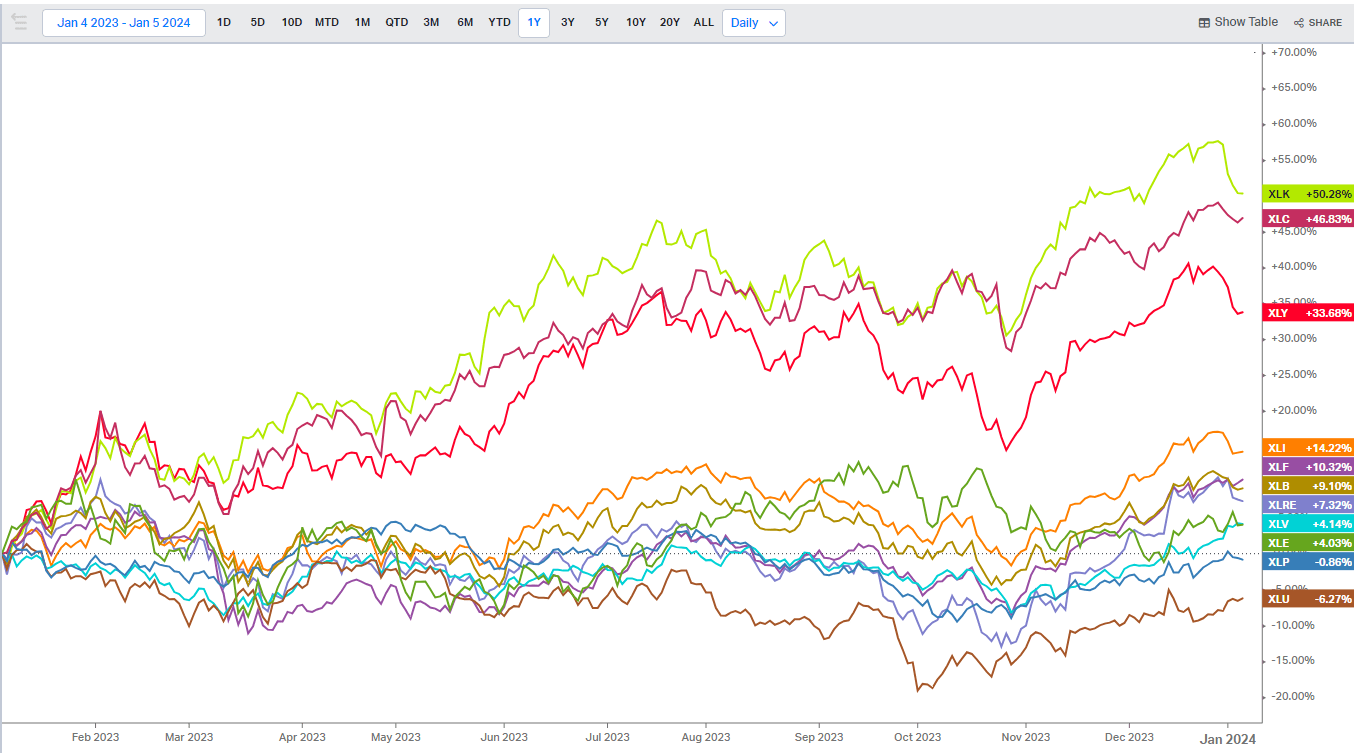

Industrials Best Non-TMT Sector YoY

{kind=link}

According to Bank of America Global Research, ITW is a highly diversified industrial conglomerate that designs and manufactures fasteners, components, equipment, consumables, and a variety of specialty products and equipment for a broad array of industries. Across its seven segments, Auto OE accounts for 19% of sales, Food Equipment 14%, Test & Measurement 16%, Welding 11%, Polymers & Fluids 13%, Construction Products 14%, and Specialty Products 13%. By region, North America accounts for about 52% of sales, EMEA 27%, APAC 19%, and SA 2%.

The Illinois-based $77.6 billion market cap Industrial Machinery & Supplies & Components industry company within the Industrials sector trades at a high 26.5 forward non-GAAP price-to-earnings ratio and pays an above-market 2.2% forward dividend yield . Ahead of earnings due out in early February, shares trade with a low implied volatility percentage of 16.9% while short interest on the stock is material at 2.9% as of January 5, 2024.

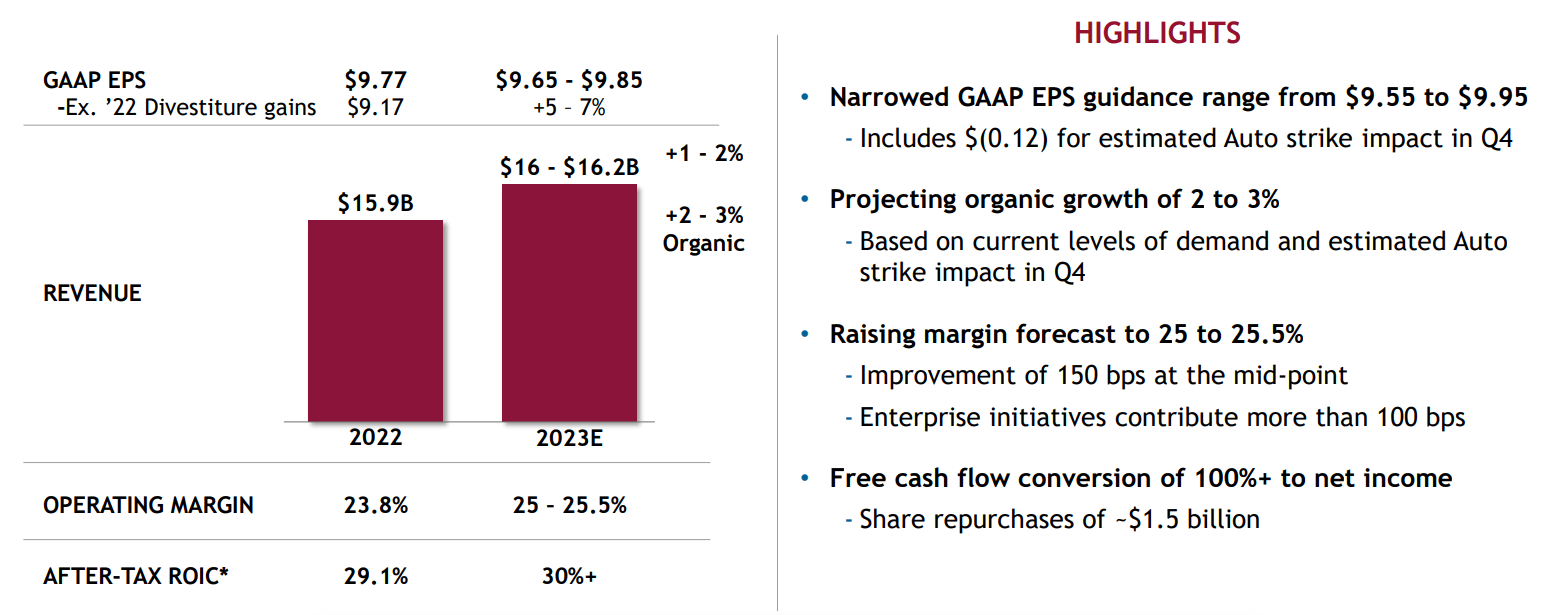

Back in October, ITW reported a mixed quarter. Q3 GAAP EPS of $2.55 beat the Wall Street consensus outlook by a dime while revenue of $4 billion, up fractionally from year-ago levels, was a significant $100 million miss. The firm narrowed its FY 2023 EPS guidance range to $9.55 to $9.95. Using those numbers, ITW trades 26.6x earnings. Of course, it's more useful to use out-year estimates and incorporate growth projections, in addition to taking a look at a company's free cash flow and yield.

Furthermore, ITW sports very strong margins, but shares are priced with that assumption. In its Q3, ITW encountered some cyclical headwinds in end markets - organic growth was negatively impacted by some inventory destocking and mild weakness in residential and electronics markets. A transitory trouble spot was the UAW strike while consumer's strength is a question mark for this year. Listen up to what ITW's executives say about margin expectations in the upcoming Q4 report.

Key risks for the company include weaker auto sales, reduced economic growth, and higher costs from lingering economy-wide inflation.

2023 Financial Guidance

{kind=link}

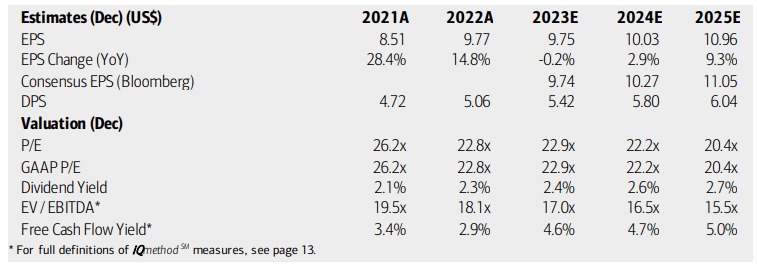

On valuation , analysts at BofA see earnings climbing at a slow pace this year, but per-share profits are expected to accelerate in 2025. The current consensus expectation, per Seeking Alpha, shows 2024 operating EPS up 5% in 2024 to above $10 with a high-single-digit growth rate in the out year. Sales growth is seen in the low single digits, though.

Dividends, meanwhile, are forecast to climb at an impressive rate over the coming quarters on this high-yield blue chip stock. Still, its earnings multiple is lofty while ITW's EV/EBITDA ratio is a few turns above that of the broader market. Free cash flow is a bright spot, and the FCF is seen rising in the years ahead.

ITW: Earnings, Valuation, Dividend Yield, Free Cash Flow Forecasts

{kind=link}

If we assume $10.30 of non-GAAP EPS over the coming 12 months and apply a 24 multiple, significantly above that of its sector, though under ITW's 5-year average, then shares should trade near $247. Given the stock's growth rate, I find it a stretch to give ITW a multiple any higher than 24 - just take a look at the current forward non-GAAP PEG ratio - it's very elevated. It will be important for the company to execute well and produce strong earnings to continue to have that high P/E. Still, with a strong dividend yield and solid free cash flow, some valuation premium is warranted.

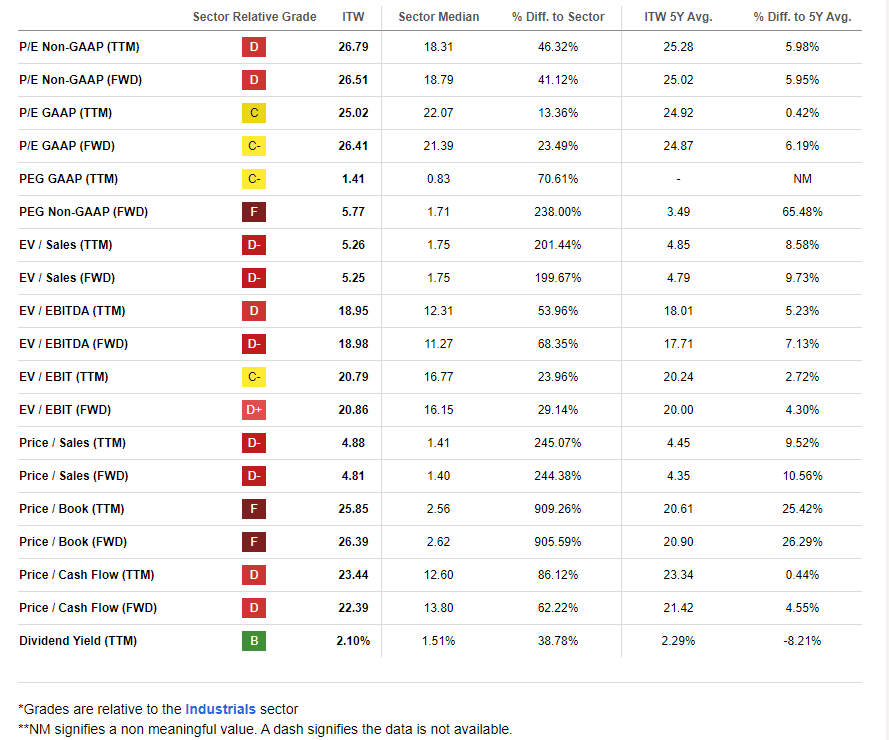

ITW: Broadly Expensive Valuation Metrics

{kind=link}

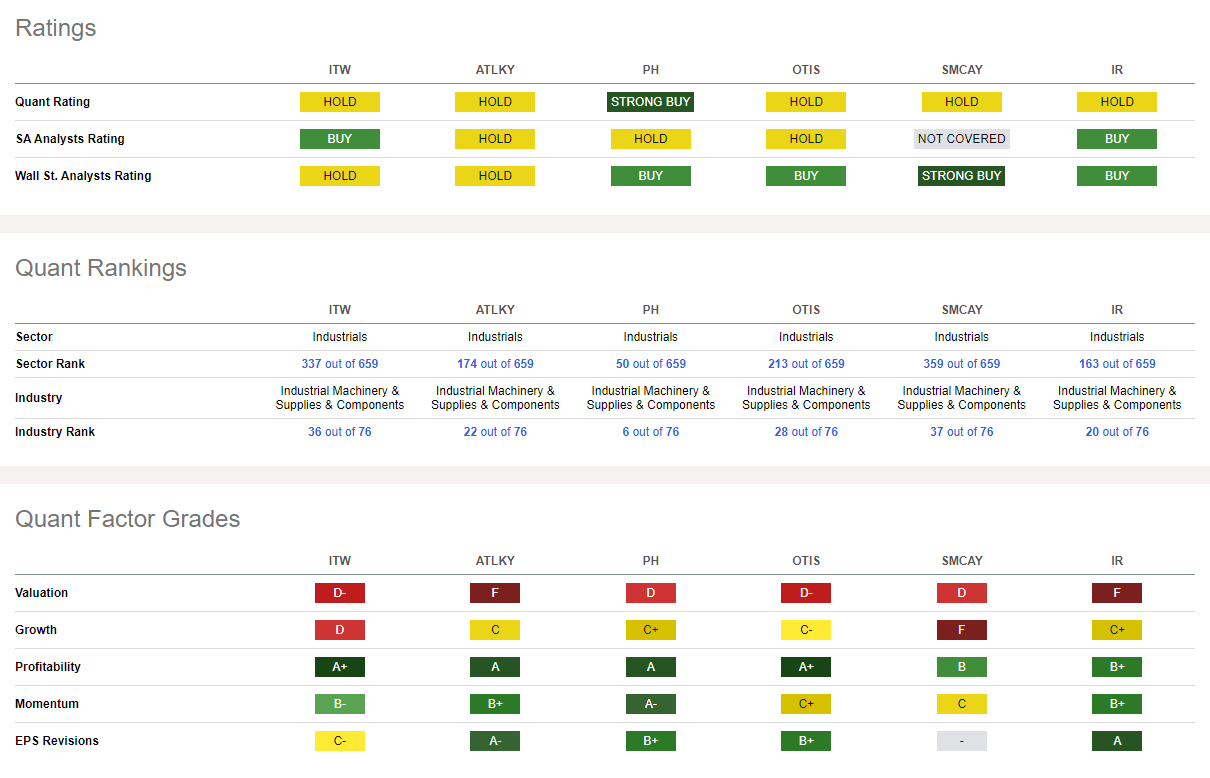

Compared to its peers , ITW's valuation is actually not all that extreme, so applying some relative value perspective is prudent. The firm's growth trajectory is also lackluster though profitability trends are very positive, which should be considered by GARP investors and those focused on owning quality businesses. EPS revisions have generally been negative while share-price momentum is robust. I will detail key price points to watch later in the article.

Competitor Analysis

{kind=link}

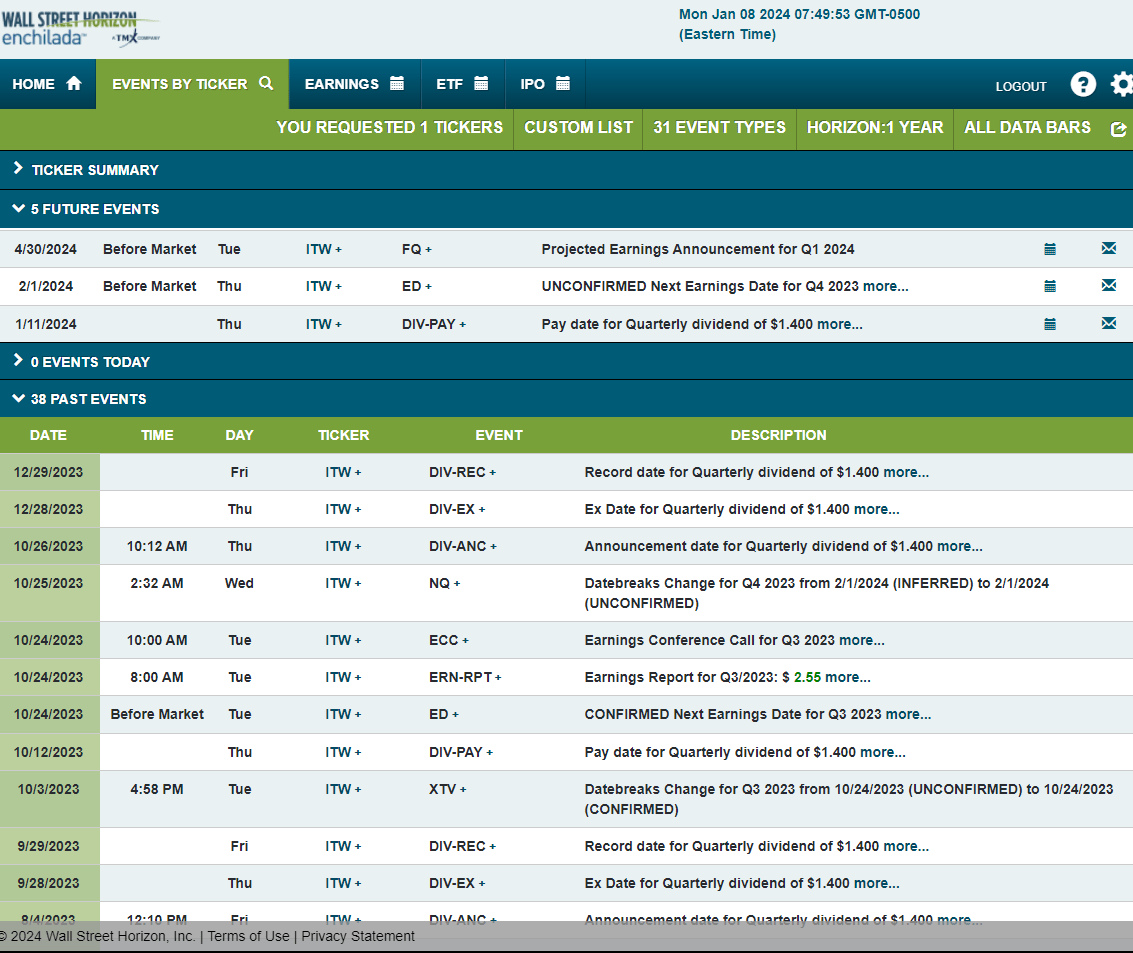

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q4 2023 earnings date of Thursday, February 1 BMO. Before that, the company has a dividend pay date of Thursday, January 11.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

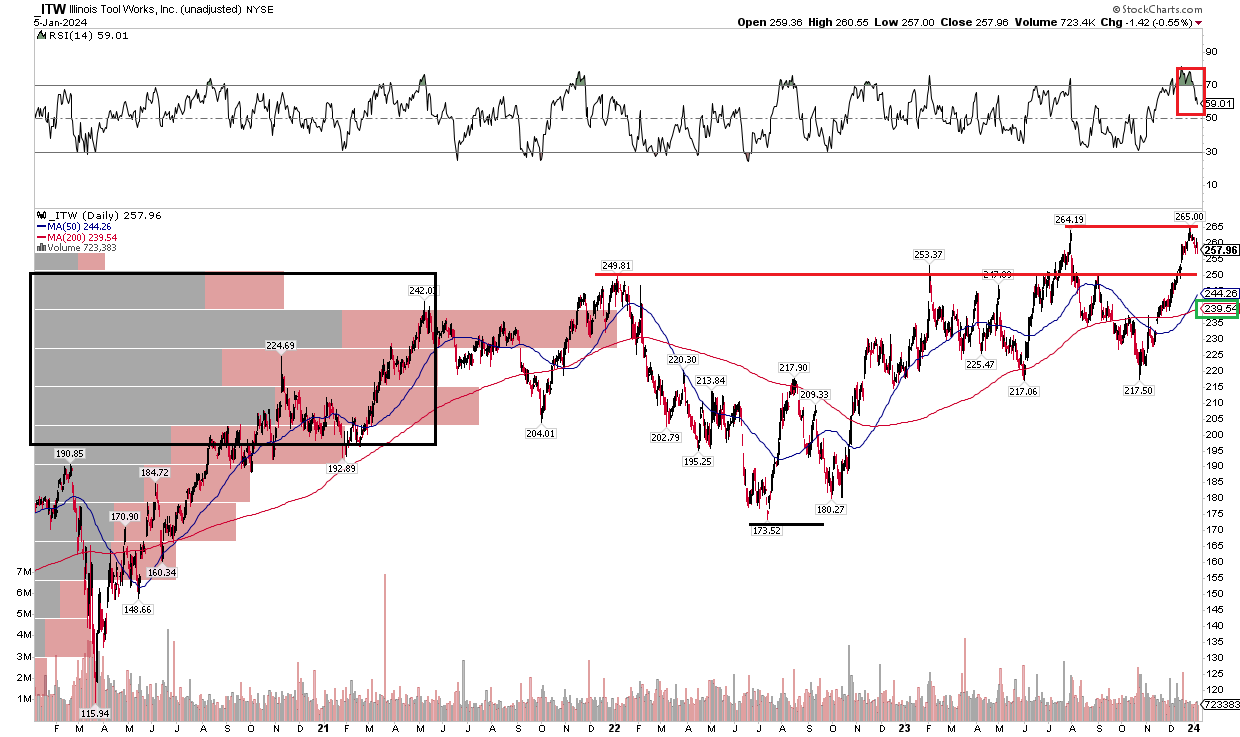

With the stock priced for a rosy outlook, the technical situation is generally healthy. Notice in the graph below that ITW has been a market leader in a risk-on and cyclical sector since notching a low in June 2022, ahead of the S&P 500's bear-market bottom the following October. I would like to see more vigor with the recent breakout, however. When a stock price simply meanders to a new high, without much volume of momentum jump, profit-taking can sometimes lead to a lower share price. I see near-term resistance in the mid-$260s, but if you zoom out, you will see that the $250 mark is pivotal. Based on the $173 low in 2022, we can take that $77 range and add it on top of the breakout point to arrive at an eventual bullish upside price target of $327.

With a long-term 200-day moving average that is positively sloped, the trend favors the bulls. A concerning indicator, though, is the RSI momentum gauge at the top of the graph - the stock's momentum has dropped off significantly after a strong rally from late October through late last year. Still, with a high amount of volume by price in the $190 to $250 zone, pullbacks should be seen as buying opportunities.

Overall, ITW's chart is constructive despite soft momentum as the stock tests the 2023 high.

ITW: A Broad Uptrend, Eyeing Momentum Trends, $327 Measured Move Target, $250 Support

{kind=link}

The Bottom Line

I have a hold rating on ITW. The technical situation is generally healthy, but its valuation is stretched in my view given what earnings growth is projected to be.

For further details see:

Illinois Tool Works: Quality Fundamentals And Technicals, But Shares Priced For Perfection