ITW - Illinois Tools Works: Right Time To Have This High Margin Company In Your Portfolio

2023-06-22 21:02:23 ET

Summary

- ITW's high-margin profile stands out as one of the best in the industrial machinery sector. This is a result of a long strategic shift, driven by several core initiatives.

- Despite macroeconomic uncertainties, the potential impact on ITW's overall result is likely to be limited, as enterprise initiatives and price/cost relationship are expected to drive most of the margin improvements.

- Investors that hold shares of this company can still achieve sizable capital appreciation over time, if history is any guide.

After recovering somewhat over the past weeks, broader market valuations are now back to historical levels, as better than expected earnings and softening inflation data have improved investors' sentiment for the time being.

Business environment is still challenging tough, as a worse than expected soft landing scenario can trim growth prospects later in 2023 or early 2024.

Meanwhile, Illinois Tools Works Inc. ( ITW ) business prospects remain strong, underscored by top-tier margins and a diversified operation across several end markets. Therefore, although short-term upside seems limited from a relative valuation perspective, ITW is an attractive option to give investors exposure to the growth potential of the industrial sector. On top of it, its earnings predictability is a positive for the shareholder.

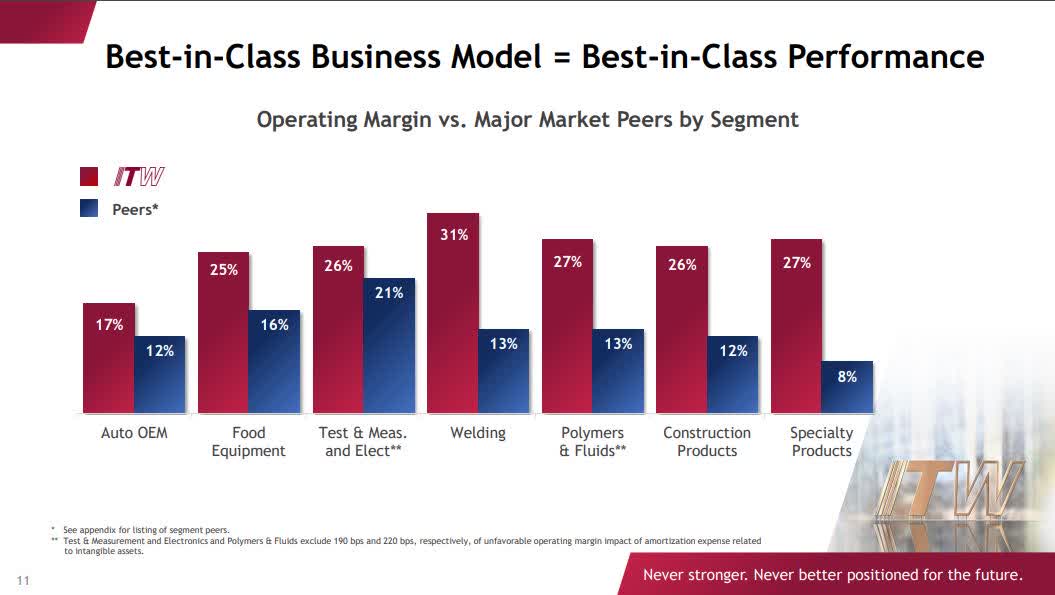

Top-tier Margins

There is no question that ITW's high-margin profile stands out as one of the best in the industrial machinery sector. As the picture below shows, ITW's operation margin in each of its business segment is well above the average of the peer group.

{kind=link}

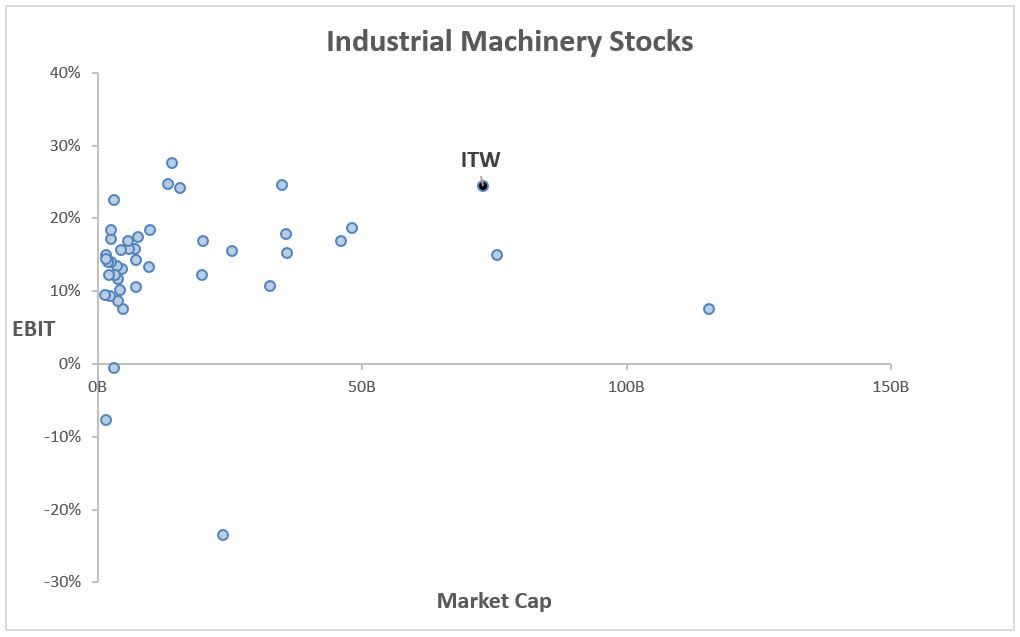

More broadly, we can see a similar picture when comparing ITW with nearly 40 industrial machinery companies with market cap above $0.5 B, as ITW's EBIT is higher than most companies in the group.

Data from Seeking Alpha, consolidated by the author

{kind=link}

This current position of ITW as a highly profitable business is a result of a long strategic shift, driven by several core initiatives, such as simplification of operational structure, divestiture of commoditized business and focus on more customer oriented, faster growth opportunities, including acquisitions over the course of last ten years, that boosted operation margin from nearly 16% to the levels seen today.

Core Initiatives to Boost Growth

ITW has also a long-term program to drive growth across the company aiming to achieve consistent 4%+ organic growth, while sustaining high-quality incremental margins at 35-45%.

In order to achieve this goal, the company is targeting 2-4% growth driven by the combination of market growth and share gain, and a growth of 2-3% from innovations based on customers' demands. The latter is an extension of an existing initiative that currently contributes roughly 2% of the annual organic growth.

This growth agenda seems well-supported, at least by some positive developments in ITW's biggest business units. In the food segment, for example, ITW has around 10-15% market share in a large addressable market estimated at $17-23 B. This is a material opportunity for a company that has gained share at a pace of 1-2% annually over the past 5 years.

There is a similar opportunity in the test & measurement and electronics segment. With $15-20 B addressable market and market share of nearly 15%, ITW can see solid growth here if it is able to maintain its historical 1-2% annual share gains accumulated annually during the same period.

Finally, in the automotive segment, ITW's biggest sales contributor, growth is primarily expected to come from share gains and new products to attend EV market, as ITW raises the relevant content per vehicle in the EV market, in an opportunity with potential to increase business from $400 M to $1 B in 5 years for the segment.

The Outlook for 2023 is Healthy

Long-term business strategy aside, the year 2023 started fairly well for ITW. In the first quarter, the company continued to show strong profitability, with operating margin jumping 150 bps to 24.2% on a year-over-year basis, primarily driven by enterprise initiatives that contributed with +100 bps, but also helped by an organic revenue growth of 5%, despite some weakness in certain end markets, such as polymers & fluids, construction and specialty products, that saw mid-single digit revenue declines during the period.

For the full-year 2023, while organic revenue growth is seen at 3% to 5%, operating margin is projected to be in the range of 24.5% to 25.5%, an increase of 120 bps over the mark of 23.8% reached in 2022.

Despite macroeconomic uncertainties, the potential impact in ITW's overall result is likely to be limited, as enterprise initiatives and price/cost relationship are expected to drive most of the margin improvements this year, rather than top-line growth itself.

On top of that, ITW's diversification across several segments (automotive, food, test & measurement/electronics, welding, polymers & fluids, construction and specialty products) is supposed to attenuate the impact of some end-market decline in the total result, absent a major recession going forward.

Valuation in Line with the Broader Market

After the recent stock rally, valuations have largely returned to the historical average. S&P 500's P/E is back to the 5-year average of roughly 25 and the same goes for ITW, as its P/E Forward now stands at 25.2, just 4% above its 5-year average of 24.2.

Extending this analysis to the peer group, we see a similar picture, as the P/E Forward average of the sub-set of S&P 500 composed by industrial machinery companies is nearly 24.1, just 4% below ITW's P/E.

While this signals that ITW upside is somewhat limited, we should not ignore that investors usually pay up for companies with good fundamentals. This is especially true during uncertain times, when most profitable companies like ITW are expected to trade at higher multiples on a relative basis.

That said, although industrial companies are generally more sensitive to economic cycles, and of course ITW is not immune to a potential mild recession, as many analysts foresee, later in 2023 or early 2024, my take here is that it is worth owning shares of ITW, looking to have exposure to the growth potential of the industrial sector, but with relatively earnings growth stability.

{kind=link}

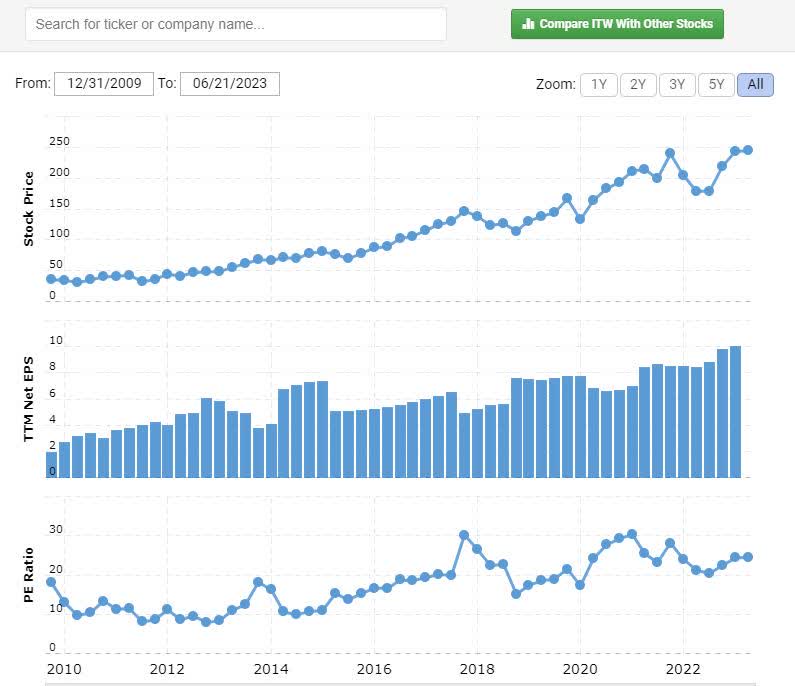

This chart above illustrates the trajectory of ITW stock prices, EPS and P/E since 2010, where we can see that EPS growth has been relatively stable over the recent years, even during the pandemic in 2020. More recently, stock prices have followed the broader market decline that started in Jan 2022, but have recovered to get close to historical highs last week, while P/E is still below previous peaks hit in 2017 and 2021.

Although shares of ITW will probably never experience the exuberance seen in the tech space driven by disruptive innovations like IA, for instance, investors that hold shares of this company can still achieve sizable capital appreciation overtime, if history is any guide.

For further details see:

Illinois Tools Works: Right Time To Have This High Margin Company In Your Portfolio