FLIN - India Fund: This Actively Managed Fund Still Offers Lots Of Positives

2023-11-15 12:44:50 ET

Summary

- Indian equities have been on a tear this year.

- Helped by its distribution policy changes, investors in abrdn's India Fund have outperformed the rest of the Indian large-cap fund complex.

- With India's fundamentals as strong as ever heading into an election year and potentially even an easing cycle in H1 2024, IFN remains poised for upside.

India's growth story has stayed remarkably resilient through the various external growth and commodity headwinds over the last year. Expect more of the same going forward as domestic strength, particularly in urban India, continues to buoy the economy. While agriculture-focused rural India has suffered some near-term road bumps due to the weather, the pending state/general election cycle presents a timely fiscal boost. As the latest CPI print (easing headline and core inflation) showed as well, monsoon headwinds are easing, bringing an end to the on/off food price shocks in recent months. So while the market dipped slightly last month on the Reserve Bank of India's (India's central bank or 'RBI') precautionary tightening (albeit via liquidity conditions vs more rate hikes) at last month's policy meeting , recent developments signal that policy easing remains well on track next year, presenting a big tailwind for equity valuations.

Ahead of a state/general election catalyst in the coming months, investors looking for an actively managed option will find a lot to like in the high-quality abrdn-managed India Fund ( IFN ) portfolio. The fund boasts a competitive expense ratio (by actively managed standards) and a track record of outperformance vs. its benchmark. And more recently, the manager has also shown a willingness to enact positive governance changes, particularly on its distribution (cash and shares), to close its historical net asset value ('NAV') discount. While IFN is now priced slightly above NAV (vs. a low-single-digit discount when I last covered the fund), its commitment to a 10% rolling distribution yield and track record of outperformance should keep the fund around NAV parity going forward.

Fund Overview – Competitive Fee Structure Intact; Notable Stock Selection Differences

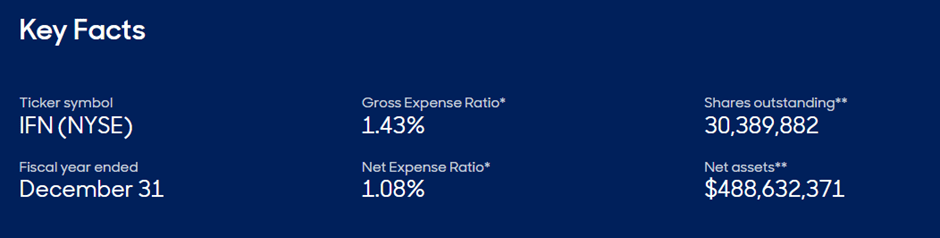

The actively managed abrdn India Fund seeks to outperform the MSCI India Index, a basket of large-cap Indian stocks, on an absolute return basis using a bottom-up stock selection approach. The closed-end fund has seen its net assets grow to $489m, in line with increasingly bullish investor sentiment on the Indian growth story. The higher asset base has shaved two basis points off the ~1.1% net expense ratio (1.4% gross), though fees remain in line with its closest US-listed comparable, Morgan Stanley's India Investment Fund ( IIF ). Even relative to comparable Indian passive funds like the iShares MSCI India ETF ( INDA ), which charges ~0.6%, the IFN fee structure is competitive.

{kind=link}

abrdn

On the other hand, the fund's active share of ~55 means it isn't far off being a 'closet indexer.' In line with this view, IFN shares a similar allocation to Financials (27.8%) with its benchmark. Outside of Financials, though, the fund has opted for overweights on Consumer Staples (11.3%) and Industrials (9.2%), while MSCI India emphasizes Information Technology and Consumer Discretionary more heavily.

IFN's single-stock exposure also shares some similarities to its benchmark but also a fair bit of differences. The largest single-stock exposure remains India's two leading banks, ICICI Bank ( IBN ) at 8.3% and HDFC Bank ( HDB ) at 7.8%. The fund notably excludes Reliance Industries, MSCI India's largest allocation, in favor of IT services leader Infosys ( INFY ), consumer goods leader Hindustan Unilever, and Bharti Airtel. The top ten holdings account for a reduced 51.2% of the overall portfolio, with a slightly increased 2.2% cash allocation.

{kind=link}

abrdn

Fund Performance – Relative Outperformance Continues; Positive Distribution Policy Changes

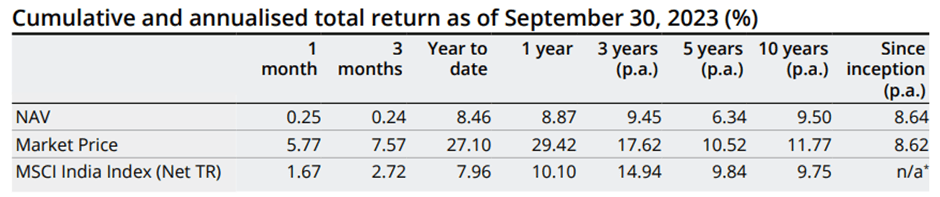

As of Q3 2023 (latest published factsheet here ), IFN has risen by +27.1% in market price terms, far outperforming its benchmark (+8.0%) and NAV return (+8.5%) due to its dissipating NAV discount. The YTD outperformance has further lifted the fund's longer-term track record as well – in market price terms, the fund has compounded at +11.8% over the last decade vs. the MSCI India Index at +9.8%. Also worth noting is that since its inception in 1994, the fund has now delivered an impressive +8.6% annualized return in NAV and market price terms, far outperforming the rest of emerging Asia.

{kind=link}

abrdn

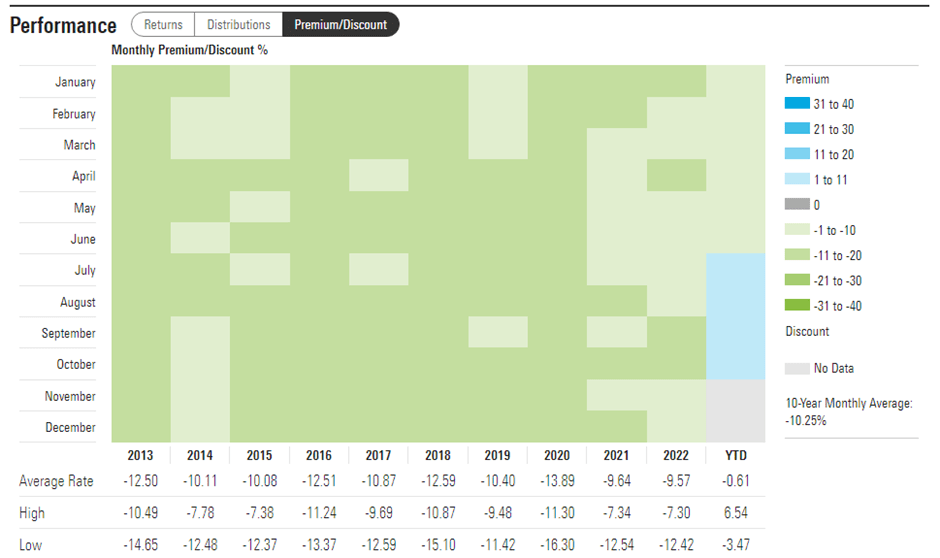

In addition to its stock selection, the manager deserves a lot of credit for its recently altered managed distribution policy - a clear driver of this year's best-in-class returns. To recap, the Board first set a 10% rolling distribution rate (including income and capital gains) in Q1 before following up with a stock distribution policy (via newly issued shares) in Q3. In tandem, the fund's historical NAV discount (~9.6% on average through 2022) has reverted to a low-single-digit premium presently. While IFN's holdings don't offer much in the way of dividends, the fund likely won't run out of capital gains or share issuance opportunities anytime soon, so the current ~10% total distribution seems sustainable. Given the volatility of the market price-NAV delta, though, investors would do well to be opportunistic about their entry points.

{kind=link}

Morningstar

Decelerating Inflation Pressure Supports the Case for Monetary Easing

Inflation has been a key issue for India's monetary policy path in recent months, and the RBI's October policy rate decision reflected this. To recap, the central bank decided to quasi-tighten via government bond sales for liquidity management (i.e., open market operations). While the choice of temporary liquidity tightening (over rate hikes) signals this is very much a precautionary measure rather than an altered policy path, the resulting upward pressure on term premia across the Indian rate complex did weigh on equity valuations.

Yet, this week's CPI inflation data, which showed a deceleration to +4.9% YoY (down from +5.0% previously), indicates tightening will likely be a short-lived phenomenon. Even on a sequential basis, the print was only modestly positive - despite supply-driven price spikes for onion and spices. With the underlying weather-driven pressures for overall vegetable prices (e.g., tomatoes, green chili, and cauliflower) reversing, headline CPI appears poised for a near-term downtrend. Similarly, the core inflation gauge (goods and services) also saw broad-based easing, confirming recent RBI data that food price inflation has done little to alter household inflation expectations.

{kind=link}

Bloomberg

While lower inflation bodes well for equity valuations via the rate channel, the more relevant metric for earnings is PMI input prices, which have also been falling in India. Producers can then pass this on via lower output prices without sacrificing profit margins, in turn boosting profitability. Oil (note India is a large importer) is probably the only major risk left here amid geopolitical tensions in the Middle East, though India is now better equipped to withstand external shocks, given the buffer from its improved fundamentals (e.g., narrower current account deficit). Barring demand-side inflation pressures pre-election (e.g., fiscal handouts), India remains on a clear path to monetary easing in early to mid-2024, in my view.

This Actively Managed India Fund Still Offers Lots of Positives

2023 could hardly have gone better for Indian equities. From here, the Indian story faces more positives than negatives, as a close state/general election contest looks poised to unleash more fiscal support than expected. Also helping are easing supply-side headwinds spilling over into lower consumer inflation numbers; alongside a lack of second-round effects from the recent inflation spike, India remains well on track to enter a monetary easing cycle next year. Low-cost ETFs remain my preferred pick (see my most recent coverage of the Franklin FTSE India ETF ( FLIN ) here ), though investors who don't mind paying higher fees for a quality manager and a 10% rolling distribution yield will find plenty to like in IFN.

For further details see:

India Fund: This Actively Managed Fund Still Offers Lots Of Positives