CCI - Inflation Cools As Earnings Heat Up

2023-07-30 09:00:00 ET

Summary

- U.S. equity markets climbed to the highest levels since early 2022 as investors analyzed a frenzied slate of corporate earnings results, economic data, and central bank policy decisions.

- Gaining for a third-straight week, the S&P 500 advanced 1.0% on the week. The Dow Jones Industrial Average snapped its record-tying winning streak at 13-straight trading sessions.

- Pressured by the jump in benchmark interest rates, real estate equities were generally laggards this week despite a very strong slate of earnings results and some notable M&A developments.

- The battered office REIT sector led the gains this week on the heels of a slate of surprisingly strong reports showing that leasing activity and pricing trends do indeed appear to have rebounded in recent months. Technology REITs were also upside standouts this week.

- Residential REITs - along with other more "defensive" property sectors - were under pressure this week despite a solid slate of reports showing buoyant rent growth and receding expense pressures.

Real Estate Weekly Outlook

U.S. equity markets climbed to the highest levels since early 2022 as investors digested a frenzied slate of corporate earnings results, economic data, and central bank policy decisions. As expected, the U.S. Federal Reserve hiked benchmark interest rates to the highest level in 22 years -continuing its most aggressive policy tightening in the central bank's history - but Fed Chair Powell signaled a tack toward a more "data-dependent" policy approach, appearing to acknowledge recent data showing a sharp deceleration in price pressures.

{kind=link}

Hoya Capital

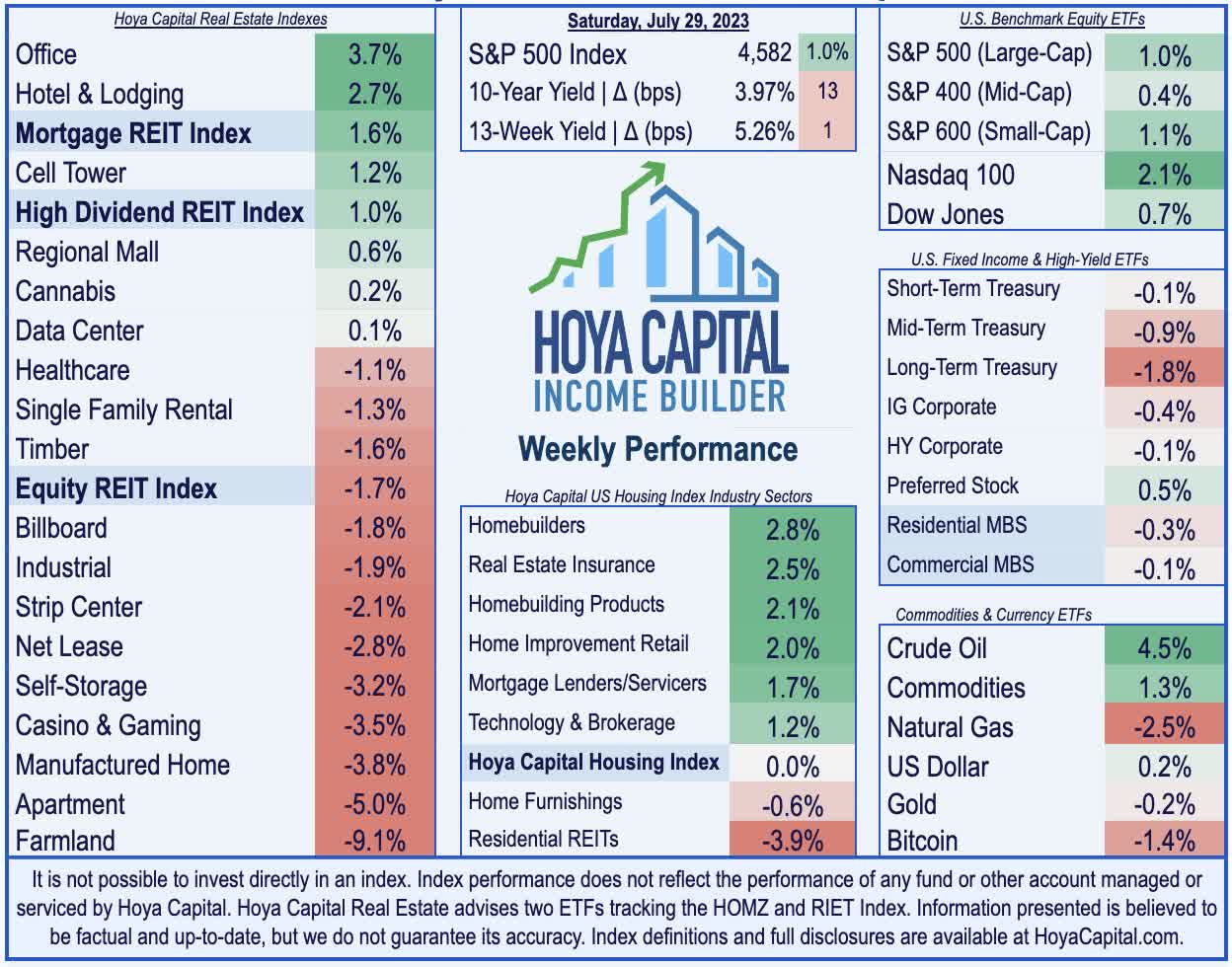

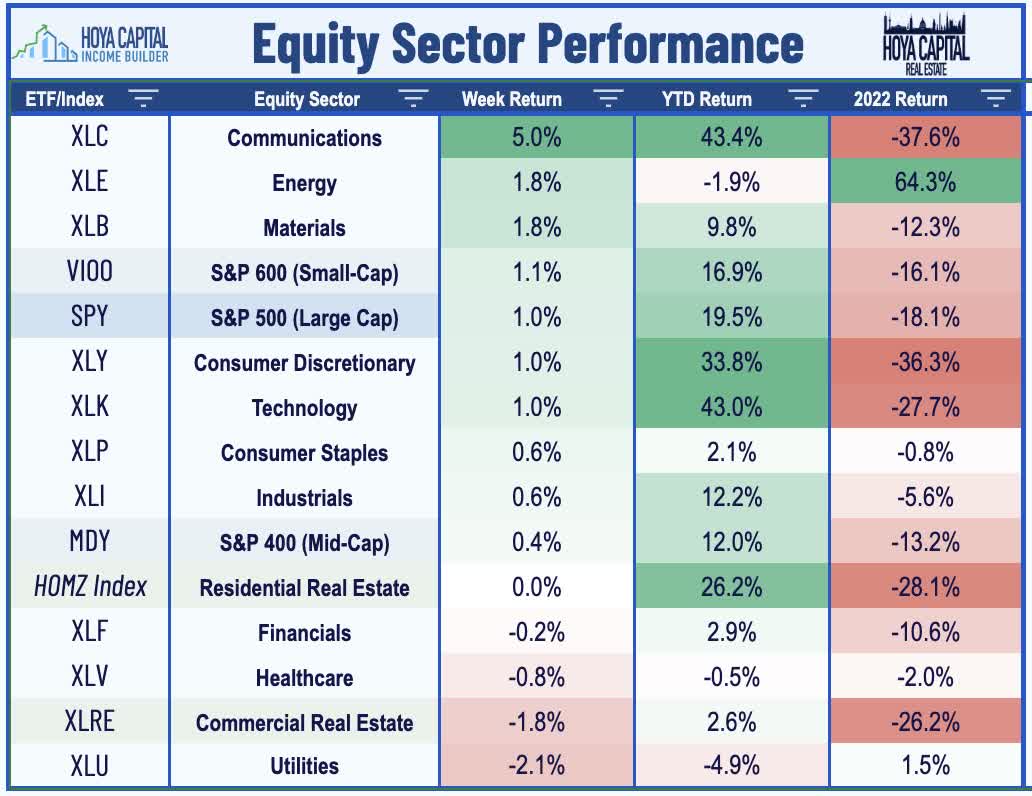

Posting its highest weekly close since January 2022, the S&P 500 advanced 1.0% on the week while the tech-heavy Nasdaq 100 rallied by over 2%. The Dow Jones Industrial Average snapped its record-tying winning streak at 13-straight trading sessions, but still posted gains of nearly 1% on the week. The other major equity benchmarks - the Mid-Cap 400 and Small-Cap 600 posted gains of 0.4% and 1.1%, respectively. Pressured by the jump in benchmark interest rates, real estate equities were laggards this week despite a very strong slate of earnings results and some notable M&A developments. The Equity REIT Index slumped 1.7% on the week, with 6-of-18 property sectors in positive territory, but the Mortgage REIT Index gained 1.6%. Homebuilders resumed their impressive rebound on very strong results from a half-dozen builders alongside housing market data showing an upward inflection in home values resulting from historically low housing inventory levels.

{kind=link}

Hoya Capital

Benchmark bond yields initially trended lower after the Federal Reserve's policy decision, but subsequent tightening actions from the ECB and Bank of Japan and relatively strong GDP data on Thursday sent the 10-Year Treasury Yield sharply higher, before retreating back below the 4%-level on Friday following the cooler-than-expected PCE inflation report. The policy-sensitive 2-Year Yield was little changed, however, closing the week at 4.88%. Potentially throwing a wrench into the improving inflation outlook, Crude Oil extended its rebound to nearly 20% over the past six weeks after hitting two-year lows in June, as OPEC production cuts and relatively resilient demand in the U.S. and Europe have offset headwinds from weak economic activity in China. Energy ( XLE ) stocks were among the top performers this week, as were Communications ( XLC ) stocks on the heels of strong results this week from chip-maker Intel ( INTC ) and from Meta Platforms ( META ).

{kind=link}

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

Hoya Capital

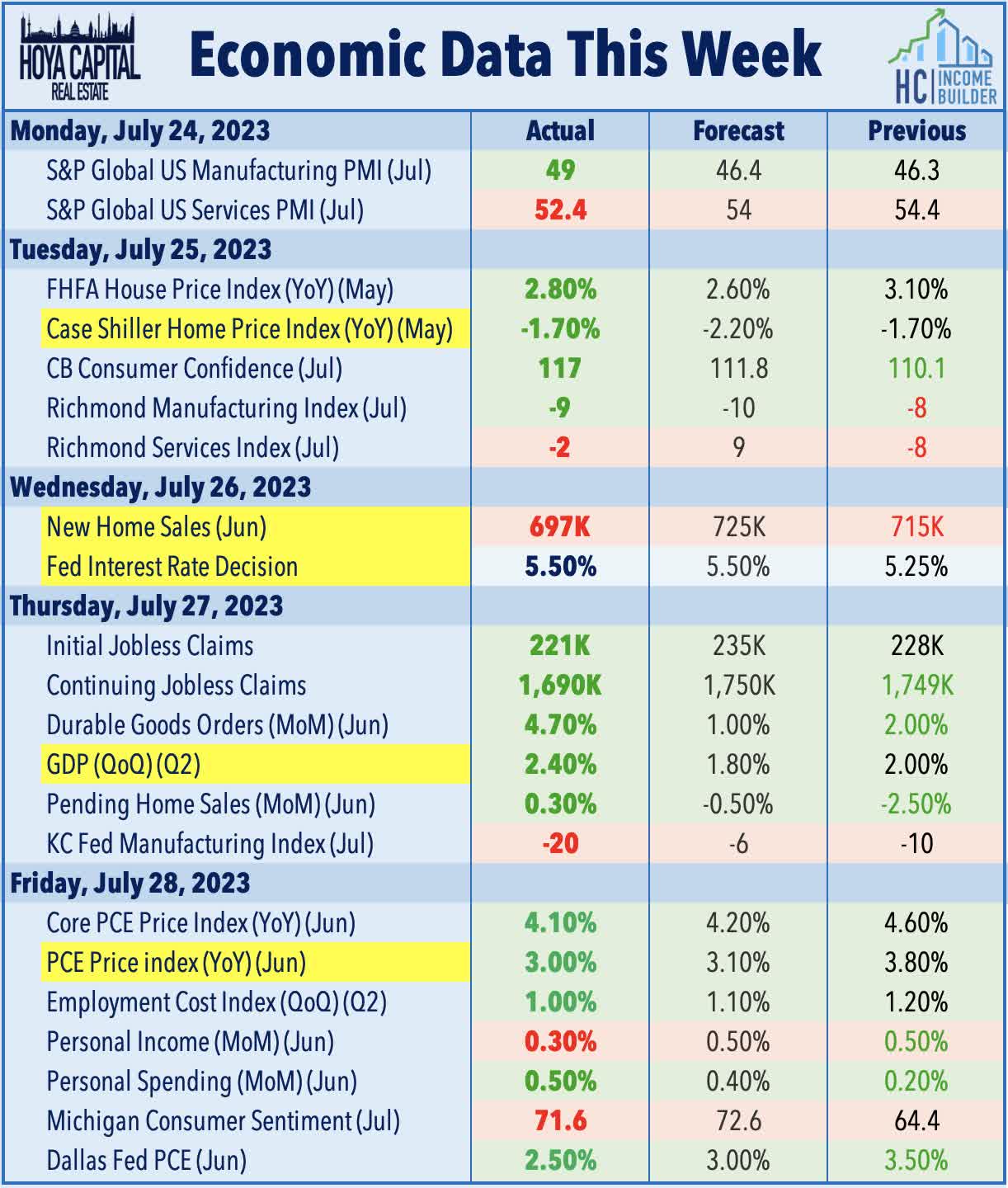

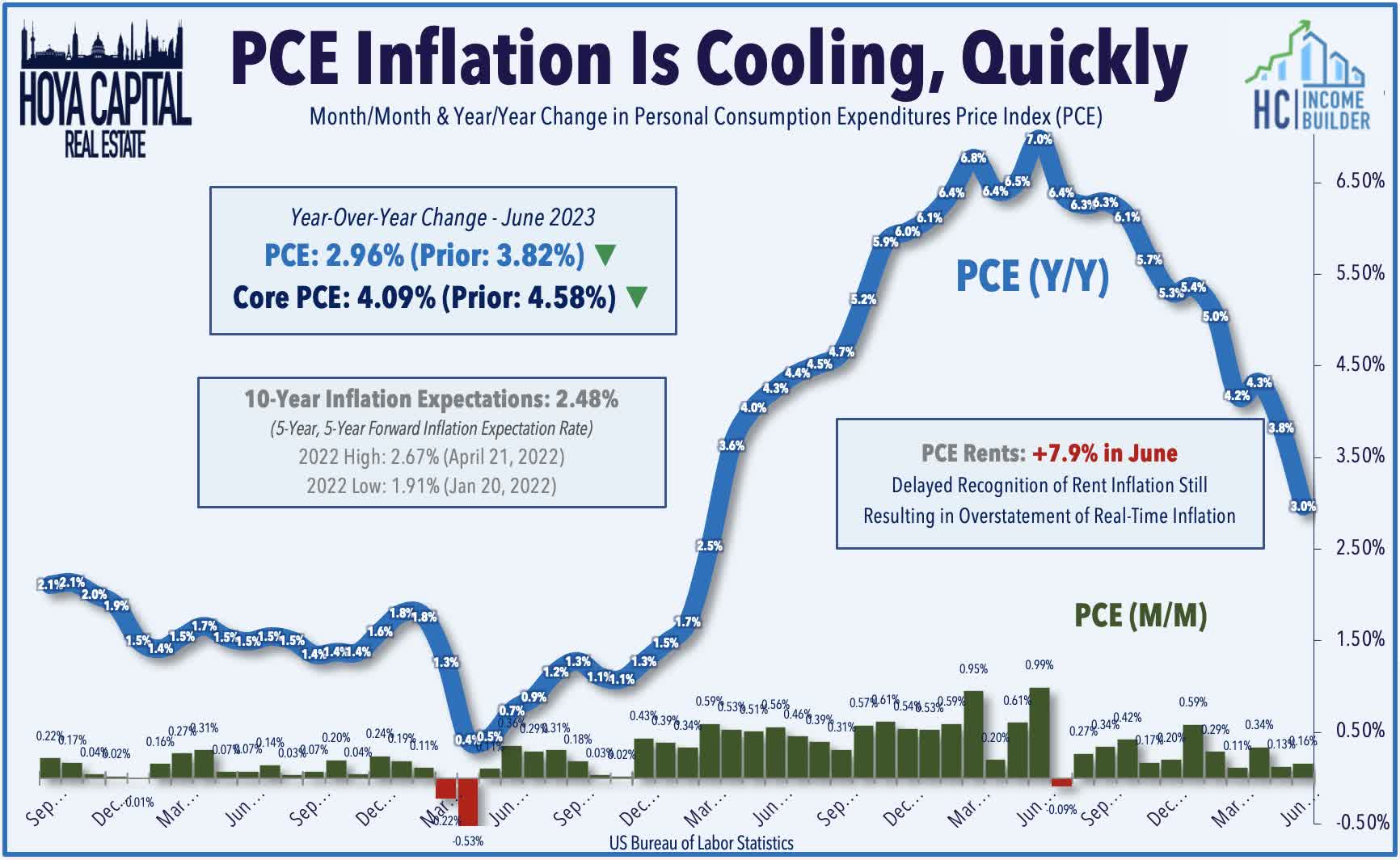

Continuing the stretch of "good news" on the inflation front seen over the past several months, the closely-watched PCE Index provided further evidence that price pressures have cooled rather significantly in recent months. The Personal Consumption Expenditures (PCE) Price Index rose just 0.16% in June - below the 0.3% consensus expectation - which dragged the year-over-year increase to below 3% for the first time in over two years. The delayed recognition of shelter inflation continues to heavily distort the headline and core metrics, however, resulting in a significant understatement of inflation from mid-2021-2022 and an overstatement of inflation since mid-2022. Consistent with the trends observed in the Consumer Price Index, the PCE Index has averaged less than 1% since last July when excluding the shelter component. The other major inflation data point this week - the Employment Cost Index - was also cooler-than-expected, rising just 1.0% in Q2 - the lowest in two years and below Street estimates of 1.1%.

{kind=link}

Hoya Capital

Equity REIT Week In Review

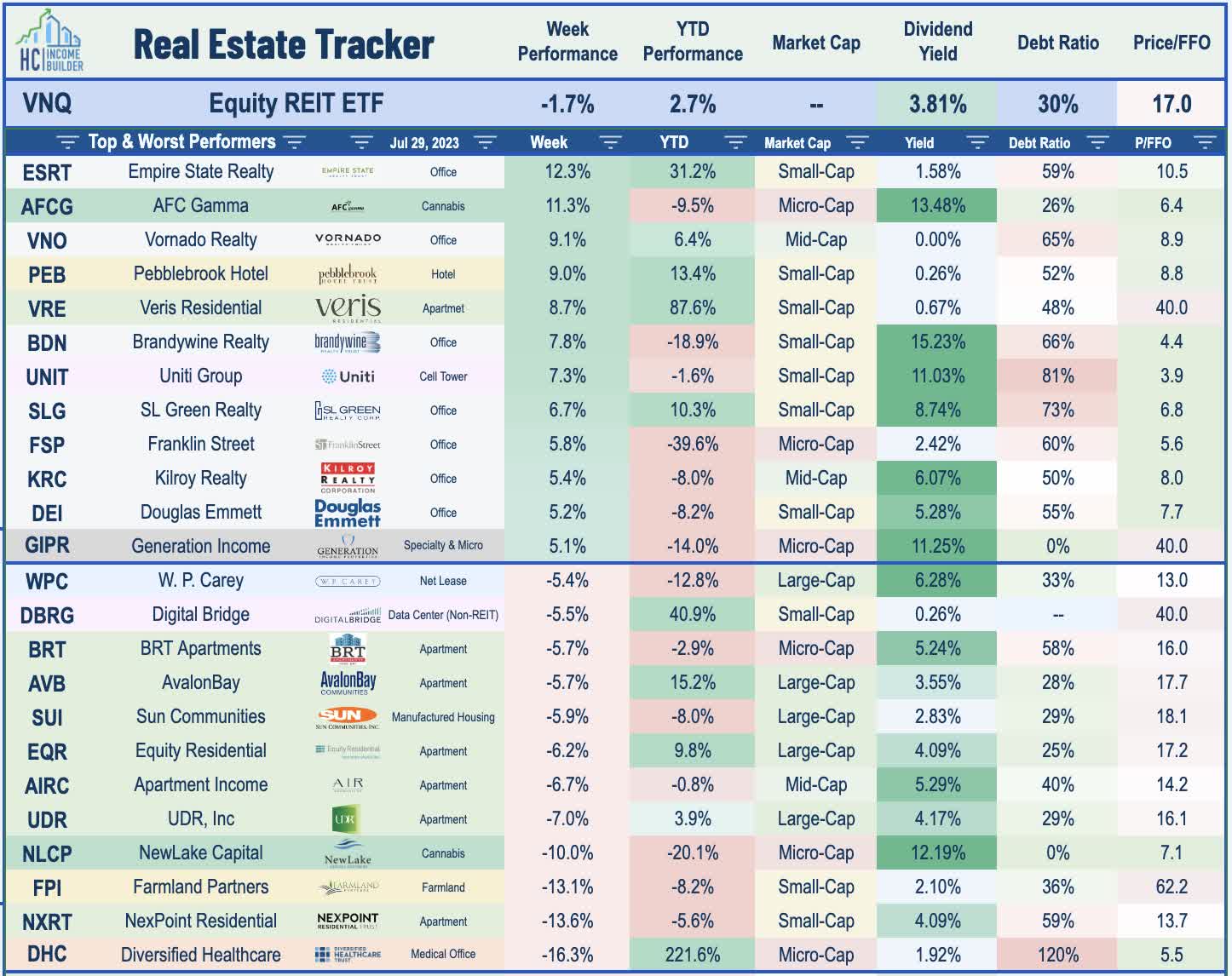

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Hoya Capital

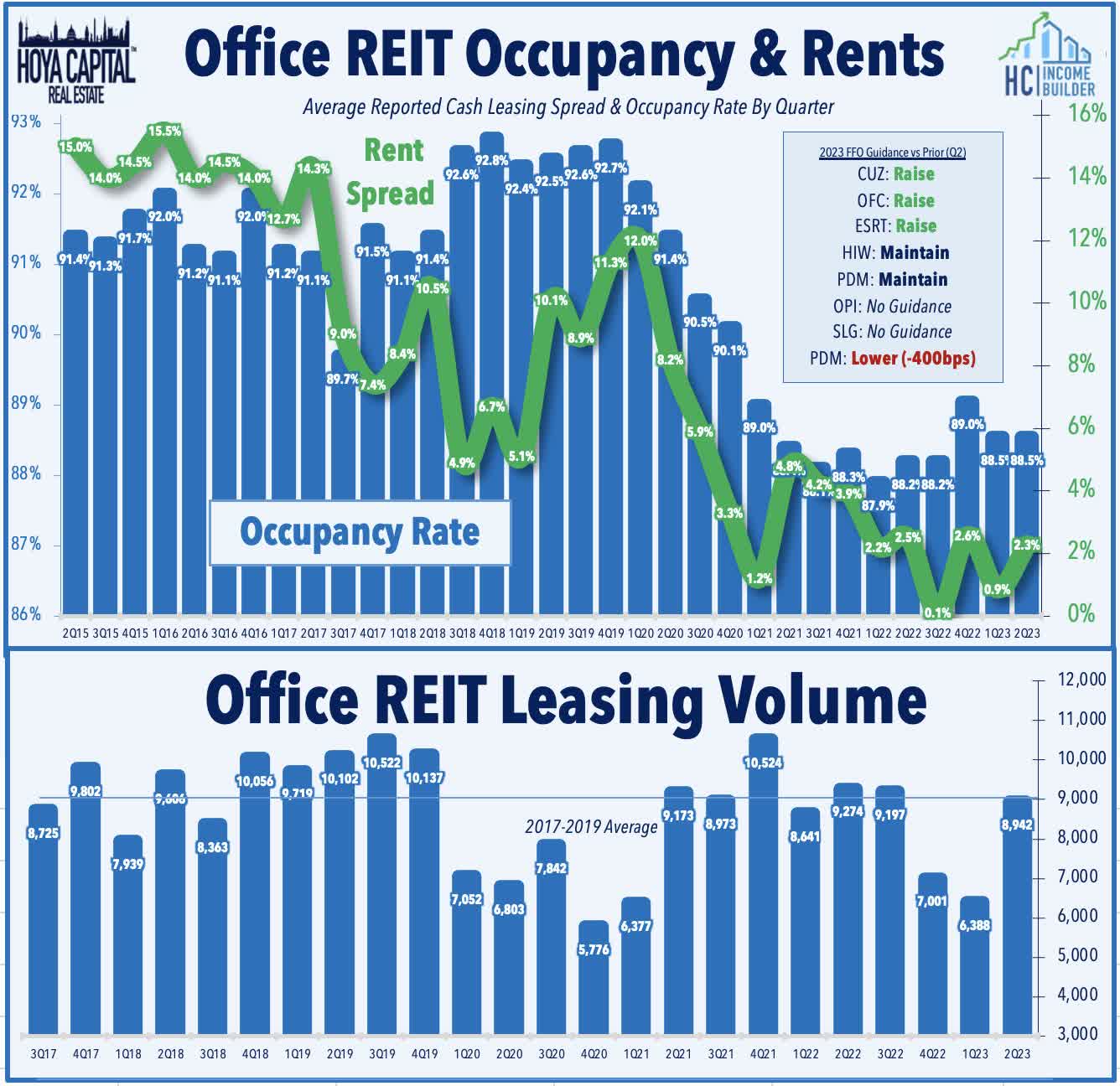

The battered office REIT sector led the gains this week on the heels of a slate of surprisingly strong reports showing that leasing activity and pricing trends do indeed appear to have rebounded in recent months, with total volume trending towards levels that are only slightly below the pre-pandemic averages after two historically weak quarters. NYC-focused Empire State Realty ( ESRT ) rallied 12% after raising its full-year FFO outlook and reporting leasing volume of 336k square feet - above its pre-pandemic average from 2017-2019 - and achieved effective rent increases of 10.1% on these leases. Brandywine (BDN) gained 8% after reporting leasing activity of 568k square feet - 40% higher than its four-quarter average and above its pre-pandemic average as well - and achieved renewal spreads of 5.8% on these leases. Cousins ( CUZ ) gained 3% after it also raised its full-year FFO growth outlook and recorded rent growth of 7.9% on leasing volume of 435k square feet - each an acceleration from last quarter. Corporate Office ( OFC ) gained 1% after it also boosted its full-year FFO growth outlook and recorded its strongest quarter of leasing activity and occupancy since 2021. Highwoods ( HIW ) reported leasing activity of 918k square feet - 16% above its four-quarter average - and achieved cash rent growth of 0.5% on these leases. Piedmont ( PDM ) finished flat, however, after it became the 23rd REIT this year to reduce its dividend, trimming its quarterly payout by about 40%.

{kind=link}

Hoya Capital

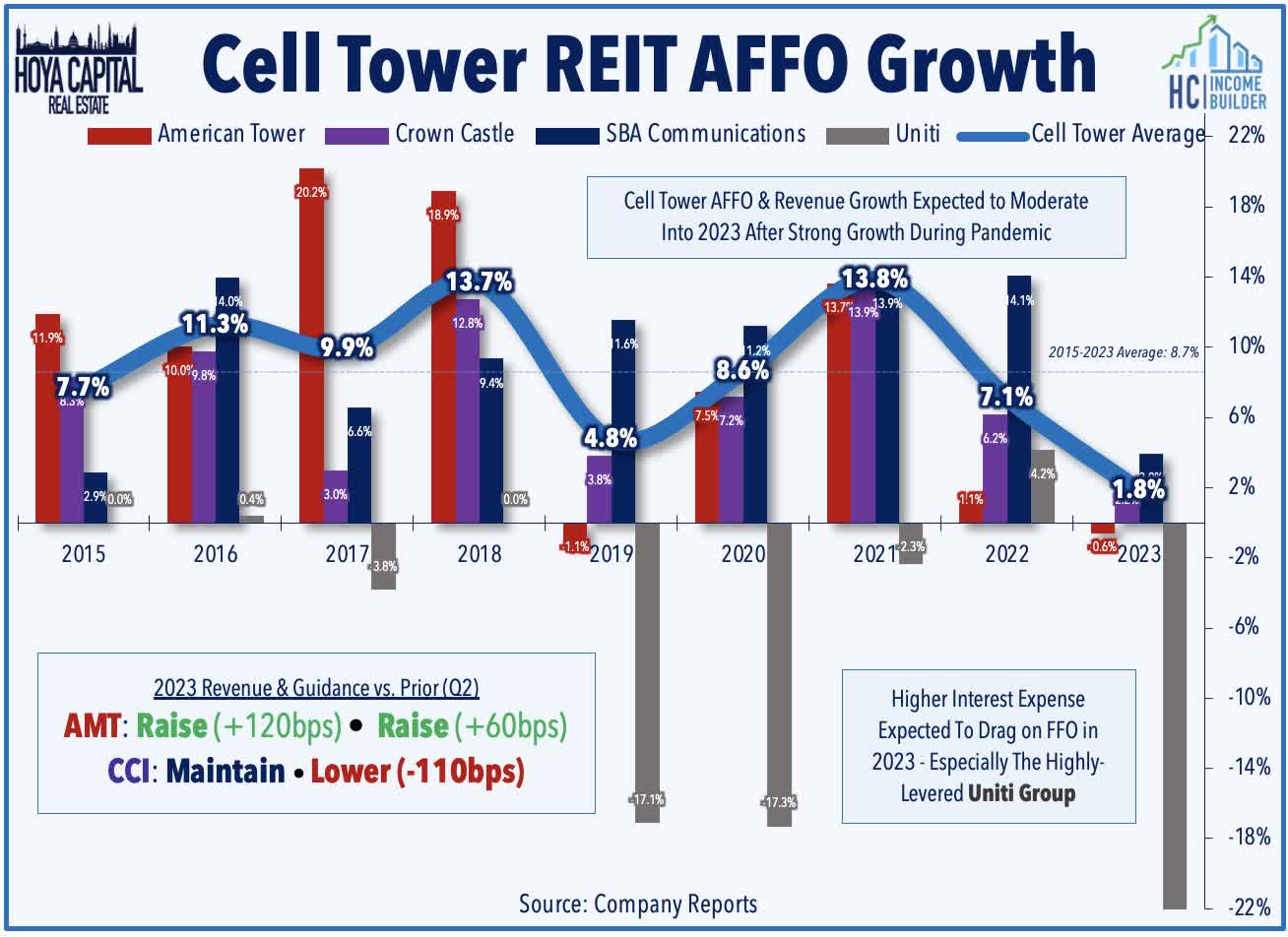

Cell Tower : American Tower ( AMT ) gained 2% after reporting strong results and raising its full-year outlook driven by strong demand in its international and data center segments. AMT now expects full-year revenue growth of 3.9% - up 120 basis points from last quarter - and expects FFO growth of -0.6% - a 60 basis point improvement from the prior outlook. Crown Castle ( CCI ) also gained about 2% this week after it disclosed that it has initiated a restructuring plan to reduce costs, which includes a reduction in employee headcount by about 15%. This week, we published Cell Tower REITs: Toxic Telecom, which discussed recent trends and our updated outlook on the sector, which has been the weakest-performing property sector since the start of 2022 amid a telecommunications industry-wide slump inflamed by tight monetary conditions. We noted that industry headwinds are rooted primarily in the ongoing disintermediation of legacy wireline business segments towards fully wireless deployments and the mounting competition on the two industry juggernauts from within the wireless industry itself via T-Mobile, Amazon, and Dish. This disintermediation has trended on a path from wired to wireless infrastructure, disruptions which actually serve to further solidify the longer-term favorable competitive positioning of cell tower REITs.

{kind=link}

Hoya Capital

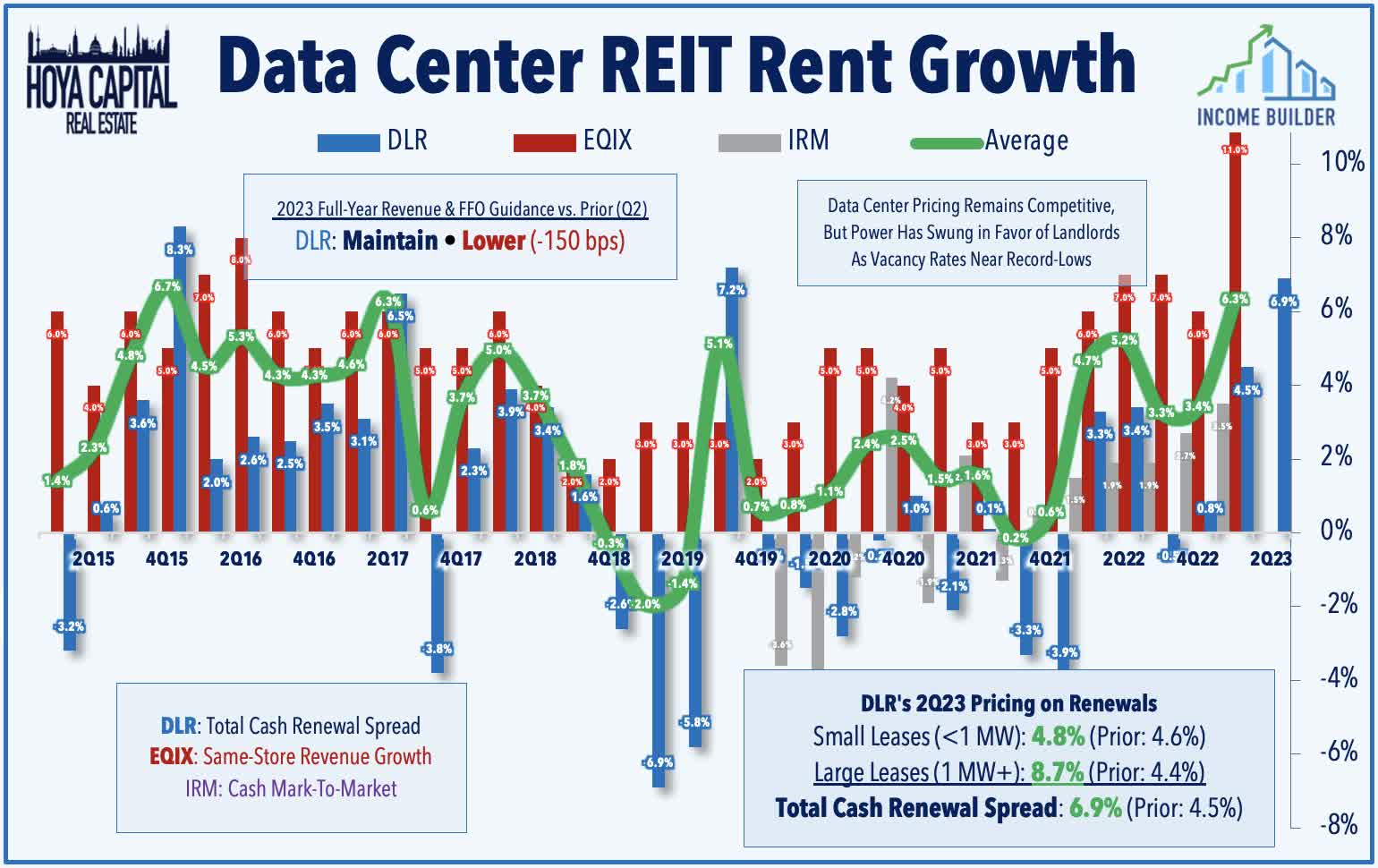

Data Center : Digital Realty ( DLR ) - which we own in the Dividend Growth Portfolio - rallied 2% this week after reporting strong second-quarter results highlighted by impressive pricing trends and the successful $1.3B capital raise through a majority sale of a portfolio in Northern Virginia to TPG Real Estate at a 6.0% cap rate. While DLR trimmed the midpoint of its full-year FFO outlook due to unpaid rent from Cyxtera - which declared bankruptcy earlier this year - it raised its outlook for cash re-leasing spread and same-store NOI growth by 100 basis points each. Rent growth trends continued on an upward trajectory in Q2 with cash re-leasing spreads of 6.9% - the highest in three years - with notable strength from larger leases which posted rent spreads of nearly 9%, which had been an area of weakness in recent years.

{kind=link}

Hoya Capital

Healthcare : Lab space operator Alexandria Real Estate ( ARE ) - another REIT that came into the cross-hairs of short-sellers in recent months - gained about 3% this week after it released second-quarter results, confirming its preliminary metrics released earlier this month in which it updated full-year guidance in a 10-K filing. ARE recorded total leasing volume of 1.3M square feet in Q2 - up slightly from the 1.2M SF signed in Q1 - and on these leases, it achieved cash rent increases of 8.3%, a rate of increase that was down from its record-high spreads in Q1 of 24.2%. ARE maintained the midpoint of its outlook for full-year adjusted FFO at $8.96 - representing a 6.5% increase from 2022 - and maintained the midpoint of its outlook for full-year average occupancy at 95.1% and for cash rental rate spreads at 14.5%. However, ARE downwardly revised its full-year unadjusted FFO guidance to reflect several recent asset sales and the previously-announced impairment related to a Boston property - 275 Grove Street - where it dropped plans to convert the office space into lab space.

{kind=link}

Hoya Capital

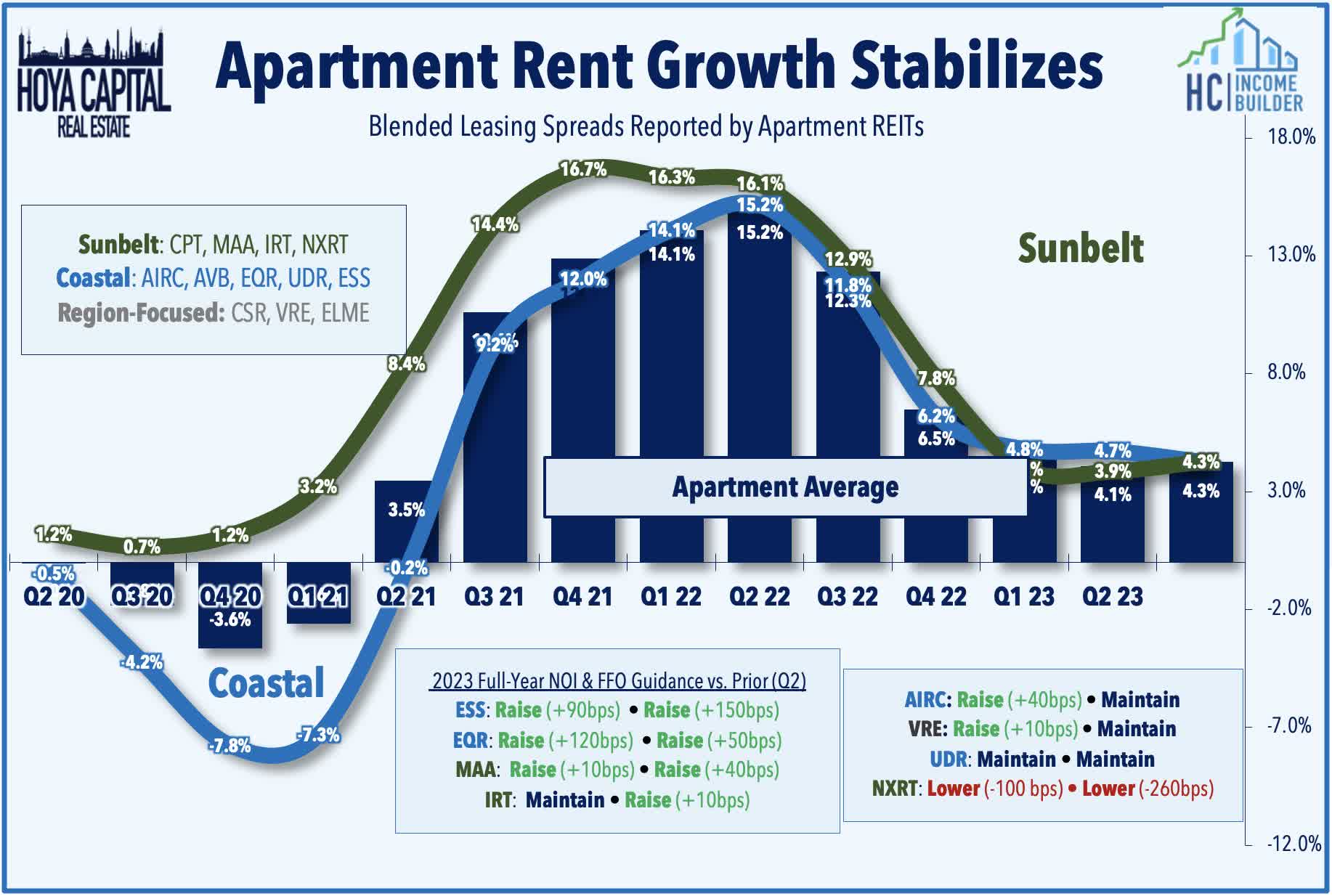

Apartment : Multifamily REITs were under pressure this week despite reporting relatively impressive results, with five of the eight REITs raising their full-year FFO guidance and recording a modest reacceleration in rent growth in recent months. Veris Residential ( VRE ) was the upside standout, surging 9% after raising its full-year outlook and announcing that it completed a $520M buyout from its joint-venture partner Rockpoint - a major step towards simplifying its business structure as a pure-play multifamily REIT. West Coast-focused Essex ( ESS ) slipped 3% despite reporting surprisingly solid results and significantly raising its full-year FFO and NOI growth outlook, citing strength in Southern California markets, which offset relative weakness in Northern California and Seattle. Sunbelt-focused Mid-America ( MAA ) declined 4% despite raising its full-year FFO outlook by 40 basis points to a sector-leading 7.2%. Independence Realty ( IRT ) also dipped 5% despite raising its full-year FFO outlook by 100 basis points to 7.0%. Equity Residential ( EQR ) declined 6% despite raising its full-year FFO and NOI growth outlook while UDR Inc. ( UDR ) and Apartment Income ( AIRC ) each dipped about 7% after maintaining their full-year outlook. Lagging this week, small-cap NexPoint Residential ( NXRT ) dipped more than 10% after lowering its outlook as it works through disruptions in asset sale plans and recording an uptick in missed rents in several markets, including Atlanta and Las Vegas.

{kind=link}

Hoya Capital

Manufactured Housing : Sun Communities ( SUI ) dipped 6% after lowering its full-year FFO outlook as outperformance in its core manufactured housing and marina divisions were more-than-offset by continued struggles in its UK portfolio, which it acquired in 2022. For a second-straight quarter, SUI posted a significant downward revision to its UK Home Sales NOI forecast, resulting in a downward revision to its full-year FFO outlook to -2.6%, down from its prior outlook of -0.4%. Domestically, SUI's business continues to post solid results, driving upward guidance boosts to its same-store NOI outlook for manufactured housing (+30 basis points to 5.5%) and to its marina segment (+110 basis points to 8.5%). Echoing results last week from Equity LifeStyle ( ELS ), however, the transient RV segment remains an area of relative weakness amid a broader post-COVID normalization in RV utilization.

{kind=link}

Hoya Capital

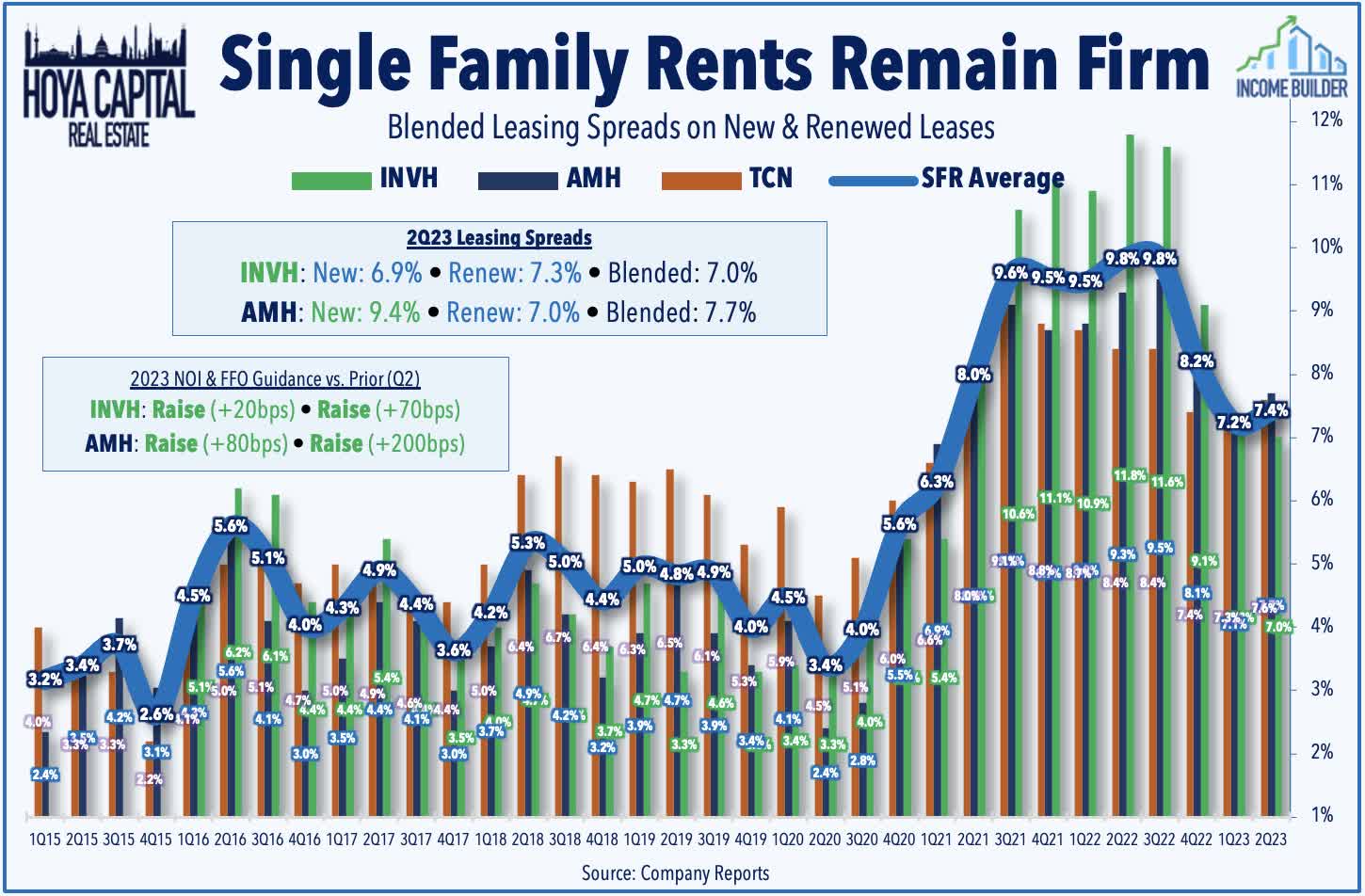

Single-Family Rental : SFR REITs were able to defy the downward pressure on residential REITs this week after reporting impressive "beat and raise" results this week fueled by buoyant rent growth across the SFR sector, which is not facing the same supply headwinds as the multifamily side. American Homes recorded blended leasing spreads of 7.7% in Q2 - which was actually an acceleration from the 7.1% rate in Q1 - which drove a boost to its full-year earnings outlook. AMH now expects full-year FFO growth of 6.5% - up 200 basis points from last quarter and sees NOI growth of 4.8% at the midpoint - up 80 basis points from last quarter. AMH also noted that it entered into a $625M second strategic joint venture with J.P. Morgan Asset Management to construct "built to rent" homes. Invitation Homes recorded blended leasing spreads of 7.0% in Q2 - which was down only slightly from the 7.3% blended increase in Q1 - and drove a boost to its full-year earnings outlook. INVH now expects full-year FFO growth of 5.0% - up 70 basis points from last quarter. INVH also reported that it acquired 1,900 homes for $650 million from Starwood Capital's non-traded REIT platform dubbed "SREIT" which has faced similar redemption requests as Blackstone's BREIT.

{kind=link}

Hoya Capital

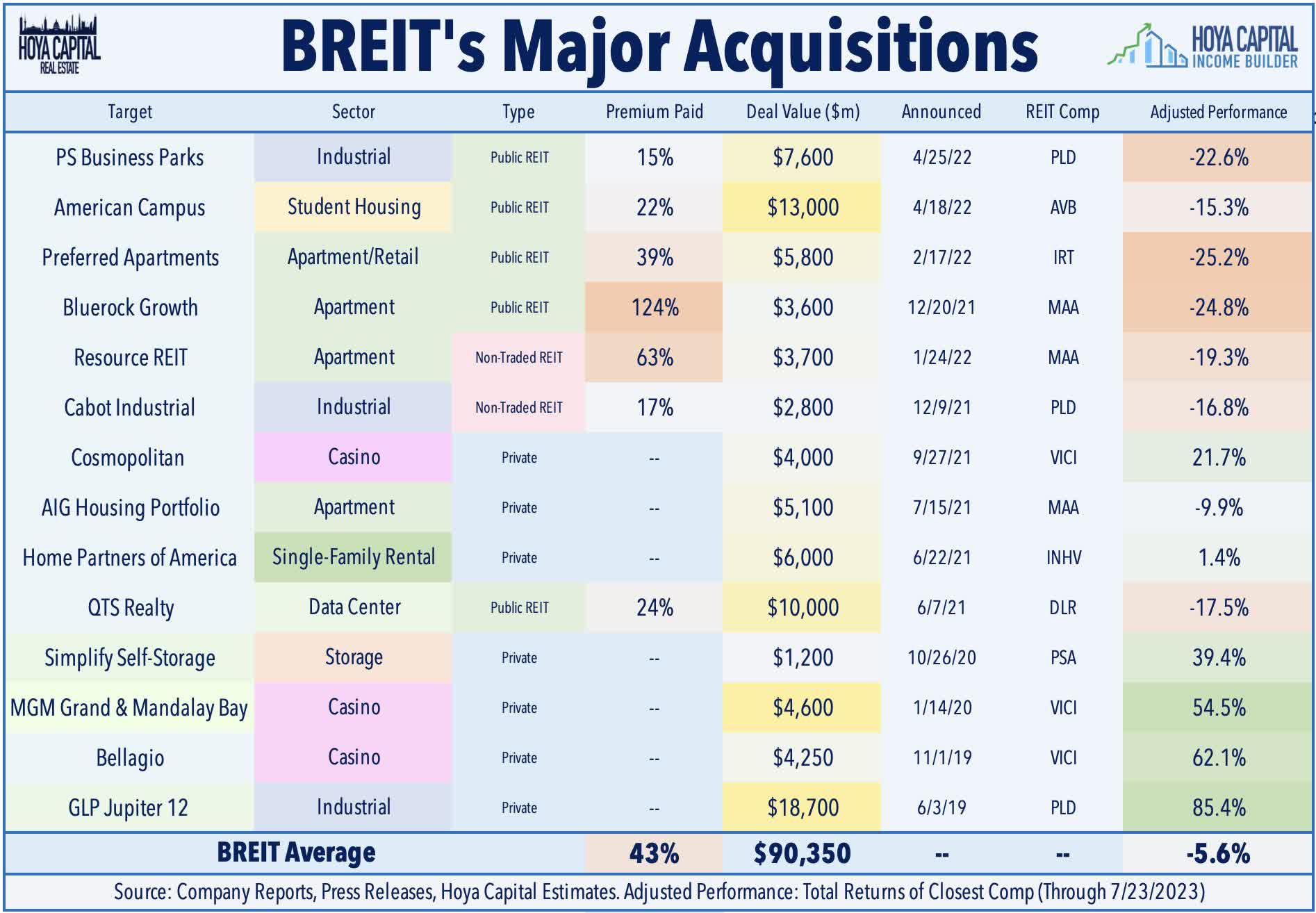

Storage : On that note, Public Storage ( PSA ) announced a $2.2B deal to acquire Simply Self Storage from Blackstone's ( BX ) Real Estate Income Trust ("BREIT") for $2.2B - one of a half-dozen portfolio sales by BREIT since late 2022 as it struggles to meet withdrawal requests from investors. The portfolio consists of 127 wholly owned properties and 9M net rentable square feet located across 18 states and in markets, about 65% of which are in Sunbelt markets. We predicted earlier this year that the Simply Storage portfolio - which BREIT acquired in late 2020 - was among the most likely assets that BREIT would sell given its preference to avoid a mark-to-market event by "selling its winners and holding its losers." Four of the six "winners" in BREIT's portfolio are its casino holdings, two of which it has already sold (MGM Grand and Mandalay) and one of which (Bellagio) it is reportedly marketing for sale. The other two "winners" are the Simply Self-Storage portfolio and the GLP Jupier 12 industrial portfolio, which BREIT acquired in 2019. Elsewhere in the storage space, S&P raised the credit ratings on Extra Space ( EXR ) to “BBB+” from “BBB” following its merger with Life Storage .

{kind=link}

Hoya Capital

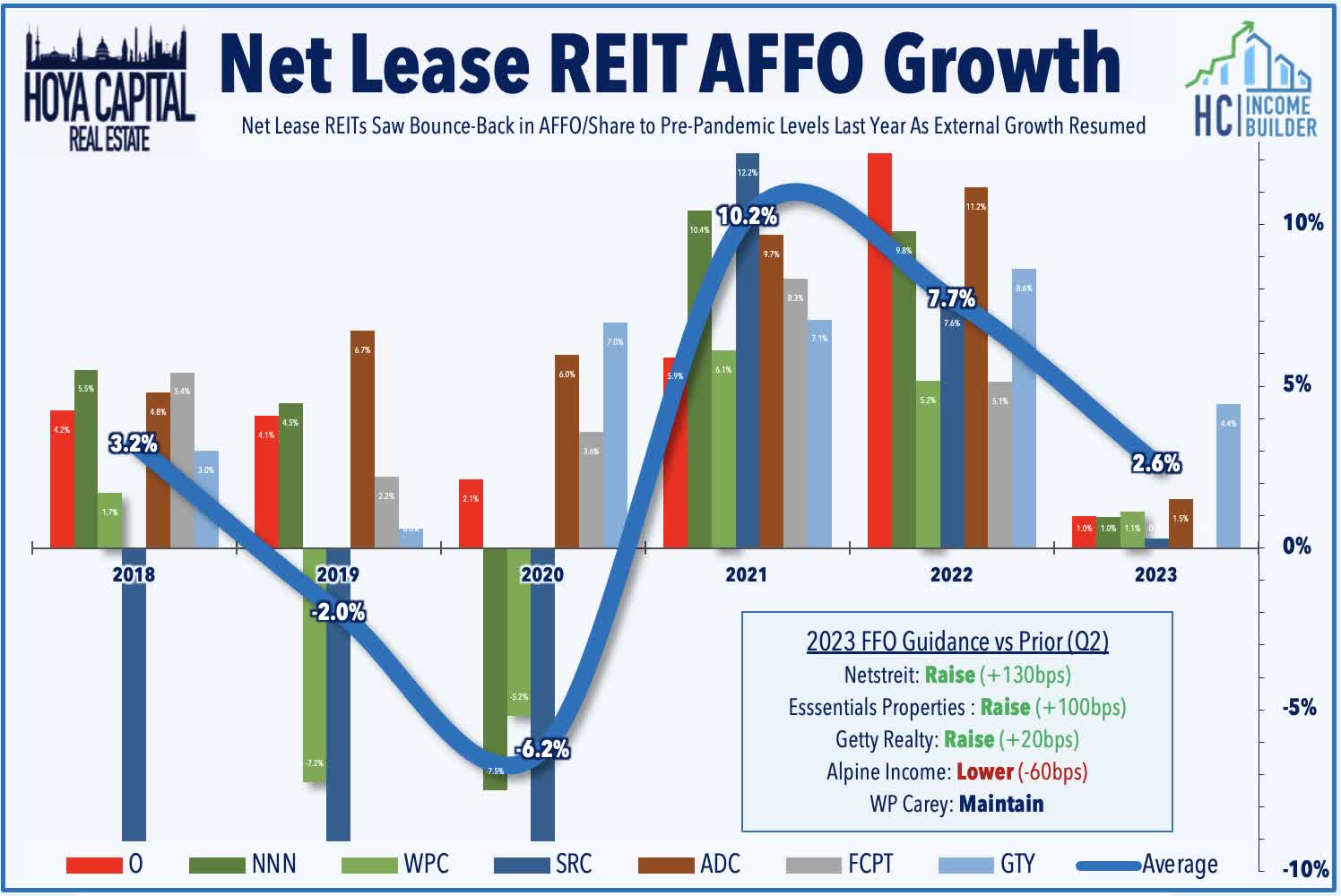

Net Lease : Pressure from higher interest rates this week overshadowed a relatively strong start to earnings season for net lease REITs. Netstreit ( NTST ) raised its full-year FFO outlook to 4.7% (up 130 basis points from last quarter), Essential Properties ( EPRT ) raised its full-year FFO growth outlook by 100 basis points to 6.9%, and Getty Realty ( GTY ) increased its FFO growth outlook by 20 basis points to 4.4%. On the downside this week, W. P. Carey ( WPC ) dipped 5% this week after reporting decent results but maintaining its full-year outlook, a bit of a disappointment after a trio of its net lease peers raised their outlook earlier this week. WPC continues to expect FFO growth of roughly 3% this year, while it also maintained its full-year acquisitions guidance which calls for investment volume between $1.75 billion and $2.25 billion. Notably, WPC sees its rent growth "peaking" this year at around 4% this year as the tailwinds from the CPI linkage may potentially become modest headwinds into 2024 given the recent inflation trends.

{kind=link}

Hoya Capital

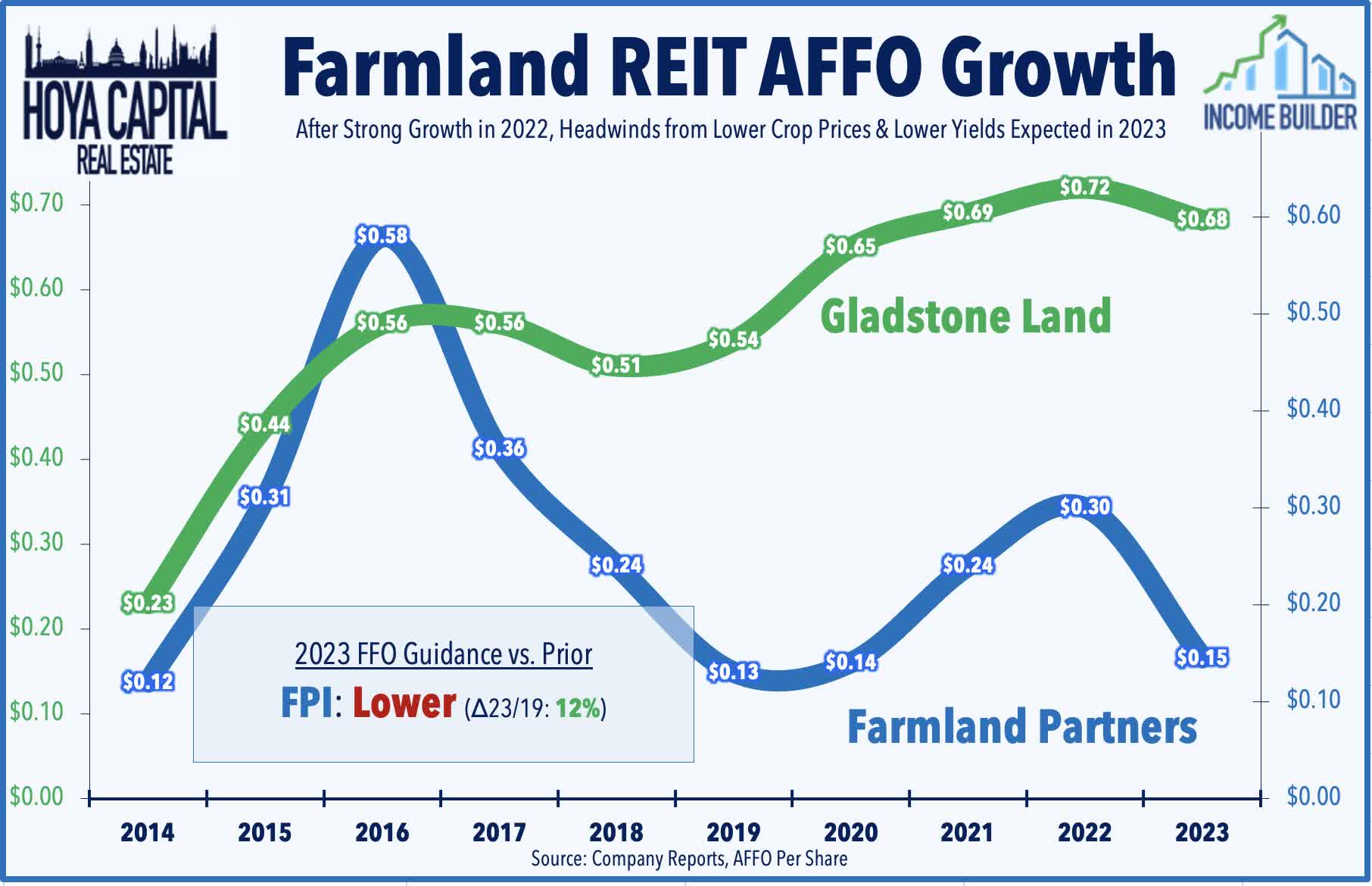

Farmland : On the downside this week, small-cap farmland REIT Farmland Partners ( FPI ) plunged more than 13% after it significantly lowered its full-year FFO outlook prompted by rising interest expense. FPI now expects its full-year FFO to dip over 50% this year compared to 2022, but to levels that are still about 12% above its full-year 2019 FFO before the pandemic. As discussed in our recent Land REIT report , farmland REITs have been pressured by a "triple whammy" of headwinds - lower crop yield due to extreme weather, lower crop prices, and significantly higher interest rate expense. One of the hottest "inflation hedges" during the pandemic, land REITs have fallen out-of-favor as rising rates and normalizing supply chains have created disinflationary - and even deflationary - headwinds for commodities. Grains prices have declined 25% from their 2022 peak despite the ongoing Russia/Ukraine War, but remain 50% above 2019-levels.

{kind=link}

Hoya Capital

Mortgage REIT Week In Review

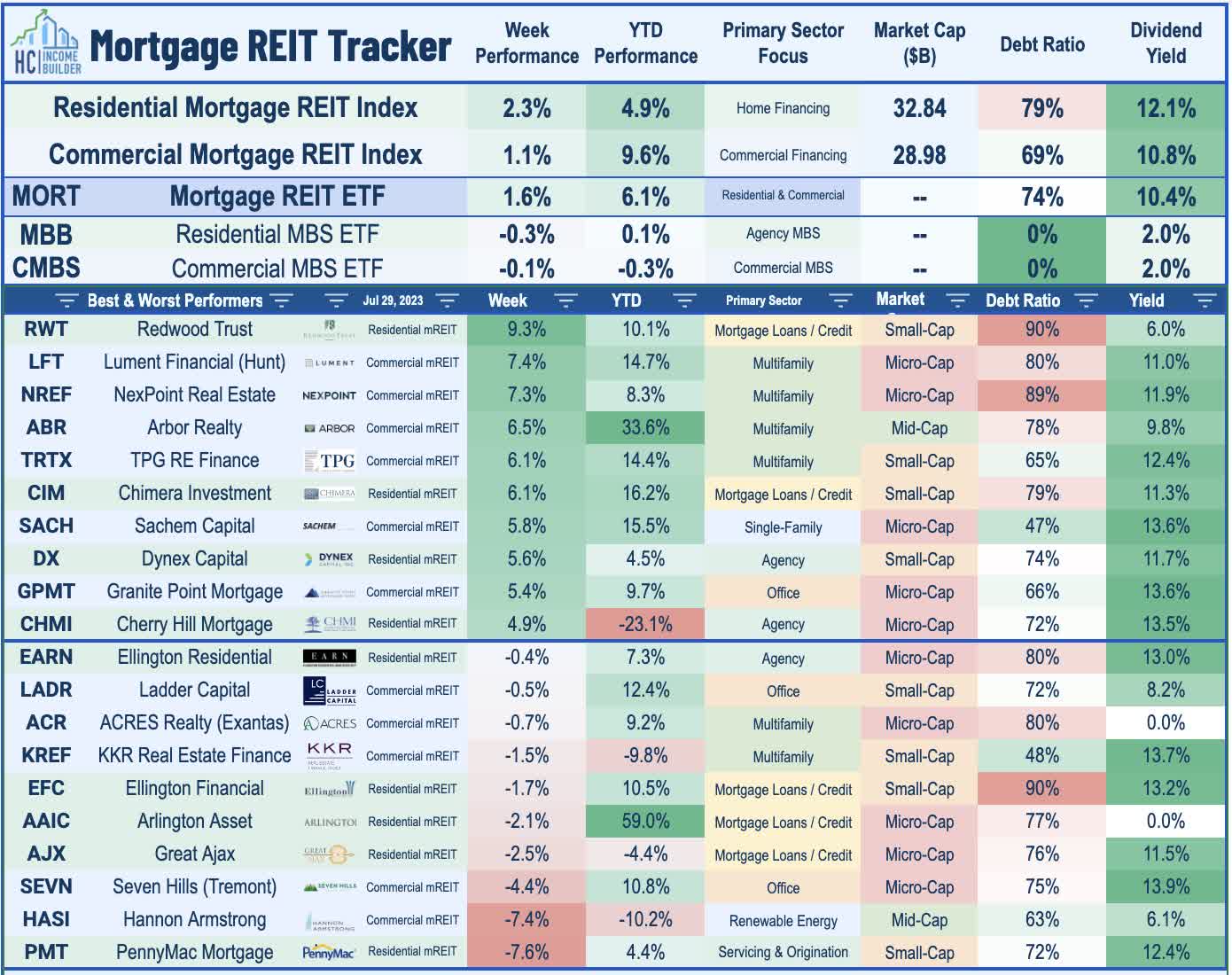

Mortgage REITs continued their strong performance this week amid a solid start to earnings season highlighted by a pair of dividend hikes, with the iShares Mortgage REIT ETF ( REM ) advancing another 1.6% to extend its rally since early May to nearly 25%. On the upside, multifamily-focused lender Arbor Realty ( ABR ) - which had come into the cross-hairs of short-sellers earlier this year - rallied 6% after reporting stronger-than-expected results and raising its dividend to $0.43. NexPoint Real Estate ( NREF ) rallied 7% after reporting solid results and declaring a special dividend of $0.185/share in addition to maintaining its regular quarterly dividend. Credit-focused residential mREIT Redwood Trust ( RWT ) also rallied more than 9% after reporting EPS of $0.14 - up from $0.11 last quarter and beating Street estimates - while its Book Value Per Share ("BVPS") was roughly flat. Dynex Capital ( DX ) rallied over 5% after reporting that its BVPS increased by 2.9% in Q2 while its comprehensive net income improved to $0.79/share - up from a negative number last quarter and now covering its $0.39/share dividend.

{kind=link}

Hoya Capital

Commercial lender Blackstone Mortgage ( BXMT ) - which we own in the Focused Income Portfolio - gained 2% after reporting EPS of $0.79/share - steady with last quarter - which covered its $0.62/share dividend. BXMT's BVPS increased to $26.30 - up 0.1% from last quarter. BXMT - which has 35% of its collateral in office-backed loans - noted that 96% of its portfolio is currently performing - down from 97% last quarter and 99% from a year earlier. Agency-focused AGNC Investment ( AGNC ) gained 3.5% after it reported comparable EPS of $0.67 - higher than Street estimates and covering its $0.36/share quarterly dividend - while its BVPS was $9.39/share at the end of Q2 - down 0.2% from last quarter. Highlighting the improved net interest spreads of 3.26% in Q2 vs. 2.88% in Q1, earnings commentary was notably upbeat with AGNC remarking, "we are at the forefront of one of the most constructive investment environments in our 15-year history." Orchid Island ( ORC ) gained 2% after reporting that its BVPS declined 3% during the quarter to $11.16, but recorded EPS of $0.25/share - well above Street estimates. Annaly Capital ( NLY ) gained 1% after reporting comparable EPS of $0.72 - slightly below Street estimates - and noting that its BVPS declined by 0.2% in Q2 to $20.73. Armour Residential ( ARR ) gained 1% after reporting comparable EPS of $0.23 - below Street estimates and shy of its $0.24/share dividend - while reporting that its BVPS declined 1.1% to $5.38.

{kind=link}

Hoya Capital

On the downside this week, PennyMac Mortgage ( PMT ) slid more than 7% after reporting disappointing results driven by underperformance from its interest-rate sensitive strategies and elevated hedge costs. PMT reported EPS of $0.16 in Q2 - down from $0.50 last quarter and short of its $0.40/share dividend - while noting that its BVPS declined about 1% to $15.81. On its dividend, PMT commented that it would "wait and see where we are at the end of next quarter" before making a decision on a potential reduction. Ellington Financial ( EFC ) slipped 1% after reporting preliminary second-quarter results, noting that its BVPS declined between 2-3% in Q2. Ladder Capital ( LADR ) - which has about 40% of its loan book backed by office assets - slipped 0.5% despite reporting comparable EPS of $0.33 - beating Street estimates - and noting that its BVPS climbed 0.2% to $12.07. Commercial lender KKR Real Estate ( KREF ) slipped 1.5% after it reported comparable EPS of $0.48/share - topping Street estimates and covering its $0.43/share quarterly dividend - but noted that its BVPS dipped 4.5% in Q2 driven by increased loan loss reserves allocated to its office loans. KREF's CECL allowance increased by $0.82/share driven by a revision in its risk rating from 4 to 5 on its $250M loan backed by a five-office building portfolio in Mountain View, California.

{kind=link}

Hoya Capital

Economic Calendar In The Week Ahead

Employment data highlights another critical week of economic data in the week ahead, headlined by the JOLTS report on Tuesday, ADP Payrolls data on Wednesday, Jobless Claims data on Thursday, and the BLS Nonfarm Payrolls report on Friday. Economists are looking for job growth of roughly 184k in July, which follows a decent month of June in which the economy added 209k jobs. The closely-watched Average Hourly Earnings series within the payrolls report - which is the first major inflation print for July - is expected to show a cooldown in wage growth in June to 4.2%. 'Good news is bad news' will likely be the theme of these reports as several Fed officials have pinned their decisions to pivot away from aggressive monetary tightening on a long-awaited cooldown in labor markets. We'll also be watching Construction Spending data on Tuesday and a flurry of PMI data throughout the week.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

Inflation Cools As Earnings Heat Up