AGNC - Inflation's Last Stand

2023-04-16 09:00:00 ET

Summary

- U.S. equity markets finished broadly higher this past week after a critical slate of inflation data provided further evidence of a definitive cool-down in inflationary pressures.

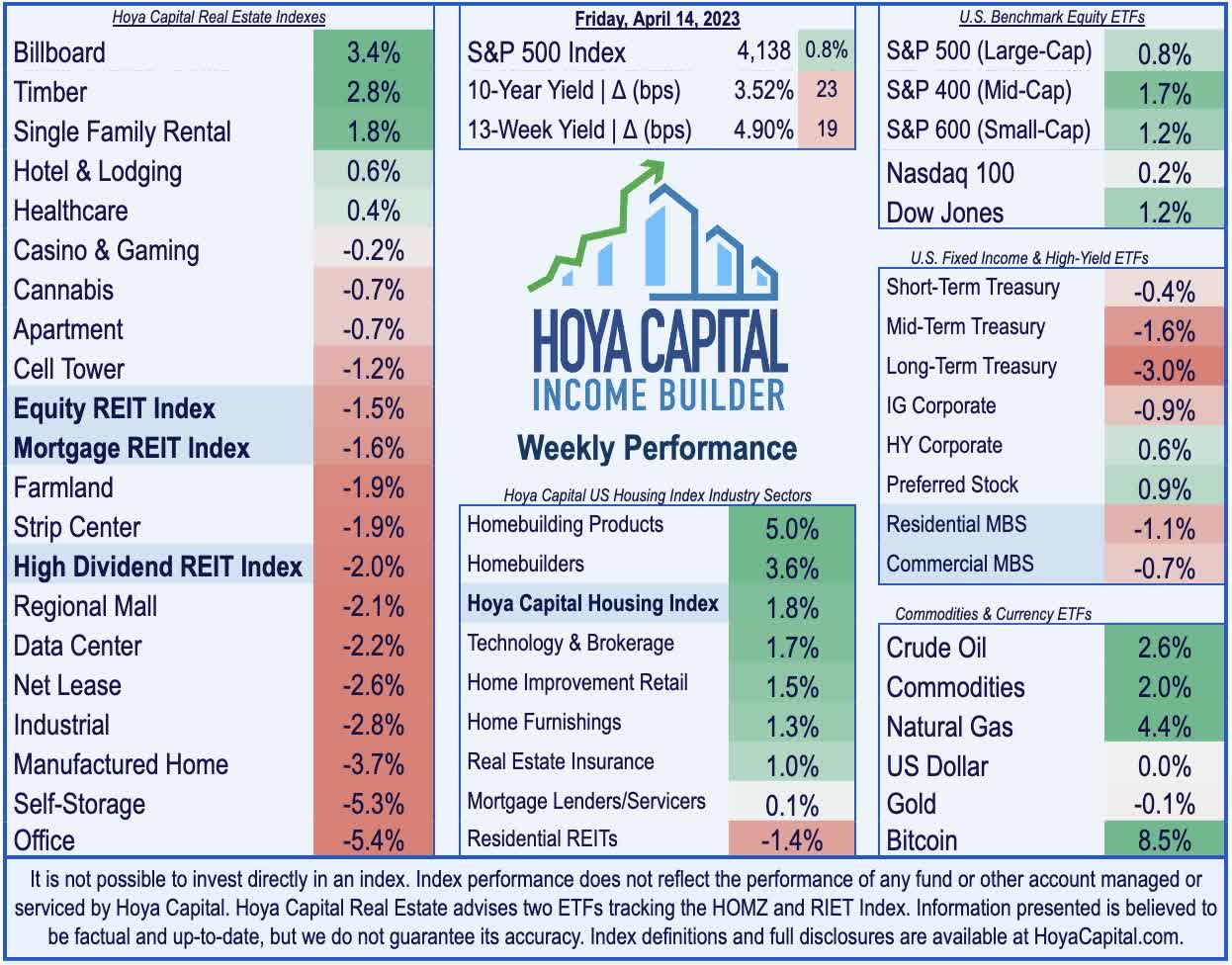

- After narrowly snapping a three-week winning streak in the prior week, the S&P 500 advanced 0.8% this week, while the Mid-Cap 400 and Small-Cap 600 posted gains of over 1%.

- Real estate equities were among the laggards for a second-straight week, pressured by a rebound in benchmark interest rates, which rose despite the encouraging inflation news.

- The darker "underbelly" of the REIT sector dominated the news flow this week, which saw a controversial merger between two RMR-advised REITs, a turbulent direct listing of a previously non-traded REIT, and Blackstone unloading assets to meet redemptions.

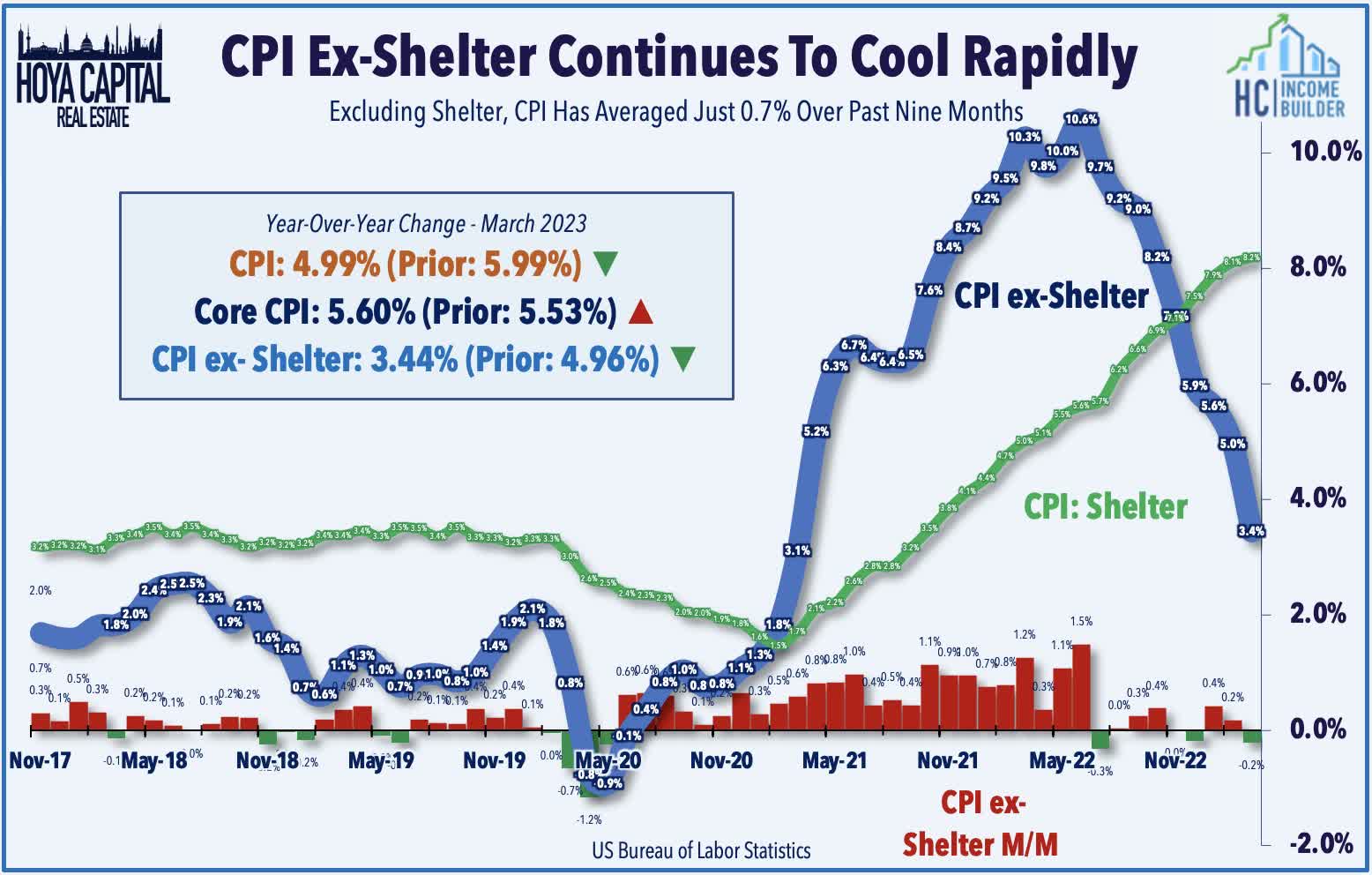

- The closely-watched CPI-ex-Shelter Index - the metric that showed the historic surge in inflation a year before it was reflected in the headline CPI and acknowledged by the Federal Reserve - has actually been in deflationary territory over the past three quarters.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on April 14th.

U.S. equity markets finished broadly higher this past week after a critical slate of inflation data provided further evidence of a definitive cool-down in inflationary pressures, which again revived "soft-landing" hopes. The closely-watched CPI-ex-Shelter Index - the metric that showed the historic surge in inflation a year before it was reflected in the headline CPI and acknowledged by the Federal Reserve - has been in deflationary territory over the past three quarters, raising questions over whether the Fed is again caught offsides.

{kind=link}

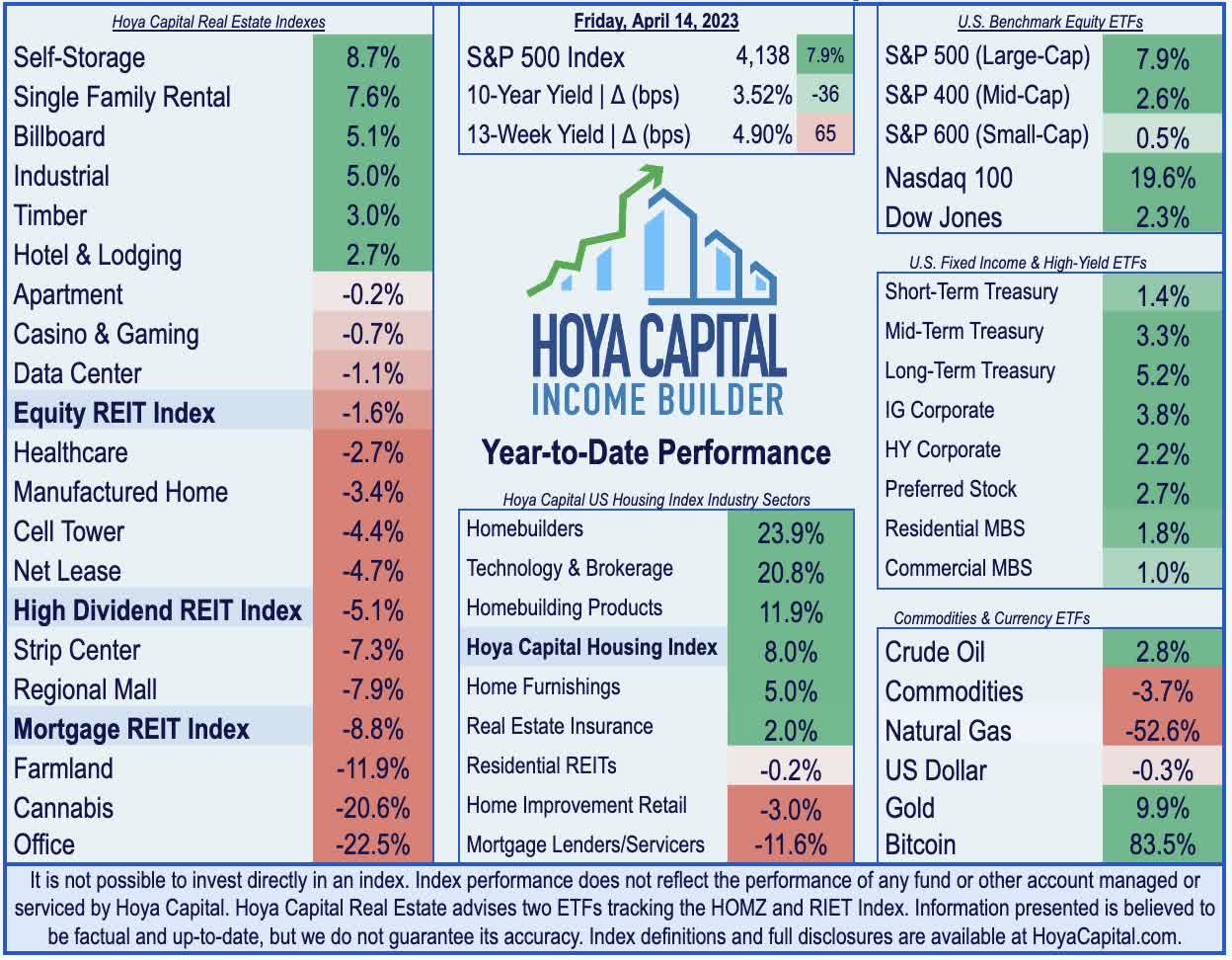

After narrowly snapping a three-week winning streak in the prior week, the S&P 500 advanced 0.8% this week, while the Mid-Cap 400 and Small-Cap 600 each posted gains of over 1%. The tech-heavy Nasdaq 100 finished higher by 0.2%, giving back some of its double-digit percentage-point outperformance this year over the other major benchmarks. Real estate equities were among the laggards for a second-straight week, pressured by a rebound in benchmark interest rates, which rose despite the encouraging inflation news. The Equity REIT Index slipped 1.5% on the week, with 13-of-18 property sectors in negative territory, while the Mortgage REIT Index declined by 1.6%. Homebuilders and the broader Hoya Capital Housing Index continued their rebound, however, on further signs of thawing in the once icy-cold housing market ahead of the critical Spring season.

{kind=link}

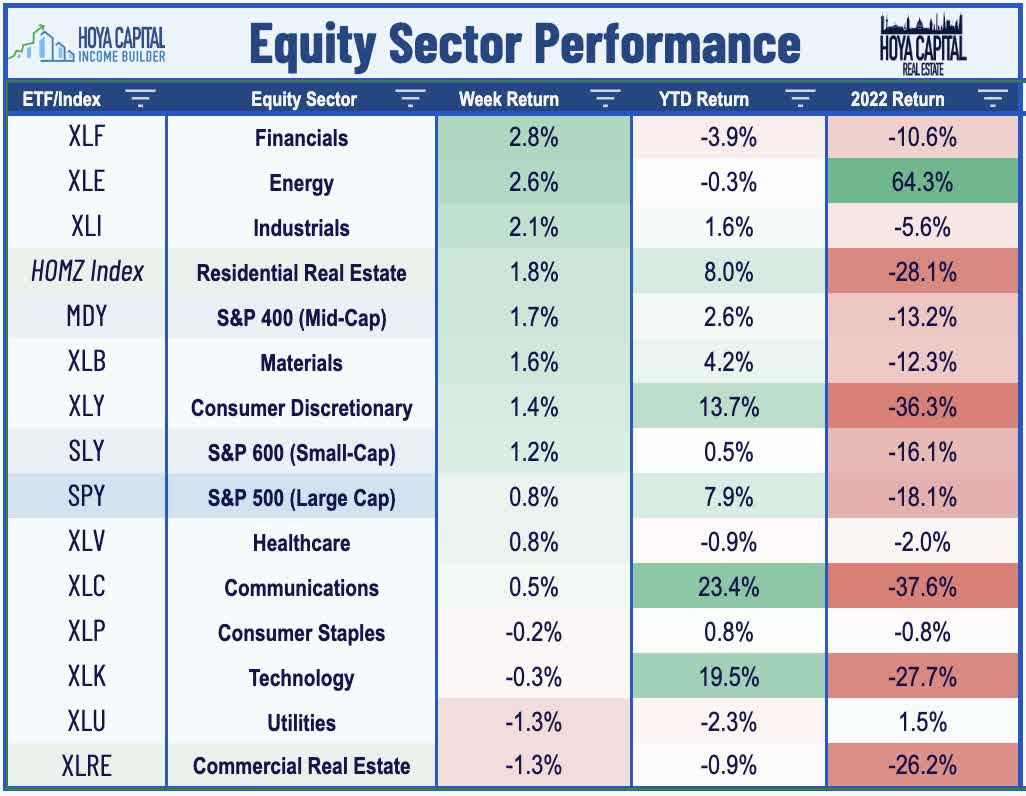

While volatility in equity markets declined to the lowest levels in over a year this week, volatility across fixed-income markets remained elevated this week, with benchmark interest rates ultimately ending the week near the highest-levels since the Silicon Valley Bank collapse in early March. Benchmark yields pared their post-CPI report declines after minutes from the Federal Reserve's meeting showed that officials were unanimous in their support for the 25 basis point rate hike in March, and ultimately pushed higher on the week following stronger-than-expected bank earnings from JPMorgan (JPM), Wells Fargo (WFC), and Citigroup (C), which showed little symptoms of contagion in the wake of the second and third-largest bank failures in U.S. history in March. Six of the eleven GICS equity sectors finished higher on the week, with Financials ( XLF ) and Energy ( XLE ) stocks leading on the upside.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

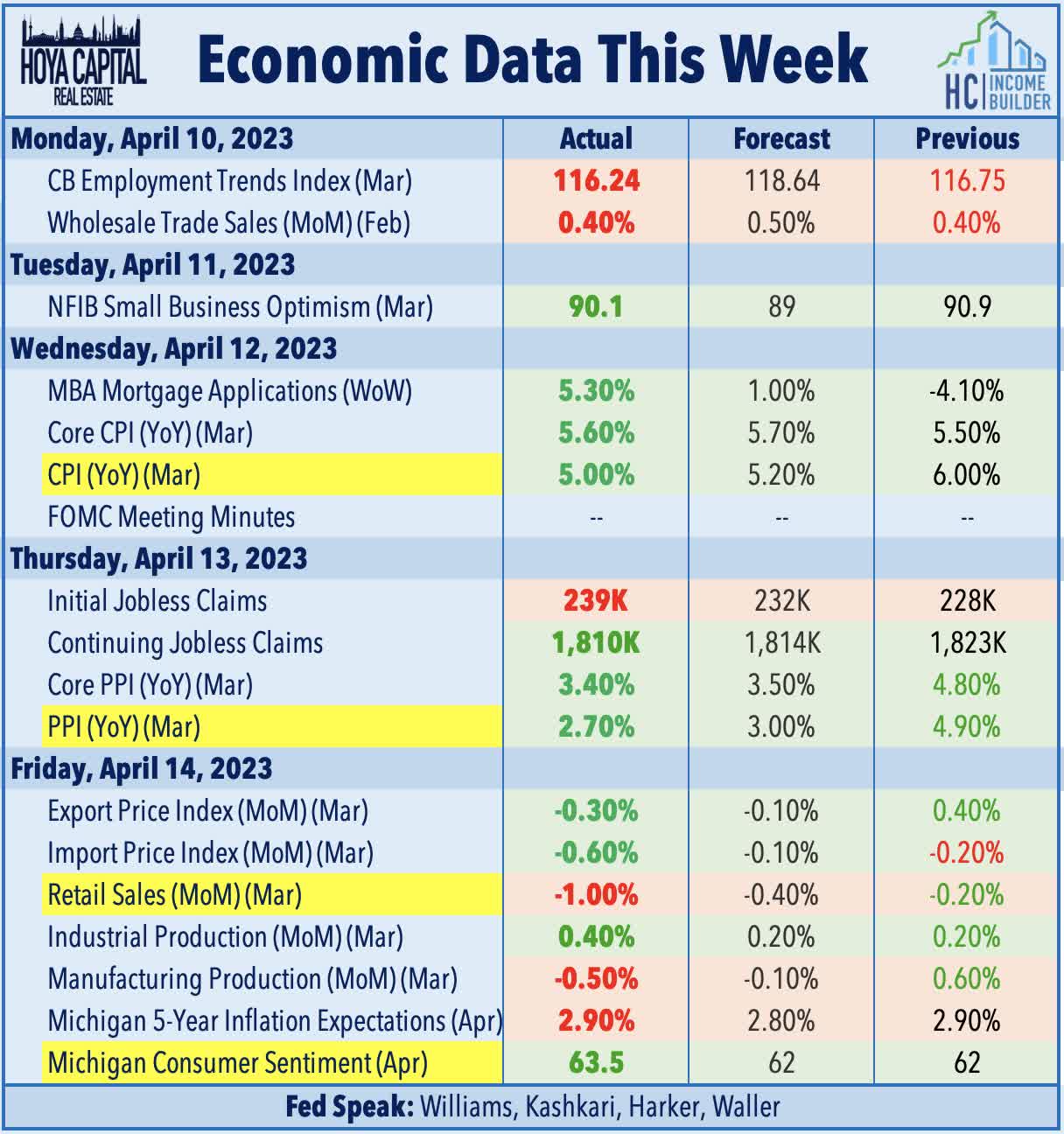

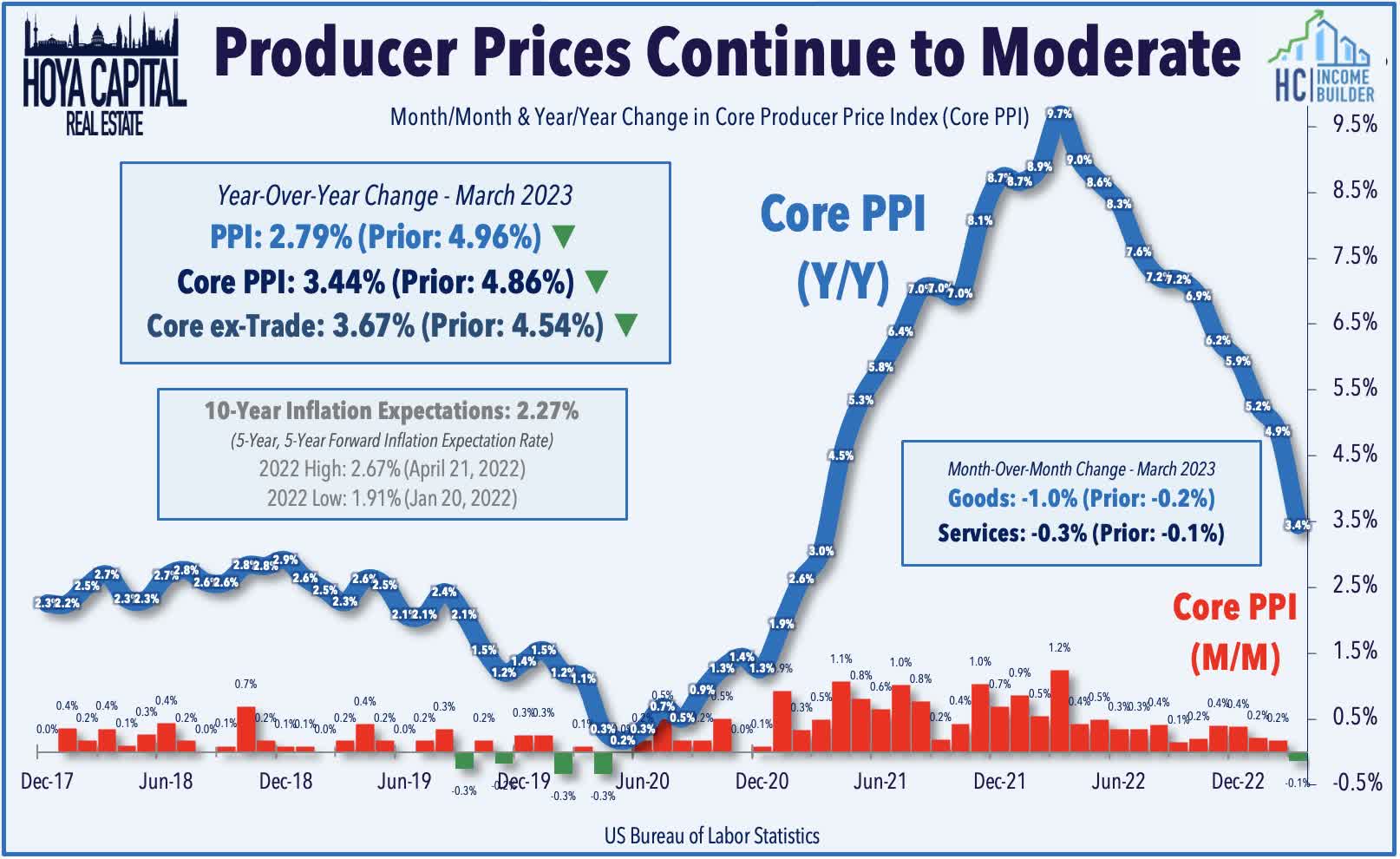

All eyes were on the Consumer Price Index report this week, which showed a rather precipitous cool-down in inflationary pressures, as the headline CPI inflation rate moderated to 4.99% in March, down a full percentage point from the 5.99% annual rate in February. Notably, just one month in the past 15 years has recorded a steeper month-over-month decline in the annual rate - April 2020. The delayed recognition of shelter inflation continues to heavily distort the headline and core metrics. Despite real-time rent and home prices metrics showing muted - or negative - increases since mid-2022, the CPI Shelter Index soared 8.2% - the highest in four decades - and accounted for 60% of the monthly CPI increase. The metric that we watch most closely - CPI-ex-Shelter Index - showed that since July, aggregate prices have declined by about 1% on an absolute basis. When the BLS Rent Index is replaced with the Zillow ZRI Rent Index, we observe a sharp decline in the CPI Index since mid-2022, with this "Real-Time CPI" slowing to just 2.1% in March.

{kind=link}

Later in the week, Producer Price Index data was also significantly cooler-than-expected, showing that wholesale prices declined by the most in nearly three years in March. The headline PPI posted a 0.5% month-over-month decline for the month, dragging the annual increase to just 2.7%, the lowest since January 2021. The Core PPI Index, meanwhile, recorded a month-over-month decline for the first time since May 2020. Sharp declines in energy prices helped to drag goods inflation lower by 1.0% in the month, while services prices - which had been 'stickier' in recent months - declined by 0.3% in March, which was the largest decline since falling 0.5% in April 2020. Forward-looking sub-series within the PPI report were encouraging as well, with the cost of partly finished goods falling for the eighth time in nine months.

{kind=link}

Equity REIT Week In Review

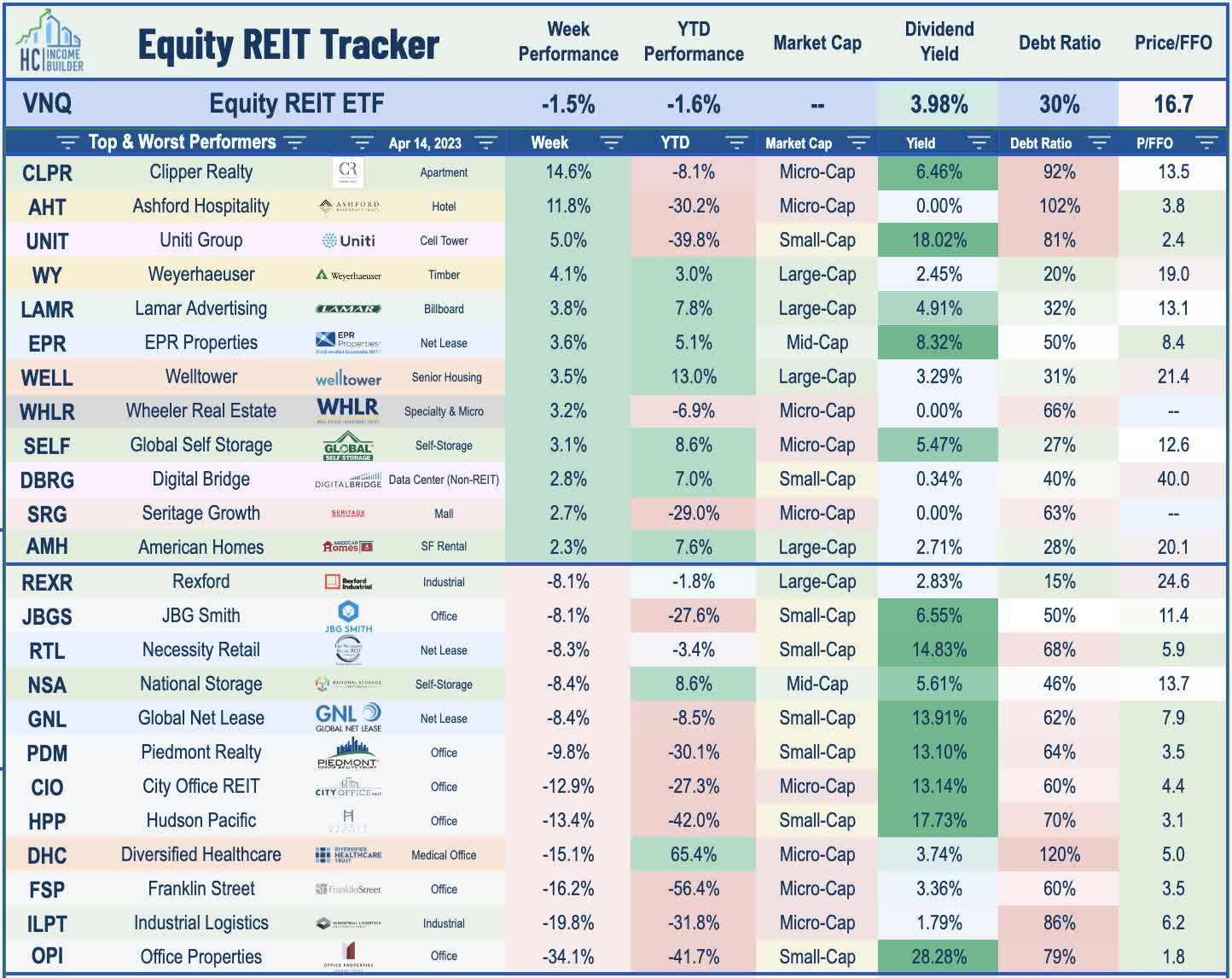

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Healthcare & Office : A pair of struggling externally-managed REITs advised by RMR Group - Office Properties Income ( OPI ) and Diversified Healthcare ( DHC ) - announced plans to combine in a controversial deal that sent both stocks sharply lower on the week. OPI owns 160 traditional office properties across 30 states, while DHC owns 379 properties across 36 states - primarily medical office and senior housing properties. Markets interpreted the deal as a "bail-out" for DHC, which traded as low as $0.65/share last year and is saddled over $3B in debt against its sub-$300M market capitalization. Under the proposed terms, DHC shareholders would receive 0.147 shares of OPI per share of DHC, which represented a nearly 40% premium to the prior closing price. DHC has $700 million of debt coming due by mid-2024 and wasn’t in compliance with its debt covenants. The combined company - which will be named " Diversified Properties " - would pay an annual dividend of $0.25/quarter, down 55% from OPI's current dividend rate of $0.55/quarter.

{kind=link}

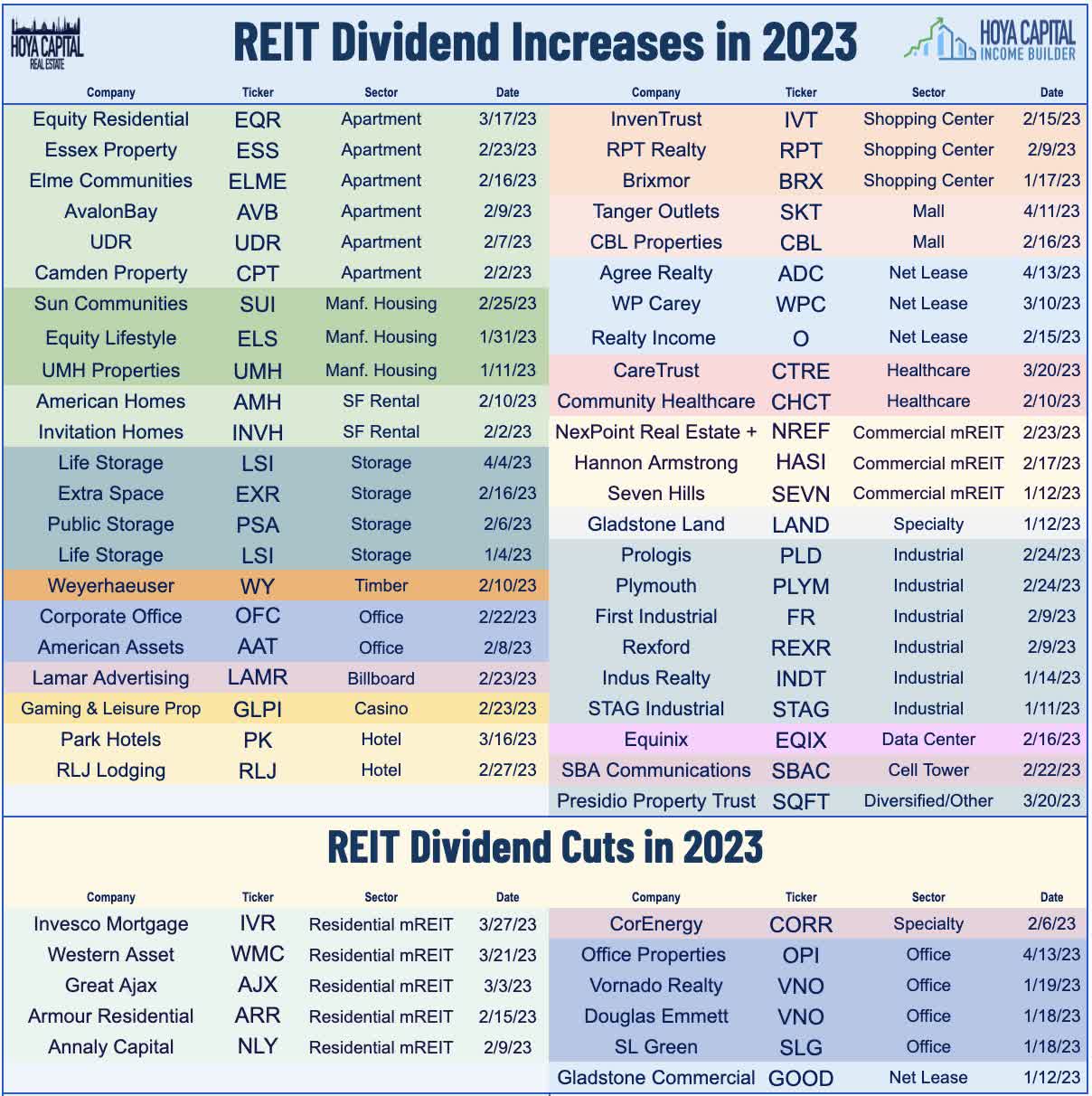

On the upside, two REITs hiked their dividends this week, raising the full-year total of REIT dividend hikes to 45. Tanger Factory Outlet ( SKT ) was among the better-performers this week after hiking its quarterly dividend by 11% (5.1% yield) - its fourth dividend hike since it resumed payouts in early 2021 after a pandemic suspension. Net lease REIT Agree Realty ( ADC ) raised its monthly dividend by 1.2% to $0.243/share (4.4% yield) - its fifth dividend hike since the start of 2021. Of note, while Tanger's dividend remains about 30% below its pre-pandemic rate, Agree's dividend is now 56% above its pre-pandemic level. The dividend reduction from Office Properties Income is the eleven REIT dividend cut this year - essentially all of which have come from either the office or mortgage REIT sectors. Last year, another RMR-advised REIT - Industrial Logistics ( ILPT ) - was one of just two REITs to lower their dividend.

{kind=link}

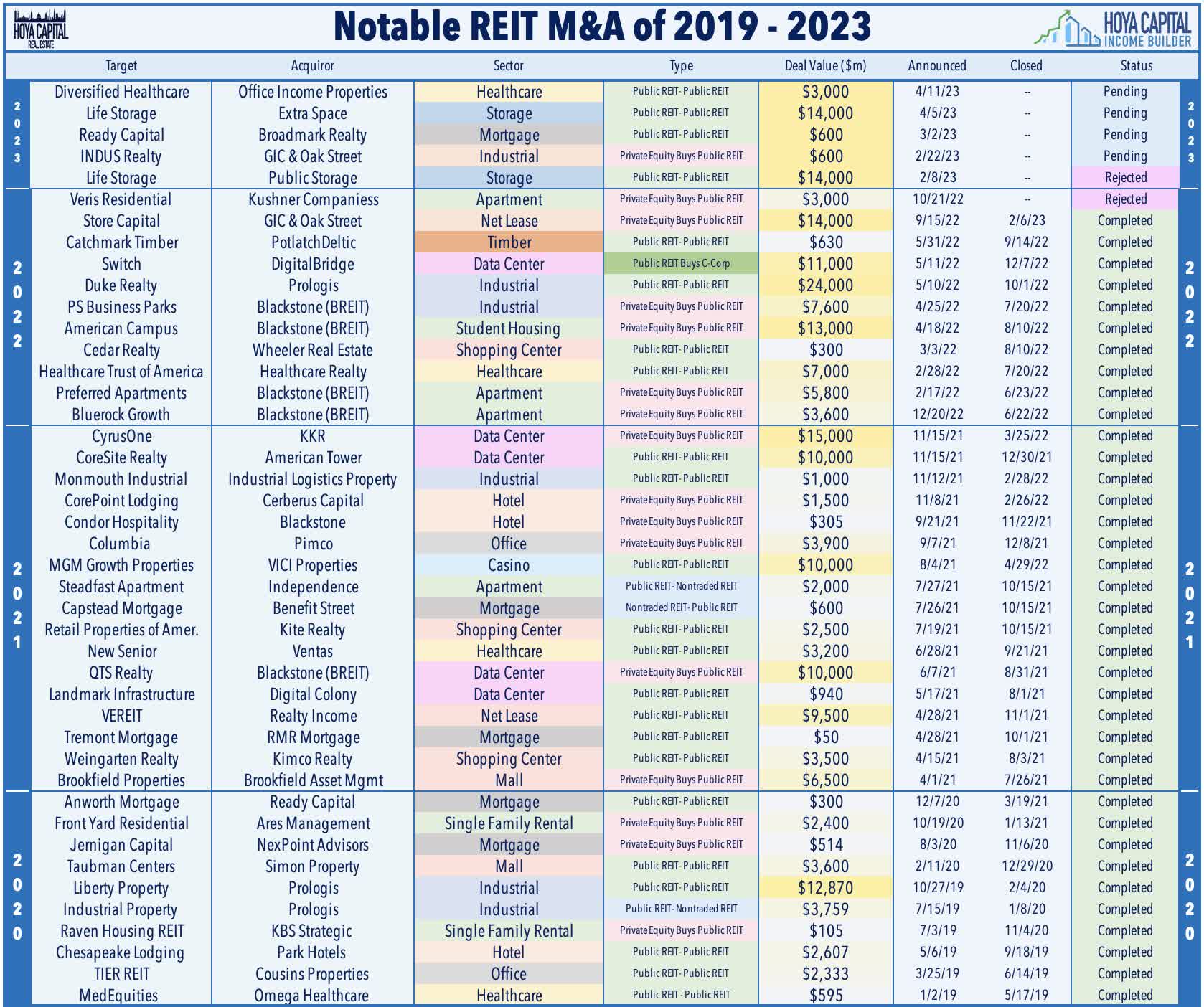

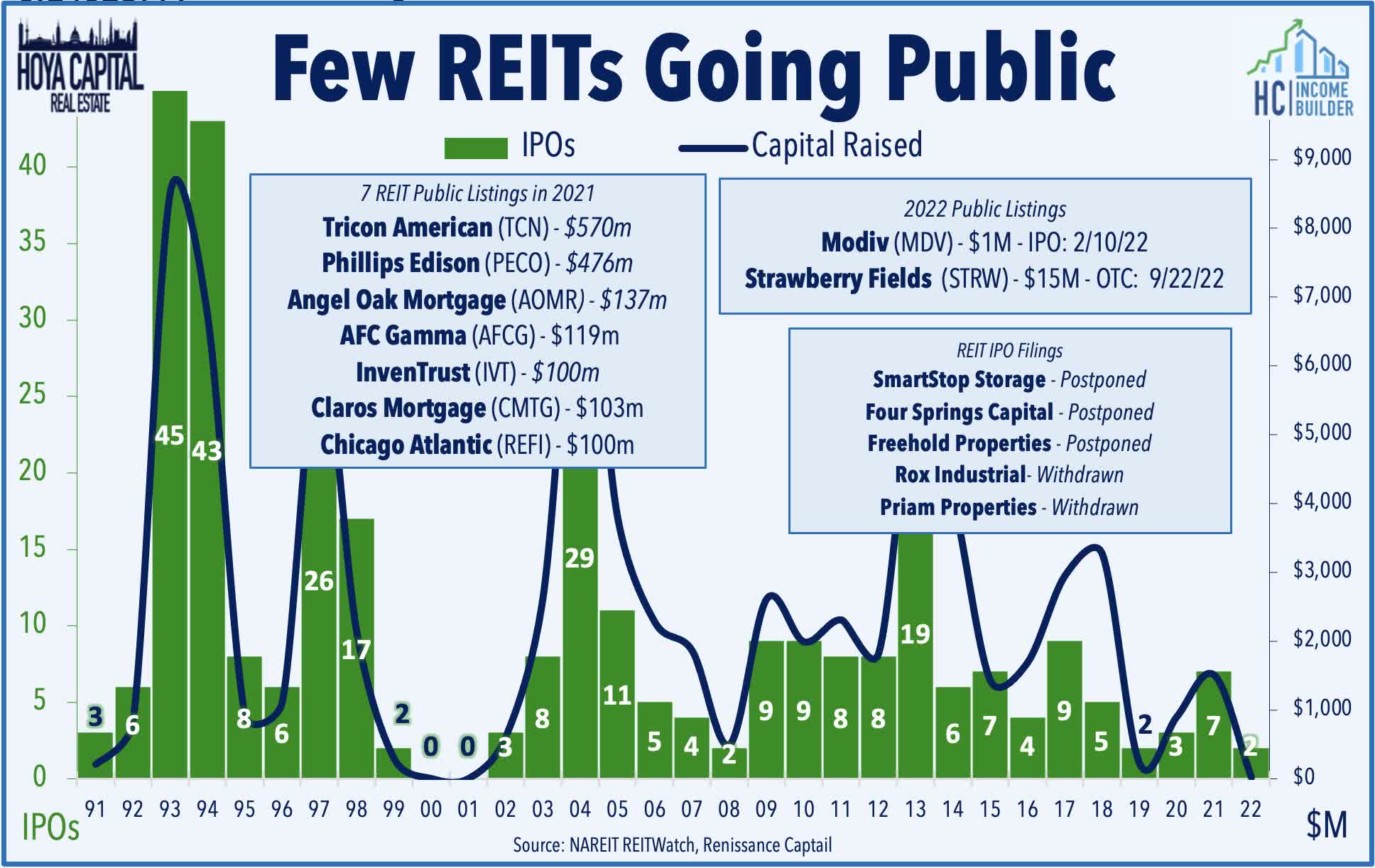

Net Lease : Speaking of REITs with a history of questionable corporate governance practices, Peakstone Realty Trust ( PKST ) - formerly known as Griffin Realty Trust - began trading on NYSE this week through a direct listing. As noted in our State of the REIT Nation report, REIT IPOs have been essentially non-existent over the past year following a wave of activity in 2021 - a year that saw seven public listings, the most since 2013. There were no REIT IPOs in 2022 for the first time since 200. Peakstone is a net lease office and industrial REIT that owns 78 properties across 24 states. Roughly 70% of PKST's Net Operating Income ("NOI") is derived from its portfolio of 55 office properties, while 30% of NOI comes from its portfolio of 23 industrial properties. The wild first week of trading resulted, in part, from confusion over a 1-for-9 reverse share split that took effect last month. Griffin Real Estate advises a collection of non-traded REITs and closed-end funds and has faced several lawsuits over its suspension of share redemptions and NAV valuations.

{kind=link}

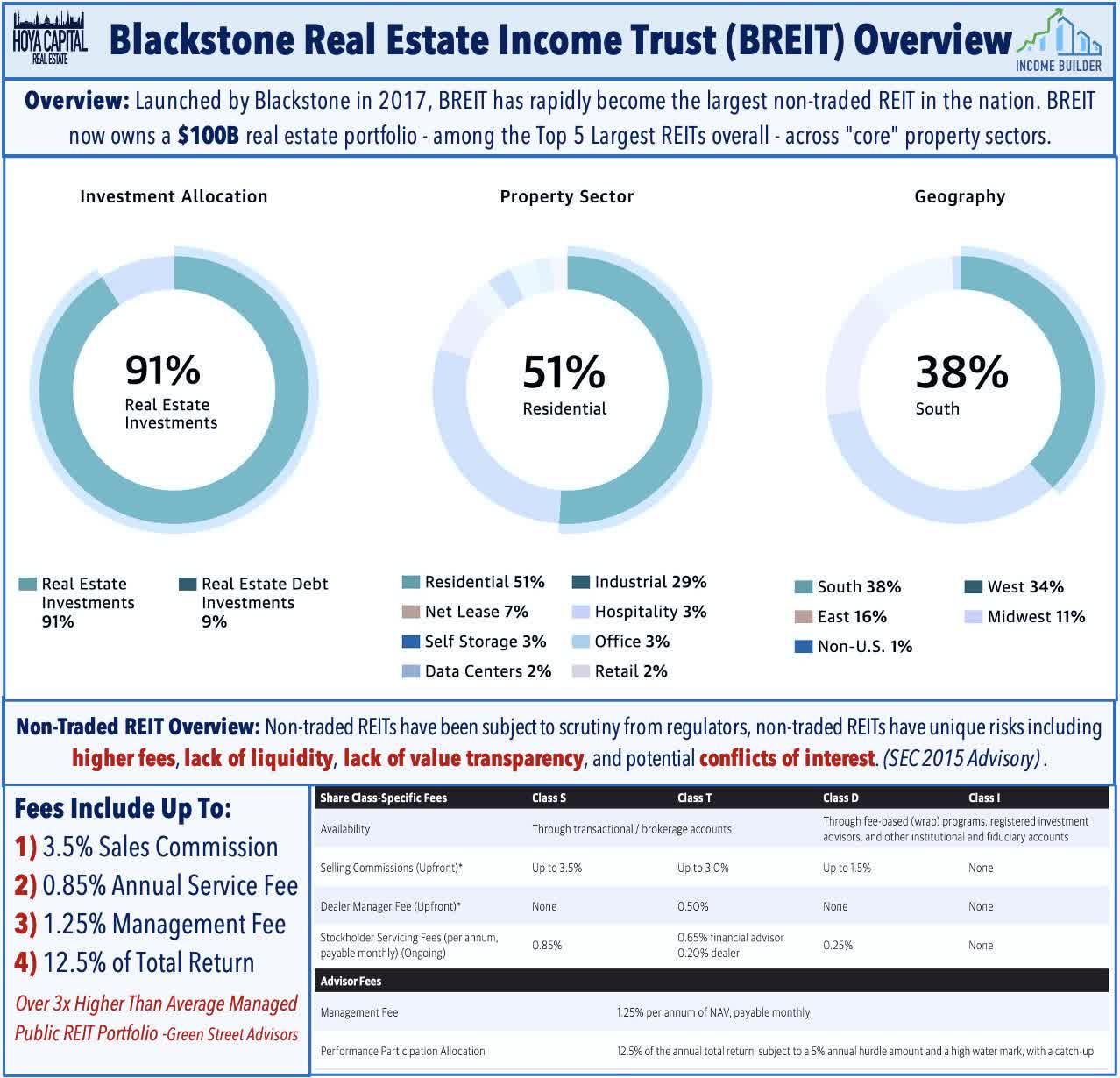

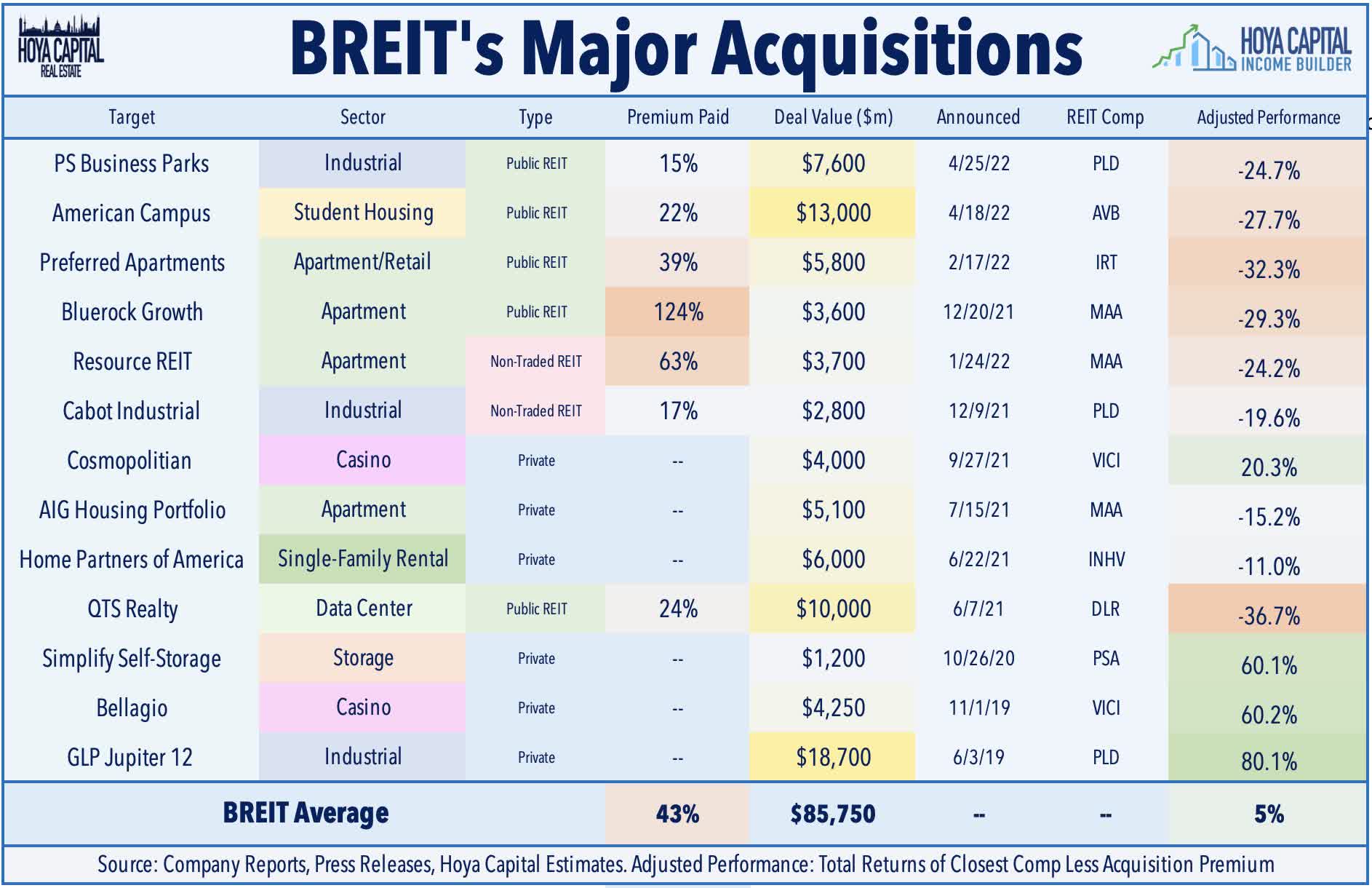

On that point, another non-traded REIT advisor - Blackstone ( BX ) - was again in focus this week after it announced that it closed on its largest real estate drawdown fund, securing $30.4 billion of total capital commitments for its Real Estate Partners X, which will target "opportunistic deals across sectors such as rental housing, hospitality and data centers." The announcement comes a week after Blackstone Real Estate Income Trust ("BREIT") disclosed that it again had to limit withdrawals from the $70 billion non-traded real estate fund in March - the fifth straight month that the firm's flagship fund limited redemptions. Total redemption requests for March jumped to $4.5B - up 15% from the prior month, and Blackstone fulfilled just 15% of these requests - $666M - down from 35% in February and 25% in January.

{kind=link}

Next week, we'll publish a report analyzing BREIT - focusing on its acquisition history and performance relative to comparable public REITs, and the effects of the wave of redemptions on the rest of the public REIT sector. While not necessarily a "forced seller" at this point given BREITs' ability to exercise these redemption limits, Blackstone has been actively shopping assets in recent months to raise capital to meet the redemption requests. This week, BREIT sold a $263M portfolio of industrial properties in Southern California that were acquired as part of its acquisition of PS Business Parks. The 850k square foot portfolio - comprised of 45 buildings in Los Angeles and Orange County - was acquired by DRA Advisors. Last week, Blackstone sold a pair of office buildings in Southern California for $82M - which was reportedly 36% less than Blackstone paid to acquire the assets nine years ago.

{kind=link}

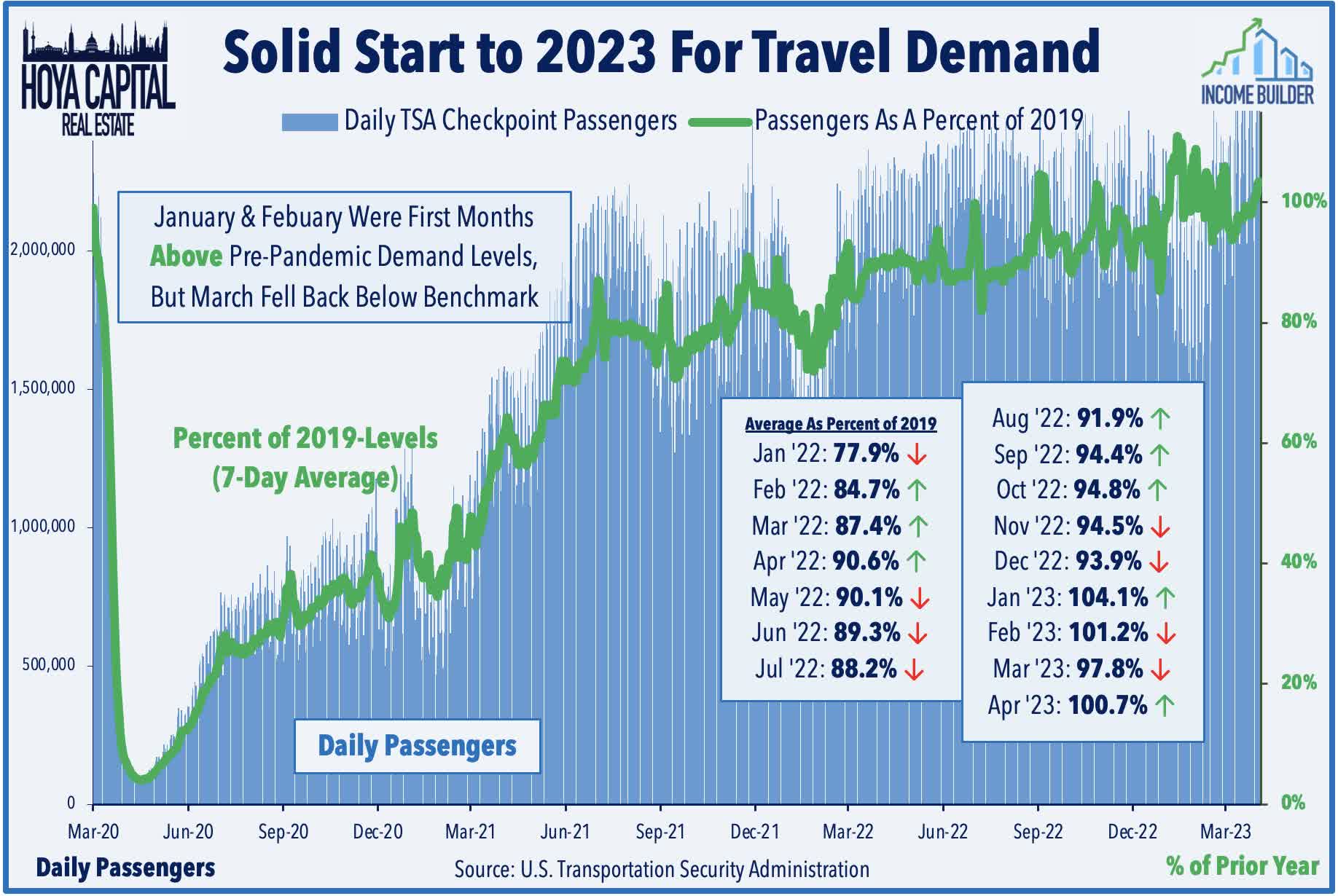

Hotel : On the upside this week, Ashford Hospitality ( AHT ) rallied more than 11% after it provided preliminary first-quarter operating metrics. AHT - which owns 100 hotels across roughly 14 markets - expects to report Revenue Per Available Room ("RevPAR") of $125 for the first quarter of 2023, which is 30% above 2022-levels and roughly 2.5% above the $122.10 reported in Q1 of 2019. AHT - which is the single-most highly-levered REIT on a Debt Ratio basis - also noted that the percentage of properties currently under 'cash traps' declined to 40%, down from 79% at the end of Q4 2022. A cash trap means that we are currently unable to utilize property-level cash for corporate-related purposes. A "cash trap" is a provision in hotel loans that is effective when the hotel is not meeting financial covenants such as debt-service-coverage ratios. During a cash trap, operating revenues from the hotel are collected in an account controlled by and pledged to the lender and then used to pay costs of the hotel in a set order. Recent TSA Checkpoint data shows relatively strong demand trends in early 2023 with both January and February exceeding pre-pandemic throughput levels, but March saw a slight downshift in demand to about 2% below comparable 2019-levels.

{kind=link}

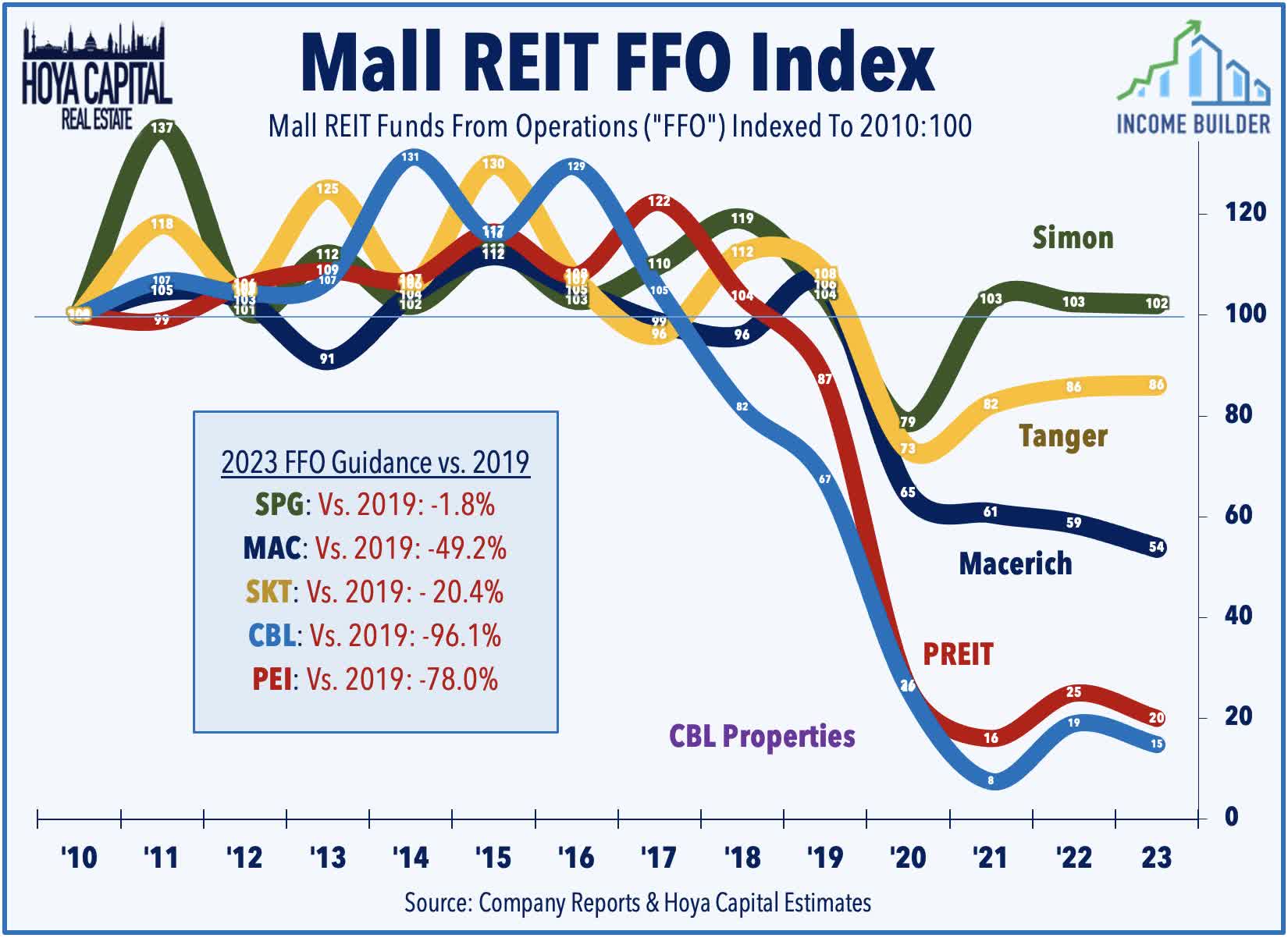

Malls : This week, we published Mall REITs: No Longer the 'Problem Child' which discussed recent earnings results and our updated outlook on the sector. Following nearly three-years of rental rate and occupancy declines, the supply-demand dynamic has recently favored retail landlords, rewarding many retail REITs with some long-elusive pricing power. Unlike their strip center REIT peers, however, mall REITs are still trying to claw their way back to pre-pandemic levels as improving property-level performance has recently been offset by higher financing costs. Outside of Simon ( SPG ) and Tanger ( SKT ), however, the remainder of the mall sector continues to teeter dangerously close to the edge. We noted that Macerich ( MAC ) needs some luck to avoid the fate of the lower-tier REITs that have been stuck in a seemingly endless loop in-and-out of restructurings and de-listings.

{kind=link}

Mortgage REIT Week In Review

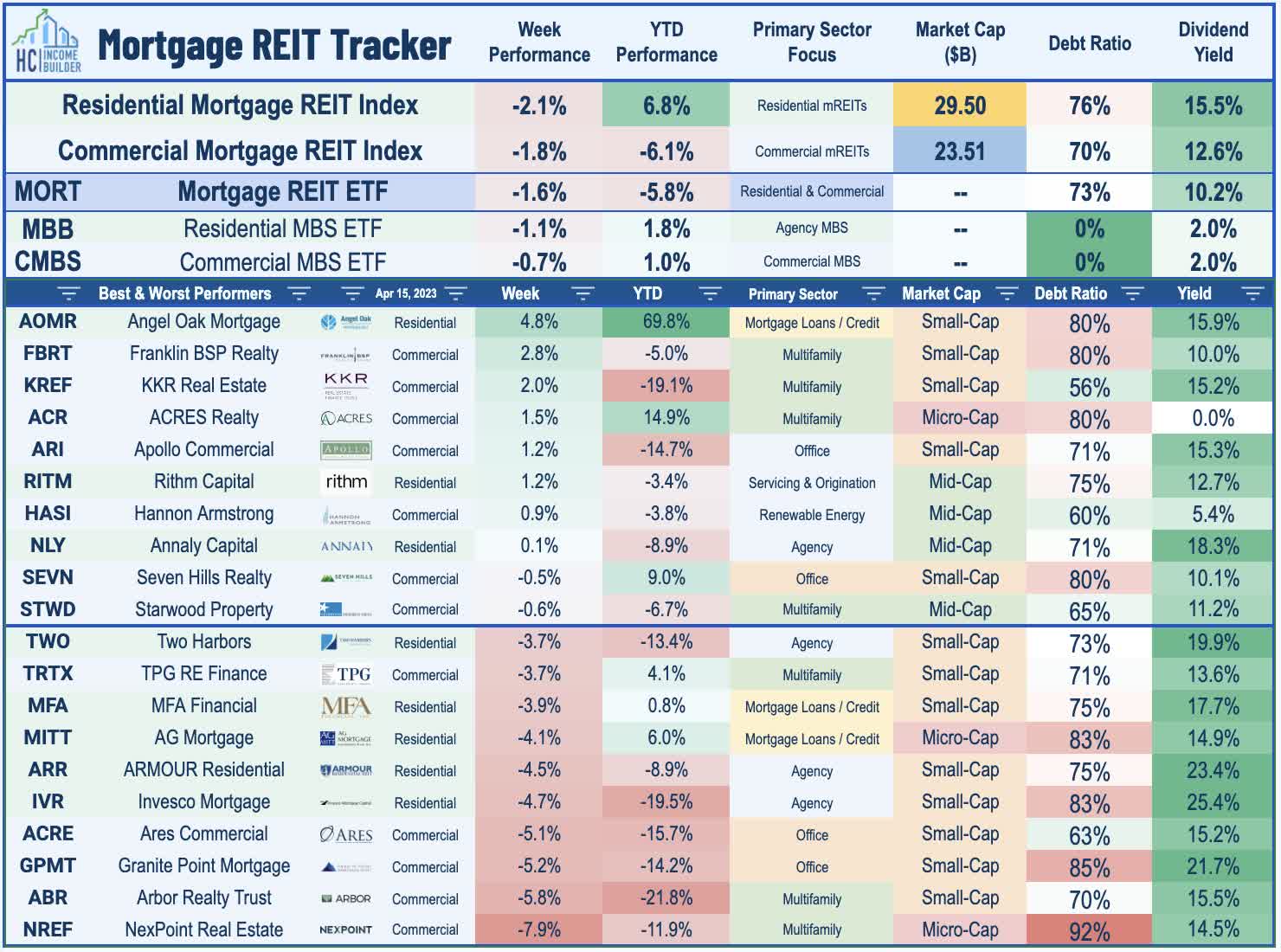

Mortgage REITs also finished lower on the week - pressured by the rebound in interest rates - with the iShares Mortgage Real Estate Capped ETF ( REM ) slipping 1.6%. News flow was quiet this week in the mREIT space ahead of the start of earnings season later this month. Orchid Island ( ORC ) was among the better-performers after it announced preliminary first-quarter results, noting that its estimated Book Value Per Share at the end of Q1 was $11.56 - down about 3% from the end of Q4 - and noted that it expects to report Q1 GAAP EPS of $0.10. ORC also held its monthly dividend steady at $0.16/share (17.5% yield) - one of six mREITs to declare dividends this week - all of which maintained their payouts at current rates: AGNC Investment ( AGNC ) held its monthly dividend steady at $0.12/share (14.4% yield), Seven Hills ( SEVN ) held at $0.35/share (14.0% yield), Dynex Capital ( DX ) held at $0.13/share (13.0% yield), Ellington Financial ( EFC ) held at $0.15/share (14.7% yield), and Ellington Residential ( EARN ) held at $0.08/share (13.4% yield).

{kind=link}

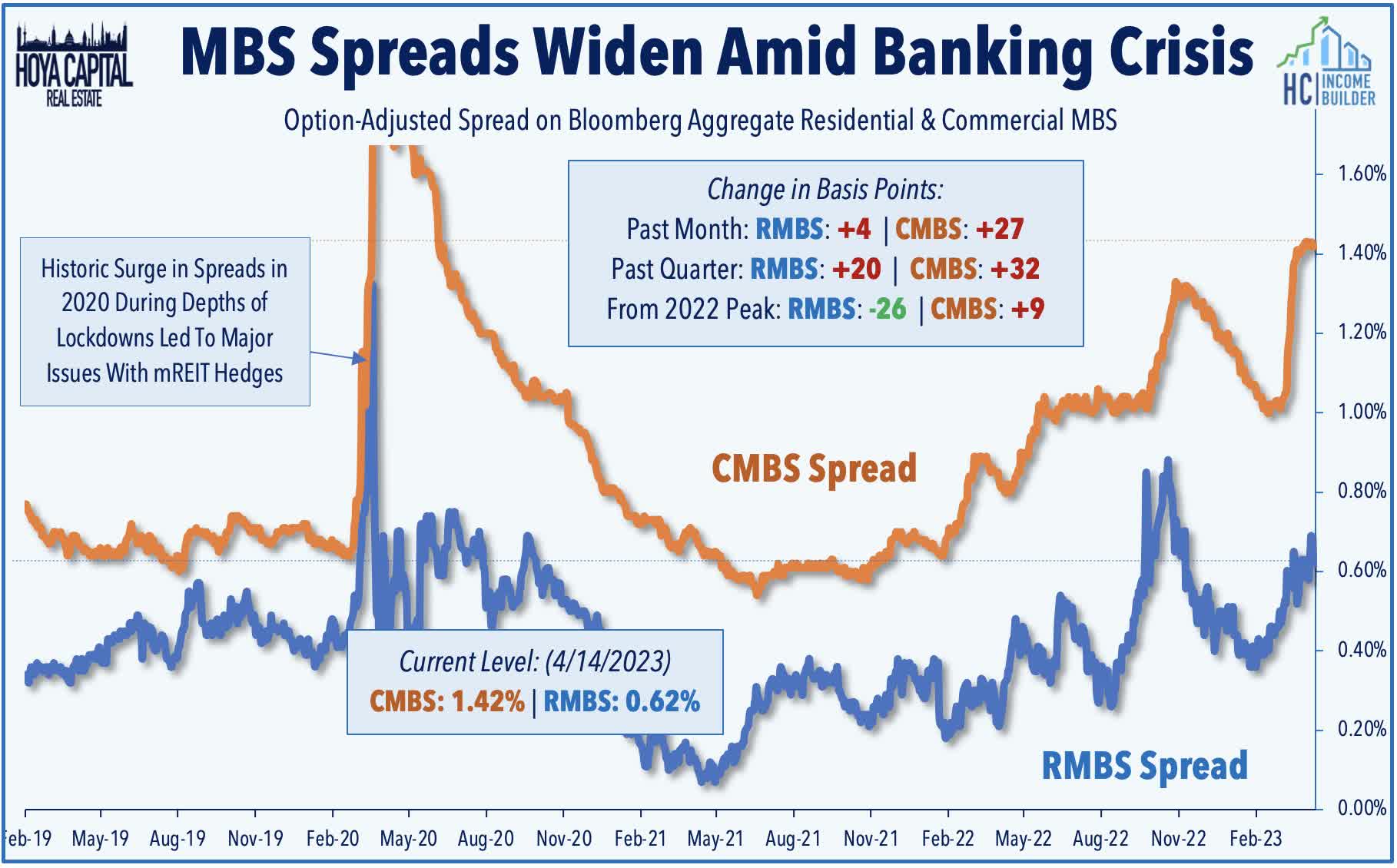

We've kept our eyes on the underlying Residential MBS ( MBB ) and Commercial CMBS ( CMBS ) markets throughout the recent banking crisis. Despite slipping about 1% ono the week, these indexes remain in positive territory for the year - a surprise for some, considering the amplified media focus in recent weeks - as downward pressure from wider spreads has been offset by tailwinds from lower benchmark interest rates. CMBS spreads widened from 1.16% at the end of Q4 to 1.42% at the end of Q1 (26 basis points) and have held steady through the first two weeks of Q2, while RMBS spreads widened from 0.50% to 0.63% during the quarter (13 basis points) and have also steady over the past two weeks. We discussed in our Mortgage REITs report how sharp changes in benchmark rates and/or spreads in either direction can wreak havoc on mortgage REITs that are caught over-levered or improperly hedged.

{kind=link}

2023 Performance Recap & 2022 Review

Through fifteen weeks of 2023, the Equity REIT Index is now lower by 1.6% on a price return basis for the year, while the Mortgage REIT Index is lower by 8.8%. This compares with the 7.9% gain on the S&P 500 and the 2.6% advance for the S&P Mid-Cap 400 . Within the real estate sector, 6-of-18 property sectors are in positive territory on the year, led by Self-Storage, Single-Family Rental, and Billboard REITs, while Office REITS have lagged on the downside. At 3.52%, the 10-Year Treasury Yield has declined by 36 basis points since the start of the year - well below its 2022 closing highs of 4.30%. The US bond market has stabilized following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 3.0% this year.

{kind=link}

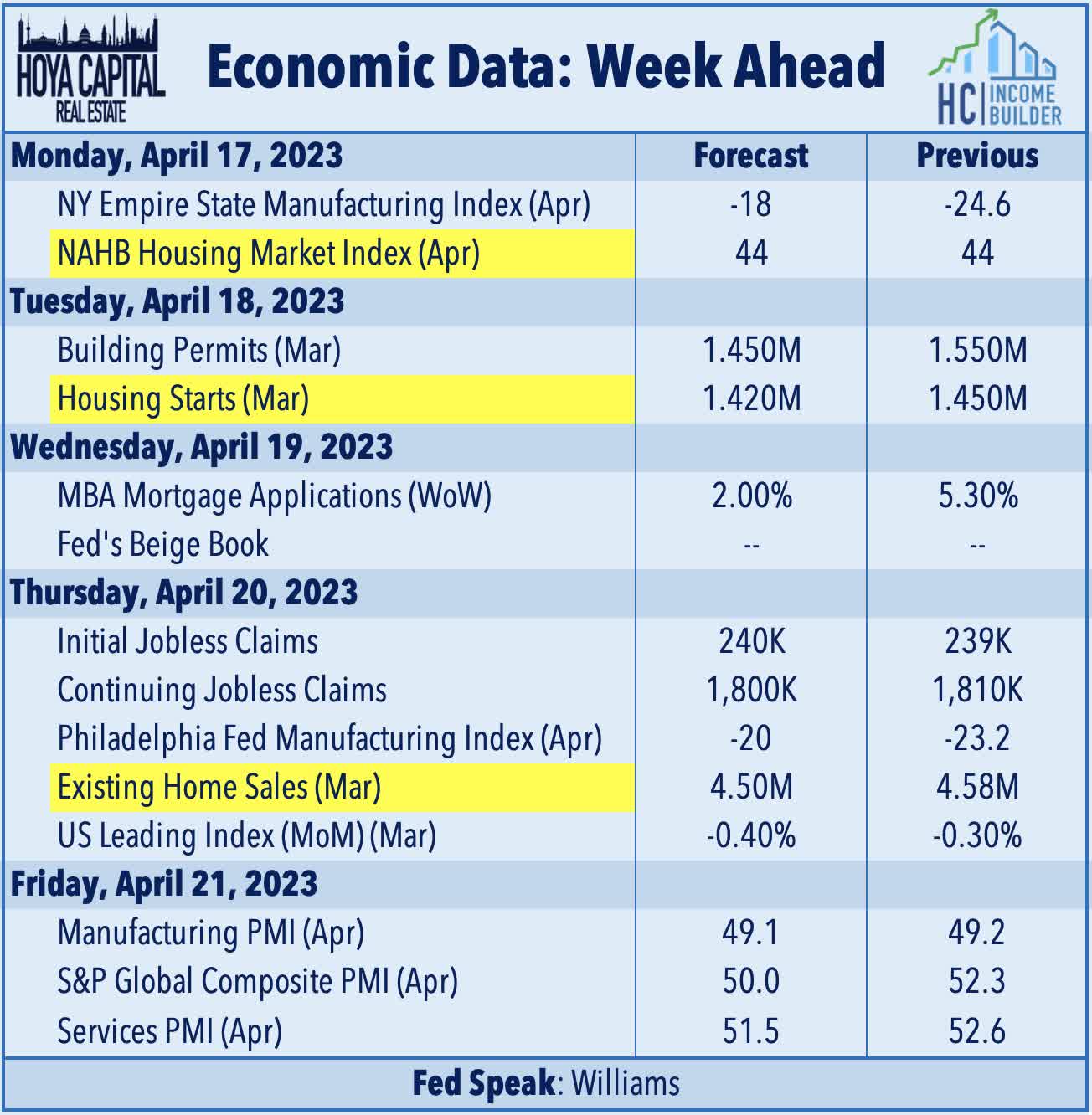

Economic Calendar In The Week Ahead

The state of the U.S. housing market will be in focus in the week ahead. The busy week starts on Monday with NAHB Homebuilder Sentiment data for April which looks to extend its streak of three-straight monthly increases after dipping to near-15-year lows late last year. On Tuesday, we'll see Housing Starts and Building Permits data for March, which are expected to moderate slightly after a stronger-than-expected February. On Wednesday, we'll be watching mortgage-market data, specifically the MBA Mortgage Applications index, which has advanced in five-of-six weeks. We'll see Existing Home Sales data on Thursday which is expected to decline slightly in March to a 4.50 million seasonally-adjusted annualized rate - up from the lows in January of 4.0 million, but well below the 2021 highs of over 6.5 million. We'll also be watching weekly Jobless Claims data on Thursday and a busy slate of PMI data throughout the week.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Inflation's Last Stand