TIPT - Inflation Update: The Fed Is In A Tight Spot Of Its Own Making

2023-05-01 14:29:31 ET

Summary

- The Fed is likely to raise rates 25 basis points this coming week.

- Inflation is slowing but not enough for the Fed to even consider rate cuts.

- The equity market seems to expect this raise to be the last one. If it's not, it could be a bumpy summer.

- Even before a credit slowdown, most measures of industrial production point to a recession having already started.

Barron's Article on Inflation

This weekend's edition of Barron's included an article about the tough spot in which the Federal Reserve finds itself. The main crux was "The central challenge for the Fed is that the economic outlook is souring at the same time that progress on reining in inflation is stalling out." Basically, many measures of economic activity reveal many sectors and geographies already in recession while inflationary measures such as CPI and core PCE are coming down at a slower pace and remain at too high levels.

I started writing about inflation in the late summer of 2021 with an article, "Inflation: Is It Something to Fear and How Do You Protect Your Portfolio From It" . If you prefer not to read it, I mentioned that I believed Jerome Powell was mistaken that inflation was "transitory" specifically when it came to food, energy, housing, and wages. I also suggested a few ways to play it.

Fortunately for my track record, I was right about inflation, and most individual stocks I suggested would perform well in an inflationary environment, which included EQT Corp ( EQT ) up 96%, Enterprise Products ( EPD ) up 33.5%, Crestwood ( CEQP ) up 8%, Bunge ( BG ) up 28%, Andersons's ( ANDE ) up 51.25%, Tiptree ( TIPT ) up 38.5%. I was wrong about Ferroglobe ( GSM ) down 47%, whose worst-case EBITDA multiple has compressed to 3x, and WP Carey ( WPC ) is only up 5%.

The trouble with inflation is that once it takes hold, it is hard to break without a restrictive monetary policy that lasts longer than I think many people realize. Without massive supply gluts, the Fed has to break demand. For example, auto production has not fully recovered, and prices remain high for new and used cars. Therefore, the Fed reduces demand by making auto financing so expensive that people simply can't afford many car payments. To this end, auto dealers such as Lithia ( LAD ) and CarMax ( KMX ) as well as auto finance companies such as Ally Financial ( ALLY ), are seeing lower volumes. But sales have not been bad enough for long enough for inventories to build and force prices down materially.

We're seeing the same dynamic play out in housing. Mortgage rates are high, too high for many people to afford new home purchases. Similarly, financing costs for new apartment development have become restrictively high for new projects, and several recently completed projects have defaulted.

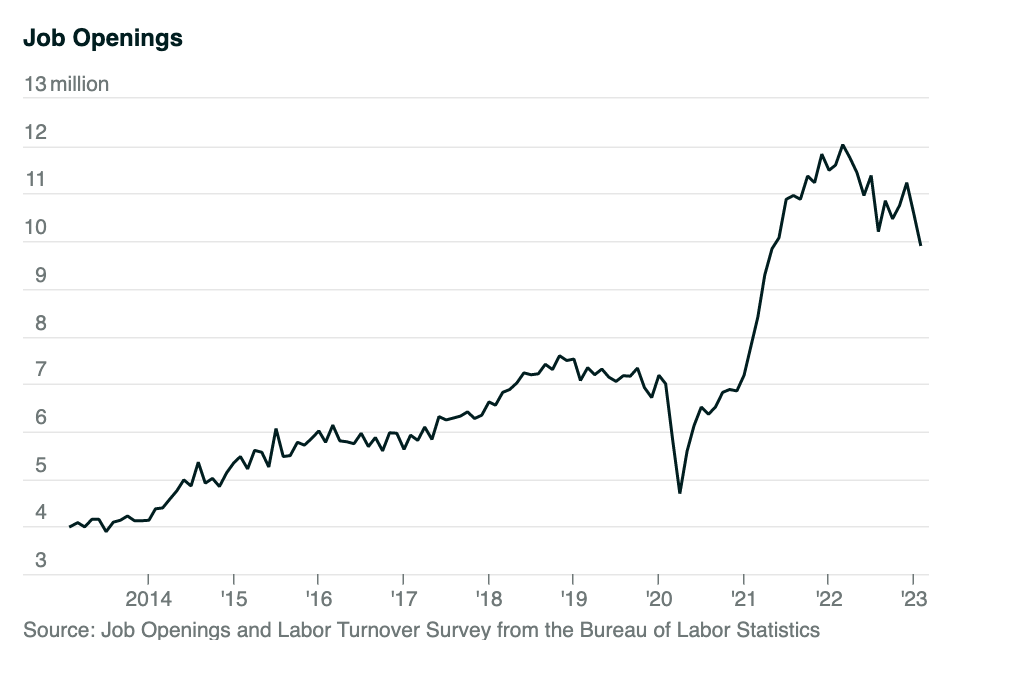

However, people still need a place to live, and they're earning decently high wages. Therefore, asking prices for new or existing homes and apartment rents have not come down yet. They might not be increasing at exceptionally high rates, but they are still increasing. In my opinion, the only thing that breaks that cycle is wages coming down enough that people simply do not have the cash to pay higher rents or these new higher mortgage costs. That only happens in an economy bad enough that job openings are not plentiful. We're not seeing that yet. In fact, the below chart shows that the job market is still quite firm.

{kind=link}

How Did We Get Here?

If you ask me, the Federal Reserve finds itself in a predicament of its own making. Central banks generally fear deflation much more than inflation. The reason for this is they feel they have a lot of tools to combat the latter and few to combat the former. Japan is a lesson in this, and in my opinion, it has terrified every central banker.

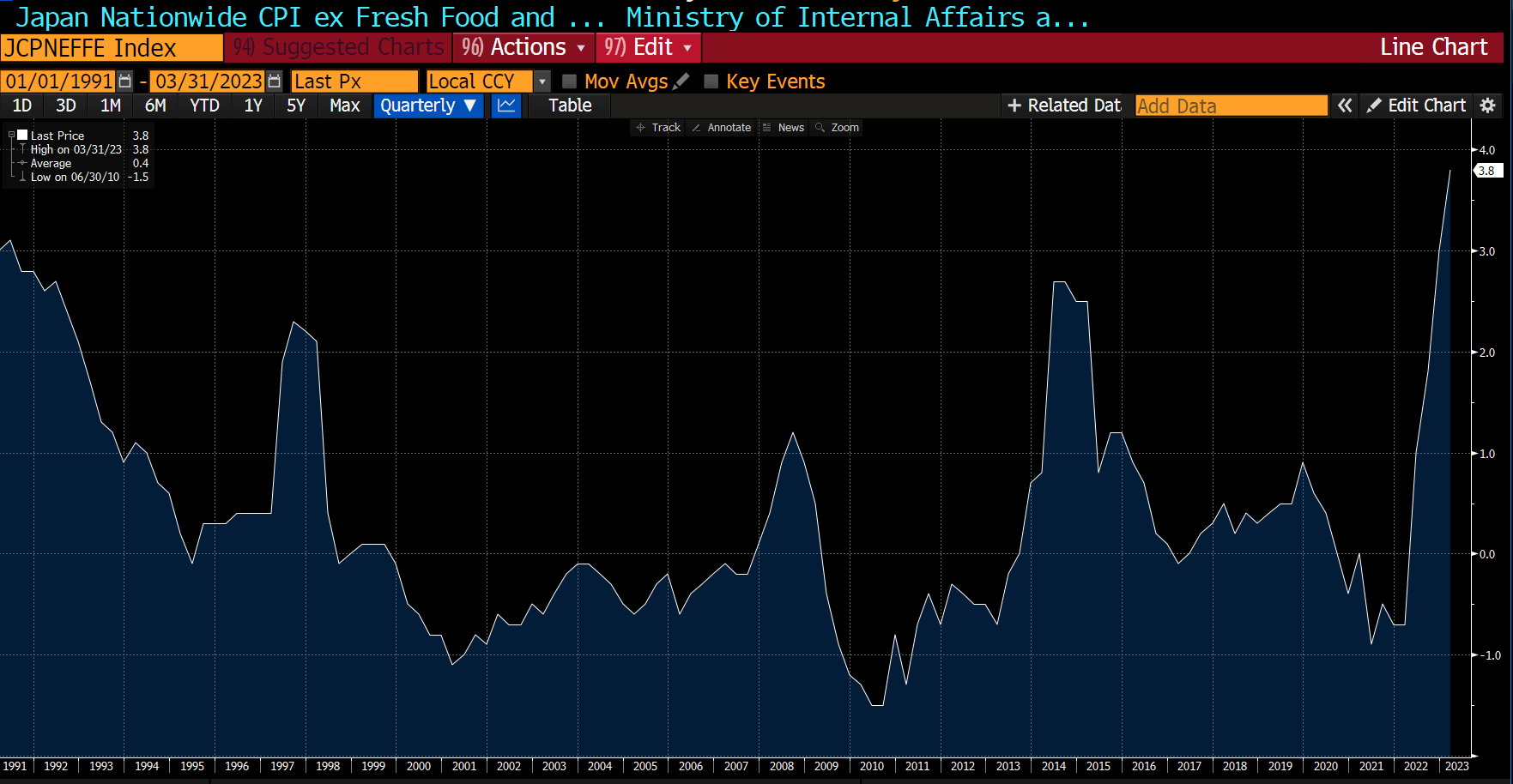

Japan's economy went from decades of torrid growth to a massive, leveraged bust in the late '80s. The result was about 30 years of inflation as measured by CPI ex-food and energy averaging barely above 0%. As you can see below, for most of the period between 2000 and 2013, CPI was negative, signaling deflation.

{kind=link}

The US Federal Reserve's Response

Federal Reserve governors are mostly economists. This situation in Japan, and the weakest recovery ever from recession after the great financial crisis, scared them. So even though low-interest rates failed to spike Japan's economy, our Federal Reserve and other central banks kept interest rates at uber-low levels and maintained quantitative easing (bond buying) to keep a lid on long-term rates for about ten years.

I believe this program was a huge policy mistake. In my opinion, similar to Japan, these low rates did nothing to spur economic activity or PCE/CPI inflation. They simply led to asset inflation (particularly for high-end real estate and collectibles) and highly speculative investment, particularly where leverage is involved.

Even though Powell embarked on a policy change and started raising interest rates in 2018, rates were not particularly high when COVID hit. The Fed responded to the economic shutdown by cutting rates to zero again and resuming its bond purchases. I believe this policy was an error as well, particularly when paired with trillions of emergency economic aid from the government.

That aid put a lot of money in people's pockets at a time when the supply of many goods was severely constricted, if not zero. That was lighter fluid and kindling to spark inflation. More fuel came from the Fed's super low rates, which allowed people to finance even the most overpriced goods (cars at 20%+ above MSRP, new homes, home remodels, etc.). Yet even more inflationary pressure came from higher food and energy prices.

As we saw with the great financial crisis, real estate prices don't reprice so fast just due to very low transaction volume. Once the process gets started, however, they can take a while to bottom. Moribund housing can act as a big damper on economic activity. That said, while economic activity, as measured by various regional surveys, is lousy, and many large tech companies are making headlines by cutting jobs, that chart on job openings above indicates they are way above where they averaged over the past ten years except for COVID. That means wages are not declining so fast.

Moreover, food and energy prices are about supply and demand for the most part. It's very difficult for the Fed to impact the supply of either, and it really can only impact the demand for oil via economic demand affecting gasoline.

Conclusion

We will see what the Federal Reserve says on Wednesday. The market reaction will depend on the follow-up commentary from Powell. I think he's in a tough spot. Inflation is slowing but not fast enough to warrant easing rates. However, the economy is showing signs of slowing...and those signs emerged before the regional banking crisis, which has definitely crimped lending to individuals and small/medium-sized businesses. Powell's goal has been to tame inflation while guiding the economy to a soft or even no landing. His job has gotten harder.

I believe the equity market is expecting signs that the Fed will "pivot" to lower rates sooner rather than later. If it becomes clear they aren't, I think the stocks could be in for a rough patch.

For further details see:

Inflation Update: The Fed Is In A Tight Spot Of Its Own Making