VRAI - Inflation Vs. Recession

- U.S. equity markets finished lower on another choppy week as troubling data showing that inflationary pressures accelerated into June clashed with the expected deflationary forces of stalling global economic growth.

- Despite a significant late-week rally that erased most of the benchmark's declines, the S&P 500 declined 0.9% on the week, posting its 12th decline in the past 15 weeks.

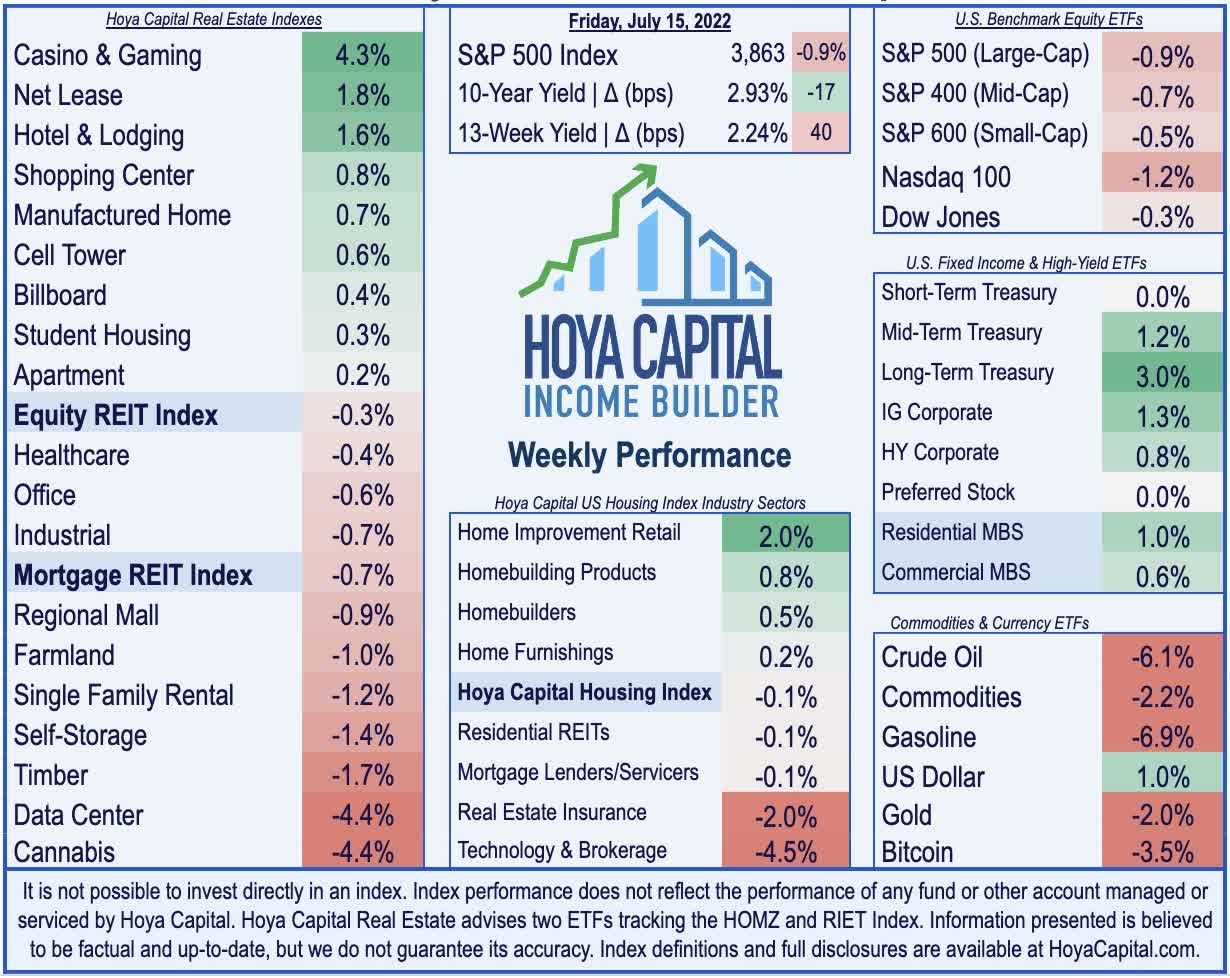

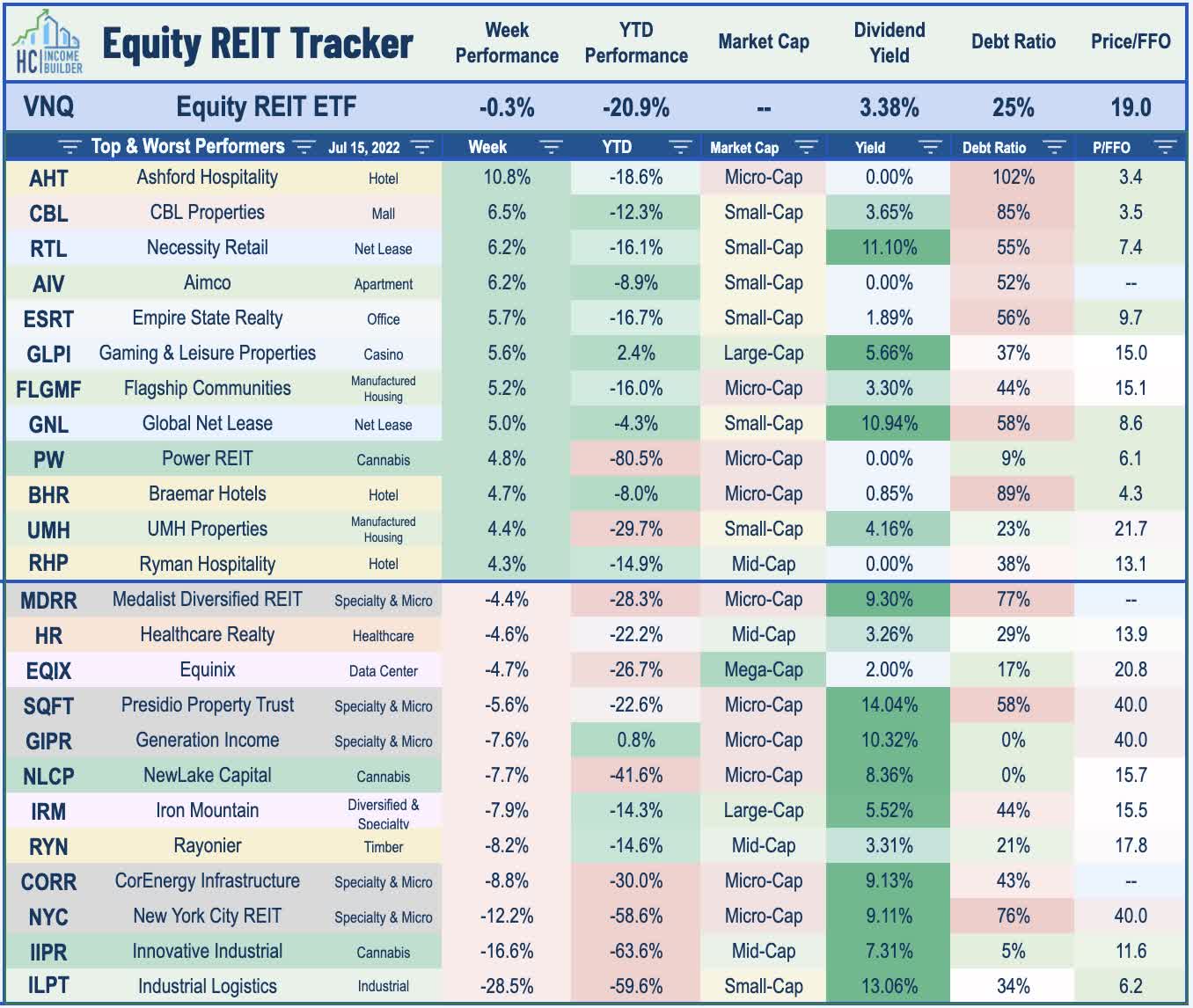

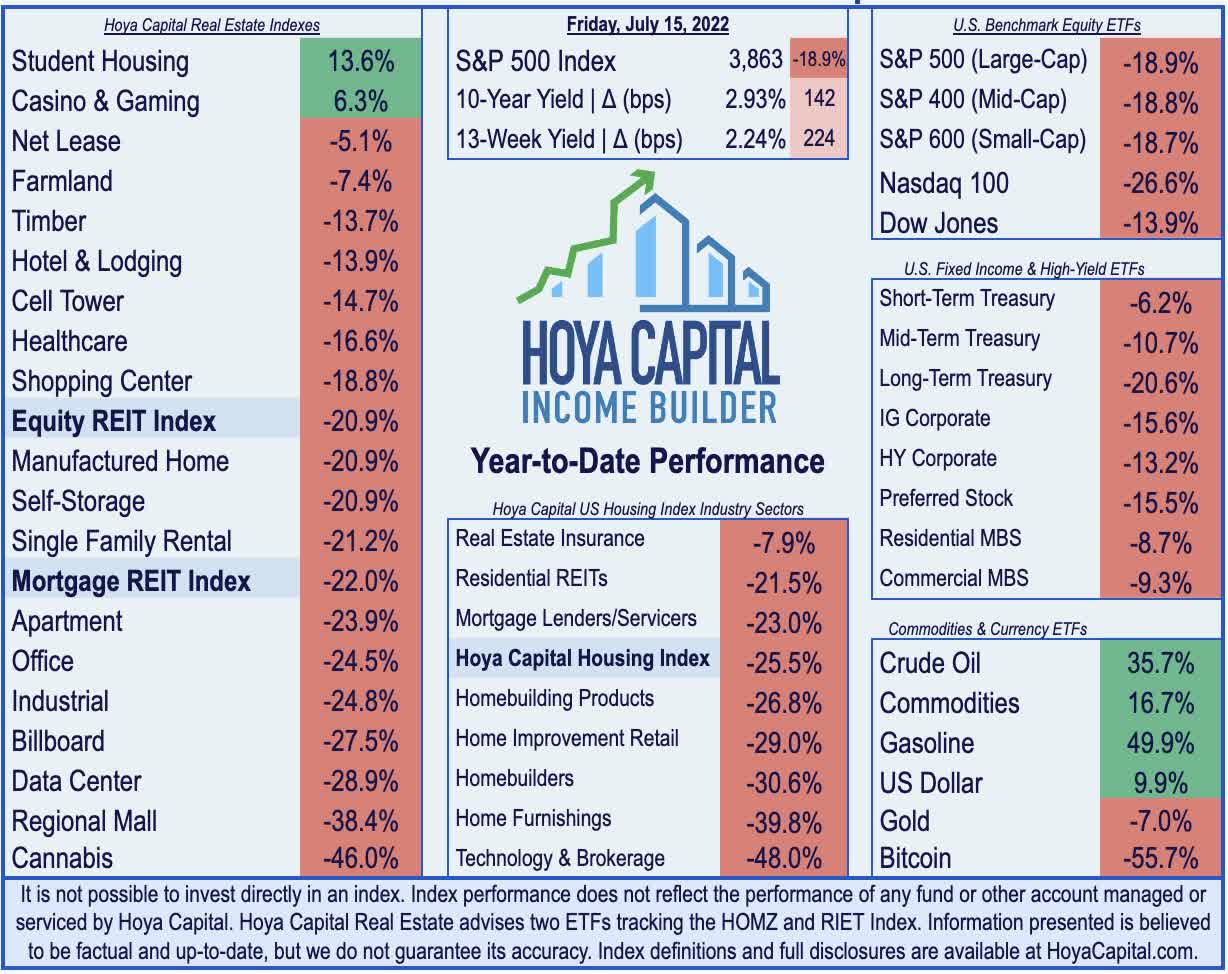

- Real estate equities were among the leaders as long-term benchmark interest rates retreated. The Equity REIT Index finished lower by 0.3% with 9-of-18 property sectors in positive territory.

- Despite the hotter-than-expected inflation data and expectations of an even-more-aggressive path of Fed rate hikes over the next several months, benchmark interest rates on the long-end of the curve continued to retreat.

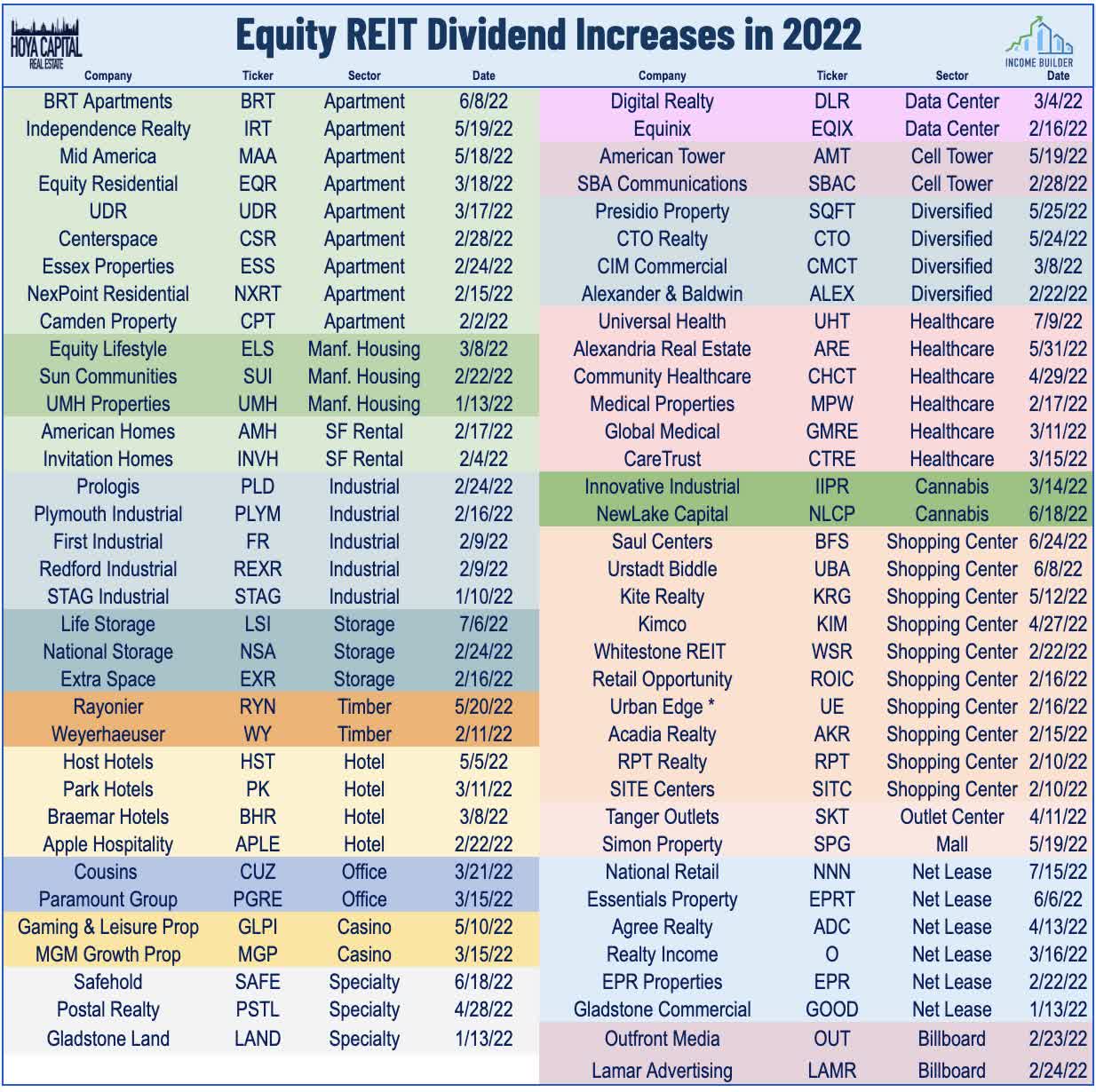

- Ahead of the start of REIT earnings season in the week ahead, a pair of REITs announced dividend hikes, bringing the full-year total across the REIT sector to 83. Net lease REIT National Retail hiked its dividend by 4% while Sachem Capital hiked its dividend by 17%.

This is an abridged version of the full report published on Hoya Capital Income Builder Marketplace on July 15th.

Real Estate Weekly Outlook

U.S. equity markets finished lower on another choppy week as troubling data showing that inflationary pressures accelerated into June clashed with the expected deflationary forces of stalling global economic growth. The slowdown in the U.S. seemingly pales in comparison to emerging issues across Europe and Asia as two major disruptive forces - the Ukraine war and China's "COVID-Zero" policy - have crippled the region's major economic hubs and appear increasingly likely to send both continents into contraction, the silver-lining of which would likely be a meaningful retreat in inflationary pressures stateside.

{kind=link}

Despite a significant late-week rally that erased most of the benchmark's declines, the S&P 500 finished lower by 0.9% on the week - posting its 12th decline in the pasts 15 weeks - and remaining right on the threshold of "bear market" territory with a 20% drawdown. Reflecting expectations of U.S. economic outperformance, the more domestic-focused Mid-Cap 400 and Small-Cap 600 posted more modest declines on the week while the tech-heavy Nasdaq 100 slipped 1.2%. Real estate equities were among the leaders as long-term benchmark interest rates retreated. The Equity REIT Index finished lower by 0.3% with 9-of-18 property sectors in positive territory for the week while the Mortgage REIT Index slipped 0.7%.

{kind=link}

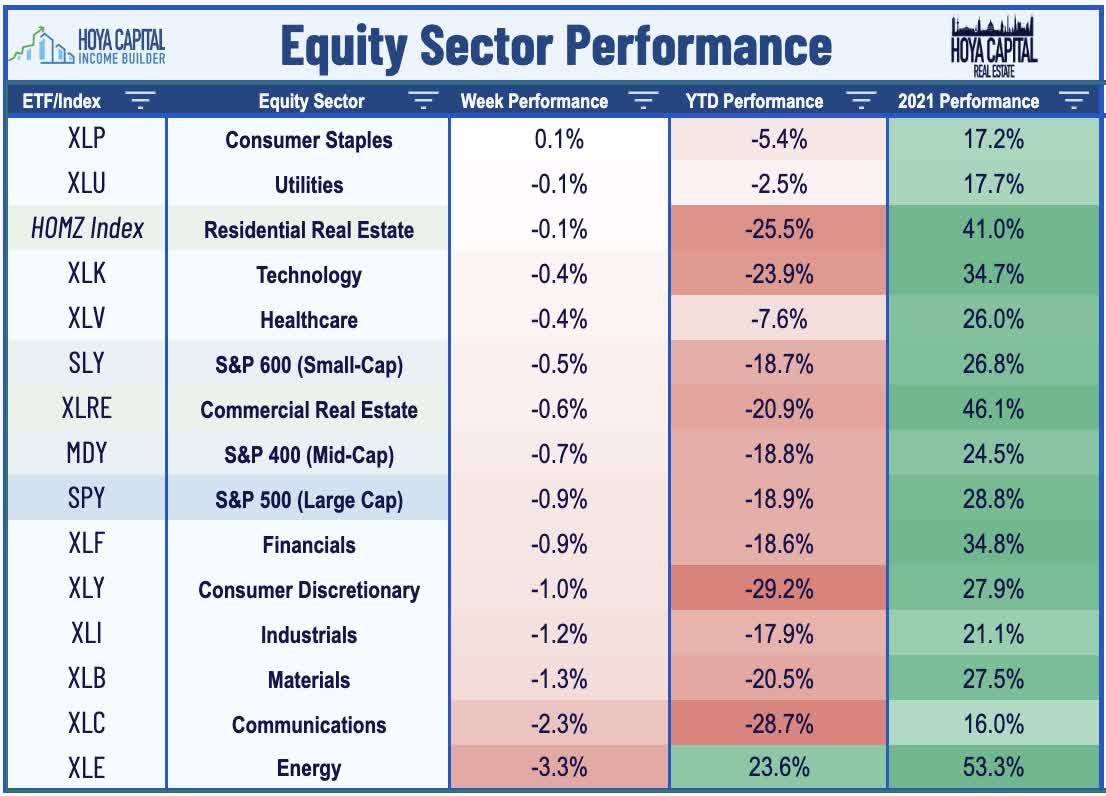

Despite the hotter-than-expected inflation data and expectations of an even-more-aggressive path of Fed rate hikes over the next several months, benchmark interest rates on the long-end of the curve continued to retreat. The 10-Year Treasury Yield dipped 17 basis points on the week to 2.93% - well below its recent high of 3.50% reached in early June - after inflation expectations data this morning showed potential signs of light at the end of the tunnel for inflation. Commodities were under pressure throughout the week amid mounting demand concerns with Crude Oil prices dipping 6% to below $100 per barrel to the lowest close since April while metals and agriculture commodities also posted sharp declines. All eleven GICS equity sectors finished lower on the week as earnings season kicked into gear with mixed reports from several major U.S. banks. Homebuilders and the broader Hoya Capital Housing Index , meanwhile, were a bright spot again this week ahead of a busy week of housing market data.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

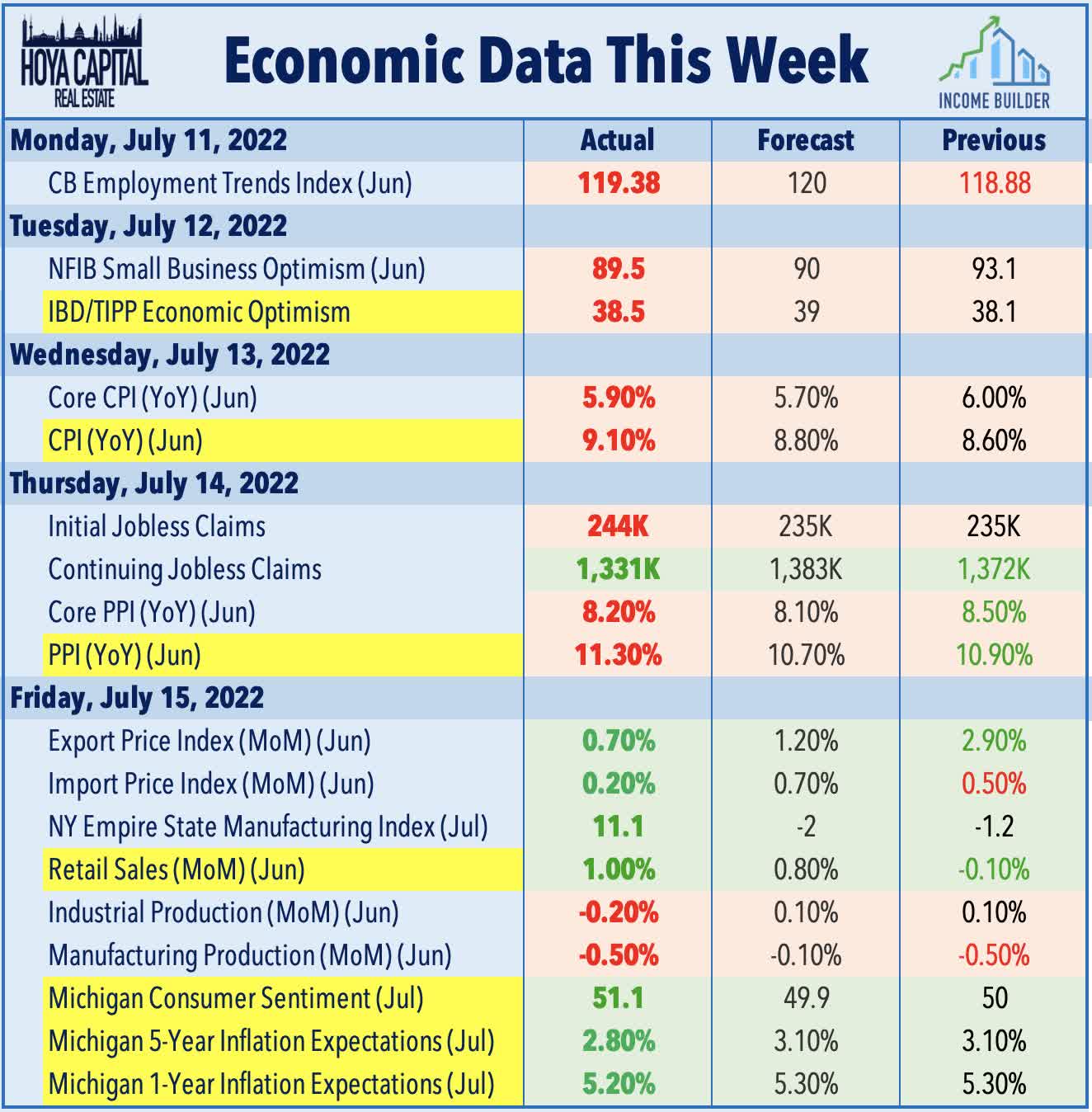

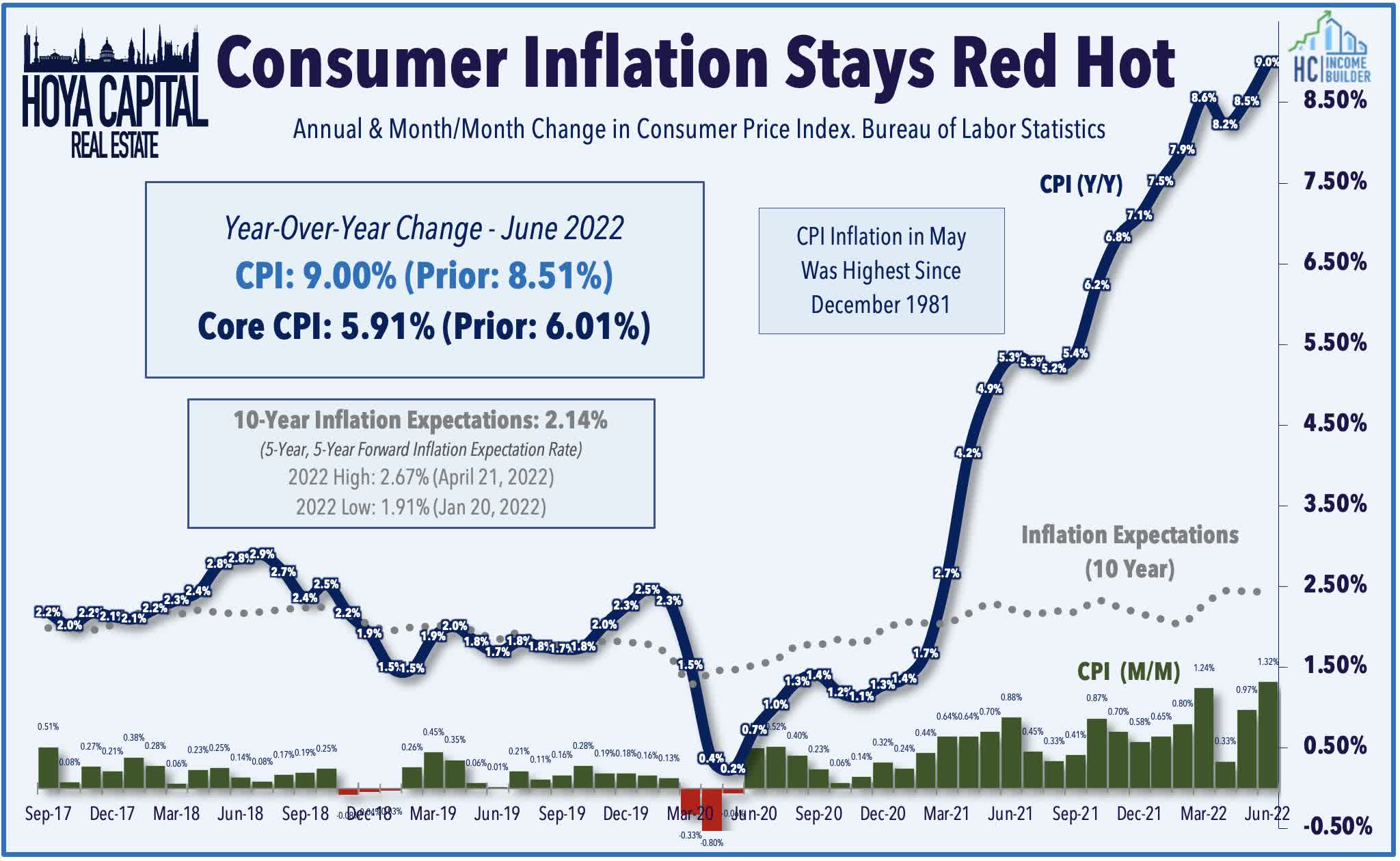

Peak Inflation? Not Yet. Consumer prices rose at the fastest pace in more than 40 years in June - and significantly above analysts' estimates - as cost pressures continue to be far less "transitory" than economics and public officials projected. The annual increase in the headline Consumer Price Index accelerated to 9.1% in June before seasonal adjustments - well above the 8.8% rate expected - which was the highest since January 1981. The Core CPI - the metric on which the Fed focuses its attention - rose 5.9% - above expectations for a 5.7% gain. Remarkably, the energy index rose 41.6% over the last year, the largest increase since April 1980 while the food index increased 10.4%, the largest increase since February 1981. Producer Price Index data showed similar trends of persistent price pressures with wholesale prices rising 11.3% from a year ago in June - above the 10.7% rate expected.

{kind=link}

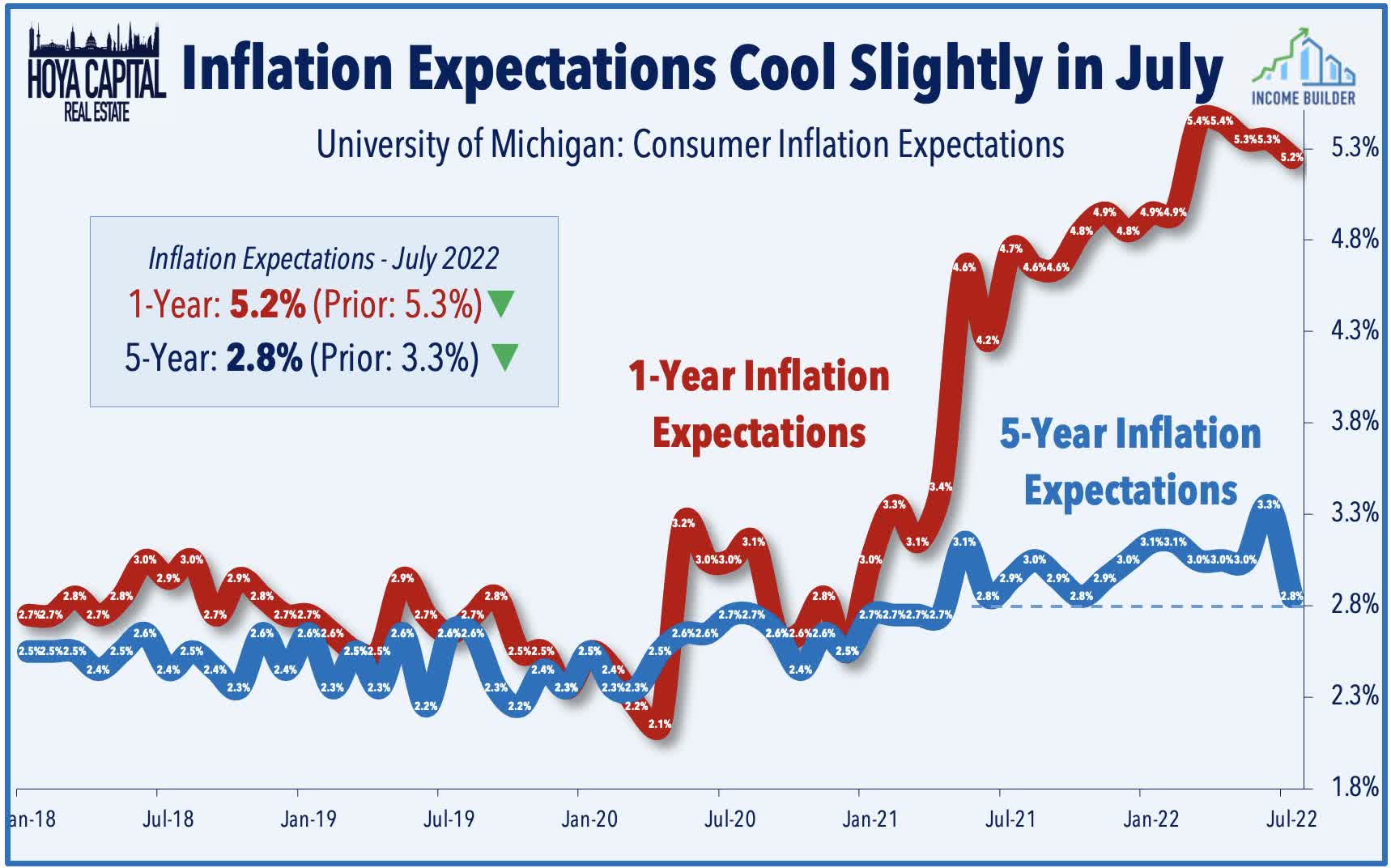

Following this pair of red-hot inflation reports, however, investors and the Fed got some reprieve late in the week as a closely-watched survey of consumer inflation expectations showed a notable moderation. The University of Michigan sentiment survey showed households’ expectations of where inflation will be in five years dropped more than expected to 2.8% from the previous reading of 3.1%. Exactly what the Fed wanted to see given the noted concerns over a potential "wage-price spiral" in which expectation of inflation lead to further inflation, the mounting recession concerns - and fears of job losses - appear to be dampening inflation expectations. The balance of the report shows that consumers are indeed as worried as ever, by some measures. The headline consumer sentiment index for July was 51.1 - barely above the all-time lows in the prior month. The consumer expectations index declined -by 40.1% year-over-year to 47.3, which is the lowest since the 1980s.

{kind=link}

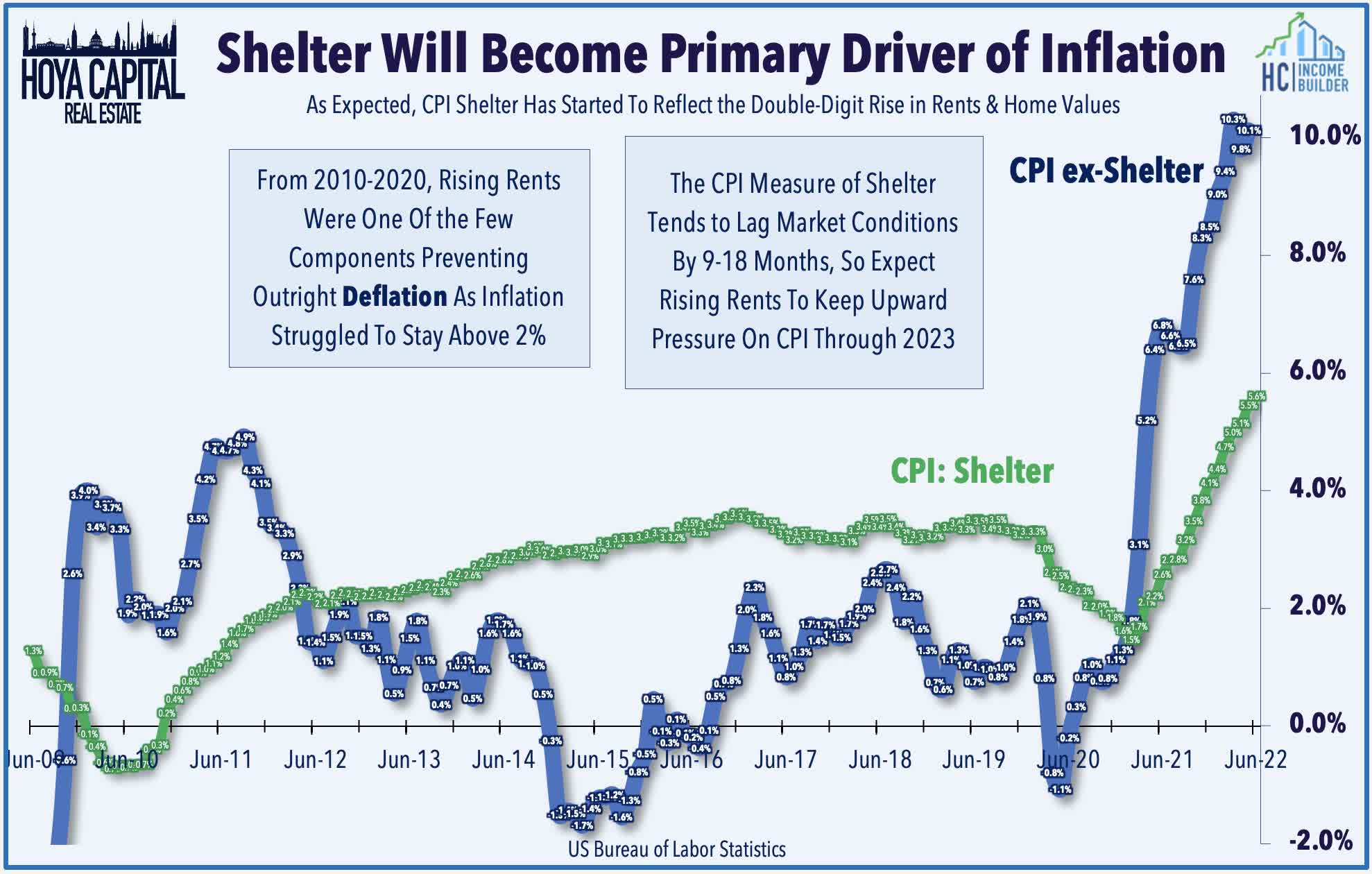

As we've discussed for the last year, we continue to project persistent pressure on the headline inflation metrics due to the delayed recognition of soaring shelter costs - the single largest weight in the CPI Index - which are just beginning to filter into the data. The cost of shelter increased 0.6% in June - matching the largest monthly increase since March 2004 - pushing its year-over-year rise to 5.6% - the largest 12-month increase since the period ending February 1991. While broader price pressure now appears to be cooling given the sharp declines in commodities prices over the past two months, it will likely take several quarters for the cooldown to be meaningfully reflected in the data. The Dallas Fed published a report highlighting the data issues at the BLS, finding a 16-month lag between the BLS inflation series and real-time market pricing of home prices and rents which will add an estimated 0.6-1.2% to the Core CPI index in 2022 and 2023.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Net Lease : Ahead of the start of REIT earnings season in the week ahead, a pair of REITs announced dividend hikes, bringing the full-year total across the REIT sector to 83. Net lease REIT National Retail ( NNN ) rallied more than 3% after hiking its quarterly dividend by 4%. Notably, the hike marks the 33rd consecutive annual dividend increase for NNN - one of three REITs to have boosted its payout in at least 30 straight years. Elsewhere, as noted in the mortgage REIT section below, Sachem Capital ( SACH ) rallied nearly 8% after it hiked its dividend by 17%. In our State of the REIT Nation report, we noted that FFO growth has significantly outpaced dividend growth over the past several quarters, driving the dividend payout ratios to just 68.8%, so REITs are well-equipped to deliver another year of robust dividend growth that may meet or exceed the record year in 2021.

{kind=link}

Industrial : We did see the first equity REIT dividend cut of the year during the week, however, as Industrial Logistics Properties ( ILPT ) dipped more than 25% after it slashed its dividend to $0.01, citing difficulties related to its recent acquisition of Monmouth. ILPT cited rising rates and difficult market conditions for delays to its post-acquisition financing plans. ILPT noted that its "taking longer than originally expected to complete ILPT’s long-term financing plan for the Monmouth acquisition, which includes the sale of additional equity interests in its consolidated joint venture, property sales and other refinancing activities" due to the "increases in interest rates and deterioration in real estate market conditions." Industrial REITs have been slammed this year in a sell-off sparked by Amazon's ( AMZN ) plans to scale back its logistics leasing activity. ILPT announced that it to "enhance its liquidity until it completes its long term financing plan for the Monmouth acquisition and/or its leverage profile otherwise improves." ILPT noted that it anticipates that its dividend will return to a rate at, or close to, its historical level sometime in 2023.

{kind=link}

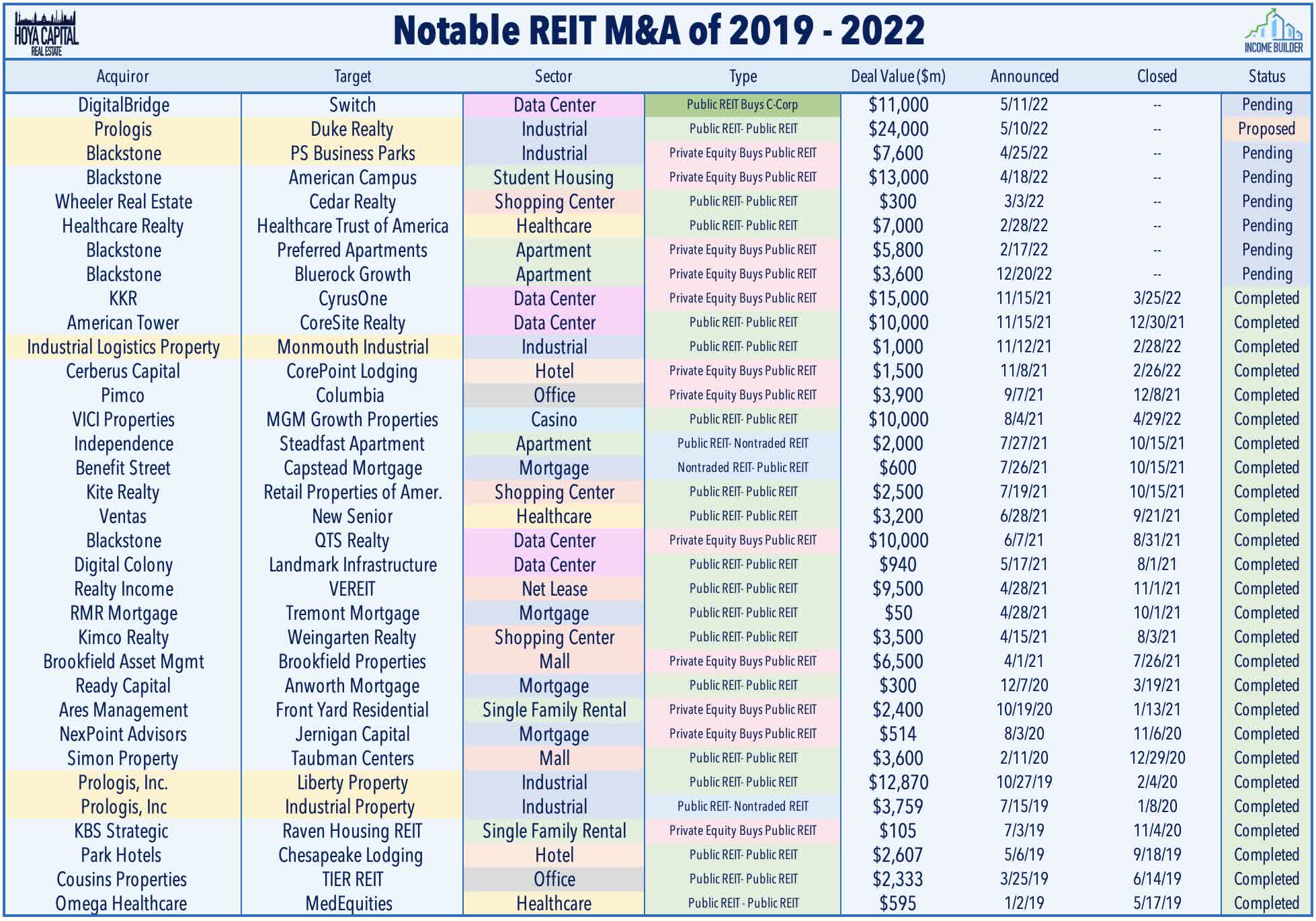

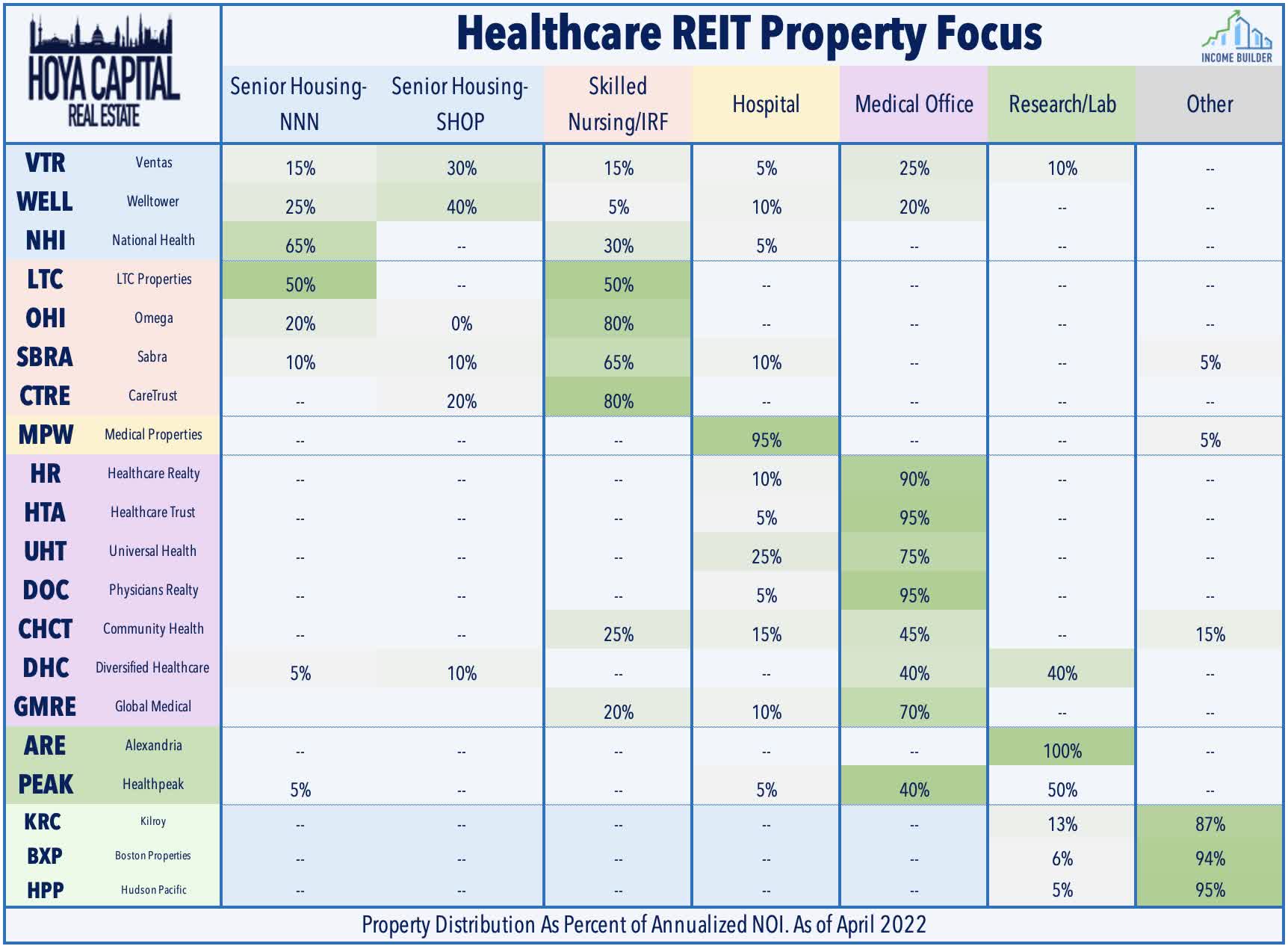

Healthcare : M&A was another theme this week in the REIT sector this week with the completion of several major pending deals and the announcement of a handful of smaller-scale transactions. Shareholders of Healthcare Trust of America ( HTA ) and Healthcare Realty ( HR ) approved a combination at a vote on Friday. Approximately 79% of HR's shareholders voted in favor of the merger transaction with HTA. The deal - which will form the largest medical office REIT - is expected to close on or around Wednesday, and comes after several months of drama - including challenges from activist investors and a competing offer from Welltower ( WELL ). Medical office demand has remained relatively steady throughout the pandemic, while lab space demand from biotechnology and pharmaceutical companies has been extremely strong.

{kind=link}

Cell Tower : American Tower ( AMT ) was among the leaders on the week with 1% gains after it announced that it sold a 29% state in its data center business for $2.5B to Stonepeak, an alternative investment firm. AMT's data center business is primarily comprised of its interests in CoreSite , which it acquired last year for $10B and consists of 27 data centers in 10 U.S. markets. Under the terms of the deal - which is expected to close in the third quarter - American Tower will retain managerial and operational control, as well as day-to-day oversight of its U.S. data center business. Strategically-located network-dense data centers have been a recent focus for cell tower REITs amid a push to build out "Edge" network capabilities - the concept that many cell tower sites will soon be hosting “mini data centers” on the "edge" of communications networks in order to reduce latency for ultra-time-sensitive applications like self-driving vehicles.

{kind=link}

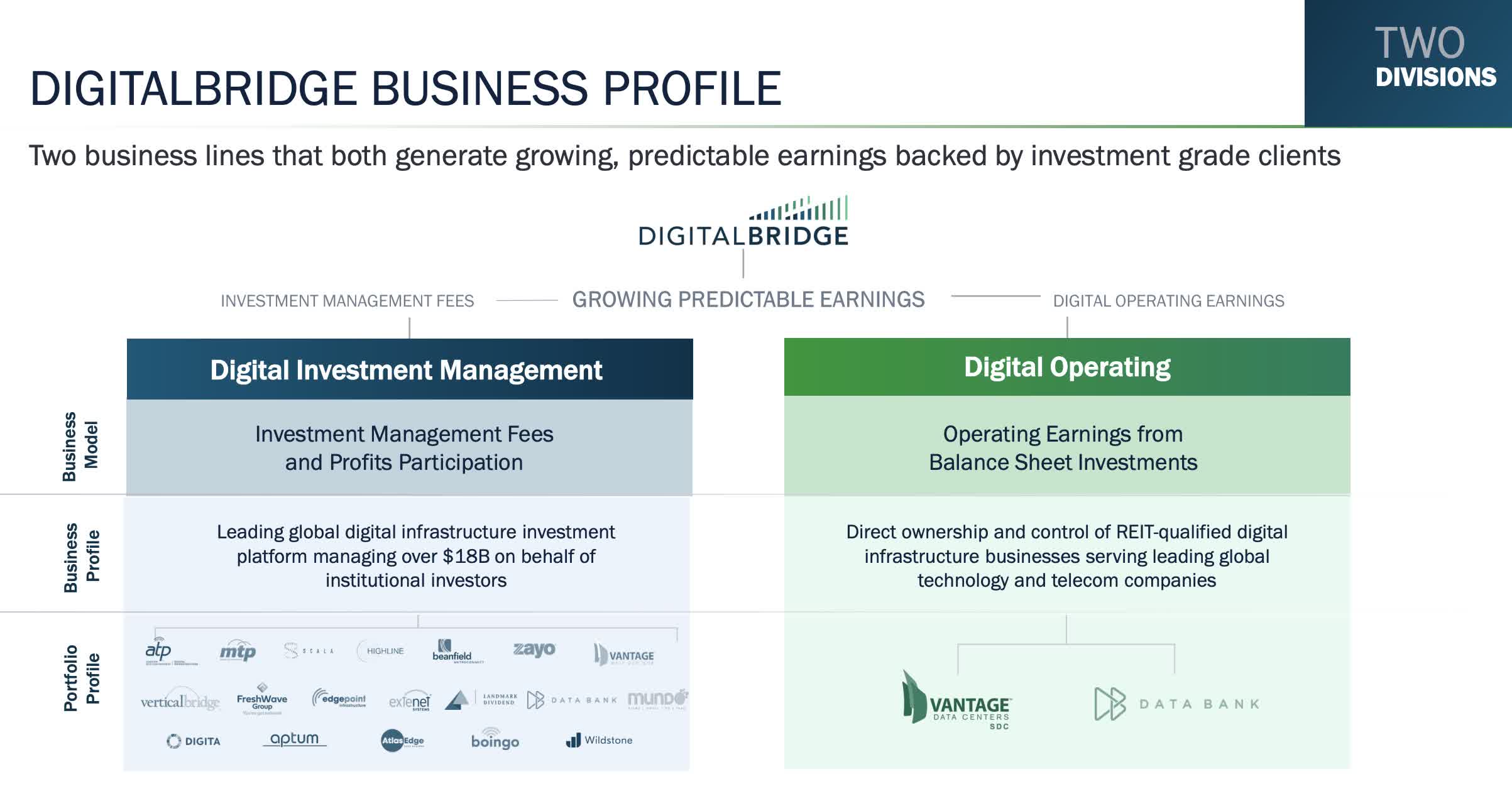

Cell Tower : Elsewhere, DigitalBridge ( DBRG ) finished flat on the week after it announced that it partnered with Brookfield Infrastructure ( BIP ) to acquire a 51% ownership stake in Germany-based GD Towers. GD Towers - the mobile telecommunications tower business of Deutsche Telekom - is Germany’s largest tower company, owning 40k towers and communications sites in Germany and Austria. Details of the ownership breakdown between Brookfield and Digital Bridge were not yet disclosed, and it's not yet clear whether any of the assets will be included in DBRG's Digital Operating business or if all will be retained under its Digital Investment Management business. The deal is expected to close in late 2022. Deutsche Telekom plans to use the proceeds to lower debt levels and fund plans to gain majority control of T-Mobile US.

{kind=link}

Shopping Center : Necessity Retail ( RTL ) - formerly known as American Finance Trust - gained more than 6% on the week after it completed the final acquisition from the previously announced agreement to acquire a portfolio of 81 shopping centers from CIM Real Estate for $1.3 billion. The Company also announced that year-to-date it has acquired 93 properties for a total of $1.4 billion. The acquired properties total 10.2 million square feet and were acquired at a cash cap rate of 7.2%. With the completed acquisitions, multi-tenant shopping center properties now comprise the majority of its portfolio as it shifts away from its previous focus on single-tenant net lease properties. As we discussed in Winning The Last Mile , shopping center fundamentals are now as strong – if not stronger than before the pandemic. Occupancy rates climbed to the highest level since early 2015 while rental rates continue to accelerate.

{kind=link}

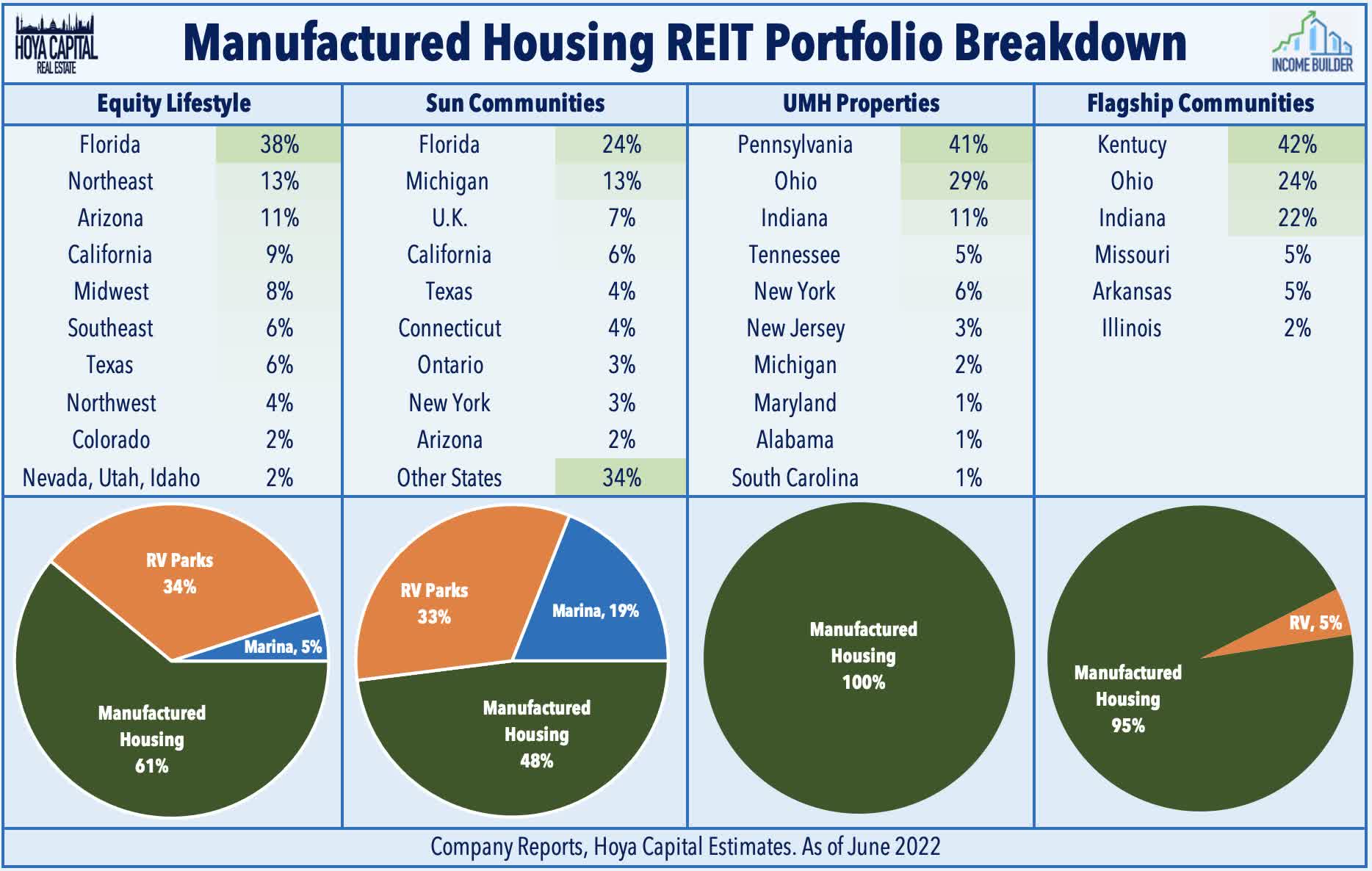

Manufactured Housing : UMH Properties ( UMH ) - which we recently added to the REIT Focused Income Portfolio - rallied more than 4% on the week after closing on an acquisition of a manufactured home community located in Erie, Michigan. The 88-acre community contains 351 developed homesites of which approximately 63% are occupied. UMH also noted that its 2022 acquisitions have totaled $39M across four communities containing 718 sites with a blended occupancy rate of 56% Manufactured Housing REITs - one of the most "recession-resistant" property sectors given their countercyclical demand profile - have rebounded over the past month following uncharacteristic underperformance in early 2022. In our recent report, we noted that MH rents are more closely linked with the CPI Index than any other residential sector and we expect rent growth to surprise to the upside this year.

{kind=link}

Industrial : STAG Industrial ( STAG ) finished modestly lower on the week after announcing that it completed the sale of two fully occupied industrial real estate properties for gross proceeds of approximately $82 million, representing a cash capitalization rate of 5.2%. The buildings consist of approximately 1 million sf and are located in Dayton, OH and Greenwood, IN which STAG acquired the buildings in 2017 and 2018, respectively, for a purchase price of approximately $63.3 million representing a cash capitalization rate of 6.2%. Elsewhere, PS Business Parks ( PSB ) announced that it expects to complete its previously announced transaction with affiliates of Blackstone ( BX ) next week following the successful shareholder vote to approve the acquisition on Friday. PSB is the lone industrial REIT in positive territory this year.

{kind=link}

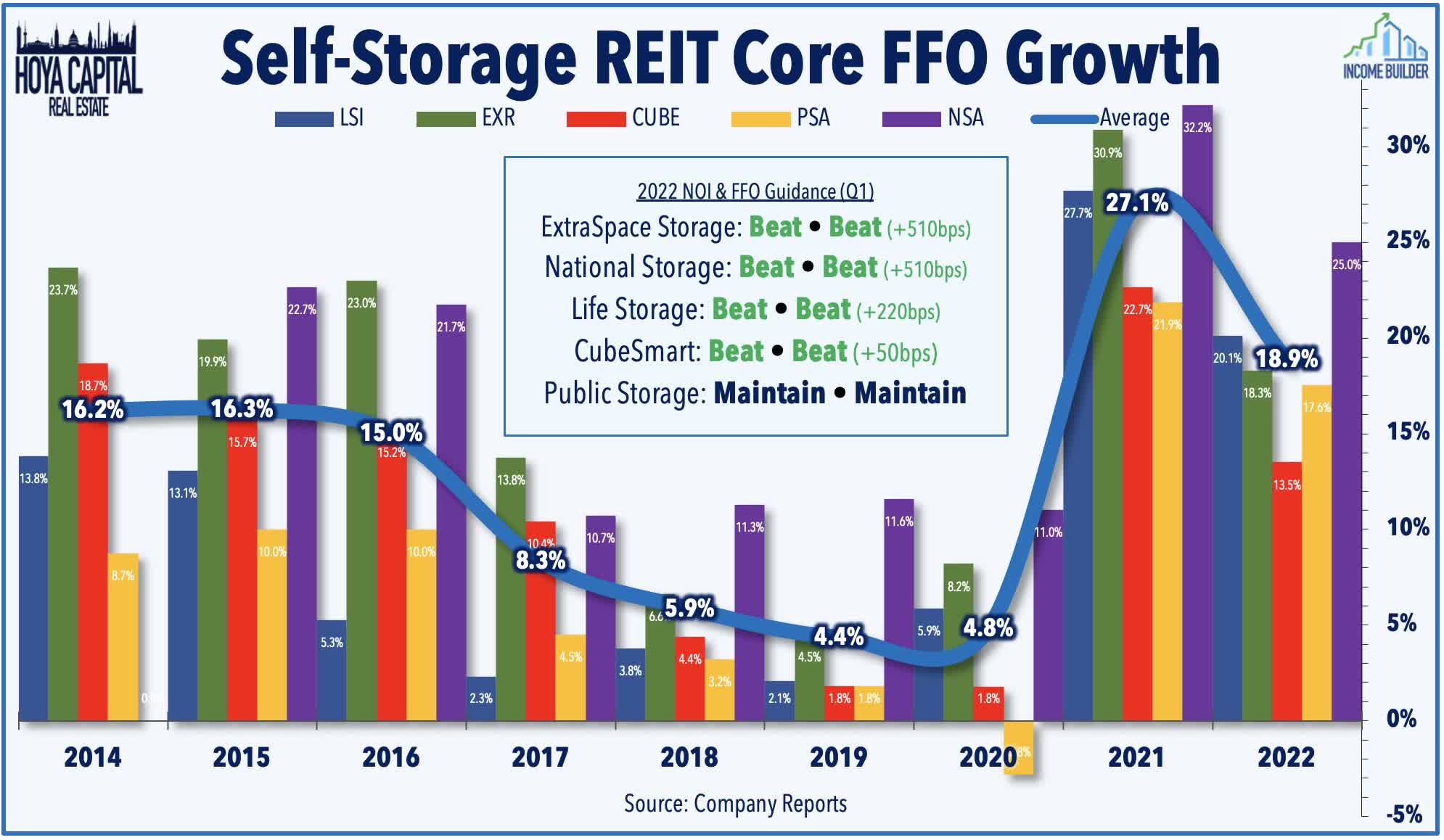

Storage: On that topic, this week we published Storage REITs: Recession Resistant, But Not Acting Like It. Self-Storage REITs - usually known for their recession-resistant characteristics - have sold off in recent months despite a stellar slate of earnings results and upbeat interim updates. Storage REITs appear to be caught up in the bearish sentiment surrounding industrial REITs – a rather distant “cousin” to the storage sector – and the unusually-high recent correlations are fundamentally unwarranted. Few REIT sectors have defied expectations as comprehensively as storage REITs since the start of the pandemic, and while several pandemic-fueled tailwinds are waning, the long-term outlook remains quite compelling. Among the relevant PPI metrics for the real estate industry, the PPI Self-Storage Index - which closely tracks rent growth in the storage REIT sector - posted brisk quarter-over-quarter growth of 4.8% in Q2 - an acceleration from Q1 to a nearly 20% annualized rate.

{kind=link}

Mortgage REIT Week in Review

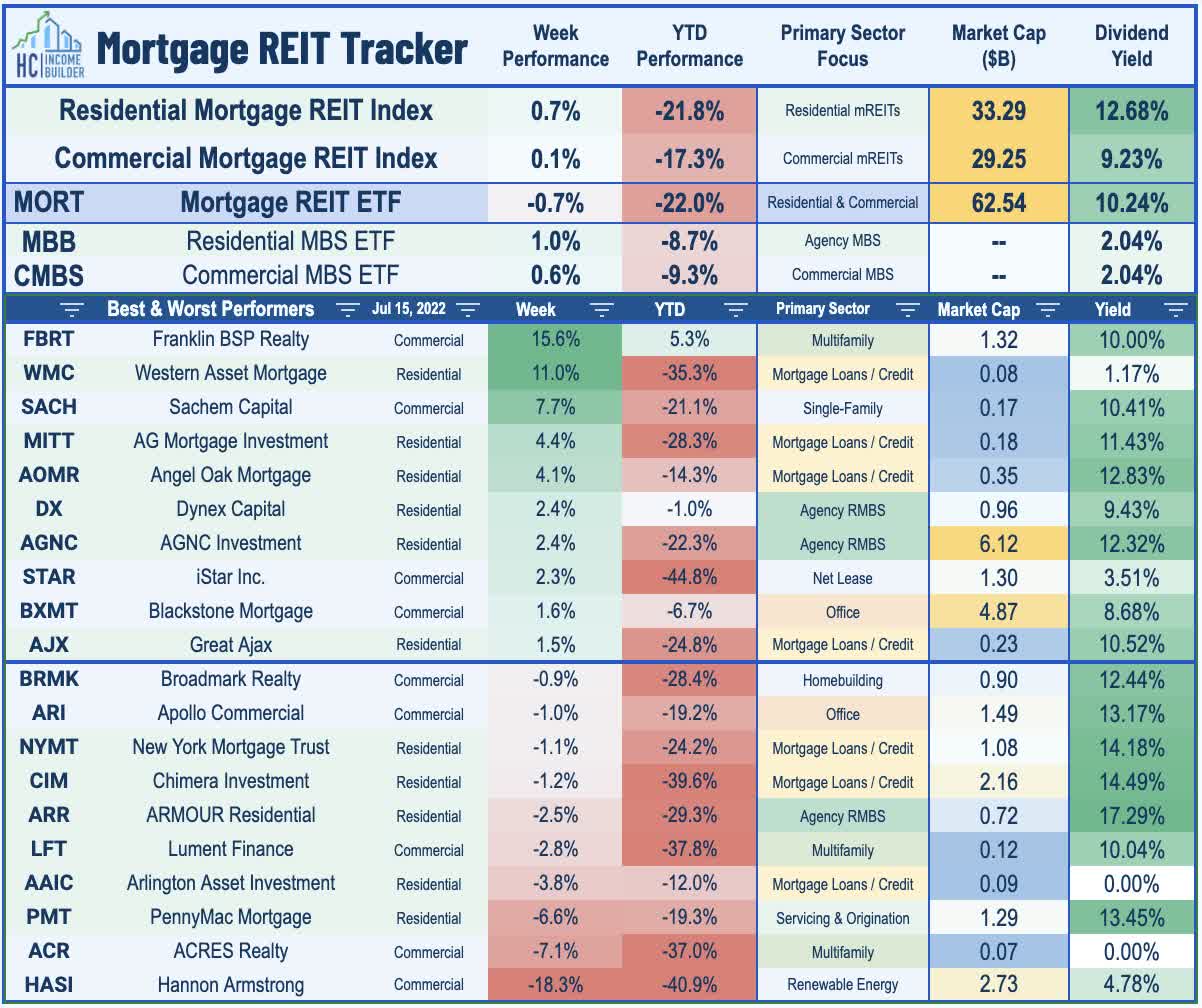

Mortgage REITs finished higher on the week with residential mREITs posting gains of 0.7% while commercial mREITs gained 0.1%. Mortgage-backed bonds continue to be notable outperformers in the fixed income market as the iShares MBS ETF ( MBB ) advanced another 1% on the week to push its gains over the past month to nearly 4%. Sachem Capital ( SACH ) rallied nearly 8% on the week after it hiked its dividend by 17%, becoming the 12th mortgage REIT to raise its dividend this year while four mREITs have lowered their dividends. Elsewhere, AGNC Investment ( AGNC ) advanced more than 2% on the week after it held its monthly dividend steady with a forward dividend yield of 12.6%. Orchid Island Capital ( ORC ) and Seven Hills Realty Trust ( SEVN ) were also among the leaders on the week after each held their dividends steady. Western Asset Mortgage ( WMC ) was also among the leaders on the week after its 1-for-10 reverse stock split became effective.

{kind=link}

Mortgage REIT Hannon Armstrong ( HASI ) plunged nearly 20% on the week after short-selling firm Muddy Waters released a new short report titled: HASI: “ESG” is for Exaggerating, Scamming, and Grifting. Muddy Waters - which has been reportedly been under scrutiny by regulators for illegal trading activity - alleges that HASI is engaged in misleading accounting practices related to the valuation of their renewable energy portfolio. HASI makes loans to renewable energy companies and other "green" energy projects that are typically secured by real estate rights. Analysts at B. Riley, Cowen and Oppenheimer defended the firm and its management team and recommended buying the shares on the weakness. HASI has been one of the strongest-performing mortgage REITs over most long-term measurement periods with average annualized total returns that are nearly triple that of the All REIT Index in the past five years.

{kind=link}

REIT Capital Raising & REIT Preferreds

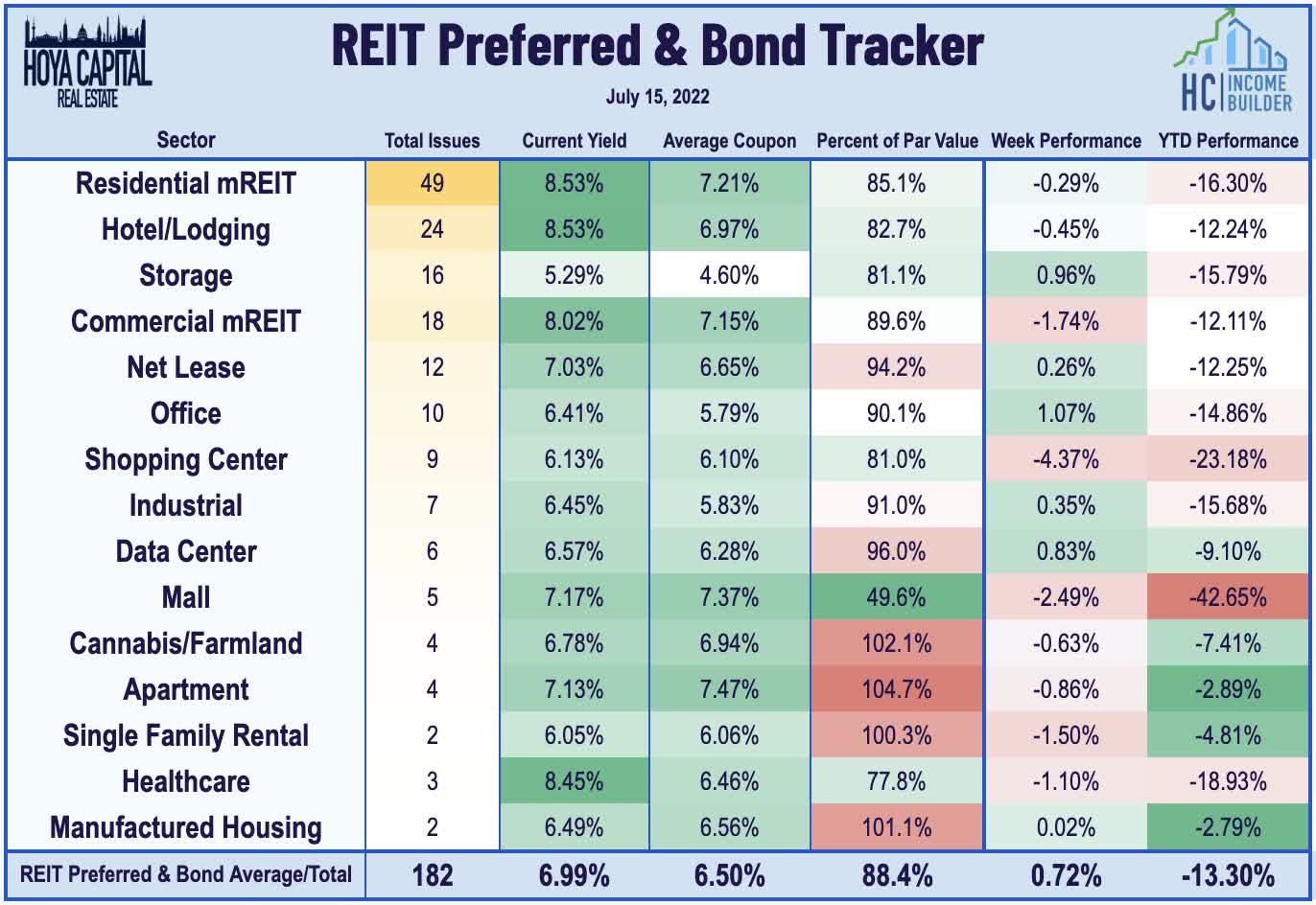

The Hoya Capital REIT Preferred Index finished higher by 0.73% this week to trim the year-to-date declines to roughly 10% on a total return basis. The preferred series of Cedar Realty ( CDR ) continued to slide this week - extending their declines to more than 75% over the past year - after CDR completed the final steps in the process to be acquired by Wheeler Real Estate ( WHLR ) in a controversial $300M deal expected to close within the month. Upon acquisition, WHLR is expected to suspend the preferred distributions on CDR's preferreds. The preferred series of Pennsylvania REIT ( PEI ) also remain in focus amid an ongoing governance battle with activist firm Cygnus Capital, which has been seeking to gain board seats through their preferred share position.

{kind=link}

2022 Performance Check-Up

Two weeks into the back half of 2022, Equity REITs are now lower by 20.9% on a price return basis for the year while Mortgage REITs have slipped 22.0%. This compares with the 18.9% decline on the S&P 500 and the 18.8% decline on the S&P Mid-Cap 400 as well. With the exception of the student housing and casino REIT sectors, every property sector is in negative territory for the year while ten property sectors are lower by over 20%. At 2.93%, the 10-Year Treasury Yield has climbed 142 basis points since the start of the year, but has been under pressure after briefly breaking through the prior post-GFC-high rate of 3.25% reached in 2018 and touching a high in June of 3.50%.

{kind=link}

Economic Calendar In The Week Ahead

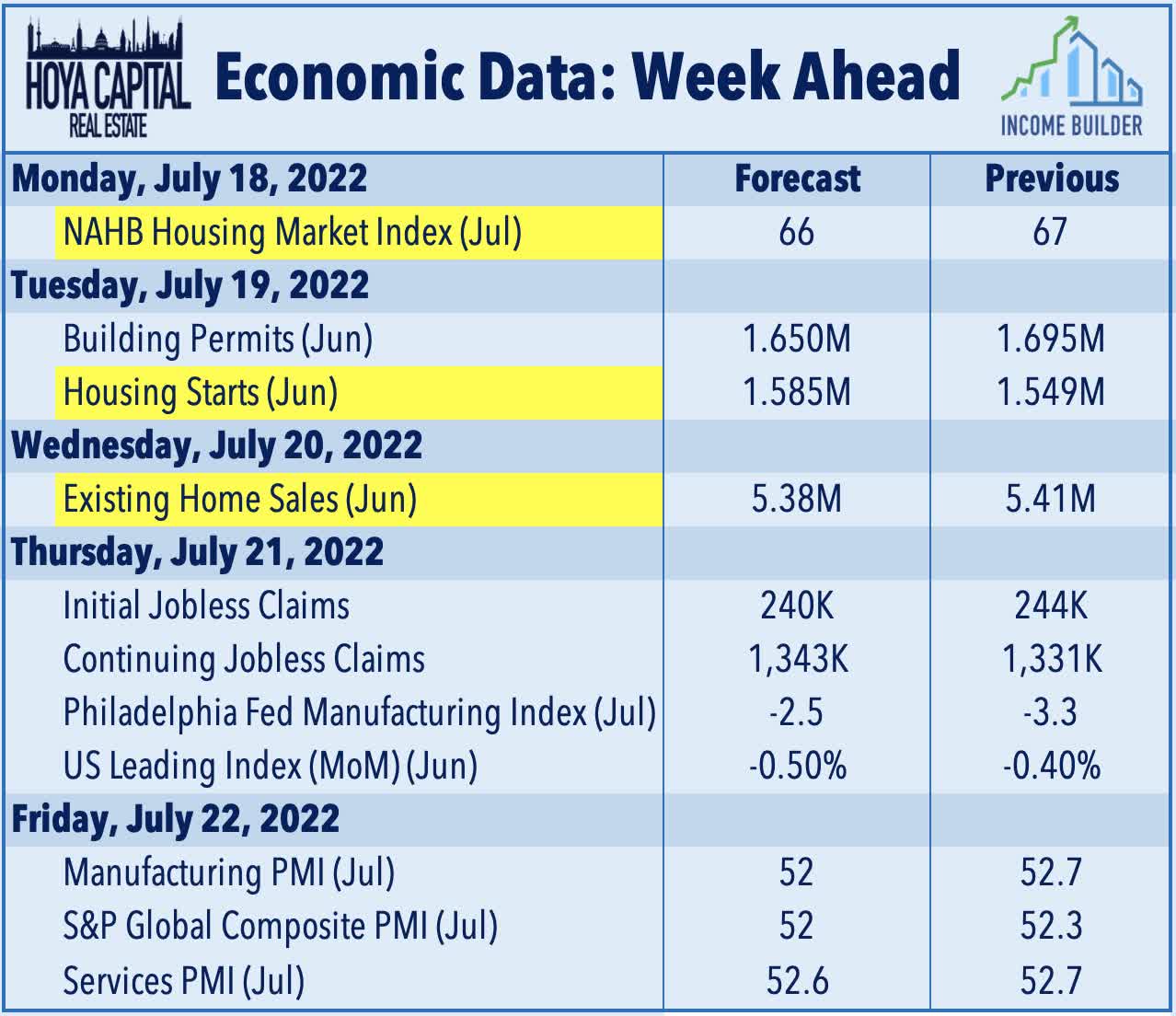

The state of the housing market will be in focus next week with a trio of reports expected to show a continued cool down in activity over the past month, reflecting the surge in mortgage rates which climbed to nearly 6% in late June before moderating in recent weeks. On Monday, we'll see Homebuilder Sentiment data which is expected to show the lowest print in four years at 66. On Tuesday, we'll see Housing Starts and Building Permits data which is expected to show a continued moderation in the pace of new home construction, particularly within the single-family segment. On Wednesday, we'll see Existing Home Sales data which is expected to slow to the lowest rate since June 2020. There are some early signs that the recent dip in mortgage rates, moderating home prices, and slightly higher inventory levels shave pulled some potential buyers back into the fold in recent weeks, however, as the Redfin Homebuyer Demand Index has rebounded about 5% from its late-June lows.

{kind=link}

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Inflation Vs. Recession