APYX - InMode: Prolonged Valuation Slump Is A Buying Opportunity

2023-08-24 10:30:54 ET

Summary

- INMD's P/E and EV/EBITDA ratios have fallen sharply in the past 2-3 years despite its revenues and net income more than doubling in this period.

- The prospect of continued profitable growth and a history of beating analysts' estimates suggest that this undervaluation will not persist for long.

- INMD has insanely high gross margins and net income margins due to unique cost advantages that competitors like Cutera and Apyx lack.

- Its strong cash position and debt-free balance sheet further strengthen the bull case.

- In the most recent quarter, it reported record growth in consumables, suggesting physicians are using its devices more frequently.

When I last covered InMode Ltd (INMD) in December 2022, I argued in my article that the Israel-based medical devices company was a top stock pick for 2023 owing to my view that its valuation understated the performance and prospects of the underlying business. 8 months into the year, the stock is up just 10%, which lags broader market indices such as the S&P 500 (up 16% YTD) and the Nasdaq (up 32% YTD).

INMD's underperformance relative to the broader market has led me to revisit my thesis in light of the company's financial performance in Q1 and Q2 and its current valuation. What's interesting is that, since my last coverage, INMD's P/E has remained largely unchanged at 17x. The underlying business has, however, continued performing as I expected. Revenues grew to $242.15 million for the first six months of 2023 vs $199.46 million in the first half of 2022. Net income over this period has increased to $96.23 million from $75.02 million a year earlier. The management further raised the guidance for the full year.

A stagnant valuation amid improving financial performance is in my view a reason to reiterate my bullish call from December. In this follow-up piece, I not only look at the main arguments supporting INMD's bull case -- such as its strong financial performance, growing cash reserves, and debt free balance sheet -- but also look at how its unique cost advantages give it a clear competitive edge over peers. I also look at some insights from the recent Q2 earnings call that suggest that its devices are being used more frequently by existing customers, indicating that the brand is gaining ground. These factors in my view warrant continued bullishness on the stock, despite the soft start to the year.

Strong demand for its devices

INMD manufactures radio-frequency powered surgical devices used by aesthetic surgeons in minimally invasive aesthetic treatments like fat reduction, skin tightening and body contouring. With a commercial presence in 92 countries, including the US, it offers a comprehensive line of products across several categories for plastic surgery, gynecology, dermatology, otolaryngology and ophthalmology.

Because non-invasive and minimally invasive cosmetic procedures are associated with less pain, shorter hospital visits and fewer complications, they are rapidly growing in popularity among patients seeking cosmetic treatment options that don't involve surgery and the risks associated with going under the knife. The number of body contouring procedures done using energy-based devices in the US reached 400,180 in 2022, up 31% from 306,174 in 2021, according to the Aesthetic Society . This underlines the strong demand for minimally invasive procedures by patients.

The rising demand for minimally invasive aesthetic treatments has resulted in aesthetic surgeons stocking up on the devices that make these procedures possible. This has in turn helped to fuel the commercial success for the likes of INMD who specialize in manufacturing these devices. INMD's revenue more than doubled from $206.1 million in 2020 to $454.3 million in 2022. Its net income has also grown at a similarly rapid pace thanks to its insanely high gross profit margin of 83.89% and net income margin of 36.77%. The chart below illustrates INMD's phenomenal topline and bottom line growth over the past six years.

InMode Investor Presentation

Stock's valuation has not kept pace

Strangely, however, INMD's valuation has not kept pace with the underlying business's growth but has in fact slumped since the beginning of 2022 when interest rate hikes in the US and elsewhere triggered a broad sell-off in growth stocks.

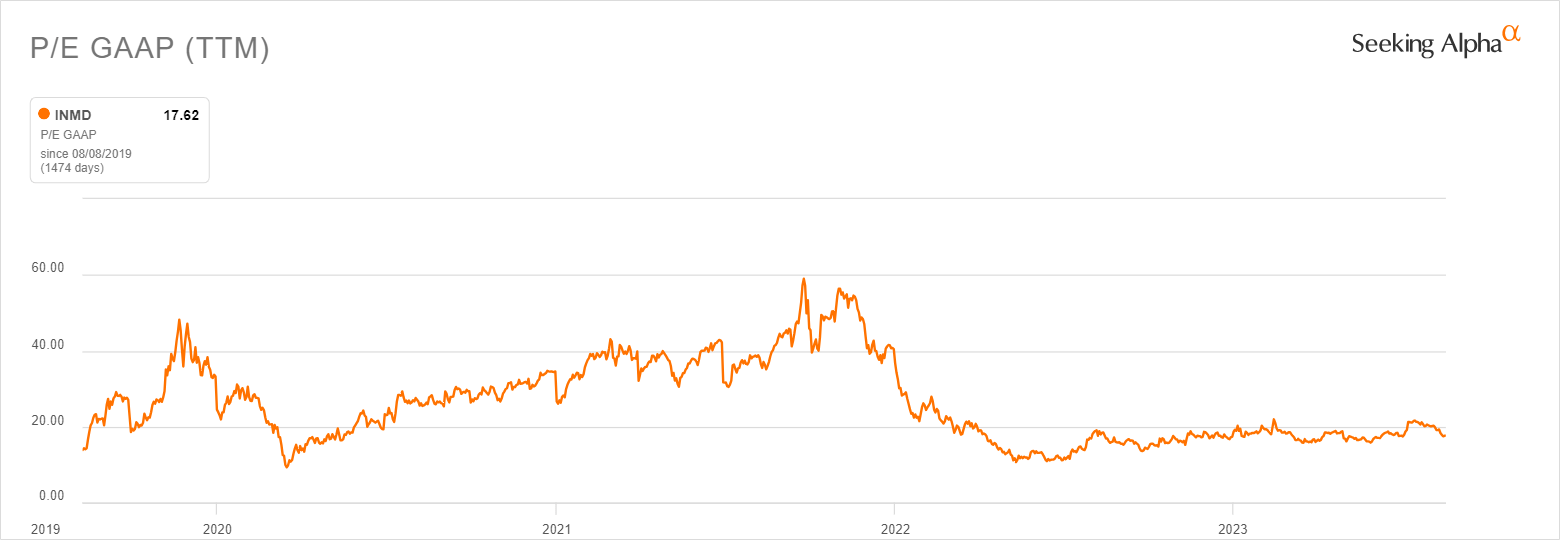

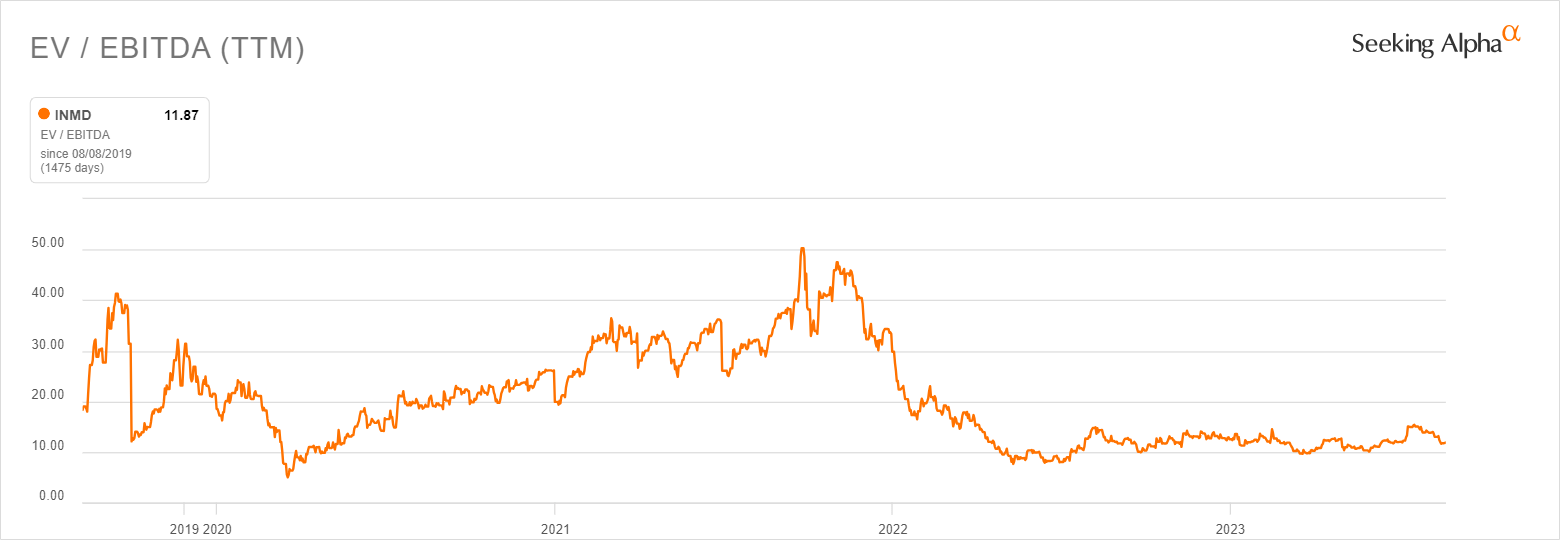

INMD is currently trading at a P/E of 17x, which looks expensive on the face of it but is actually cheap when compared with its 5 year average P/E of 24x. Its EV/EBITDA is currently at 11.87x vs a 5 year average of 20.83x. In comparison, the median healthcare sector P/E is 30.48x and the median EV/EBITDA is 14.76x as per SA data. The medical devices industry in particular had an average P/E of 35.18x as at August 2023, according to Full Ratio data . INMD is not only cheaper than it was historically, but is cheaper than most stocks in the medical device industry as well as the broader healthcare sector.

{kind=link}

{kind=link}

INMD has gotten cheaper by as much as 50% in the past 2- 3 years, despite the size of its business over this period more than doubling from a topline and bottom line perspective. INMD's depressed valuation suggests that the market is expecting the company's growth and profitability to slow down in coming years. This outlook is, however, not supported by the evidence, which suggests that INMD will continue growing profitably and robustly. Investors who believe this to be the case can take advantage of the current low valuation to build positions.

INMD's Management raised its guidance for FY 2023 in its Q2 earnings announcement . It now expects revenues between $530 million and $540 million; Non-GAAP gross margin between 83% and 85%; Non-GAAP income from operations between $238 million and $243 million; and Non-GAAP earnings per diluted share between $2.62 and $2.66. This represents continued growth from 2022. It's worth adding here that, since going public in 2019, INMD has never missed analysts' quarterly revenue estimates and has missed EPS estimates in only one quarter. This history of outperformance points to the strong growth momentum, which I believe is still at play today despite the deflation in valuation.

Bull case strengthened by cost advantages, clean balance sheet

Thanks to its high margins, INMD has the ability to maintain competitive advantages over its competitors by protecting its long-term profits. Its high margins also give it pricing power, which can help it protect its market share in market environments where price points drive customer decisions. INMD is able to maintain a very low cost base because it outsources manufacturing to contractors in Israel at a fixed cost per unit and maintains very low inventory, essentially ordering platforms when a customer needs it. Israel's government also provides generous incentives such as tax breaks and subsidies to grow its science and technology industries. INMD's facilities are in the highest tax benefit zones in Israel and, from 2022, the company's corporate tax rate is expected to be approximately 7.5 - 10%, according to its latest investor presentation .

In comparison, INMD's publicly listed competitors are all loss making as they don't enjoy the same cost advantages. Apyx Medical Corporation ( APYX ), an energy technology company that develops, manufactures, and sells medical devices in the cosmetic and surgical markets worldwide, has posted net losses in nine out of 10 years since 2013. Cutera ( CUTR ), which also sells energy-based devices for aesthetic treatment globally, had a net loss of 82.3 million in 2022 - the largest among several annual losses it has posted in the past 10 years.

INMD operating performance vs peers (Seeking Alpha)

Importantly, INMD has a strong balance sheet . It has no long-term debt and has been consistently improving its cash position, with its last reported total cash and short term investments coming in at $629.4 million in Q2 2023 vs $547.4 million in 2022, $415.9 million in 2021 and $260.5 million in 2020. CUTR in comparison has an outrageously high debt of $417.6 million vs $222.6 million cash in the most recent quarter while APYX has debt of $14.41 million vs $18.48 million.

From its strong profitable growth, to its low cost business model and clean balance sheet, there's a lot to like about INMD. Its recent Q2 results give further insights into how its devices are being used, with sales of disposables (or consumables) reaching an all-time high of over 270,000. Overall, revenue from consumables and service for the second quarter grew nearly 44% year-over-year and reached a record level of $21.6 million. Consumables and service revenues are an indicator of how frequently INMD's devices are used since they are used once and disposed. This growth in revenue from consumables indicates that physicians are using INMD's devices more, which is a bullish sign that the brand is gaining ground with doctors and patients alike.

A final word on the risks

No investment is without its own unique risks. A key risk for INMD is that it depends on the sale of platforms for over 80% of its revenue. This means that, if existing customers do not replace or upgrade devices, it must constantly seek new customers in order to grow. The risk with this is that growth prospects could dim if the market is saturated or if some physicians choose to go with competitor products.

Another risk is the fact that, despite its impressive profitability and growing cash reserves, INMD has a poor history of returning cash to shareholders. It has never paid a dividend and the buybacks it has done in the past have not moved the needle in terms of reducing the outstanding shares. In fact, outstanding shares have increased from 75.6 million in 2020 to 83.4 million in the most recent quarter. The lack of cash returns to shareholders could put off a section of institutional long-term investors who typically look at factors like dividends and buybacks before allocating capital. Without a solid base of institutional investors with longer-term time horizons, the stock could struggle to hold on to gains.

Finally, another risk (which some may view as an opportunity) is that INMD is still tightly controlled by the founders Moshe Mizrahy (the CEO and Chairman of the Board) and Dr. Michael Kreindel (the Chief Technology Officer and Director). The two , who founded the company in 2008, collectively own around 7.5% of the shares (Moshe approx 3.48% and Michael approx. 4.17%) , according to Refinitiv data on the Interactive Brokers online trading platform on 24 August. In comparison, Blackrock, the largest institutional investor, owns 5.74%. This level of control by executive founders means that strategic decisions such as potential acquisitions, returning cash to shareholders, or investing in new business lines could be disproportionately influenced by the two, even if other shareholders are opposed to these plans. Dependence on these executives also introduces key man risks, which is the phenomenon of placing knowledge, skills, and important relationships in the hands of one or a few staff members. Key man risks can affect issues such as succession planning, discouraging longer-term investors with 5-10 year time horizons.

These risks notwithstanding, INMD is deeply undervalued given the historical performance and prospects for continued profitable growth. It could prove to be a potentially rewarding buy for investors who take advantage of the historically low P/E and EV/EBITDA multiples.

For further details see:

InMode: Prolonged Valuation Slump Is A Buying Opportunity