NRGX - Innovative Conversion: How PIMCO Is Narrowing NRGX's NAV Discount

2023-11-15 18:36:22 ET

Summary

- PIMCO is converting the PIMCO Energy & Tactical Credit Opps closed-end fund from an energy MLP stock fund to a multi-sector bond/credit fund to narrow the discount-to-NAV.

- The NRGX fund currently trades at a discount of 11.42% compared to the average multisector credit fund discount of 3.4%.

- By combining the long position with short exposure, the potential return is isolated and independent from market/sector returns.

PIMCO is converting its PIMCO Energy & Tactical Credit Opps ( NRGX ) from an energy MLP closed-end equity fund, or CEF, to a multi-sector bond/credit fund. This is an interesting trick to narrow the discount-to-NAV of this fund. It is working. The market has picked up on it, and the discount has narrowed noticeably:

There's still an interesting opportunity to buy this closed-end fund and benefit from the discount to net-asset value shrinking further.

The announced conversion will take place on November 21, 2023. That's just six days from now. Meanwhile, the fund trades at a discount to net asset value of 11.42%.

To put that into perspective, the average multisector bond/credit fund trades at a discount of only 3.4%. If the NRGX fund starts trading in line with its peer group, it could appreciate by 8.6%. I pulled up data on every CEF with the multi-sector qualification through Morningstar (see table below). Interestingly, the PIMCO multi-sector funds trade at an average premium of 0.34%. The deepest discount on one of these funds under PIMCO management is -4.2%:

| Name |

| Morningstar classification |

| Manager |

| AUM |

| Discount |

| FS Credit Opportunities Corp. |

| Morningstar US CEF Multi-Sector |

| FS Global Advisor LLC |

| $1,146 MM |

| -16.47% |

| Virtus Global Multi-Sector Income Fund |

| Morningstar US CEF Multi-Sector |

| Virtus Investment Advisers, Inc. |

| $79 MM |

| -13.88% |

| Western Asset Diversified Inc Fund |

| Morningstar US CEF Multi-Sector |

| Franklin Templeton Investments |

| $670 MM |

| -11.73% |

| TCW Strategic Income |

| Morningstar US CEF Multi-Sector |

| TCW |

| $222 MM |

| -6.83% |

| BNY Mellon Alcentra Gl Crd Inc 2024 Tgt |

| Morningstar US CEF Multi-Sector |

| BNY Mellon |

| $116 MM |

| -5.80% |

| DoubleLine Yield Opportunities Fund |

| Morningstar US CEF Multi-Sector |

| DoubleLine Capital LP |

| $679 MM |

| -5.47% |

| Virtus Convertible & Income 2024 Tgt |

| Morningstar US CEF Multi-Sector |

| Virtus Investment Advisers, Inc. |

| $156 MM |

| -5.23% |

| PIMCO Access Income |

| Morningstar US CEF Multi-Sector |

| PIMCO |

| $594 MM |

| -4.19% |

| PIMCO Income Strategy II |

| Morningstar US CEF Multi-Sector |

| PIMCO |

| $549 MM |

| -1.96% |

| Doubleline Opportunistic Cred |

| Morningstar US CEF Multi-Sector |

| DoubleLine |

| $234 MM |

| -0.84% |

| PIMCO Income Strategy |

| Morningstar US CEF Multi-Sector |

| PIMCO |

| $294 MM |

| 1.33% |

| PIMCO High Income |

| Morningstar US CEF Multi-Sector |

| PIMCO |

| $658 MM |

| 1.61% |

| BlackRock Multi-Sector Income Trust |

| Morningstar US CEF Multi-Sector |

| BlackRock |

| $549 MM |

| 3.41% |

| PIMCO Dynamic Income Fund |

| Morningstar US CEF Multi-Sector |

| PIMCO |

| $4,726 MM |

| 5.09% |

| Guggenheim Strategic Opp Fund |

| Morningstar US CEF Multi-Sector |

| Guggenheim Investments Asset Management |

| $1,543 MM |

| 8.66% |

NRGX has $1.14 billion in assets under management ("AUM"). Its leverage ratio is 13.29%, and the distribution rate is 4.47%. The management fee is 1.35% and will be lowered to 1.25% in the future (on conversion). The total expansion ratio, including interest expenses, sits at 2.66%. Usually, I like to look at the portfolio of CEFs I'm buying to gather information on what to expect of the managers in the future. Here, the portfolio isn't super-relevant. The portfolio will be turned over on conversion. I just need to know what's in there for hedging purposes.

I always buy CEFs at a relatively deep discount to NAV to hold on to them until the discount narrows. In this case, that could happen unusually fast. Because my bet is to profit from the discount narrowing, I don't want this uncorrelated "return stream" to get polluted by moves in the MLP sector. That's why I want to pair the long position with a hedge offsetting most of the market and MLP risk.

Theoretically, the expected return is higher if I go long with this CEF. I would profit from the CEF's beta and the narrowing of the discount. In practice, the beta could easily overshadow any return from the narrowing of the discount, and it would greatly reduce the risk-adjusted return. An MLP fund has quite a bit of risk (a bit less than most equities). An isolated return stream dependent on whether investors will value a multisector credit like a credit fund instead of an MLP fund seems like a much better risk-reward. It is hard for me to fathom the spread moving in the opposite direction, for example. I consider that a low probability over the next month.

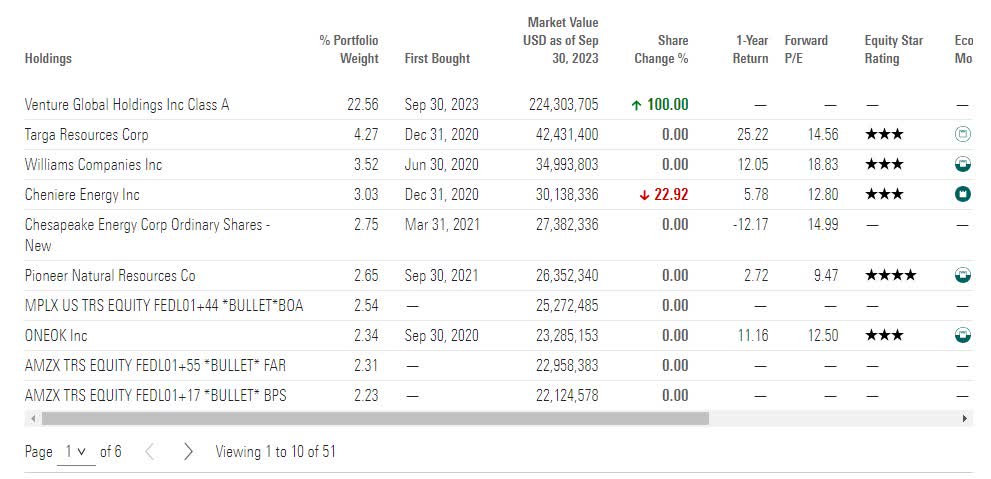

I pulled the top 10 positions from Morningstar:

NRGX portfolio (Morningstar.com)

{kind=link}

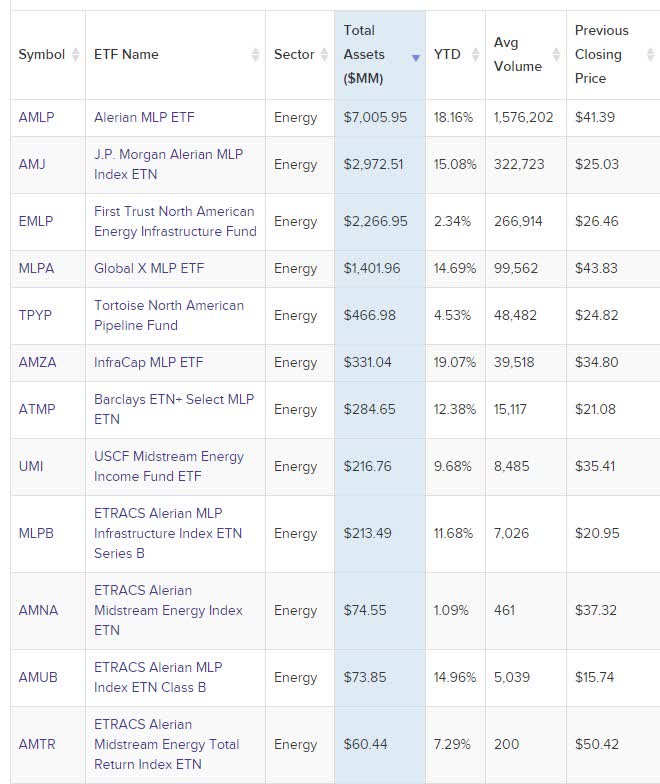

My preferred way to hedge this fund is through a proxy hedge like an MLP ETF to offset most of the market/industry risk. I've used the Alerian MLP ETF ( AMLP ) to offset around 70% of the risk. I also shorted the iShares High Yield ETF against it to offset 10% of the position. This simple proxy short could be improved by adding a short in the Spider Bloomberg 1-3 Month Treasuries ( BIL ) worth around 20% of the position.

I'm unsure why the fund carries several short-term notes and short-term investment-grade securities. I'm guessing it is a function of the transformation. These relatively high-yielding cash alternatives keep the fund more competitive while it is approaching its conversion date.

The MLP ETF I used has a 0.78 correlation with the CEF and generally moves between 0.7 and 0.9. A value of 1 would indicate perfect correlation. There are periods where the correlation suddenly breaks down, though. Keep in mind that's a risk.

Ideally, you could attempt to hedge out all the individual components, but the costs will quickly increase. A full holdings report is NRGX)%20Portfolio%20Holdings.xlsx&id=q4HTsPkNnM%2byJJNlupnMthFXo9CRh%2fJyx8%2bmMjPaa1Mduc6n3DUVGiIviFurtk6eB9LyDG0WmhNiACen%2f2QYj%2bLhfU9f1VuOHO35fcdS%2fZd%2fLSLk3RZlp9poS%2bqHHneqhcQR8Ui%2bEqjcc2CkQbPpUBk07EY7hPkUL5Prc90ZZ5xAl9F1WDihwQlSjEedLdNfZEcpr3N1OC%2bmqhqD3pbUlKvB%2f%2f5TZ2NeiyoRpwzsX7QDZ7oZSXS9%2fVFqQPtF6%2fnrYeqSDGFm4DUa8Yhf%2fKyt4rg2Hg5YI05IOE%2fpxzUT0QKWkHDN37VY034wQ8otLoAbWVbUA2al1DZV%2bcfuiNTaWrNVimaa0Y2OPv0BWqTuf5NUoROOQMHN93bImdcOWrdn0PlNklHMEJls7ZMcc%2fRulp6Gdug9UCXysg3a7Ni6FynE2H7WaUOGBX4a0IZPEBCYtrw0jr%2fYKFeOoHlEHWvLZLJl%2bFY42zGDrK1bHXxcKNg%3d" > available here . You could also use other MLP ETF's or short a combination of them. There are many options available. The table below is from ETFDB :

NRGX portfolio (Morningstar.com)

{kind=link}

Another one worth mentioning is the JPMorgan Alerian MLP ETN ( AMJ ), which shows a very high current correlation. Its correlation has generally been in the 0.8 - 1 range for the year.

Even though the correlations generally look good, the hedges won't be perfect. ETFs aren't using leverage, for example. Even if an ETF contained the same holdings, it would move slightly differently. Things will get tricky after the conversion date. Likely, the discount won't disappear on the ticker change. I think it takes time for the information to percolate through the market. Over time, CEF investors looking for credit funds will notice this one has a relatively attractive discount. It should attract a relatively large slice of the flows into credit CEFs, and this will close the discount.

The problem is that we won't know exactly what the fund is invested in after the conversion date until it next reports. It is unrealistic to expect management to turn over the billion-dollar portfolio in a day or even days.

On or around the 21st, I plan to switch out the MLP short leg. I'll replace it with a combination of the high-yield ETF I mentioned earlier (another high-yield ETF should also work) and the iShares 1-5 Year Investment Grade Corporate Bond ETF (IGSB). I would allocate 40% of my short exposure to either and keep the 20% already dedicated to shorting BIL. As more information about the new portfolio becomes available, it will be easier to fine-tune the short leg.

In conclusion, the imminent conversion of PIMCO's NRGX into a multi-sector bond/credit fund is an opportunity to generate uncorrelated returns. The fund’s discount to net asset value ((NAV)) has already begun to narrow noticeably. As the conversion date rapidly approaches there is still a lot of potential upside. Using a hedging strategy, like the suggested combination of MLP ETFs and short positions in various other instruments, investors can reduce a lot of market and sector risk. As the fund converts, it is important to shift hedges towards a credit profile and keep tabs on the new portfolio as it becomes available.

For further details see:

Innovative Conversion: How PIMCO Is Narrowing NRGX's NAV Discount