POTX - Innovative Industrial Properties: Probably Best Not To Chase

2024-01-18 01:10:19 ET

Summary

- Innovative Industrial Properties has delivered strong returns of over 4.4x in the last 6 months, outperforming the broader market.

- The growing public sentiment and potential reclassification of cannabis to Schedule 3 bode well for IIPR's position in the regulated cannabis industry.

- IIPR's valuation is higher compared to peer- NewLake Capital Partners, and the latter also offers better FFO growth and dividend prospects.

- The risk-reward on the standalone chart looks fair, but relative to other cannabis stocks, IIPR looks overextended.

Strong Performance Off Late

Innovative Industrial Properties Inc ( IIPR ) is a mid-cap REIT, that leases its industrial properties on a triple-net lease basis to cannabis operators with the requisite state licenses ( 98.5% of its 103 operating portfolios were leased to 29 regulated cannabis operators).

Over the last 6 months, when the broader markets have only eked out single-digit returns, IIPR has proven to be a star, delivering returns of over 4.4x during this period.

{kind=link}

Rumblings Of A Reclassication Shift Bode Well

Currently, roughly 40 states across the US, including the District of Columbia, have legalized cannabis for medical use (meanwhile 22 states have legalized the drug for adult use alone), and IIPR is well-positioned to benefit from the growth of these markets as it already owns properties in 19 of these states. One can be reasonably hopeful of further development in the existing markets and the opening up of other obdurate markets, as the stigma associated with cannabis is quickly dissipating.

Already in 2022, a survey conducted by Pew Research showed that an overwhelming share of US adults (89%) were backing the legalization of cannabis for both medical and adult use, or medical use alone.

Pew Research

It appears that growing public sentiment appears to be leaving a mark on the regulatory authorities, and last year we saw the Department of Health and Human Services ((HHS)) recommend that the US DEA (Drug Enforcement Agency) reclassify cannabis from the Schedule 1 (which currently also includes dangerous drugs such as LSD and heroin) to Schedule 3 (which currently includes drugs with moderate to low potential for physical and psychological development) of the Controlled Substances Act ((CSA)).

What’s even more encouraging is that a few days back even the US FDA provided scientific support for marijuana’s use in the medical field, and they’ve also gone ahead and endorsed the reclassification towards Schedule 3.

Now the DEA still needs to make an independent evaluation on the same and is not bound by any specific timeline, but given that we are in an election year, it's reasonable to expect some clarity this year itself.

Besides the obvious sentiment shift associated with a Schedule 3 tag, it would also mean that the pernicious section 280e of the IRC (Internal Revenue Code) which is levied on items in Schedule 1 and 2 of the CSA would no longer apply to cannabis. As things stand, sales of products in schedule 1 and 2 don’t get the benefit of tax credits or tax exemptions, and this tends to weigh adversely on the financial health of these operators.

From a risk management perspective, we think the shift to schedule 3 could work well for IIPR as the regulated cannabis industry has been prone to a lot of consolidation, as the smaller players with weak financial profiles inevitably get taken over. IIPR which strives to limit its single-tenant exposure to 20% of its total assets thus runs the risk of breaching this. But now, as the broad interest rate regime shifts lower, and with the potential of schedule 3 classification, we think the financial health of a lot of IIPR’s tenants could be looking up.

Valuation Considerations

To better understand IIPR’s valuation quotient, we thought it would be pertinent to contextualize its numbers relative to NewLake Capital Partners ( NLCP ), the other major triple-net lease REIT that dabbles in the state-regulated cannabis space.

Note that IIPR is the pricier option of the two, priced at a multiple of 11.53x, based on an FFO (Funds from Operations) per share of $8.13 for FY24. In contrast, NLCP can be picked up at a -21% discount on a P/FFO basis, with a corresponding multiple of 9.15x (based on the FY24 P/FFO of $1.84 ).

Seeking Alpha

We would have no qualms about paying that premium if you were getting solid enough FFO growth this year, but that isn’t the case. Note that even though NLCP is priced at a discount it still offers a decent cadence of annual FFO growth of +4% for FY24, whereas IIPR won’t offer you any positive FFO growth this year, with the metric poised to decline by -0.9% annually.

Dividend Considerations

Prima facie, prospective investors who take a cursory interest in the IIPR stock may also be moved by the stellar current yield of 7.77%, but we feel some additional context is required here again.

Firstly, consider that since H2-22, IIPR’s yield hasn’t been as competitive as NCLP’s corresponding figure, and except for a brief contraction in the variance last year, the gap between the two yields has been large enough (over +160bps currently).

{kind=link}

As far as target dividend policies are concerned, both link their payouts to their respective AFFOs (Adjusted Funds from Operations), and as things stand, NCLP is also paying out a larger chunk of its AFFO via dividends (82% as of Q3-23, whereas IIPR only distributed 79%).

It’s worth noting that IIPO’s dividend growth p.a. has already been on a declining trend for the last two years. A couple of years back it grew at an impressive pace of +17%, but last year the growth slumped to 3%, and recently the hike in Dec has come in at only 1.1%.

Investor Presentation, Earnings transcripts

Now, as covered in the previous section, IIPR’s FFO is already at risk of contracting in FY24 (no AFFO estimates are available), so the payout growth too is unlikely to be too resplendent this year. But even otherwise, do consider that NCLP has a better target AFFO payout range of 80-90%, as opposed to IIPR’s lower target of 75-85%. So given that the former is looking at FFO growth this year, and that its current AFFO payout is at the lower end of its target range, investors can be more optimistic about NCLP's dividend prospects than IIPR's.

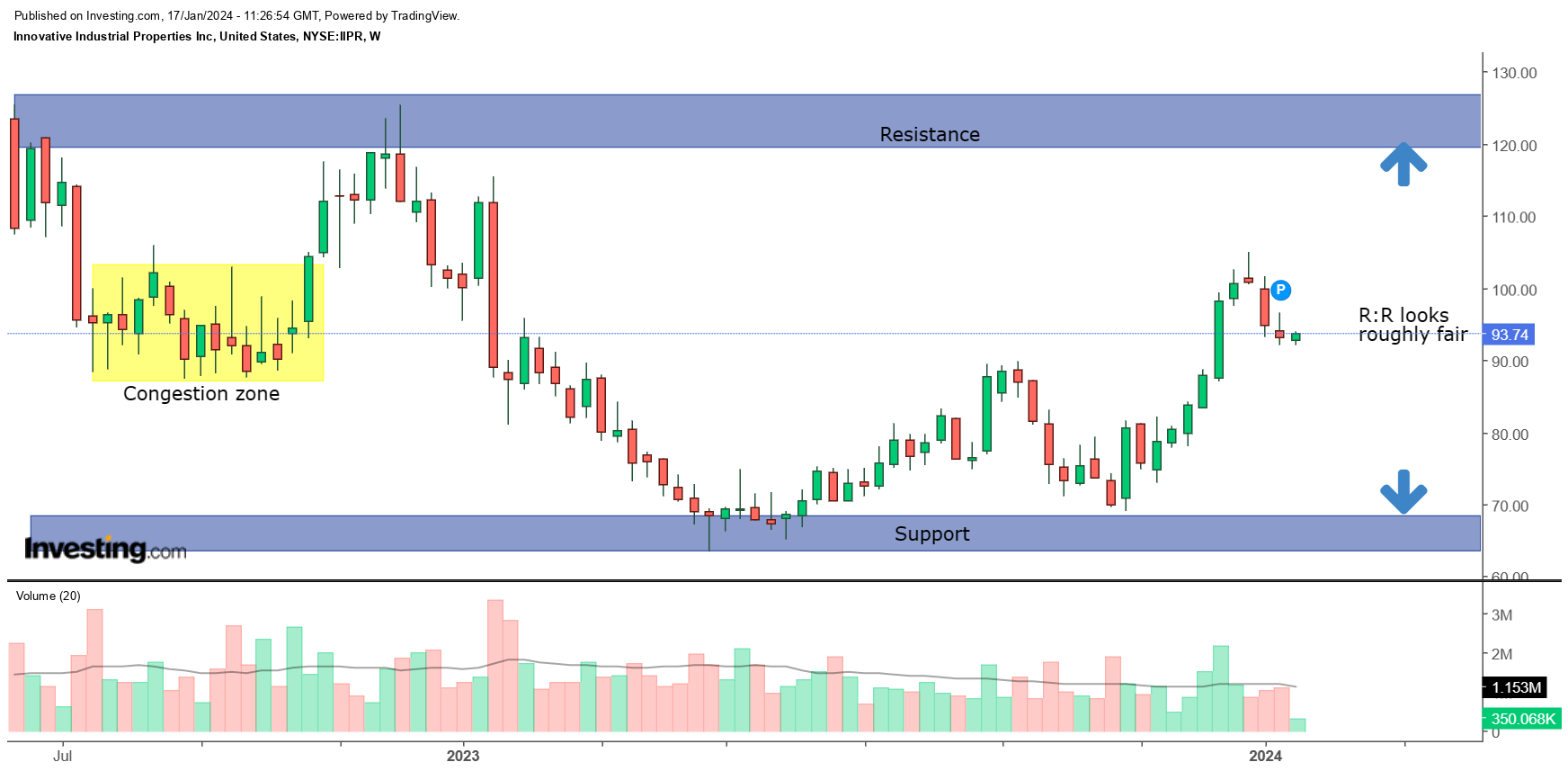

Closing Thoughts - Technical Considerations

On IIPR's standalone weekly chart, it looks like the stock has established a trading range within the last 1.5 years; at the lower end, you have some support at around the $63-$70 levels, and at the $120-$125 levels, there appears to be a resistance zone.

{kind=link}

After bottoming out in April last year, the IIPR stock has done well to trend up offering two pullback opportunities in the process (we are currently in the middle of the second leg pullback).

Now if one were to contemplate a long position at current price levels, keeping the resistance and support in mind, one is neither enthused nor put off as the risk-reward looks roughly fair.

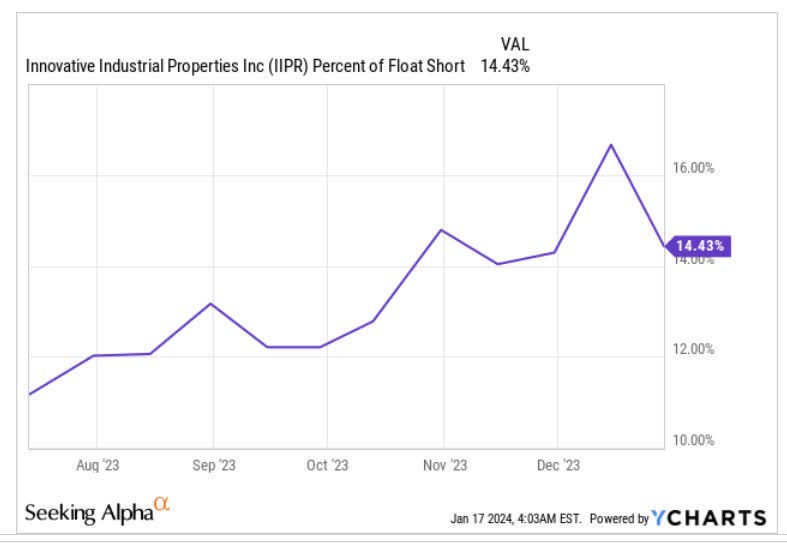

Having said that, also bear in mind that you’re dealing with a stock that has traditionally been a popular target of the bears (as things stand, the % of IIPR’s float that is short stands at over 14%), and in light of this, you ideally want to get in somewhere closer to support, rather than the mid-point of the long-term range.

{kind=link}

Finally, also consider that over the years IIPR has emerged as one of the popular routes to play the cannabis trade, but at this point it's also worth pondering if interest here has gone too far. The relative strength ((RS)) ratio is a useful ratio to help ascertain the rotational prospects of a stock within a certain industry (you ideally want to go long when the relative strength ratio is at lowly levels relative to its long-term range), and here we’ve looked at how IIPR is positioned relative to other cannabis play. Given how elevated the current RS ratio looks, it’s difficult to make a case for IIPR to benefit from rotational interest at this juncture.

{kind=link}

For further details see:

Innovative Industrial Properties: Probably Best Not To Chase