IGIC - International General Insurance: This Top-Rated Small-Cap Is Still Cheap

2023-11-16 02:28:42 ET

Summary

- International General Insurance Holdings is a $520-million market cap specialist commercial insurance and reinsurance group with a presence in over 200 countries and markets worldwide.

- In Q3 FY2023, IGIC reported a 51.8% YoY decrease in net income. But the firm is growing strong YTD, expanding tangible book value and keeping the shareholder return policy generous.

- IGIC stock is still cheap even after the YTD run-up in its price. My simple calculations say IGIC should be ~42% higher by the end of FY2024.

- I believe the Company is well-positioned to keep on growing further. Hence my today's 'Buy' rating, despite some crucial risk factors.

The Company

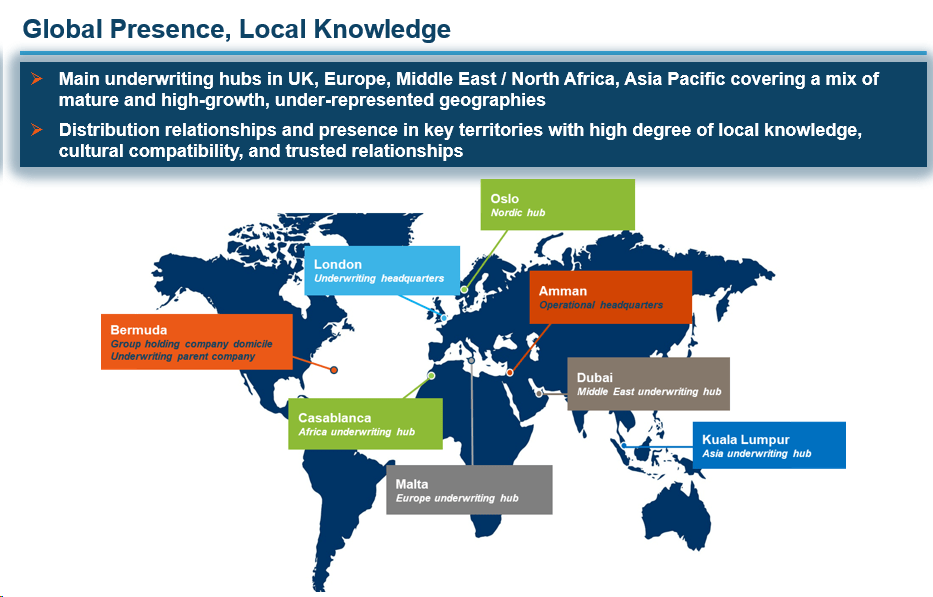

International General Insurance Holdings Ltd. ( IGIC ) is a $520-million market cap specialist commercial insurance and reinsurance group with a presence in over 200 countries and markets worldwide. With offices in London, Bermuda, Amman, Malta, Oslo, Dubai, Casablanca, and Kuala Lumpur, the company is distinguished for its niche underwriting expertise and responsive claims services. Operating since its founding in 2001 and headquartered in Amman, Jordan, IGI offers a diverse portfolio of specialty insurance and reinsurance solutions across three segments: Specialty Long-tail, Specialty Short-tail, and Reinsurance. The company's underwriting scope encompasses a wide range of risks, including energy, property, construction and engineering, ports and terminals, general aviation, political violence, professional lines, financial institutions, marine, contingency, treaty, and casualty reinsurance.

{kind=link}

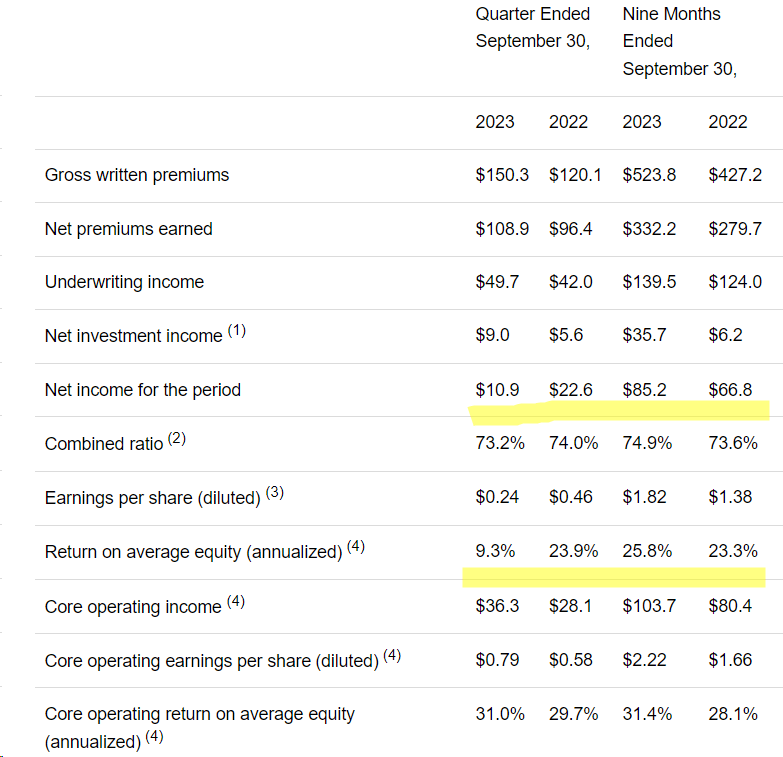

In Q3 FY2023 , IGIC reported a 51.8% decrease in net income to $10.9 million compared to the same quarter in 2022. This decline was mainly attributed to a negative movement of $17.2 million in the fair value of derivative financial liabilities, coupled with higher net loss, loss adjustment expenses, and general and administrative expenses. However, it was partially offset by a $12.5 million increase in net premiums earned and a positive movement of $3.4 million in net investment income. The return on average equity for Q3 2023 was 9.3%, down from 23.9% in Q3 2022.

{kind=link}

You would think that this 14.9% year-on-year drop in return on equity should lead to an immediate drop in shares following the release, but at the moment we are seeing the opposite reaction:

Seeking Alpha

Why?

I think it's because the market perceives the drop in ROE in Q3 as a one-off event, focusing mainly on the YTD results. For the nine months ended September 30, 2023, IGI reported a 27.5% increase in net income to $85.2 million compared to the same period in 2022. This growth was primarily driven by a $52.5 million increase in net premiums earned and a positive movement of $29.5 million in net investment income. The return on average equity for YTD was 25.8%, up from 23.3% in the same period in FY2022.

The underwriting results for Q3 DY2023 and 9M FY2023 showed positive trends, with underwriting income increasing and gross written premiums growing across all segments. The combined ratio for the quarter ended September 30, 2023, improved to 73.2% compared to 74.0% for the same period in 2022.

Segment-wise, the Short-Tail Segment demonstrated substantial growth, recording a 28.4% increase in gross written premiums for Q3 2023 compared to the same quarter in 2022, resulting in higher net premiums earned and underwriting income. The Reinsurance Segment also experienced significant growth, with gross written premiums increasing from $6.4 million in Q3 FY2022 to $15.3 million in Q3 FY2023 [+139% YoY], leading to improved underwriting income.

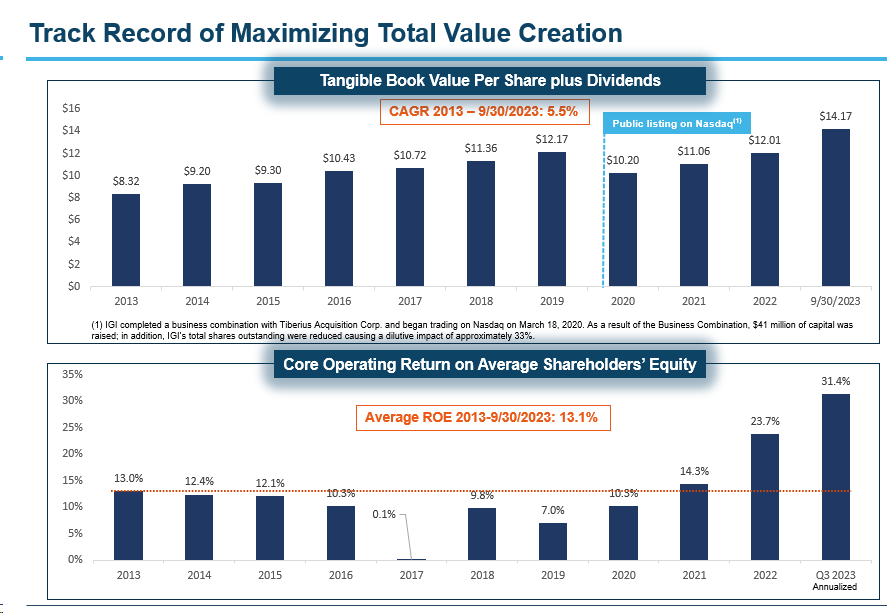

So despite challenges in the derivatives market, IGIC demonstrated positive operational performance in underwriting and premium segments, sustaining exceptional momentum in tangible book value growth during the reporting period:

{kind=link}

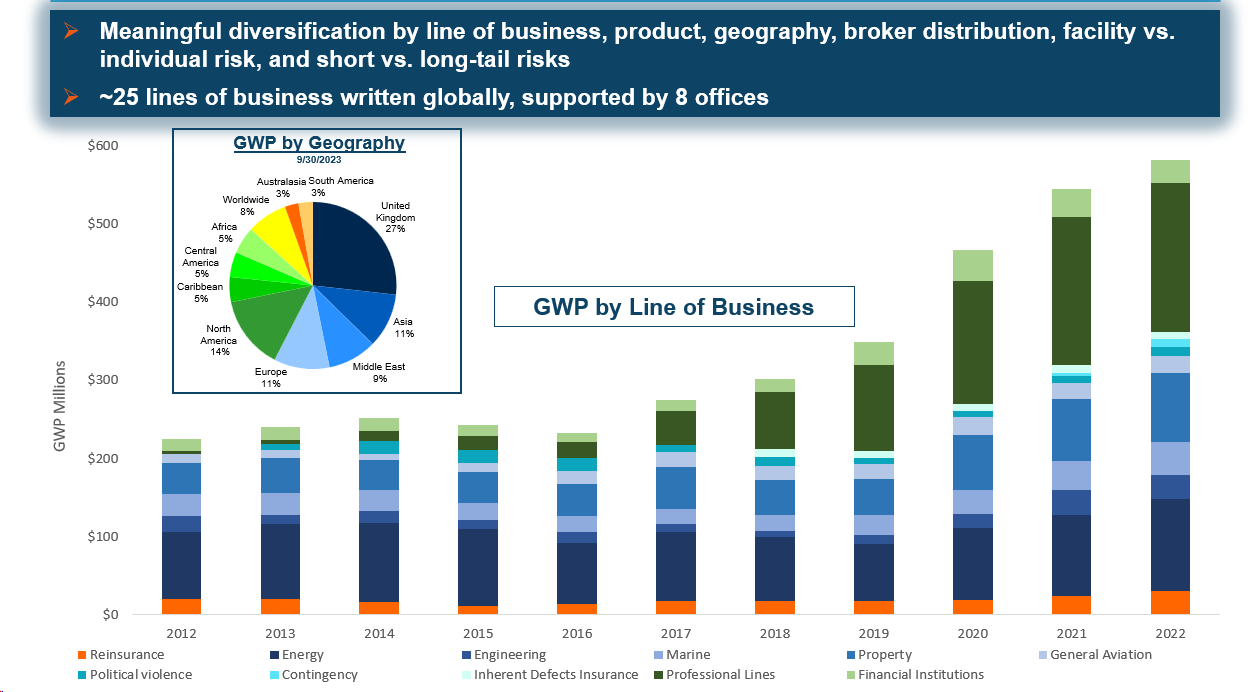

From what I see, IGIC seems to be strategically positioned for future value creation, emphasizing expansion in the US and European markets. In the US, it has achieved $72.8 million in business, primarily in short-tail segments, according to the latest IR materials. In Europe, the focus is on long-tail lines with additional short-tail business. The company aims to capitalize on market opportunities by adapting its underwriting focus and promoting efficiency through a single "hub" approach.

Diversification and growth remain key priorities, with plans to capitalize on the recent acquisition of the Norwegian Energy Insurance Oslo AS for growth in Nordic markets. IGIC also maintains a presence in Bermuda, gradually expanding its reinsurance treaty business.

{kind=link}

The management emphasizes IGIC's prudent capital management with a focus on profitable underwriting growth and returning capital to shareholders through dividends and share repurchases. The company has repurchased 3,329,800 common shares, utilizing 67% of its current authorization, and holds a repurchase authorization of up to 5 million common shares [according to Q3 FY2023 IR presentation ]. The firm also pays a regular quarterly common share dividend of $0.01 per share [ <1% in yield ], which looks like a nice addition to the overall shareholder return policy. On September 19, 2023 , IGIC purchased all outstanding warrants and basically made its capital structure clearer, now having more room to grow its common share dividend.

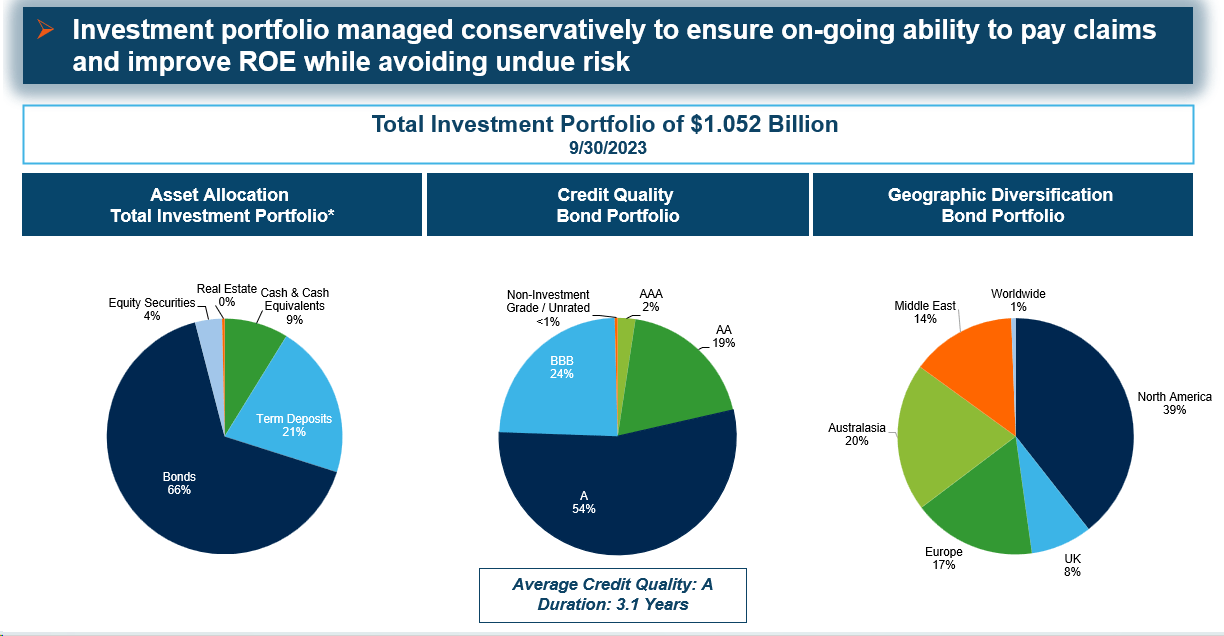

Overall, IGIC appears to be a fairly stable company with a growing presence in the world and a high-quality investment portfolio that is favorably positioned for the Fed's monetary policy turnaround (66% of the portfolio in bonds with an average credit rating of "A" and an average duration of 3 .1 years):

{kind=link}

IGIC definitely has a future, given its current focus and historical development. But to what extent is the stock valued favorably?

The Valuation

The company has actively increased its tangible book value in recent years. Today, IGIC's price-to-tangible book value ratio is slightly above the average historical range and is still a modest 1.118x:

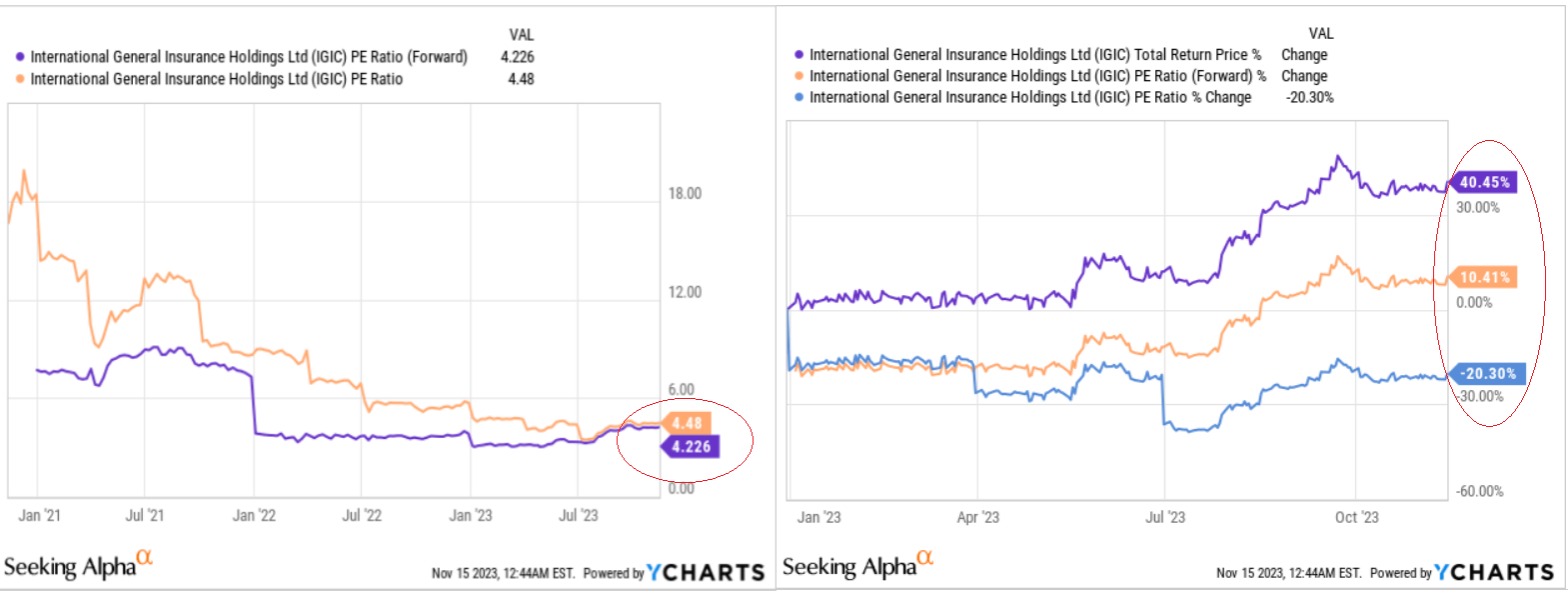

In my opinion, we cannot call the IGIC stock expensive with a forwarding P/E ratio of only ~4.2x. Surprisingly, the 40% YTD share growth we observed was not due to multiple expansions (as was the case in the tech sector in 2023) as the TTM P/E continued to fall as the stock grew:

{kind=link}

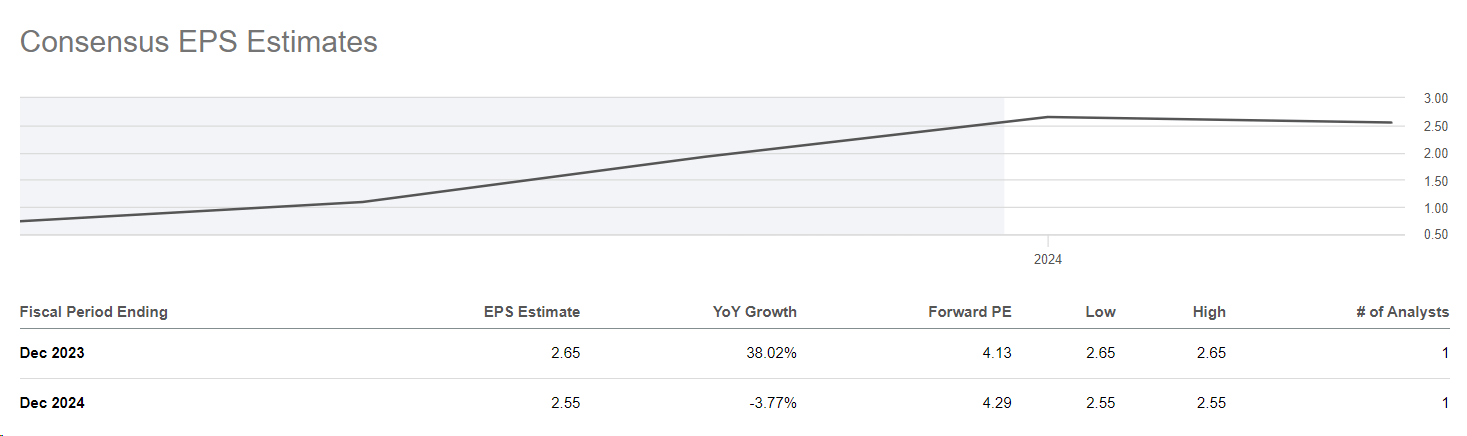

There are two explanations for this: Either the stock was overvalued from the outset, or the market expects IGIC's earnings per share to fall significantly in the future. In IGIC's case, the second option is more likely, as multiples were low to begin with and Wall Street is factoring a 3.77% YoY decline in EPS in FY2025, according to consensus estimates :

{kind=link}

But even if we assume that the only estimate for FY2025 is close to reality: isn't the implied 4.29x in FY2025 P/E ratio too small to be fair?

| P/E in FY2024 |

| EPS growth in FY2024 |

| IGIC |

| 4.29 |

| -3.77% |

| UVE |

| 7.05 |

| 5.02% |

| GBLI |

| 10.52 |

| 30.33% |

| HCI |

| 10.04 |

| 45.23% |

Source: Author's compilation, multiple sources

IGIC's Q3 FY2023 results beat the consensus expectations by ~80% ($0.79 actual vs. $0.44 expected), so if it continues for the next few quarters, the firm is unlikely to post even a decline in EPS next year. So I assume IGIC's "relatively fair" P/E ratio to be ~6x by the end of FY2024 at about $2.65 EPS (5 cents higher vs. consensus). That brings me to the target price of $15.9, which is ~42% higher than today's price of IGIC.

The Bottom Line

Of course, investing in IGIC stock comes with some risks that should be carefully considered by investors. This non-US company is exposed to market fluctuations, underwriting uncertainties, and regulatory changes. Also, every small-cap company, especially in the insurance industry, is quite volatile, so every potential investor should be ready to stomach that volatility. Global economic conditions, competition, and cybersecurity threats further contribute to the risk profile. Additionally, dependencies on key personnel and the success of growth strategies introduce additional considerations.

But despite these risk factors, I believe IGIC is well-positioned to keep on growing further. I like the fact that it's a family-run business (Jabsheh family ownership is at 33.1%), so the management is more than motivated to drive growth and keep it of a high quality. At the same time, the stock is still cheap even after the run-up in its price YTD. My simple calculations say IGIC should be ~42% higher by the end of FY2024, so I rate the stock as a 'Buy' and recommend everyone pay attention to this company.

Thanks for reading!

For further details see:

International General Insurance: This Top-Rated Small-Cap Is Still Cheap