IPGP - IPG Photonics Corporation: Could Go Either Way

2023-06-16 05:52:18 ET

Summary

- The stock has soared higher in recent days for a couple of reasons, a rally some may or may not want to participate in.

- IPGP got a timely upgrade for its potential growth upside, but it’s worth questioning its validity when sustained growth has been a problem for quite some time.

- IPGP has problems that it is trying to get resolved and IPGP is making progress in that regard, even if there’s work left to do.

- There is an argument to be made for or against long IPGP and there is really no one size fits all as things stand right now.

IPG Photonics Corporation ( IPGP ) has certainly turned it around in recent days. IPGP stock was heading lower as recently as June 6, but the stock has soared higher in recent days to match the 2023 high, thanks to a 13.47% jump in the stock after an upgrade from Raymond James Financial. Why will be covered next.

The stock breaks out

The stock gained 13.47% to close at $132.83 on June 14. At one point, the stock got as high as $136.72, which is a 2023 high, before pulling back. This is rather interesting because the stock closed at $133.41 on February 16, which is just $0.58 more than $132.83. It’s too early to tell, but the stock peaking at roughly the same price level months apart may be a sign resistance is present nearby.

The stock spent months trending lower between the February high of $133.41 and the June high of $132.83. The slide started after the February 16 high and it ended on June 6 when the stock hit an intraday low of $107.54 before rebounding to end the day up for the day at $110.29. That the stock bounced where it did was most likely not a coincidence.

Note the lower ascending trendline in the chart below, which has provided support since last year. The stock came into contact with this trendline on June 6, which could explain why the stock bounced that day. The stock rose in the following days, culminating in a 13.47% one-day gain on June 14.

{kind=link}

Source: finviz.com

The 13.47% gain happened the day Raymond James Financial, an investment bank, upgraded the stock from market perform to outperform. This upgrade came at a good time. Note the upper descending trendline. The upgrade came at a good time because it happened at a time the stock was facing resistance imposed by this trendline. If there had been no upgrade or if the upgrade happened on some other day, the stock would likely not have jumped as much as it did. The stock is now up 40.3% YTD.

Why some may not want to buy the rally

The stock has turned it around in recent days. The stock hit an intraday low of $107.54 as recently as June 6, but the stock has gained 23.5%, most of it on June 14, to end at $132.83 just eight days later. However, such a quick gain also means the stock is now overbought with an RSI value of 74.37. Some sort of pullback is likely in the coming days due to this.

Furthermore, there is reason to question whether the stock is worth buying at this time as some like Raymond James argue. The stock was upgraded for its potential earnings upside, but there is very little real growth to be found at IPGP at this time. Granted, some segments like EV are showing growth, but this is offset by contraction elsewhere. IPGP has potential, but it’s not living up to it at the moment.

{kind=link}

Source: macrotrend.net

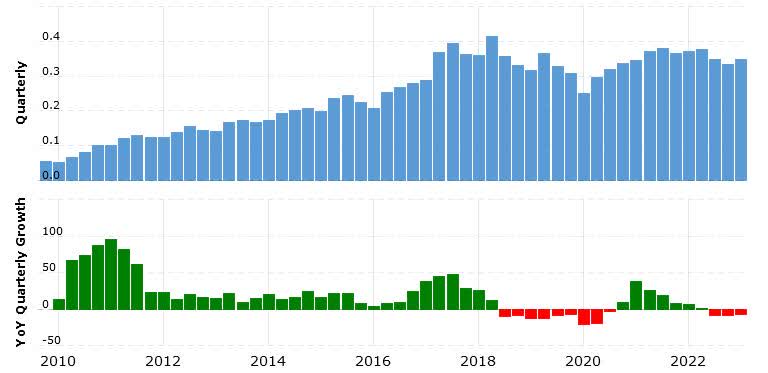

A look at the most recent report shows as much. Q1 FY2023 revenue increased by 4.1% QoQ, but it also decreased by 6.2% YoY to $347.2M. Revenue growth has been rather flattish in recent years as shown in the chart above. Margins shrank YoY, resulting in a 3.8% YoY decline in EPS to $1.26. The table below shows the numbers for Q1 FY2023.

The decline could have been even greater if not for foreign currency transaction gains, which added $3M to operating income and $0.06 to EPS. On the other hand, fluctuations in foreign exchange rates did reduce revenue by $15M. The bottom line also benefited from a YoY decline in operating expenses to $71.5M, but keep in mind that this was mostly the result of less spending on R&D, which fell to $22.77M from $33.45M a year ago.

The EPS number should be seen in another light. Note that net income fell by a greater amount than EPS with a 13.6% YoY decline. This is because IPGP spent $113M in Q1 to buy back shares, which reduced the share count to 47,776K. This helped boost earnings per share in Q1, similar to what happened in previous quarters.

On the other hand, stock buybacks have left their mark on the balance sheet. Cash, cash equivalents and short-term investments decreased to $1,069.6M in Q1 FY2023, down from $1,177.6M in Q4 FY2022 and $1,514.5M in Q1 FY2022. IPGP has spent a big chunk of its cash hoard on stock buybacks and this is set to continue with a new $200M share repurchase program announced by IPGP.

IPGP also posted big QoQ gains in Q1, but keep in mind that Q4 FY2022 was badly affected by a $79M asset impairment of long-lived assets, a $74M inventory provision charge and $10M of other restructuring charges, which increased expenses, reduced margins and ultimately led to a loss of $1.91 per share in Q4 FY2022.

| (Unit: $1000, except EPS, margins and shares) |

| (GAAP) |

| Q1 FY2023 |

| Q4 FY2022 |

| Q1 FY2022 |

| QoQ |

| YoY |

| Net sales |

| 347,174 |

| 333,539 |

| 369,979 |

| 4.09% |

| (6.16%) |

| Gross margin |

| 42.3% |

| 18.2% |

| 46.4% |

| 2410bps |

| (410bps) |

| Operating margin |

| 21.7% |

| (26.5%) |

| 25.2% |

| 4820bps |

| (350bps) |

| Operating expenses |

| 71,512 |

| 149,304 |

| 78,678 |

| (52.10%) |

| (9.11%) |

| Operating income |

| 75.426 |

| (88,480) |

| 93,143 |

| - |

| (19.02%) |

| Net income (attributable to IPGP) |

| 60,135 |

| (92,895) |

| 69,572 |

| - |

| (13.56%) |

| EPS |

| 1.26 |

| (1.91) |

| 1.31 |

| - |

| (3.82%) |

| Weighted-average shares outstanding |

| 47,776K |

| 48,720K |

| 53,100K |

| (1.94%) |

| (10.03%) |

Source: IPGP Form 8-K

Guidance calls for Q2 FY2023 revenue of $325-355M, a decline of 2.1% QoQ and 9.8% YoY at the midpoint. The forecast sees EPS of $1.05-1.35, which is an increase of 9.1% YoY at the midpoint. However, keep in mind that Q2 FY2022 EPS was negatively affected by an outsized loss in forex, which reduced operating income by $18M and EPS by $0.28 in that quarter, skewing the quarterly comparisons.

| (GAAP) |

| Q2 FY2023 (guidance) |

| Q2 FY2022 |

| YoY (midpoint) |

| Revenue |

| $325-355M |

| $377.0M |

| (9.81%) |

| EPS |

| $1.05-1.35 |

| $1.10 |

| 9.09% |

Note that consensus estimates expect IPGP to do somewhat better than the midpoint with GAAP EPS of $1.24 on revenue of $346M. Estimates also project GAAP EPS of $5.23 on revenue of $1.42B by the end of FY2023. In comparison, IPGP earned $5.16 on revenue of $1.46B in FY2021 and $2.16 on revenue of $1.43B in FY2022, but remember that the FY2022 number includes Q4’s $1.91 loss, which was due to several charges as mentioned previously, not to mention all the recent stock buybacks.

Why IPGP finds itself in somewhat of a predicament

There is little if any growth to be found at IPGP and that has been the case for quite some time. Revenue has essentially gone nowhere for years. Worse, gross margin has gradually declined. This has pressured earnings, which has forced IPGP to take countermeasures like spending money on stock buybacks and cutting back on expenses like R&D, which might be concerning for some, especially when dealing with a tech stock.

IPGP is facing several headwinds that have yet to go away. For instance, IPGP faces increased competition in China, IPGP’s biggest market. China still accounted for 29.2% of Q1 revenue, even after sliding by 22% YoY. Still, that share used to be much higher in the past and there is no reason to believe competition is getting any less. On the contrary, Chinese competitors are climbing the food chain and releasing new products that compete against IPGP, which include high-powered fiber lasers China was not known for in the past.

More recently, IPGP has been negatively affected by the war in Ukraine since IPGP used to do a lot of manufacturing in Russia. IPGP has been forced to make changes to its supply chain, but this has led to higher costs and hence lower margins, which explains why gross margin has gone lower and likely to keep getting lower. Worse, gross margin may take a very long time to get back to where it used to be, if ever.

IPGP has tried to offset these headwinds with some positive results. For instance, IPGP has pursued new markets and/or new products. From the Q1 earnings call:

“IPG has been making good progress in diversifying our revenue and reducing our exposure to cyclical and economically sensitive industrial markets. While these markets and applications are still account for a major portion of IPG revenue, we have been investing on our R&D sales and operating resources to support growth of emerging products and to drive further diversification of our revenues.”

A transcript of the Q1 FY2023 earnings call can be found here .

These emerging products seem to have been well received and they are growing as a result, but they have yet to show they can put an end to the stagnation that has taken root at IPGP. There is also no guarantee they won’t slow down in the case of say EV. IPGP is and remains a company with a stagnant top line and a bottom line that needs to be propped up with stock buyback programs and other measures that will be difficult to sustain in the long run.

IPGP is no bargain

There is another reason why some may decide to take a pass on IPGP. Multiples for IPGP are not low enough to convince buyers the time has come to get in on IPGP. IPGP is not necessarily expensive, but in the context of all the other headwinds IPGP has to deal with, it may not be worth the risk.

| IPGP |

| 5-years average |

| Market cap |

| $6.28B |

| - |

| Enterprise value |

| $5.23B |

| - |

| Revenue ("ttm") |

| $1,406.7M |

| - |

| EBITDA |

| $302.0M |

| - |

| Trailing GAAP P/E |

| 65.46 |

| 40.72 |

| Forward GAAP P/E |

| 26.49 |

| 32.18 |

| PEG GAAP |

| N/A |

| N/A |

| P/S |

| 4.67 |

| 5.88 |

| P/B |

| 2.69 |

| 3.21 |

| EV/sales |

| 3.72 |

| 4.97 |

| Trailing EV/EBITDA |

| 17.33 |

| 16.41 |

| Forward EV/EBITDA |

| 13.72 |

| 15.68 |

Source: Seeking Alpha

Investor takeaways

The stock is hot right now, but I would not be a buyer and I remain neutral on IPGP as stated in a previous article . The stock has soared higher in the last two weeks, but this also means IPGP is due for a pullback with the stock overbought. Multiples are such that there is no reason to rush, especially if a better entry point is likely in the near future.

IPGP is making progress in certain areas and that’s worth noting. Emerging growth products like LightWELD are doing well. These products have offset the headwinds IPGP is facing in other areas, at least to a certain degree. If they can keep it up, it’s conceivable to think they could someday be big enough to make the rest fade into irrelevance.

However, that day has yet to come. IPGP is still facing a number of headwinds for which it has yet to find a solution. The top line has remained pretty much stagnant for years. Gross margins have gone down and there is reason to believe they have ways to go before bottoming. In response, IPGP has taken a number of measures to offset the pressure on earnings.

This includes cutting back on R&D and spending cash reserves on stock buybacks. Both have helped with keeping EPS afloat, but neither is sustainable in the long run. On the contrary, both could have less than desirable consequences down the road for IPGP. Some might argue these policies are too heavily weighted towards what is beneficial in the short term, even if they come with good intentions.

Bottom line, an argument can be made for or against long IPGP. Long IPGP is worth considering, especially if one does so for the long term and assuming emerging growth products continue to grow in the coming years. The stock is within the lower end of the range it has traded in for the last five years. It’s still roughly 50% off the highs in early 2021. There is a lot of ground to recover after the long decline the stock went through in the last two years.

Still, not everyone is likely to be onboard with IPGP and there are several reasons people may cite. Whether it is being asked to pay a relatively high multiple for IPGP, higher than most, or the fact that IPGP has struggled to sustain growth for years, there are valid reasons why some may have their doubts about IPGP. If that applies to you, then it may just be better to play it safe by not participating in the current rally.

For further details see:

IPG Photonics Corporation: Could Go Either Way