IQV - IQVIA: I Would Stay Away Until Debt Issues Are Resolved

2023-11-12 06:33:20 ET

Summary

- IQVIA is a global provider of contract research services and data analytics for the healthcare industry. The company helps clients drive healthcare forward by providing insights and solutions to improve.

- The Net Debt/EBITDA ratio is 4.6x, moreover, 55% of its debt is at a floating rate, which is very worrying in an environment with high rates.

- Although the company doesn't seem particularly expensive at its current valuation, I would demand a greater margin of safety until debt concerns are resolved.

Investment Thesis

IQVIA ( IQV ), as a leading company in its sector, provides high-value services to its clients, so it's no wonder that the company has been a great outperformer with respect to the S&P500 in the last decade. However, recent challenges with debt have emerged , indicating that management might have become complacent during a period of nearly zero interest rates. During 2022, the company had to address this by incurring significant amounts of floating rate debt, a move that could impact short-term profits due to elevated interest payments resulting from what appears to be suboptimal management decisions.

This article aims to analyze IQVIA's business model, delve in its debt-related challenges, and conduct a valuation to assess the potential returns for investors at the current stock price. The overarching question is whether these returns can justify the issues stemming from the company's debt situation.

{kind=link}

Business Overview

The company was formed in 2016 through the merger of IMS Health and Quintiles. Nowadays, IQVIA is a global provider of contract research services and specialized data analytics for the healthcare industry. The goal is to help clients drive healthcare forward by providing insights and solutions to improve patient outcomes. IQVIA plays a crucial role in supporting various stakeholders in the healthcare sector, including pharmaceutical companies, biotechnology firms, healthcare providers, and government agencies. It does so by offering data-driven insights, research services, and technology solutions to address complex challenges in the healthcare ecosystem.

Prior to introducing a new medication to the market, it typically undergoes thorough preclinical and clinical testing, along with regulatory scrutiny, to confirm its safety and effectiveness. This process is quite expensive , with an estimated cost ranging from $314 million to $2.8 billion for the approval of a new drug, and it generally spans an average duration of 10 years.

Phases of a New Drug (Cancer Institute NSW)

Hence, smaller and mid-sized companies frequently encounter obstacles when autonomously developing their pharmaceuticals. This is where CRO (Contract Research Organization) like IQVIA become essential, as they possess the capacity to adeptly manage these responsibilities and facilitate the successful advancement through the developmental stages, spanning from Phase I to Phase IV. Two pivotal factors contribute to this proficiency:

- IQVIA well-established professional infrastructure.

- Their expertise in orchestrating these therapeutic trials.

Even large pharmaceutical companies like Pfizer, Novo Nordisk or Gilead can find value in outsourcing these processes, as CROs can provide services at a lower cost than in-house teams. This is particularly beneficial for tasks that are not core to the pharmaceutical company's business and thus they can better focus their efforts and resources.

Revenue Distribution

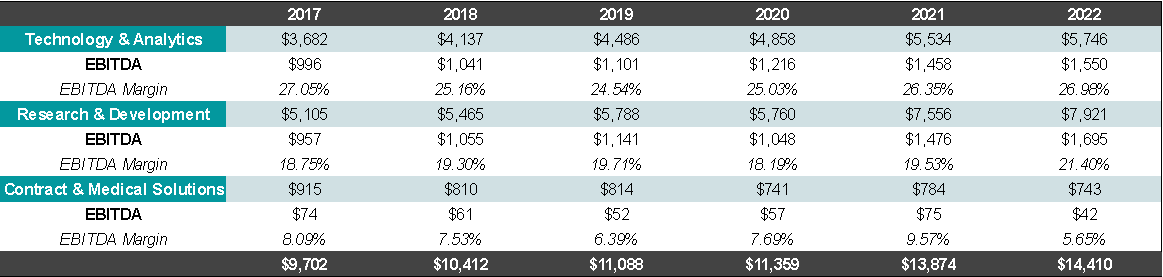

The company categorizes its revenues into three main sources, but I'll focus on two, excluding the Contract Sales & Medical Solutions segment due to its minimal margins, declining revenues, and representing only 5% of total sales.

The primary revenue driver is the Research & Development segment , where the company operates as a Contract Research Organization (CRO), as mentioned earlier. Revenues in this segment have shown a consistent annual growth rate of 9% since FY2017, and EBITDA margins hover around 20%, aligning with competitors like Medpace.

The second significant segment is Technology & Analytics , inherited from the legacy of IMS Health. This appears to be a business with compelling competitive advantages. In this domain, the company provides insights derived from a vast database of over one billion patient medical records sourced from approximately 150,000 medical providers. Revenues have also grown 9% annually, but the margins are somewhat higher, around 25-27%

In an era where data is considered the gold of the 21st Century , IQVIA leverages this extensive information to assist clients in enhancing their clinical and financial performance. The wealth of data enables clients to make informed decisions regarding resource allocation, monitor the safety and efficacy of their products in the long term, and derive various other benefits. Obtaining such comprehensive data independently is challenging for clients and isn't readily available to everyone. Given the years of accumulated studies necessary for reliability, it can be considered that IQVIA possesses a substantial intangible asset in this regard and that is why the Technology & Analytics segment provide a further degree of solidity to a business that was already quite good only with the Research & Development segment.

{kind=link}

Key Ratios

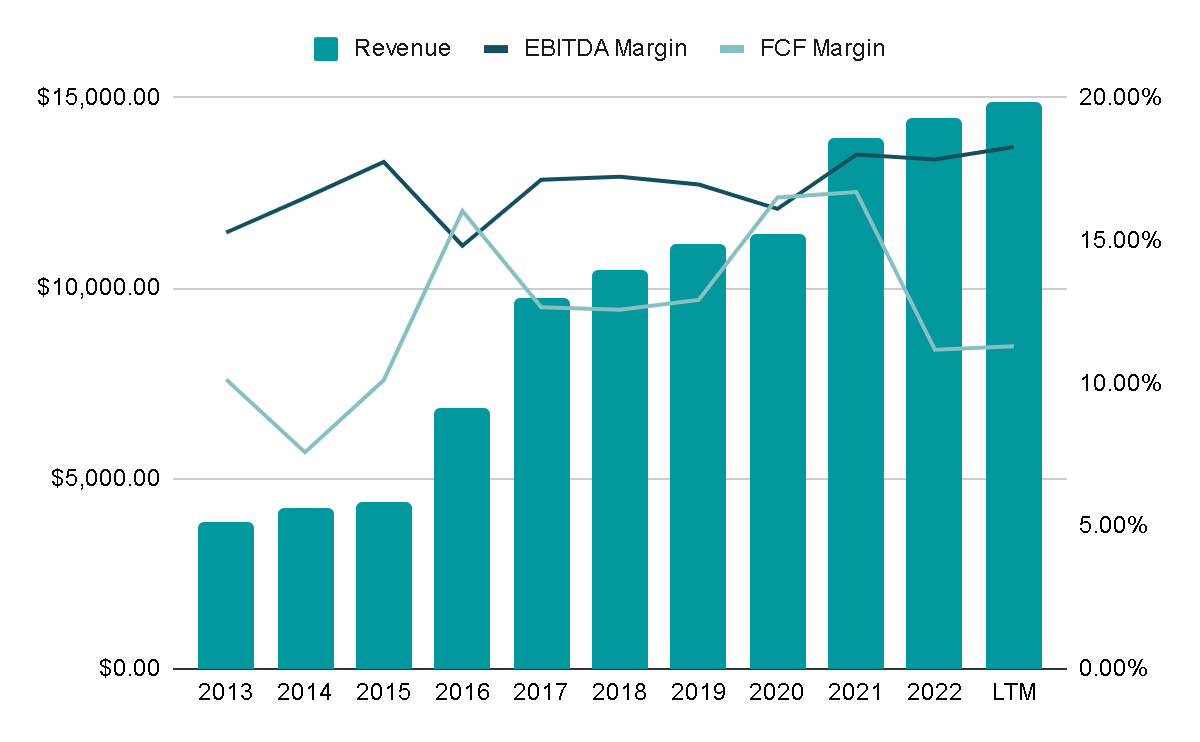

Overall, the company has experienced a remarkable 16% annual revenue growth over the past decade. However, it's important to note that a substantial portion of this growth can be attributed to the merger executed in 2016/2017, and particularly, the benefits realized in 2021 when numerous projects were initiated to develop the COVID-19 vaccine.

When these extraordinary events are excluded, sales have maintained a more moderate growth rate of 5% annually. Despite this, there is a positive trend in increasing margins, with current figures standing at 18% for EBITDA and 11% for Free Cash Flow.

{kind=link}

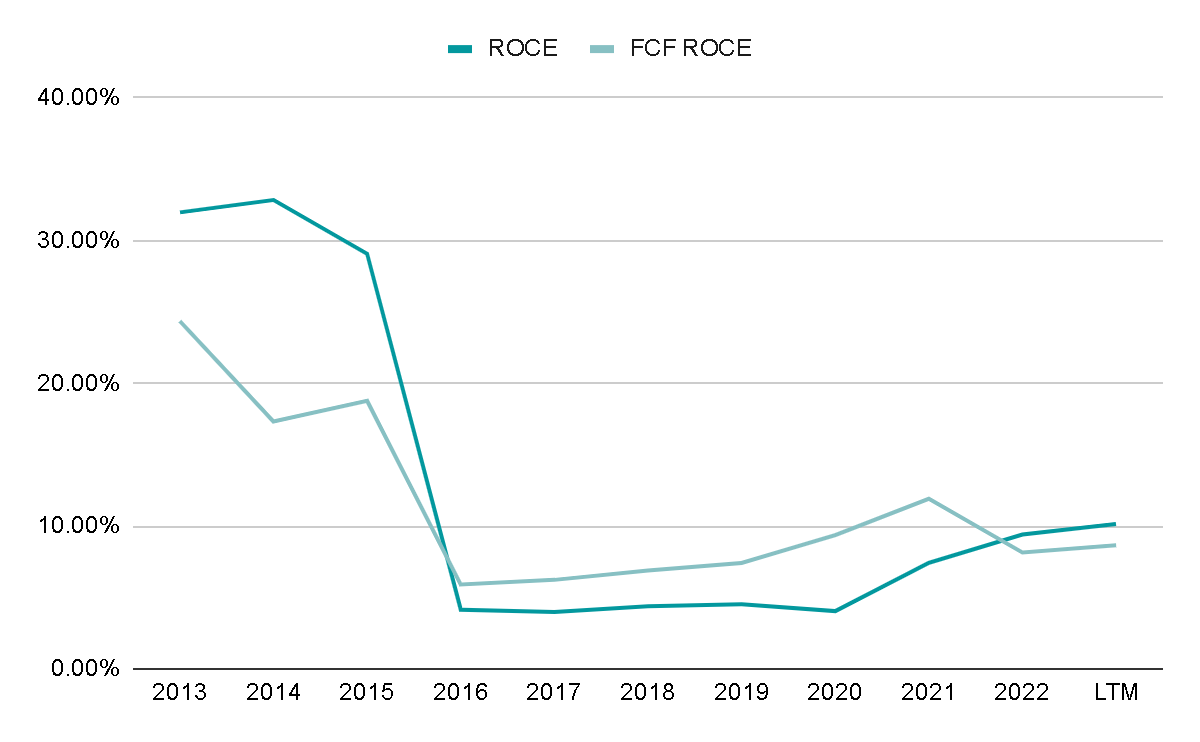

It's interesting to note that despite the perceived qualitative benefits of the merger, since the Technology & Analytics segment is a high-quality business, the company's Return on Capital Employed (ROCE) and Free Cash Flow ROCE experienced a significant decrease post-merger with IMS Health. The ROCE has hovered around 7%, which is notably low. The explanation for this decline appears to be the substantial addition of Goodwill to the company's balance sheet during the merger. If Goodwill is excluded from the ROCE calculation, the figures would be closer to 12%, suggesting that the impact of Goodwill on the balance sheet is a crucial factor influencing the overall return on capital employed and this adjusted metric indicates that operationally the business has better returns than what appears at first glance.

{kind=link}

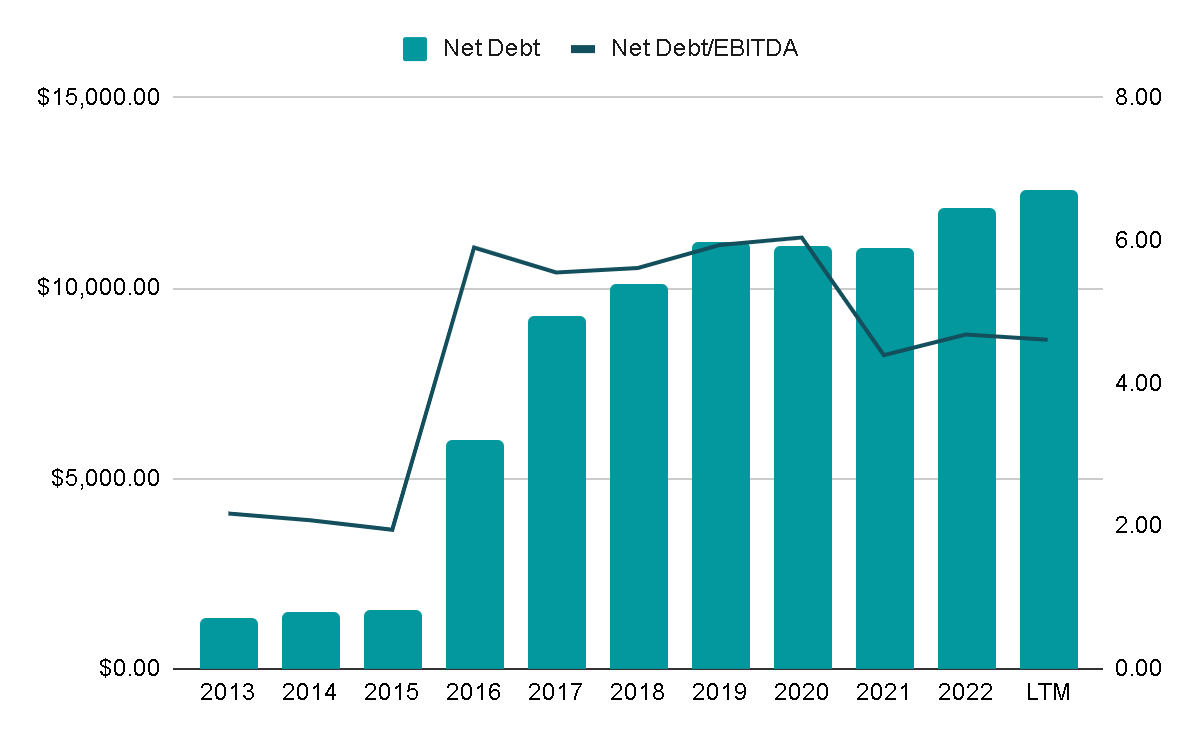

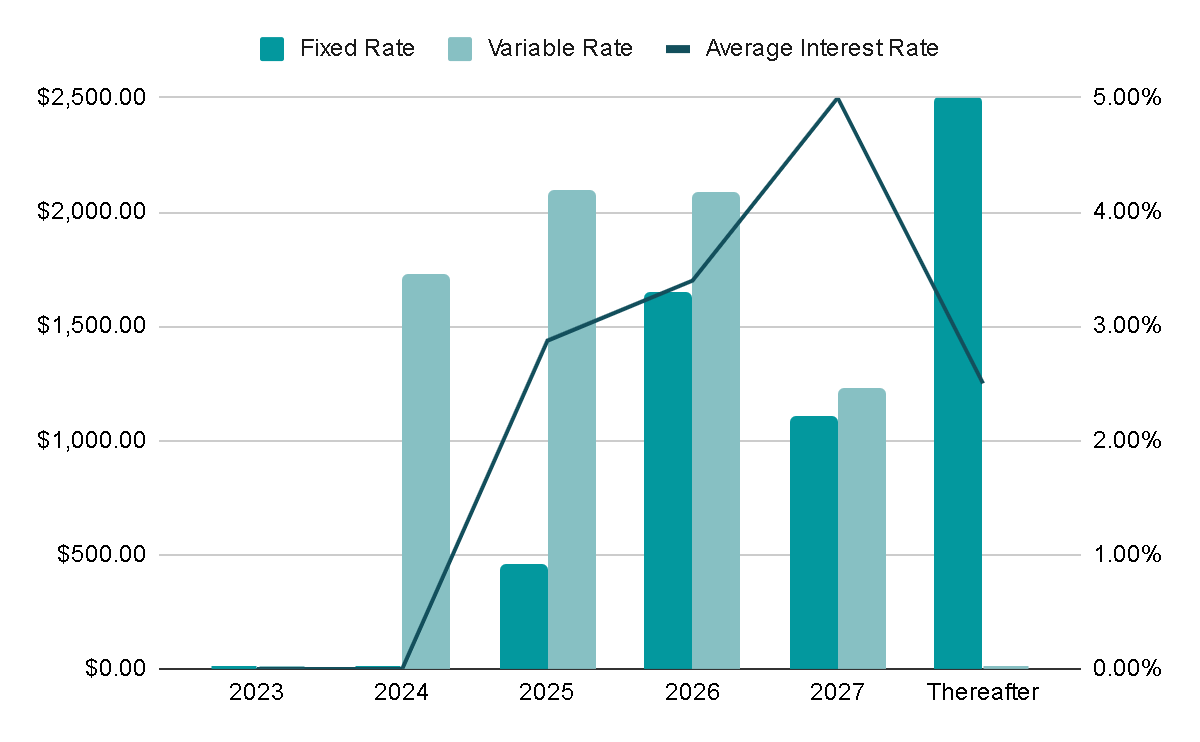

The aspect that raises significant concern and indicates potentially poor capital allocation is the company's debt situation . Presently, the company carries a Net Debt of $12.5 billion, resulting in a Net Debt/EBITDA ratio of 4.6x. This ratio is considerably high and could be deemed as imprudent, especially when considering the current macroeconomic conditions. High debt levels can pose substantial risks, including increased financial vulnerability and challenges in servicing debt obligations, particularly if economic conditions take a downturn or interest rates rise.

{kind=link}

And the situation becomes even worse when we delve into the debt structure: 55% is at a floating rate with maturities between 2024 and 2027. And as for the portion of the debt with a fixed interest rate, this averages 3.45%, so it is not so negative considering that most of it has maturity dates after 2026.

All of the debt issued at a variable rate corresponds to two Term Loans that the company borrowed in October 2022, which shows that management planned the debt terribly and had to desperately issue it at a variable rate at one of the worst times to do so

{kind=link}

Valuation

Now that we have delved into the business model and recognized its significance for clients, along with the high quality of services the company provides, I would like to conduct a valuation to estimate potential returns if we were to purchase at the current price.

Considering historical growth, I suggest projecting a 6% annual growth in Revenues in the coming years, unless there is a substantial acquisition or a one-off event similar to the impact of COVID-19. Additionally, I anticipate a potential 2% annual decline in shares , mirroring past trends. However, this projection is contingent on effective debt management since, as we observed earlier, the company is significantly leveraged, which could impact regular buybacks.

Lastly, I posit that the company can continue enhancing its margins, especially as the "Contract & Medical Solutions" segment, characterized by low margins, diminishes in significance within the overall sales mix, and the company continues to achieve economies of scale. Assuming exit multiples of 15x EBITDA and 20x FCF, based on the business's quality and historical multiples within the company and the sector, we could anticipate an annual return of 9% from the current price in my base case scenario.

{kind=link}

The selection of multiples, such as for EBITDA, was grounded in historical metrics, considering a period when interest rates were not as close to zero as they have been in the last decade. This approach enables us to incorporate the current macroeconomic landscape into the valuation.

However, it's crucial to acknowledge that if interest rates were to revert to those exceptionally low levels, a reevaluation would be necessary. In such a scenario, it might be reasonable to consider paying up to 25x Free Cash Flow if the company's quality still justifies it. Adapting the valuation to changes in interest rates ensures a more dynamic and responsive approach to the ever-evolving economic environment.

{kind=link}

Final Thoughts

Despite the company operating in a resilient sector with characteristics that make it less susceptible to economic downturns, the current valuation doesn't appear compelling. This is particularly concerning considering the company's historical tendency toward slower growth, which may suggest potential market share losses to more rapidly expanding competitors like Medpace , operating in the Research & Development sector with growth rates of ?20%.

Moreover, the capital allocation decisions thus far have been suboptimal, leading to a precarious situation with the accumulation of debt. Monitoring this situation is crucial , as the company needs to navigate its way through until interest rates potentially decrease again, easing the burden of its floating rate debt.

Balancing the positives and negatives, a ' hold ' rating seems most fitting at the moment, providing a cautious stance until there's more clarity on the company's ability to address competitive challenges and manage its financial obligations more effectively.

For further details see:

IQVIA: I Would Stay Away Until Debt Issues Are Resolved