WLK - Is LyondellBasell A Good Dividend Stock To Own?

2023-11-14 16:15:38 ET

Summary

- LyondellBasell Industries has a clear capital allocation strategy of distributing 70% of its free cash flow through dividends and buybacks.

- LYB pays out a significant portion of its free cash flow as dividends, surpassing the average of its peer group by 3x.

- Cash flow conversion levels have been remarkably strong of late, and Q4 could see another strong conversion quarter as working capital commitments could be light.

- While LYB offers a high yield, its current yield is lower than its historical average, and its track record of dividend growth is not as strong as Westlake.

- We close with some thoughts on the technicals and the valuations.

Introduction

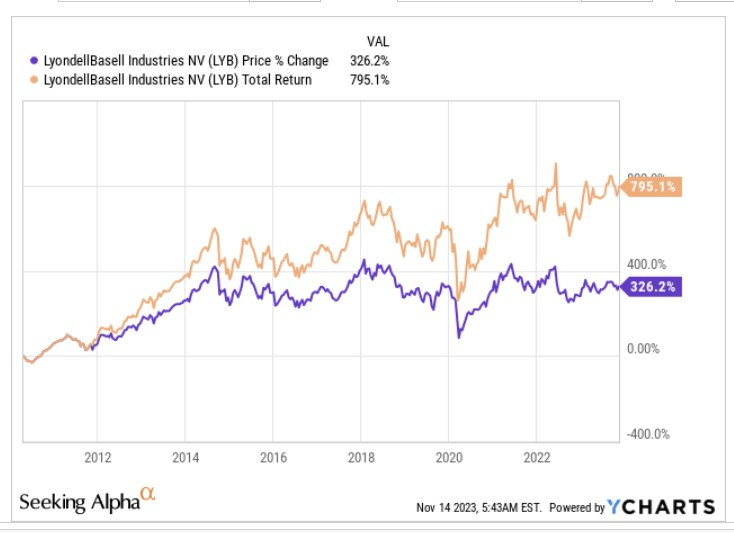

LyondellBasell Industries N.V. ( LYB ) is a global chemical entity that is predominantly noted for its expertise within the petrochemical value chain. Besides this core story, you also have a supplementary dividend sub-plot that has been very instrumental in driving a significant variance between the price return and the total return of the stock.

{kind=link}

So how good is LYB’s dividend profile and is it worth pursuing now? Read on to find out.

Various Components Of The Dividend

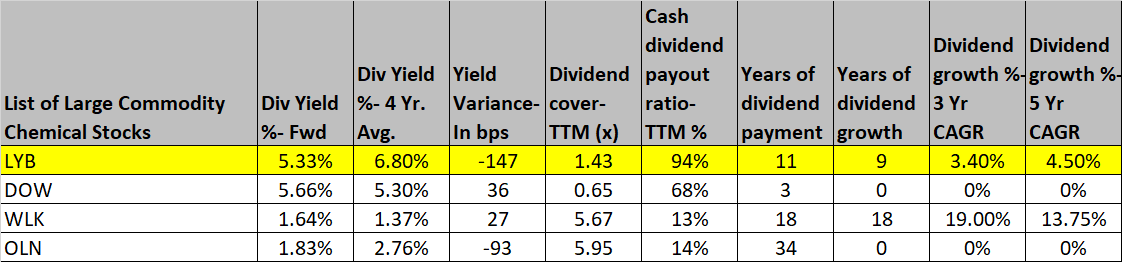

To get a sense of LYB’s dividend prowess, it wouldn’t be appropriate to just focus on one single metric. Rather what we’ve done is measure the stock under four broad dividend themes- the coverage, the yield, the longevity of dividends, and the quantum of growth. Also note that within each theme you have certain sub-metrics. We’ve then measured how LYB stands under all these parameters, relative to the top four commodity chemical stocks (by market-cap). The other three stocks in this study are Dow Inc. ( DOW ), Westlake Corporation ( WLK ), and Olin Corporation ( OLN ).

{kind=link}

A lot of stocks follow half-baked or haphazard dividend policies that oscillate every other year, but LYB should be appreciated for not going down that path, as they’ve laid down a rather clear capital allocation strategy of seeking to distribute 70% of their free cash flow (after accounting for M&A as well) by way of dividends and buybacks. Based on commentary in LYB’s 10-K , it is evident that LYB intends to keep paying quarterly dividends and grow it over time, whilst maintaining a strong investment grade balance sheet.

Now, if one were to look at LYB’s dividend cover ((TTM)) of 1.4x, it’d be hard to get too excited, particularly when you consider that the trailing EPS of the likes of Westlake and Olin are currently covering their dividends by 5-6x. However, we feel that the dividend cover can often be skewed by one-off or non-cash items, and we think the more appropriate gauge is to see how much of free cash flow gets distributed via dividends.

As noted earlier LYB has a target of distributing 70% of its FCF by way of dividends and buybacks, but the latest data shows that it is currently paying out a whopping 94% of its FCF by way of dividends alone! The comfortably trounces the peer set average by 3x.

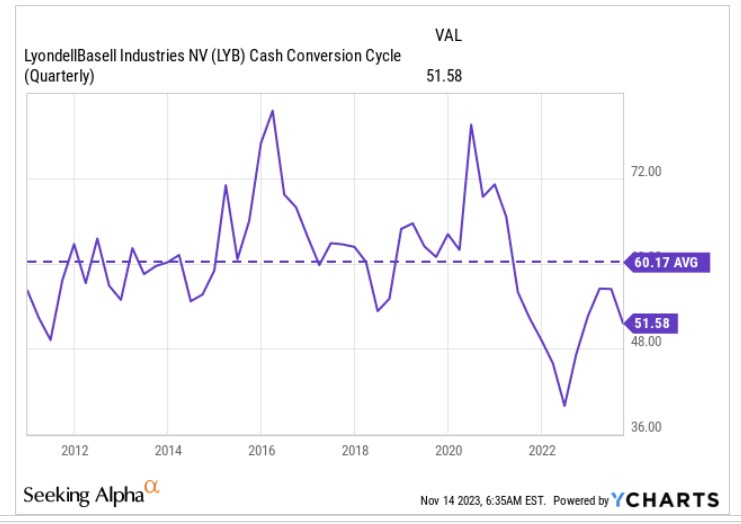

Yes, LYB pays out an inordinate share of its FCF as dividends, but is it doing a good job with cash flow generation? We believe so, and you can get a sense of this with the EBITDA to operating cash flow conversion ratio in three out of the last four quarters (the Q1 ratio was a one-off as the company resorted to generating additional inventory ahead of maintenance shutdowns).

Earnings call transcripts

On average what we can see is that this is a business that typically converts well over 100% of its EBITDA to operating cash flow. For this to happen, the business needs to be running a tight ship with working capital, and we can see how that has meaningfully improved in recent years.

On average cash gets locked up with working capital for 60 days but in recent periods it has been hovering at the lower half of the chart, highlighting the degree of improvements seen here. With softness expected in some end markets in Q4 and some maintenance shutdowns, we believe working capital is unlikely to be a source of encumbrance in Q4 as well.

{kind=link}

On the yield front, a lot of passive observers of LYB will be pleased to discover a rather enticing figure of 5.33% (LYB is part of the esteemed dividend dogs portfolio ), and whilst it is up there with DOW’s corresponding figure, some additional context is required. I think it’s also important to see how the current yield stacks up against the historical average (4-year average), and here note that LYB fares rather poorly as its current yield is a good 147bps lower than what you’d normally get.

We then move on to the track record of dividend payments, and typically we find that a longer track record usually means a lower probability of the dividend being cut. Here LYB’s track record of 11 years is below average. Some investors may not be too enthused to just receive flat dividends year in and year out, and that's what an OLIN offers you with no growth whatsoever. In that regard LYB deserves credit for growing its dividends for nine straight years, and by ~3% over the short-term and 4.5% over the medium-term. However, that dividend growth track record is still nothing compared to what Westlake Corporation has delivered; 18 years of growing its dividends with tremendous double-digit growth rates over a 3-year and 5-year span.

In summary, LYB’s dividend profile may not necessarily be the best, but it certainly has its strengths and should not be scoffed at.

Closing Thoughts- Other Considerations

Despite a relatively competent all-round dividend profile, we are conflicted about whether a long position in LYB would be too conducive right now. Here’s what’s driving our neutral positioning on the stock. We’ll start with what we like.

{kind=link}

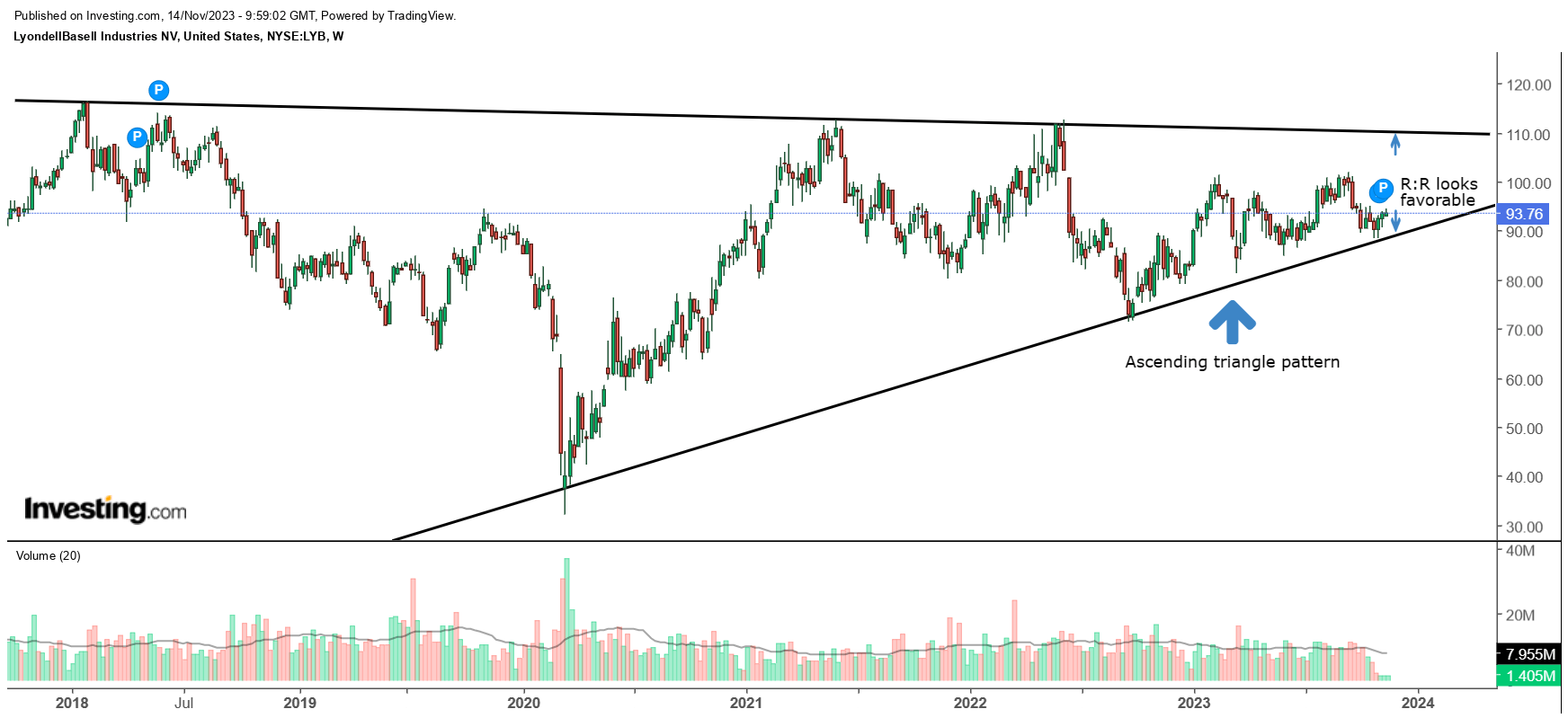

Those who pursued LYB in the pre-pandemic years are unlikely to be too pleased with it, as the stock hasn’t quite been able to take out its 2018 highs despite a couple of attempts in 2021 and 2022. Whilst LYB may not be delivering the highs, do also note that the downside support keeps getting scaled up over time; all in all, what you have is something similar to the ascending triangle pattern .

That’s also why we feel that if you’re looking at LYB as a trading play, the current reward-to-risk dynamics look quite encouraging with the stock not too far off from its upward-sloping support line. Eventually the $110-$112 resistance levels may give away, but even if that doesn’t quite happen, you still have a decent amount of runway to get involved in (if you get it now), and potentially trim your positions as you get closer to the upper boundary of the triangle.

{kind=link}

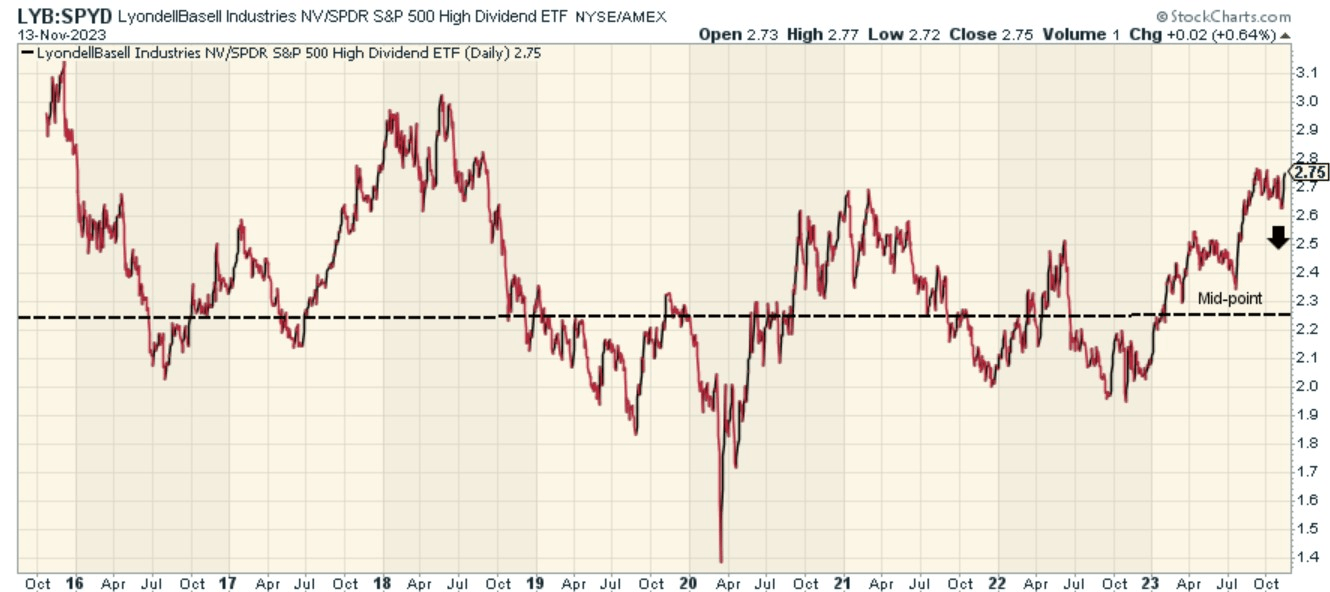

Whilst developments on the standalone chart of LYB look encouraging, we can’t say the same for the relative strength chart which measures LYB’s positioning versus its high-yielding contemporaries from the S&P500.

You ideally want to get into LYB when the ratio is perched towards the lower end of the chart, like it was in 2020, or even a year ago, but right now, LYD looks quite overbought compared to its peers from this portfolio.

Then one also ought to consider that the near-term outlook isn’t the rosiest. LYB will likely deliver a weak Q4 as multiple cogs of the business experience seasonal weakness, particularly the European portfolio. There will also be some planned maintenance activities in a few plants which will prevent the company from operating at full tilt.

{kind=link}

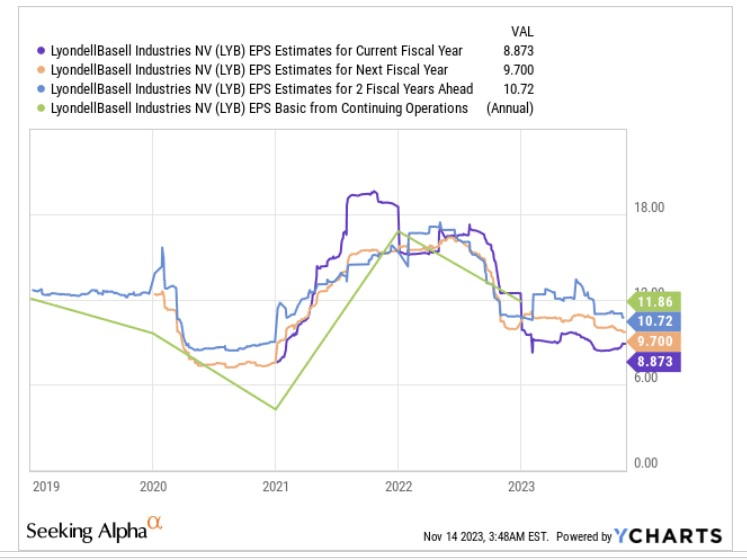

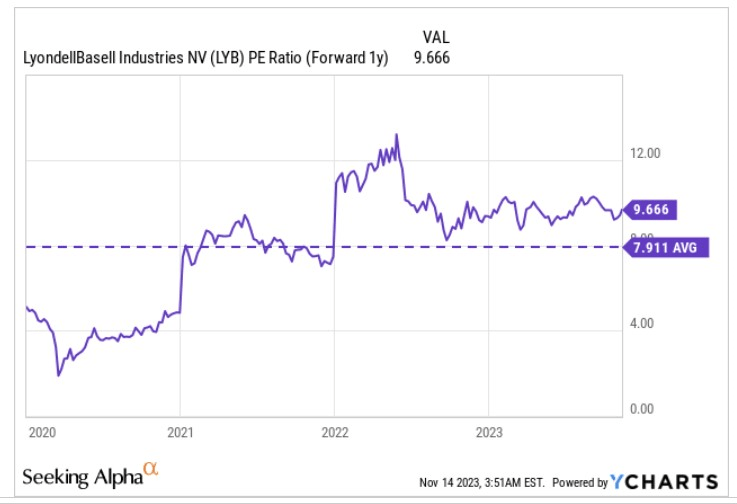

LYB is also contemplating exiting certain businesses and that won’t reflect well on the earnings cadence. If one looks at how consensus estimates are positioned through the next few years, it’s hard to get too excited. Whilst EPS growth should pick up in FY24 and FY25, the eventual number in FY25 will still likely be 10% short of the FY22 reported EPS of $11.86. With an underwhelming EPS trajectory of this sort, one can’t be jumping for joy to discover that the stock is currently priced at almost 10x forward P/E, a 22% premium over its 5-year average.

{kind=link}

Thus, to conclude, we think LYB has a decent dividend profile, but we have our conflicts over whether this is the best time to own the stock.

For further details see:

Is LyondellBasell A Good Dividend Stock To Own?