SPTI - It's Still All About Interest Rates And The U.S. Economic Data

2023-10-02 05:07:00 ET

Summary

- Anytime during the trading day in the last few weeks, when the 10-year Treasury yield moved to multi-year highs, the dollar strengthened and stocks got wobbly.

- In early September ’23, the JOLTS report put a temporary bid under the Treasury market as the JOLTS number showed a sharp drop in corporation job openings, which was ultimately supported by a weaker August ’23 non-farm payroll report.

- The US economy needs to see a weaker labor force and weaker economic data to have any hope of seeing inflation get down to 2%.

Anytime during the trading day in the last few weeks, when the 10-year Treasury yield moved to multi-year highs, the dollar strengthened and stocks got wobbly.

I don’t really have an opinion on crude oil other than it seems like the price of gasoline is still awfully high given the number of Teslas ( TSLA ) on the road. Yes, I know there hasn’t been a new gasoline distillation facility opened in years. After reading a piece from the IEA (Int’l Energy Agency) in 2011-2012, noting that gasoline distillation accounted for about half of the demand for US crude oil, and even noting back then there were more and more Teslas on the north side of Chicago streets, the energy sector was never bought for any client, in other than small amounts, for short-term trades.

The obvious question I don’t hear discussed is what number of Teslas on US roads will it eventually take to permanently reduce US gasoline demand.

Labor Force Update this week:

In early September ’23, the JOLTS report put a temporary bid under the Treasury market as the JOLTS number showed a sharp drop in corporation job openings, which was ultimately supported by a weaker August ’23 non-farm payroll report. However, the weekly jobless claims, which do get some attention, are still pretty strong and ended the month of September closer to 200,000, which always makes bond investors nervous.

On Friday morning, October 6th, the September ’23 nonfarm payroll report will be released, with Briefing.com consensus expecting 155k-165k overall and private sector payroll expecting 150k-155k. August overall nonfarm payroll growth was 187k, but that’s before revisions.

The August revisions amounted to almost 100,000 jobs removed from the June and July reports, so revisions matter too.

You’ve also got ADP in there on Wednesday morning.

The one shoe left to fall is the generally heightened levels of US economic growth despite a 525 bp increase in the fed funds rate.

Two really interesting Treasury/bond market charts:

{kind=link}

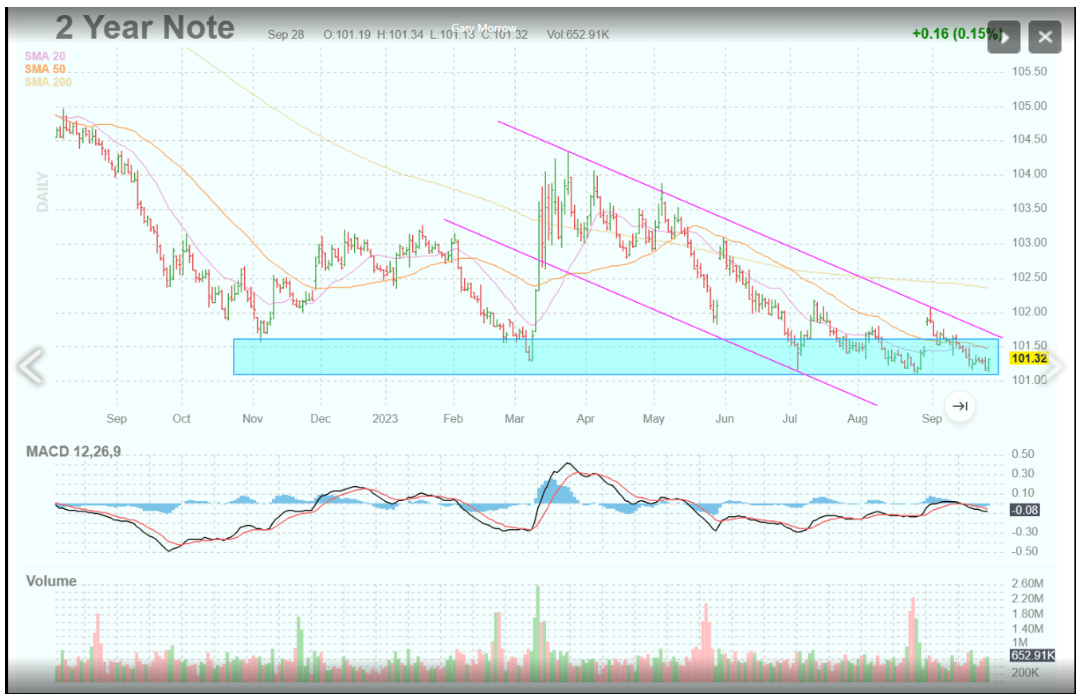

As readers know, Trinity uses a very good technician - Gary Morrow (@Garysmorrow) to provide me with opinions on key holdings and market happenings. Gary is a former CME trader, from way back in the day, and is very good at what he does.

Morrow thinks the TLT (first chart above) could be ready for a decent rally. Could happen this week with weak jobs data.

{kind=link}

{kind=link}

The other interesting comment Morrow had post the Fed meeting bearishness is that the 2-year Treasury did not take out the August ’23 lows (the chart immediately above this paragraph) as 5s, 10s, and 30s did following the very bearish reaction to the Jay Powell’s post-Fed meeting statement and presser.

This may be why there is a sudden burst of discussions around the yield curve steepening.

Potential Targets for the 10-year Treasury Yield:

- 4.33% was the October ’22 high print for the 10-year Treasury yield in 2022;

- 4.66% was the next yield target and that was hit last week. (Not sure where the 4.66% level came from; presume it was some or a group of technicians' target yield);

- 5% is the next target rate heard more frequently;

- A 6% 10-year Treasury yield is the rate Rick Rieder, BlackRock’s bond head, has been talking about of late;

- 7% is the rate Jamie Dimon thinks the 10-year Treasury will eventually peak at - Jamie is still pretty bearish, which fits with his “economic hurricane” comments made in early 2022;

Thankfully, for readers, I offer no opinion on this and am simply waiting for the US economic data to weaken.

Muni bond closed-end funds:

Way back in 1994, while sitting on a bond desk, and then again in 2013, with the Detroit bankruptcy, I often heard about muni closed-end funds (CEFs) selling at very steep discounts to NAV (net asset value). With the sharp rise in the fed funds rate, the last 18 months, although I just might not be seeing the research, I’ve heard almost nothing about muni closed-end funds.

A few clients currently have a long position in Nuveen’s Municipal Value Fund ( NUV ), which carries just 1% leverage, hence it only trades at a 7% discount to NAV, but that’s a bigger discount to its 3-year discount of 1% and 6-month discount of -6.43%, and has a current distribution rate of over 4% (per Morningstar’s website). Perusing Nuveen’s closed-end fund website, there are huge discounts to NAV for those CEFs with high leverage (i.e. preferred stock) but you’ve got the risk that accompanies the potential reward.

BlackRock ( BLK ) is another big issuer of muni closed-end funds, and the BlackRock MuniHoldings ( MUE ) CEF is trading at a 17% discount to NAV, with 33% leverage. Like Nuveen’s NUV, the MUE is a bond portfolio of high credit quality.

The only reason this is brought to readers' attention is that there could be some real pain in this asset class over the next few weeks and months, so do your homework now and see where you might find value. Do the homework now and identify what you might like to own, and then wait for the Fed/Jay Powell to give you the signal that Fed funds rate reductions are coming.

As of this weekend, there is an 86% chance the Fed/FOMC maintains the 5.25%-5.50% fed funds rate at the November 1st meeting and just a 13%-14% chance (as of today) of a 25 bp hike.

Let’s see what the CME FedWatch Tool says after the Friday, September ’23, jobs report and the JOLTS report this week.

Summary/conclusion:

The one persistent condition since the FOMC started raising interest rates in March ’22 is that the US economy has ignored all prognostications for a US recession - even after Silicon Valley Bank ( SIVBQ ) - and has continued to generate consistent +2%-3% GDP growth despite the interest rate shock to the US economy.

Personally, I’m just waiting for the data to soften, and then see if it warrants a change to bond portfolios. It’s still “stocks over bonds” in most accounts since the 2000-2009 decade for stocks was the worst since the 1930s. I don't think the S&P 500 will generate a worse annual return after last year’s -18% for a while but don’t bet the farm on that. The bond market is the issue, and after 10 years of zero interest rates, that 10-year Treasury yield could misbehave for most of the decade.

The US economy needs to see a weaker labor force and weaker economic data to have any hope of seeing inflation get down to 2%.

Take everything above with substantial skepticism, and a healthy grain of salt. Nothing here is to be construed as a recommendation or advice - do your own homework - and past performance is no guarantee of future results. All S&P 500 earnings data is typically sourced from IBES data by Refinitiv unless otherwise noted. Readers should gauge their own sentiment to market volatility and adjust their investments accordingly.

Thanks for reading.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

It's Still All About Interest Rates And The U.S. Economic Data