TD - It's The Best Time In 3 Years To Buy Canadian Banks

2023-09-14 07:15:00 ET

Summary

- Certain value stocks, including REITs, utilities, and particular financials, have suffered in recent months.

- Canadian banks are ranked among the safest banks in the world and have not cut their dividends in nearly 200 years. These are the most dependable dividend stocks on earth.

- The current bear market in Canadian banks presents a buying opportunity with attractive yields and solid long-term growth prospects.

- Canadian bank yields are 4.5% to 6.7%, the highest in over 3 years. One of them has a yield approaching Pandemic highs, completely not justified by solid fundamentals.

- Three Canadian banks offer 20% annual return potential through 2025, 3X better than the S&P 500. The others offer 15% to 17% annual return potential, with AA-quality, including the single safest bank on earth not owned by a government.

Certain value stocks, including real estate investment trusts ("REITs"), utilities, and particular financials, have suffered in recent months.

This highlights that it's always and forever a market of stocks, not a stock market.

{kind=link}

Some of the world's most legendary and dependable high-yield stocks are down 34% from record highs! For these companies, the bear market of 2022 never ended.

Be greedy when others are fearful and fearful when others are greedy." - Warren Buffett.

"Templeton concedes that when people say things are different , 20 percent of the time they are right." - Howard Marks.

Is the current bear market in Canadian Banks a sign of something wrong with this legendary high-yield institution?

{kind=link}

Is A Canadian housing crisis about to bankrupt Canada's banks?

Or is it simply a fantastic opportunity to buy world-beater quality and safety in a high-yield package offering yields as high as 6.6%?

Several people have asked me to review Canadian banks to highlight the best opportunities and possibly warn about storm clouds potentially coming over the horizon.

How Fair The Canadian Banks?

Each year, Global Finance Magazine uses rating agency ratings to rank the world's safest banks. And every year, Canada's big five are in the top 50, a list dominated by government-owned banks with AAA ratings because those governments can print infinite money.

In other words, even among "risk-free" banks, Canada's big five stand out.

Global Finance Magazine Global Finance Magazine

{kind=link}

{kind=link}

Excluding ten banks owned by European governments that will never fail, barring the apocalypse:

- The Royal Bank of Canada (RY) is the safest bank on earth

- The Toronto-Dominion Bank (TD) is the 10th safest

- The Bank of Nova Scotia (BNS) 16th

- Bank of Montreal (BMO) 17th

- Canadian Imperial Bank of Commerce (CM) 19th.

So, among banks investors can own, Canada's legendary banks remain the platinum standard. And among North American banks? There is no contest.

{kind=link}

Among North America's safest ten banks, Canada takes the top six, with the National Bank of Canada (NTIOF), the largest regional bank in Canada, rounding out the big 6.

Canada's banking regulation is so good that it hasn't had a banking crisis since the 1840s.

How many bank failures has Canada had since the 1840s? Zero, including during the Great Depression when 9,000 banks failed in the U.S.

- Canada did have one bank fail due to fraud in the last 180 years.

This banking safety isn't just due to regulators imposing higher capital requirements and creating a regulated oligopoly business model.

- the big 5 control 90% of Canadian market share

- no foreign bank is allowed to buy them

- they are not allowed to merge

- they are essentially a national banking utility consortium.

Canada's banks are permitted higher profitability in exchange for a symbiotic relationship with regulators that ensures what today is known to be common sense banking practices.

- like making conservative mortgages that banks have to own on their books

- instead of selling all of it onto some sucker like US banks did before the GFC.

Legendary Risk Management Across Their Entire Business

The DK risk rating is based on the global percentile of a company's risk management compared to 8,000 S&P-rated companies covering 90% of the world's market cap.

ENB scores 96th Percentile On Global Long-Term Risk Management

S&P's risk management scores factor in things like:

- supply chain management

- crisis management

- cyber-security

- privacy protection

- efficiency

- R&D efficiency

- innovation management

- labor relations

- talent retention

- worker training/skills improvement

- Occupational health & safety

- customer relationship management

- business ethics

- climate strategy adaptation

- sustainable agricultural practices

- corporate governance

- brand management

- Interest rate risk management.

How do Canadian Banks rank on complete long-term risk management?

| Classification |

| S&P LT Risk-Management Global Percentile |

| Risk-Management Interpretation |

| Risk-Management Rating |

| BTI, ILMN, SIEGY, SPGI, WM, CI, CSCO, WMB, SAP, CL |

| 100 |

| Exceptional (Top 80 companies in the world) |

| Very Low Risk |

| Toronto-Dominion |

| 96 |

| Exceptional |

| Very Low Risk |

| Bank of Montreal |

| 94 |

| Exceptional |

| Very Low Risk |

| Scotiabank |

| 92 |

| Exceptional |

| Very Low Risk |

| Royal Bank of Canada |

| 91 |

| Exceptional |

| Very Low Risk |

| Canadian Imperial |

| 87 |

| Very Good (Bordering on exceptional) |

| Very Low Risk |

| Strong ESG Stocks |

| 86 |

| Very Good |

| Very Low Risk |

| Foreign Dividend Stocks |

| 77 |

| Good, Bordering On Very Good |

| Low Risk |

| Ultra SWANs |

| 74 |

| Good |

| Low Risk |

| Dividend Aristocrats |

| 67 |

| Above-Average (Bordering On Good) |

| Low Risk |

| Low Volatility Stocks |

| 65 |

| Above-Average |

| Low Risk |

| Master List average |

| 61 |

| Above-Average |

| Low Risk |

| Dividend Kings |

| 60 |

| Above-Average |

| Low Risk |

| Hyper-Growth stocks |

| 59 |

| Average, Bordering On Above-Average |

| Medium Risk |

| Dividend Champions |

| 55 |

| Average |

| Medium Risk |

| Monthly Dividend Stocks |

| 41 |

| Average |

| Medium Risk |

(Source: DK Research Terminal.)

On over 1,000 metrics, the most comprehensive risk management model I've ever seen, the basis for every S&P credit rating of the last 20 years, the Canadian banks are a paragon of sound and prudent long-term risk management.

Safe Dividends: The Ultimate Canadian Tradition

Canada's big six have never cut their dividends , ever.

And during the Great Recession, regulators froze all bank dividends, but none were cut.

To showcase the legendary dependability of Canadian Banks, consider their uninterrupted dividend streaks.

How often have they stopped paying quarterly dividends to investors? Ben Graham considered 20+ years of uninterrupted dividends an important sign of quality.

- Bank of Montreal 194-year streak (since 1829)

- Scotiabank 190-year

- Toronto-Dominion 166 years

- Canadian Imperial 155 years (has never cut its dividend)

- Royal Bank 153 years.

Almost two centuries without missing a dividend and never cutting it? The day Canada's banks cut their dividends is the day the world has ended; the living envy the dead, and money no longer matters;)

The Best Canadian Banks To Buy Today: The Answer May Surprise You

Everyone has different goals, but the #1 priority for Canadian bank investors is safe yield.

Dividend Kings Zen Research Terminal

{kind=link}

- Bank of Nova Scotia

- Canadian Imperial Bank of Commerce

- Bank of Montreal

- Toronto-Dominion

- Royal Bank of Canada

For near-perfect safety, a 5.6% yield for the big five is very attractive.

BNS at 6.7% offers the best yield, though Canadian Imperial is slightly undervalued at a 30% discount.

Overall, you can't go wrong with any of these. Here is the updated long-term return potential (I didn't have time to wait 15 minutes for the update to go through).

| Investment Strategy |

| Yield |

| LT Consensus Growth |

| LT Consensus Total Return Potential |

| Long-Term Risk-Adjusted Expected Return |

| Schwab US Dividend Equity ETF |

| 3.5% |

| 9.70% |

| 13.2% |

| 9.2% |

| Nasdaq |

| 0.8% |

| 11.2% |

| 12.0% |

| 8.4% |

| REITs |

| 4.6% |

| 7.0% |

| 11.6% |

| 8.1% |

| Vanguard Dividend Appreciation ETF |

| 1.9% |

| 9.7% |

| 11.6% |

| 8.1% |

| Toronto-Dominion |

| 4.8% |

| 6.40% |

| 11.2% |

| 7.8% |

| Dividend Champions |

| 2.6% |

| 8.1% |

| 10.7% |

| 7.5% |

| Bank of Montreal |

| 5.2% |

| 5.3% |

| 10.5% |

| 7.4% |

| Dividend Aristocrats |

| 1.9% |

| 8.5% |

| 10.4% |

| 7.3% |

| Canadian Imperial Bank of Commerce |

| 6.6% |

| 3.6% |

| 10.2% |

| 7.1% |

| Scotiabank |

| 6.7% |

| 3.2% |

| 9.9% |

| 6.9% |

| S&P 500 |

| 1.4% |

| 8.5% |

| 9.9% |

| 6.9% |

| Royal Bank of Canada |

| 4.5% |

| 5.0% |

| 9.5% |

| 6.7% |

| 60/40 Retirement Portfolio |

| 2.1% |

| 5.1% |

| 7.2% |

| 5.0% |

(Source: FactSet, Morningstar.)

Scotia Bank offers the best yield but long-term S&P-like like-return potential.

Toronto-Dominion offers the best long-term return potential, though not as good as other dividend growth opportunities like SCHD.

2025 Consensus Total Return Potential

- if and only if all companies grow as analysts expect

- and if and only if return to historical market-determined fair value

- This is how much you'll make by the end of 2025.

Bank of Nova Scotia

{kind=link}

Canadian Imperial Bank of Commerce

{kind=link}

Bank of Montreal

{kind=link}

Toronto-Dominion

{kind=link}

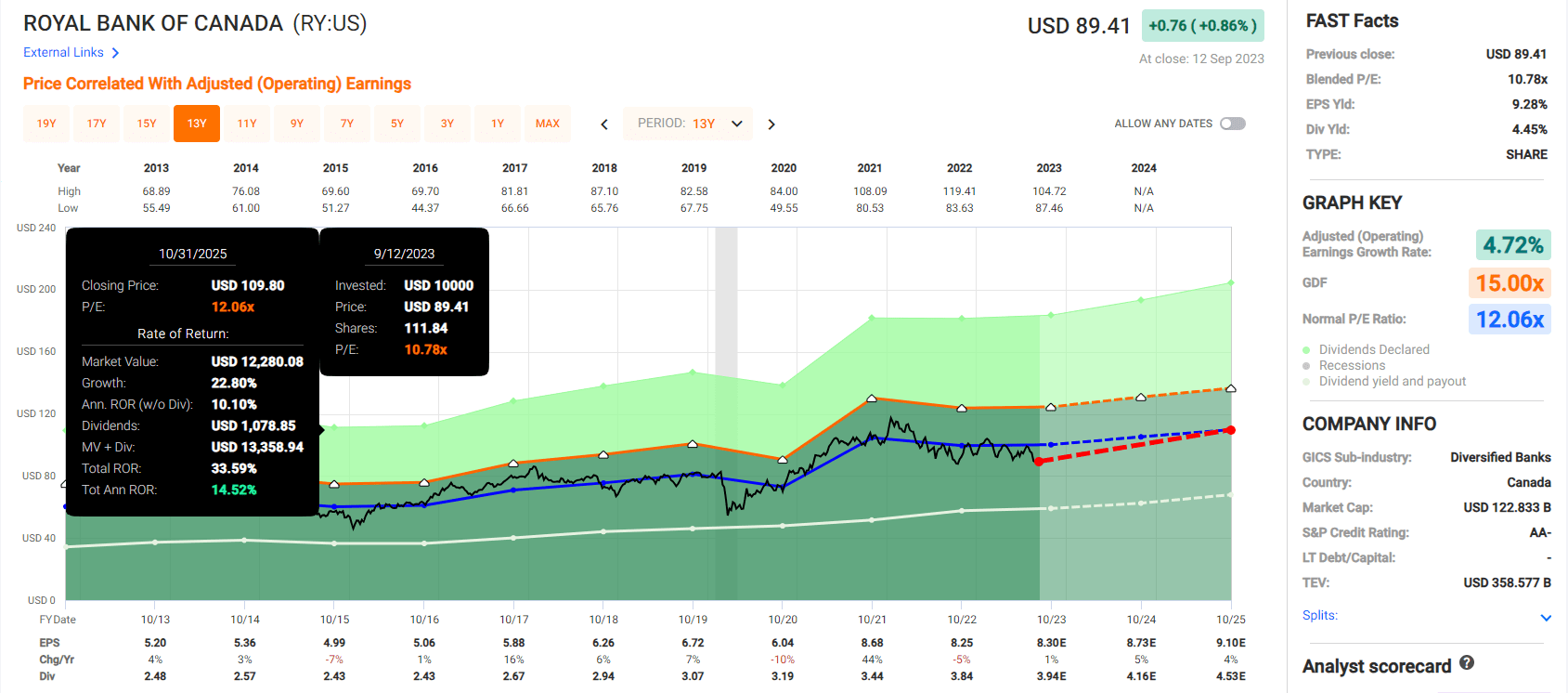

Royal Bank of Canada

{kind=link}

S&P 500

{kind=link}

Bottom Line: It's The Best Time In 3 Years To Buy Some Canadian Banks

{kind=link}

BNS's yield is at its highest in over three years. It wasn't that much higher in the Pandemic.

I can guarantee you the economy isn't about to get locked down and fall almost 10% in a single quarter.

There is nothing in the data or analyst reports that might justify BNS trading at a yield of almost 7%.

Bank of Nova Scotia Earnings: Results Starting To Improve

Narrow-moat-rated Bank of Nova Scotia reported improving fiscal third-quarter results. Expenses were roughly flat sequentially, better than the previous trend of increases, and revenue grew sequentially, driven by fees and net interest income. Not all Canadian banks have increased their NII in the current quarter, so we view this as a positive sign. With results coming in as we expected, we will maintain our fair value estimate. We await an updated strategy refresh for the bank, which will likely result in additional repositioning charges and new operational targets, so the next chapter for Scotiabank is still in its early stages." - Morningstar.

Is there anything going on with the bank to justify this yield? The strategy review ending soon will eliminate uncertainty and likely cause BNS to fly higher.

Here's what the data is saying to me.

Management, analysts, rating agencies, and the bond market all agree, the Canadian banks are doing fine and this is a wonderful buying opportunity.

I can say with 80% confidence, the Templeton/Marks certainty limit on Wall Street, that anyone buying these banks today will be very happy in 5+ years.

In one year? It's a crap shoot.

In 5+ years? It's fundamentals-driven destiny.

And for the most dependable dividend payers on earth, with very safe yields of 4.5% to 6.7%, and solid long-term growth prospects, I am bullish on Canadian banks right now.

For further details see:

It's The Best Time In 3 Years To Buy Canadian Banks