UNCRY - Italian Windfall Tax: The Impact On Intesa And UniCredit

2023-08-10 11:36:45 ET

Summary

- Italian banks face a windfall tax on extra profits from rising interest rates.

- The tax will be 40% on profits from net interest margin (NIM) in 2022 or 2023.

- Strong results and upgraded profit outlooks for Italian banks due to higher rates may be impacted by the tax.

- We'll see what the real impact of the tax on Intesa Sanpaolo and UniCredit could be, considering in particular if the dividend will be hurt.

Introduction

Another windfall tax on extra profits. After the big oil majors, major banks are now the target.

In the night of Aug. 7, 2023, the Italian government announced it will apply a windfall tax on the extra profits the Italian banks are earning thanks to rising interest rates.

As a consequence, the whole Italian banking sector, which over the past year is up 50% vs. the 20% gains made by the European banking sector, is tanking, with the two main Italian banks bleeding: Intesa Sanpaolo ( ISNPY ) is down 8%, and UniCredit ( UNCRY ) losing more than 5%. At the time of writing, two days later, there's a little rebound, but still not strong enough to offset this drop.

What's the impact of this new tax? How will shareholders be affected by it? In this article, I will give my take based on the available data.

The tax

As reported by the media , Italy will apply, only in 2023 and to be paid by June 30, 2024, a 40% tax on profits coming from net interest margin, which is the income coming from the spread between lending and deposit rates. Under this tax, 40% of the NIM earned by Italian banks in 2022 or 2023 (depending on the bigger sum between the two). The law has been approved by the government, but it has to be voted by the Parliament. Therefore, we don't have yet a final draft. However, it seems likely that there will be two thresholds set to trigger the tax: 5% for 2022 and 10% for 2023. This means that if banks had a NIM growth above 5% in 2022, the income made above this threshold will see a 40% tax withdrawal. The levy is a one-off, as stated by the government. It's estimated to give almost €5 billion to the state.

Immediately, many reactions considered this tax to come out of the blue and there were mixed reactions between the surprise of seeing the supposedly "bad guys" - aka, the banks - finally paying a part of their profits and the worries that this act could actually backfire and generate further chaos.

As a result, after a whole day of debate, on the night of Aug. 8, 2023, the Italian Department of The Treasury issued a note giving some reassuring detail on this tax. Here's the translation of the note:

The measure proposed by the Minister of Economy and Finance, shared and approved by the Council of Ministers, comes in the wake of existing regulations in Europe on bank extra margins. At the same time, the measure, for the purpose of safeguarding the stability of banking institutions, also provides a ceiling for the contribution, which cannot exceed 0.1 percent of total assets. In this regard, it is recalled that the taxable base of this tax is determined by the greater value between the amount of the interest margin under item 30 of the income statement, prepared in accordance with the formats approved by the Bank of Italy, relating to the year prior to the year ending Jan. 1, 2023, that exceeds the same margin by at least 5 percent in the year prior to the year ending Jan. 1, 2022, and the amount of the interest margin under item 30 of the income statement prepared in accordance with the formats approved by the Bank of Italy, relating to the fiscal year prior to the one in progress on Jan. 1, 2024, that exceeds the same margin by at least 10 percent in the fiscal year prior to the one in progress on Jan. 1, 2022. Finally, it is noted that banking institutions that have already adjusted rates on deposits as recommended last Feb. 15 in a specific note from Bankitalia, a recommendation later recalled by Minister Giorgetti at the ABI assembly last July 5, will not have significant impacts as a result of the law approved yesterday.

So, it seems that the situation has become a little clearer, enabling us to do some math and understand the real impact of this measure on Italian banks. In this article we will only deal with the two major banks. Shareholders of other Italian banks may just follow along our reasoning to see how to deal their own specific situation.

Before we move, let's summarize the main data we will need for our valuation.

- Item 30 on the income statement is net interest margin.

- If in FY 2022 this item exceeded by at least 5% the same item in FY 2021, then the bank will see the extra profit taxed with a one-off 40%.

- However, if FY 2023 ends up with the same item up at least 10% of FY 2022, in case this amount is larger than the one of the prior year, this will be the amount taxed.

- There's a ceiling on the contribution banks will pay: It can't exceed 0.1% of total assets.

- In addition, those banks that have already adjusted rates on deposits won't be impacted by the law.

The impact on Intesa and UniCredit

First of all, all main Italian banks recently reported very strong results that led many of them to give higher guidance.

Considering the two banks we are talking about, let's take a look at two slides from the respective 1H23 results presentation.

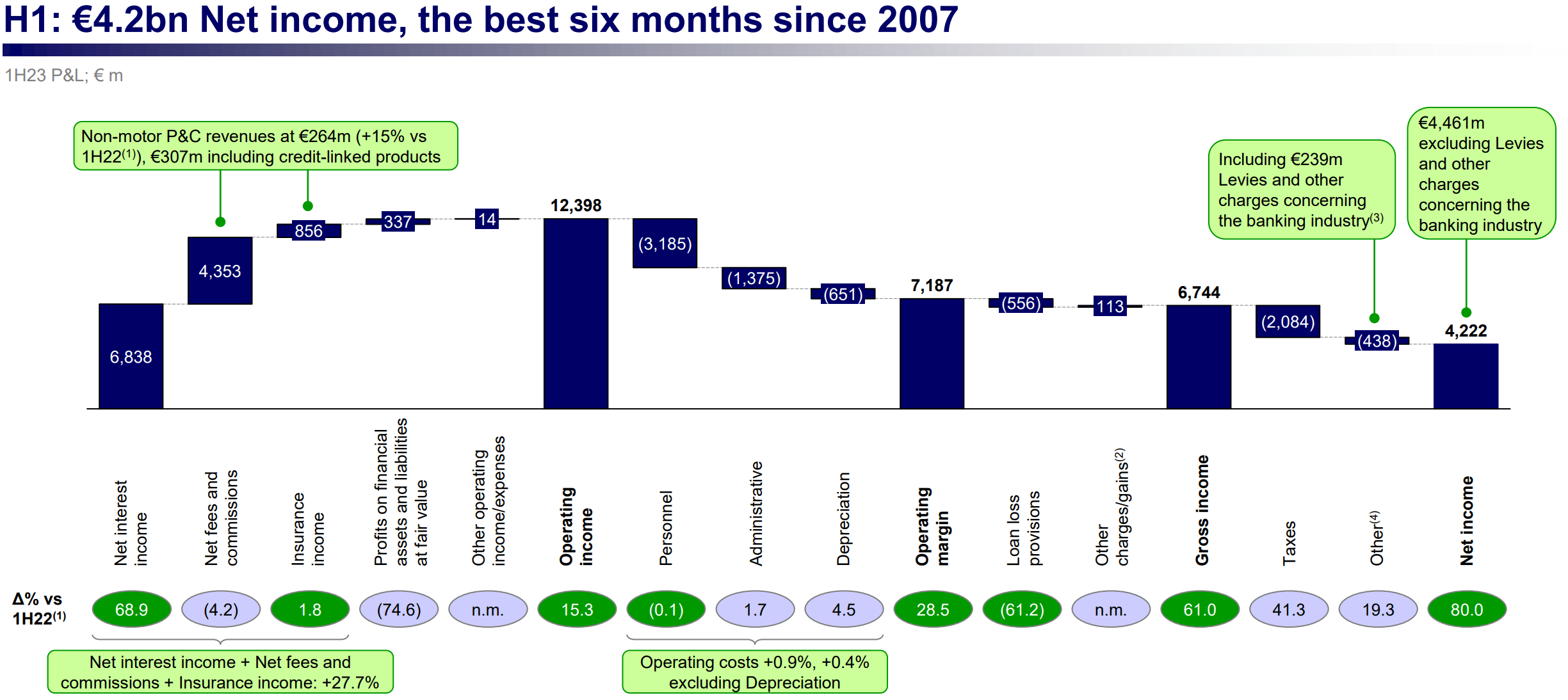

Intesa Sanpaolo wasn't shy about the outstanding results achieved in the first six months of this year, which brought the bank back to its highs before the Great Financial Crisis of 2008.

{kind=link}

If we look at the mix leading to the operating income, we clearly see the big contribution coming from net interest income: €6.8 billion out of €12.4 billion (54%).

During the earnings call , Intesa Sanpaolo also said it expected its net interest income to come above €13.5 billion for this year with further growth to come in the next two years. Therefore, the bank upgraded its 2023 net income guidance to "well above €7 billion," with this being a floor the upcoming years. Investors celebrated this report because Intesa Sanpaolo has a dividend policy which pays 70% of its net income. With these numbers, this is a bank with a previous dividend yield is 11%, with potential additional capital distributions to be elevated year-by-year.

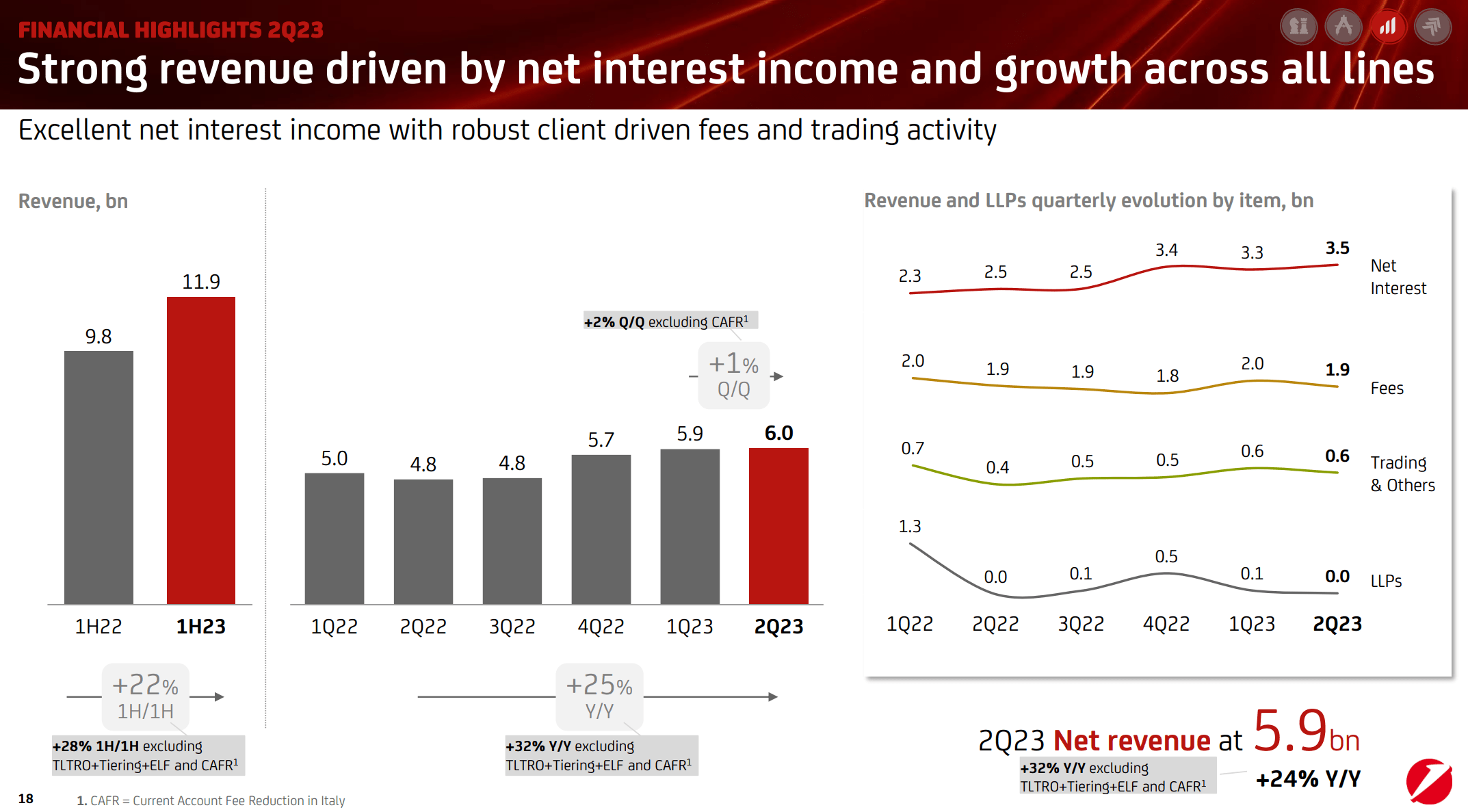

UniCredit reported a similar situation, highlighting how the main driver of revenue growth was net interest income.

{kind=link}

During the earnings call , UniCredit admitted that "we continue to experience a positive net interest dynamic driven by higher loan rates and still low deposit beta." In other words, the bank said it is not raising rates on deposits at the same speed it is raising loan rates.

UniCredit also said it expects a FY 2023 net interest income of at least €13.2 billion. In addition, it disclosed how its net interest income sensitivity for a one percentage point of deposit beta is about €130 million at current rates and deposit volume assumption. For every rate increase of 50 bps, the bank will see a positive impact of about €300 million.

I think these two slides show what is going on: Indeed, these banks are reporting record profits because the gap between loan interest rates and deposit rates.

Scanning through the quarterly reports of the past two years and a half, I put together the data of the net interest income earned by the two banks.

Author, with data from Intesa Sanpaolo and Unicredit Financial Reports

{kind=link}

We see how three quarters ago, around 4Q of 2022, net interest income began to quickly increase for both banks. This shows us even better where the issue lies: Customers are being penalized because they are not yet awarded high rates on deposits. In the meantime, banks benefit from the same environment that's making many households uncertain about their future.

Now we can finally calculate the impact this tax might have on the two bank's profits.

{kind=link}

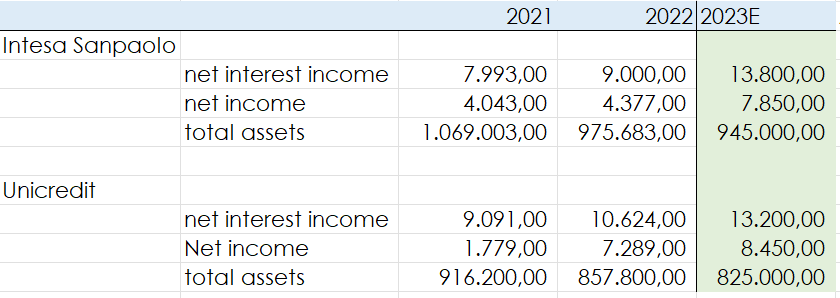

Looking at the data taken from the past two annual reports and the forecast we can make for FY2023 results, given the already reported 1H23 results, we have what is show above.

Intesa could have €13.8 billion of net interest income, which will lead to a net income of €7.85 billion. UniCredit will see its net interest income at €13.2 billion, but it should beat Intesa in when considering its net income, which could come in close to €8.5 billion.

We have to consider total assets, too, because that will determine the value of the tax cap. One word on why total assets are declining for both banks. If we look at the balance sheet of both companies, the main reason for this decline is the reduction of gross loans over the past two years, which I think is understandable, given the high rate environment.

The first thing we need to do now is to understand whether both banks will pay the tax on the 2022 or the 2023 extra profits. At the end of FY2022, Intesa saw its net interest income grow by 12.6% or €1 billion. At the end of this year it should see its net interest income grow by 53.3% or €4.8 billion. Intesa will pay the 40% tax on this year's expected profits.

The same is true for UniCredit. Last year it saw its NII grow by 16.9% or €1.5 billion. This year, the expected growth is 24.3% or €2.6 billion.

Both banks have results that will trigger the tax in 2023. Therefore we will see the impact of the tax on the 2024 income statement.

How much will both banks pay?

Intesa will see its €4.8 billion taxed and it will have to pay €1.9 billion. However, this exceeds the tax cap, which should be around €945 million for Intesa. Therefore the tax will actually be a 20% tax on the extra profits.

The same happens for UniCredit. It should pay €1 billion, but since its tax cap should be around €825 million, it will end up paying a 32% tax on the extra profits.

There's actually one factor we can't really estimate but that's in favor of these banks. The Italian government has anticipated it will use this tax to help Italian households pay their mortgages. Therefore, part of this money will go back into the pockets of the banks, just like it happened for the windfall tax on oil companies that were used to help households pay their bills.

Impact on dividends

Italian banks are good dividend payers. Since the Great Financial Crisis and the Sovereign Debt crisis, they have worked to have stronger balance sheets and high CET1 ratios. Intesa has also reached the zero-NPL bank status.

So, how much will this tax impact the hefty checks these banks pay to their shareholders?

Intesa's dividend policy aims at paying in the form of dividends 70% of the annual net income. The bank will evaluate year-by-year if it will add other returns. For example, the bank finished back in April a €3.4 billion buyback program.

UniCredit has been also on a run since the arrival of the new CEO Mr. Orcel, who announced a massive program to make the bank a very profitable one, with the ability to return a lot of cash to shareholders.

Currently, UniCredit targets to pay 35% of its profits in the form of dividends, while aiming at €16 billion total distribution from 2021 to 2024 through a mix of dividends and share repurchases. Currently, if we sum up buybacks and dividends, UniCredit already returned almost €12 billion, leaving at least €4 billion for next year.

In any case, Intesa will end up with a net income after the windfall tax of €6.9 billion. This means it will probably pay €4.8 billion in dividends, which means that it will hand out €0.26 per share, which is an 11% yield.

Unicredt could end this year with a net income after the windfall tax of €7.6 billion, which gives us a €1.47 dividend per share, which is equal to a 6.6% yield, not counting buybacks. UniCredit will use around €2.7 billion for its dividend, leaving at least €1.3 billion available for a further buyback. This is an additional 3% return at the current share price of €22.4.

Last year, Intesa paid a dividend of €0.164 per share, while UniCredit paid €0.99 per share.

The math is clear: Investors will end up just fine. Actually, investors may profit from the current volatility to pick up some shares of solid banks with high returns.

For further details see:

Italian Windfall Tax: The Impact On Intesa And UniCredit