IVOL - IVOL: Not The Right Environment For This ETF

Summary

- The IVOL ETF holds a position in the SCHP ETF plus a portfolio of yield curve steepener options.

- The IVOL ETF benefits when TIPS bonds increase in value or if the yield curve steepens.

- As the Fed continues to raise short-term interest rates and invert the yield curve, IVOL will continue to lag.

The Quadratic Interest Rate Volatility and Inflation Hedge ETF (IVOL) holds a position in the SCHP ETF plus a portfolio of interest rate steepener options. IVOL benefits when TIPS bonds increase in value or when the yield curve steepens.

The IVOL can be useful relative to the SCHP ETF if and when the yield curve steepens. However, the yield curve is actually inverted and getting more inverted every day as the Fed continues its interest rate hiking cycle. Until the Fed stops hiking interest rates, IVOL may continue to suffer.

Fund Overview

The Quadratic Interest Rate Volatility and Inflation Hedge ETF is a fixed income ETF that seeks to hedge relative interest rate movements from falling short-term interest rates or rising long-term interest rates, and benefit when fixed income volatility increases.

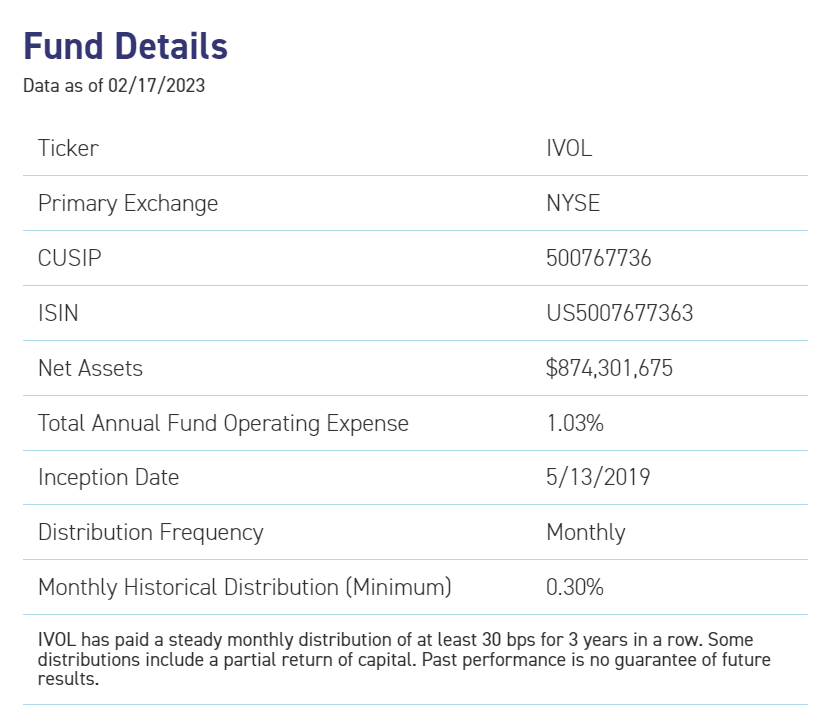

The fund is popular with investors, with $874 million in assets and charges 1.03% operating expense ratio (Figure 1).

{kind=link}

Strategy

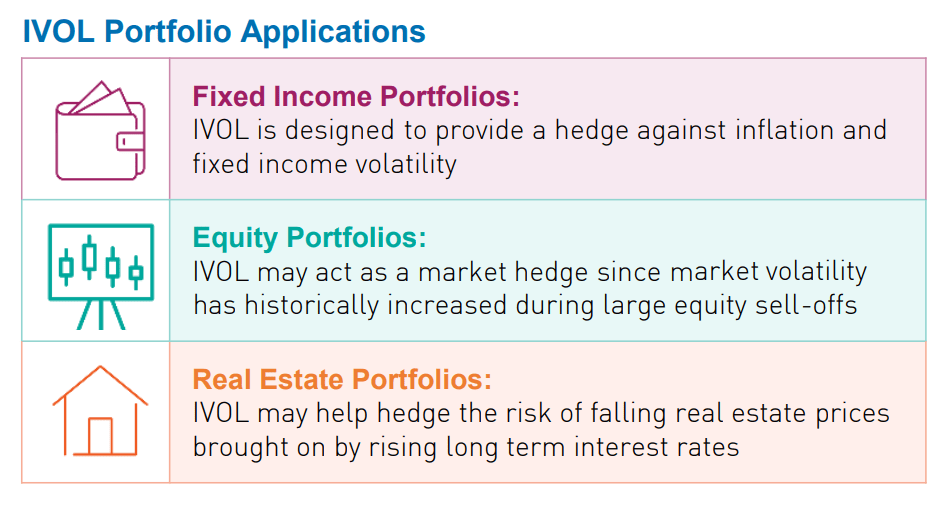

According to the fund's marketing documents, IVOL is designed to protect against inflation and fixed income volatility and may act as a market hedge since volatility has historically increased during large equity sell-offs (Figure 2).

{kind=link}

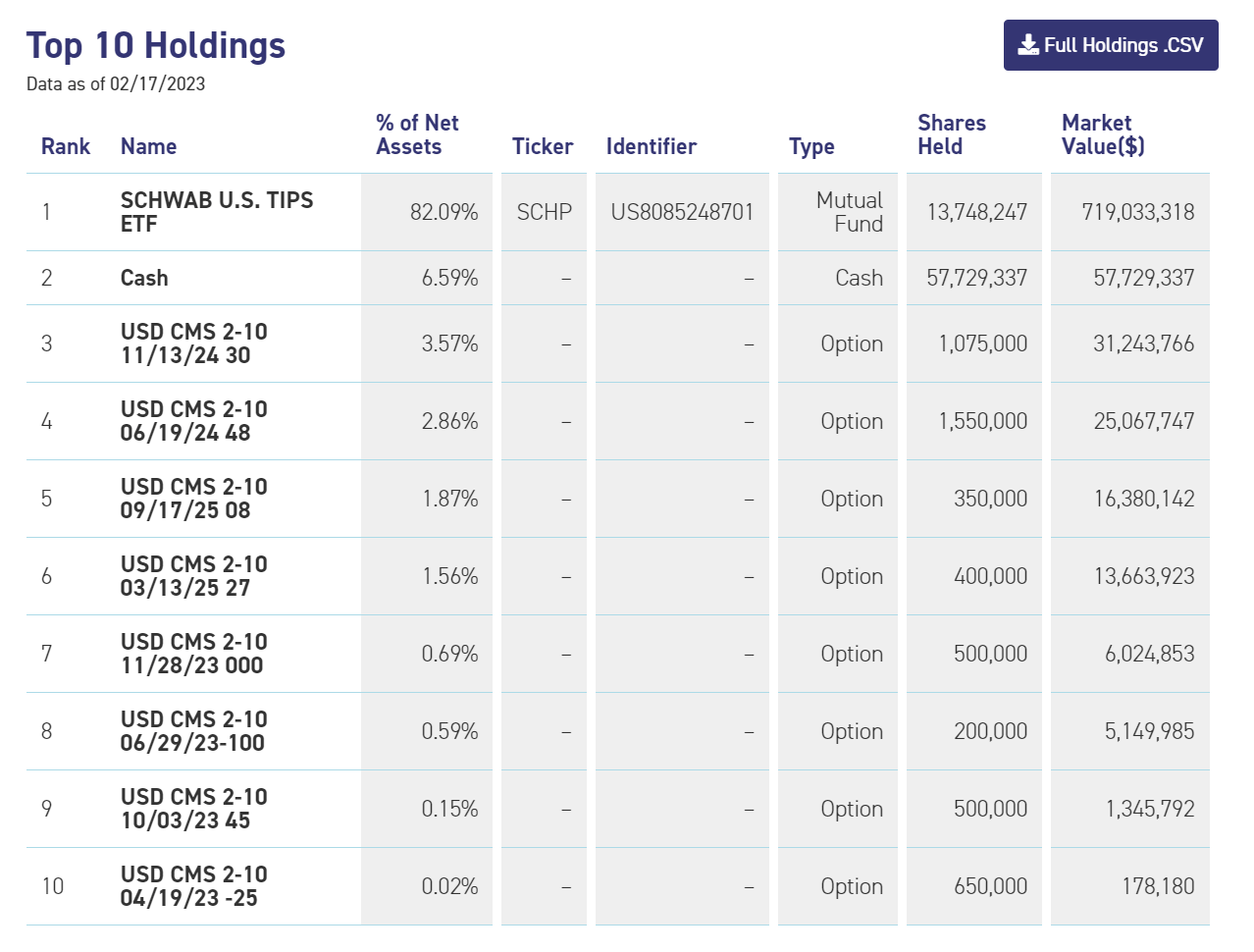

IVOL achieves its objective by owning Treasury Inflation Protected Securities ("TIPS") and a portfolio of fixed income options (Figure 3). As of February 17, 2023, the ETF has 82.1% allocated to the Schwab U.S. TIPS ETF ( SCHP ), 6.6% allocated to cash, and the rest allocated to long OTC options on interest rate 'steepeners' (expecting the interest rate yield curve to steepen).

{kind=link}

Star Manager = Star Product?

IVOL is managed by Nancy Davis , a former Goldman Sachs head trader who have won numerous awards and industry accolades including being named to Barron's inaugural list of "100 Most Influential Women in U.S. Finance" and labeled as a "Rising Star of Hedge Funds" by Institutional Investor .

There was quite a bit of hype surround IVOL when it launched, as the fund won a 'prestigious' award from ETF.com in the category of Best New U.S. Fixed Income ETF. The actively managed IVOL provides institutional-type access to retail investors.

IVOL Hit It Out Of The Park During COVID

IVOL's curve steepener trade hit it out of the park during the COVID pandemic, as the Fed lowered interest rates to essentially zero, anchoring 2Yr treasury yields at ultra-low levels. As we can see from figure 4 below, IVOL raced to a 14.7% return in 2020, far ahead of SCHP's 10.9% return.

Figure 4 - IVOL outperformed in 2020 (Author created with price chart from stockcharts.com)

{kind=link}

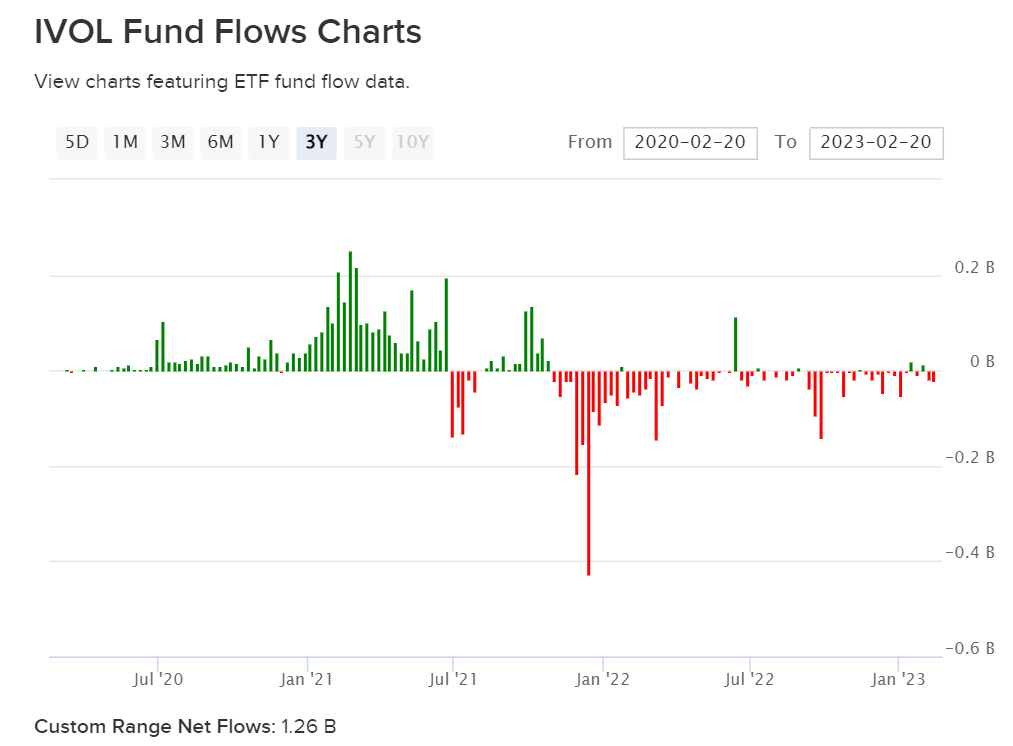

IVOL's strong performance out of the gate allowed the fund to gather lots of assets, with net fund flows of $3.3 billion in the first 2 years of operation (Figure 5). However, as inflation started to rear its head in 2021 and short-term yields rose, IVOL's performance started to lag and fund flows reversed.

Figure 5 - IVOL had strong fund flows out of the gate (etfdb.com)

{kind=link}

Returns

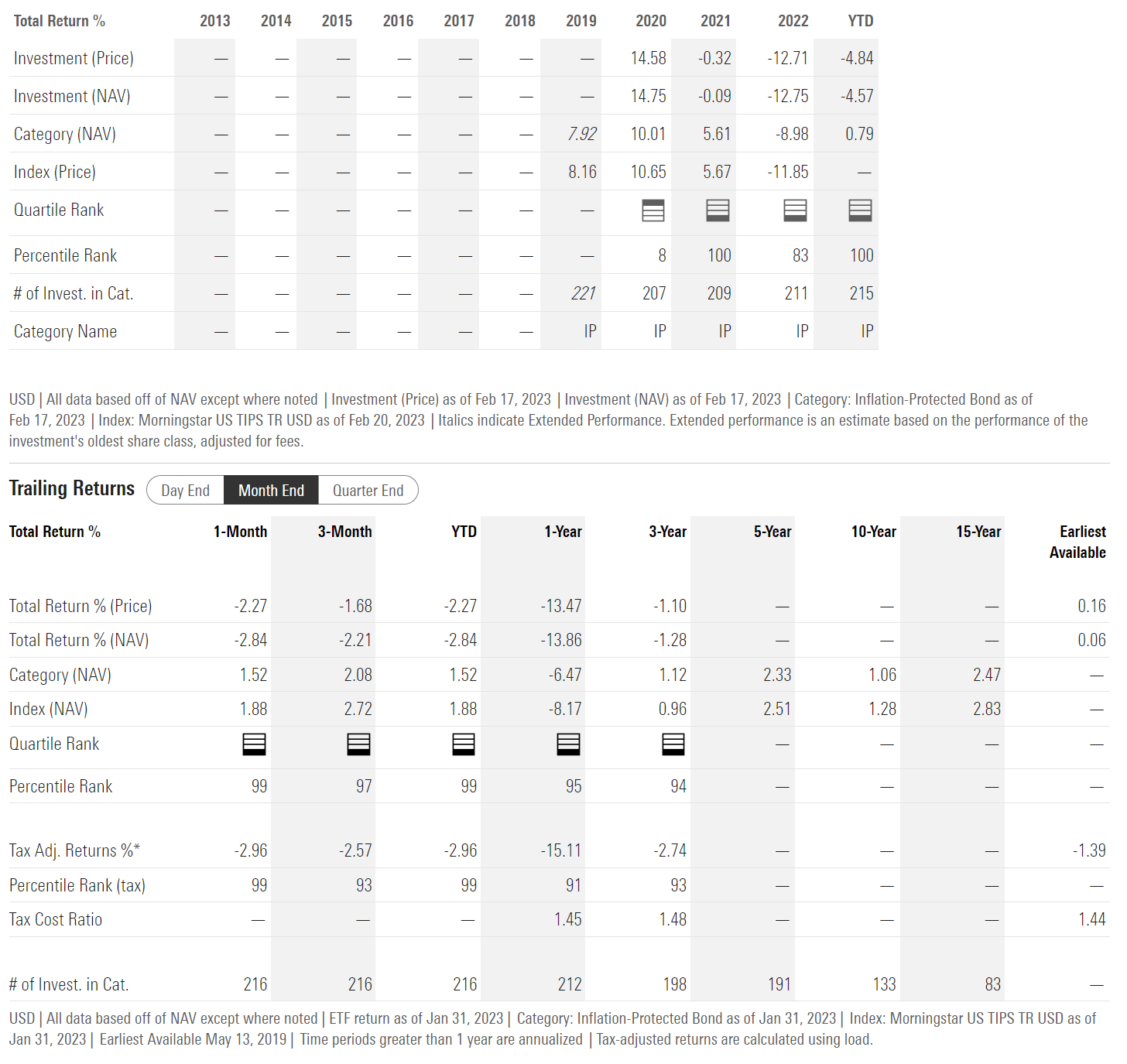

Overall, IVOL's historical performance has been poor, as the fund followed a strong 2020 with a flat 2021 and a -12.8% loss in 2022 (Figure 6). This gives the IVOL ETF a 3yr average annual return of -1.3% to January 31, 2023.

Figure 6 - IVOL annual and historical returns (morningstar.com)

{kind=link}

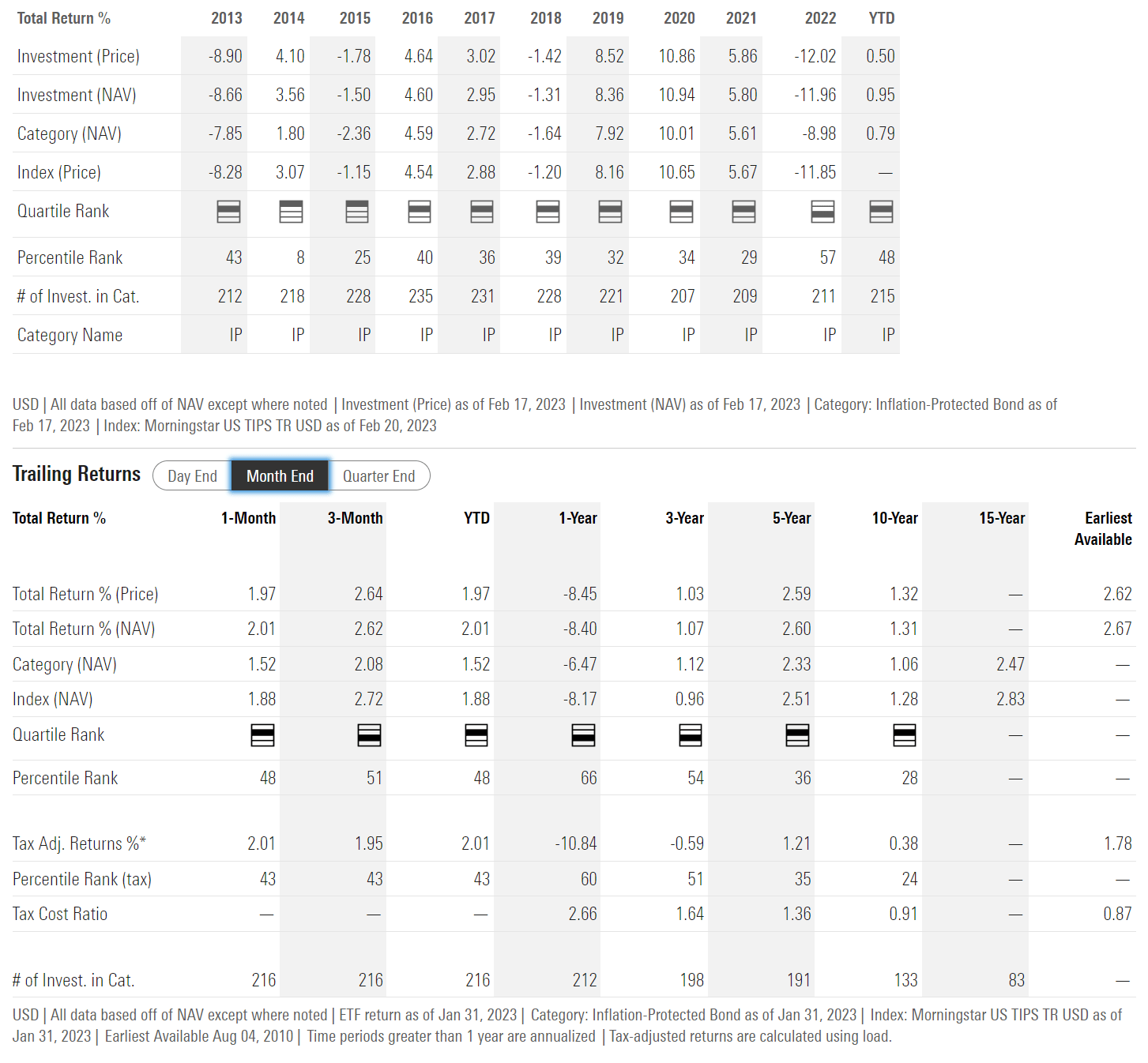

In fact, although the IVOL ETF outperformed SCHP in 2020, it lagged significantly in both 2021 and 2022 due primarily to its interest rate steepener trade (Figure 7).

Figure 7 - SCHP annual and historical returns (morningstar.com)

{kind=link}

Distribution & Yield

The IVOL ETF pays a moderate monthly distribution, with a trailing 12-month distribution of $0.87 or 4.1% yield (Figure 8).

{kind=link}

However, given IVOL has an approximate ~80% allocation to the SCHP ETF, IVOL's distribution is actually less than expected, as SCHP has paid a trailing 12-month distribution yield of 7.1% (Figure 9).

Figure 9 - SCHP yield (schwabassetmanagement.com)

Does IVOL Really Protect Against Inflation?

In hindsight, IVOL may need to change its marketing pitch, as the ETF failed to protect investors during 2022, which saw the highest inflation rates in decades. As I wrote in an article on the SCHP ETF, a fund of TIPS bonds does not necessarily protect investors from inflation, especially if interest rates are rising in response, like they did in 2022.

Although TIPS bonds have their principal and interest payments adjusted for CPI inflation, they are still long-duration assets that suffer when long-term interest rates rise.

Furthermore, IVOL's long position on interest rate steepener options were the wrong trade for most of 2021 and 2022, as the economy improved and the Fed raised interest rates to fight inflation, flattening the yield curve.

A more accurate description of the IVOL ETF should be 'TIPS ETF Plus Options On Interest Rate Steepeners' , although that would sound less catchy than 'Interest Rate Volatility and Inflation Hedge ETF' .

IVOL Could Work During Market Corrections

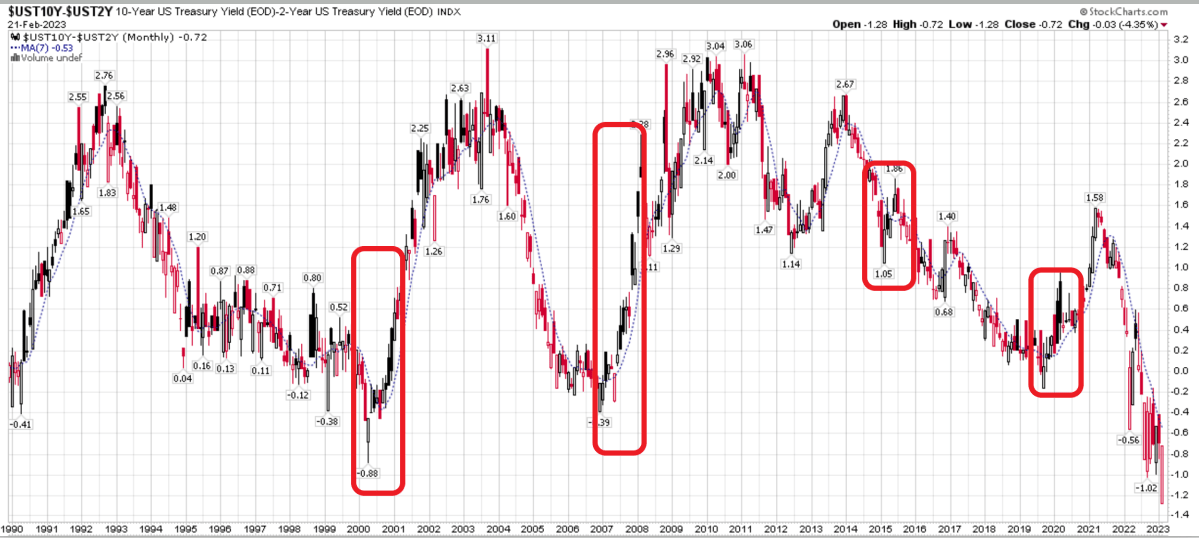

However, before one gets too critical of management, I believe the IVOL ETF does have utility. If we look historically, 4 of the past 5 market correction /crash episodes (2000-2001, 2008-2009, 2016, 2020) saw the yield curve steepen, as they were accompanied by the Fed 'cutting' interest rates in response to weak growth (Figure 10). 2022 was more of a special case, as the market correction was actually driven by the Fed 'raising' interest rates, instead of the Fed 'cutting' interest rates.

Figure 10 - 10-2 Treasury yield curve (Author created with price chart from stockcharts.com)

{kind=link}

Fee

As mentioned above, the IVOL ETF charges a 1.03% expense ratio. However, if we look at the fund's holdings, it has a relatively static 80% allocation to the SCHP ETF, which charges a 0.04% expense ratio itself. Therefore, investors are actually paying ~5% for the interest rate steepener options portfolio, which is quite a 'steep' price to pay.

Conclusion

The IVOL ETF holds a position in the SCHP ETF plus a portfolio of interest rate steepener options. IVOL benefits when TIPS bonds increase in value or when the yield curve steepens. The IVOL can be useful relative to the SCHP ETF if/when the yield curve steepens. However, as the yield curve is currently inverted, investors may have to wait until the Fed is done with its current interest rate hiking cycle before the IVOL will come into favour again.

For further details see:

IVOL: Not The Right Environment For This ETF