SJM - J. M. Smucker: Margins Improving However I'd Welcome Another 10% Pullback

2024-01-13 04:59:12 ET

Summary

- J. M. Smucker recently reached its 52-week low due to an expensive acquisition of Hostess Brand, adding significant debt to its books.

- The company's debt levels are manageable, with a good debt-assets ratio and debt-equity ratio below 1.5.

- Margins have been deteriorating but are expected to improve as inflation eases and production costs decrease.

Investment Thesis

I wanted to take a look at J. M. Smucker ( SJM ) as it recently bounced off its 52-week low. I wanted to take a look at its financials for some clues as to why it may have dropped in price so much. I believe the recent decline was due to the company's expensive acquisition of Hostess Brand, which added a lot of debt to its books, however, I believe that is a bit of an overreaction as the debt seems to be more than manageable, and the company's margins have been improving. However, based on my conservative estimates, I would like it to retreat even more before I would consider investing my capital into the company, therefore, I assign the company a hold rating and will wait for a pullback.

Briefly on the Company

J. M. Smucker is a leading marketer and manufacturer of a variety of consumer products. It sells many types of spreads, including Jif peanut butter, and its iconic fruit spreads. It also operates the retail coffee business with a network of over 600 cafes under the brands Dunkin´ Donuts (partnership) and Caribou Coffee.

Financials

As of Q2 ´24 , the company had around $3.6B in cash and equivalents, against $7.7B in long-term debt, which is quite a decent amount that would keep many investors away from the company. It is more than half of the company's market cap. Many investors tend to avoid such companies due to the solvency risks. I don't think it's a good reason to avoid companies just based on the levels of debt it has on its books, as you might miss out on a quality company that smartly uses debt. There are a few metrics that I like to look at when deciding if a company is being smart with debt.

The first one I like to look at is the Debt-assets ratio. A good ratio is anywhere from 0.30 to 0.60. Historically, the company has been comfortably on the lower end of this range. As of the latest quarter, that stood at around 0.42, which is a good spot to be in.

The company's debt-equity has been in the range of 0.55 to 0.74, while in the latest quarter, it inched up to around 1. Anything under 1.5 is considered not overleveraged in my opinion, so the company gets another plus there. Lastly, I like to look at how easily can the company pay off its annual interest expense on debt, in FY23, the interest coverage ratio stood at around 7.7x, meaning EBIT can cover the interest expense almost 8 times over and around 9 times over as of Q2 ´24. For reference, many analysts consider a coverage ratio of 2x as healthy. In my opinion, a 2x is a little close for comfort because there's very little room for bad years of operations, which will bring down EBIT considerably. I think a 5x is much more sufficient to account for those bad years of performance. So, it seems that the debt is quite manageable in my opinion, and shouldn't be too high of a factor in deciding whether the company is a good investment. It will certainly affect it somewhat given that it is quite high, but I don't think it is an issue.

{kind=link}

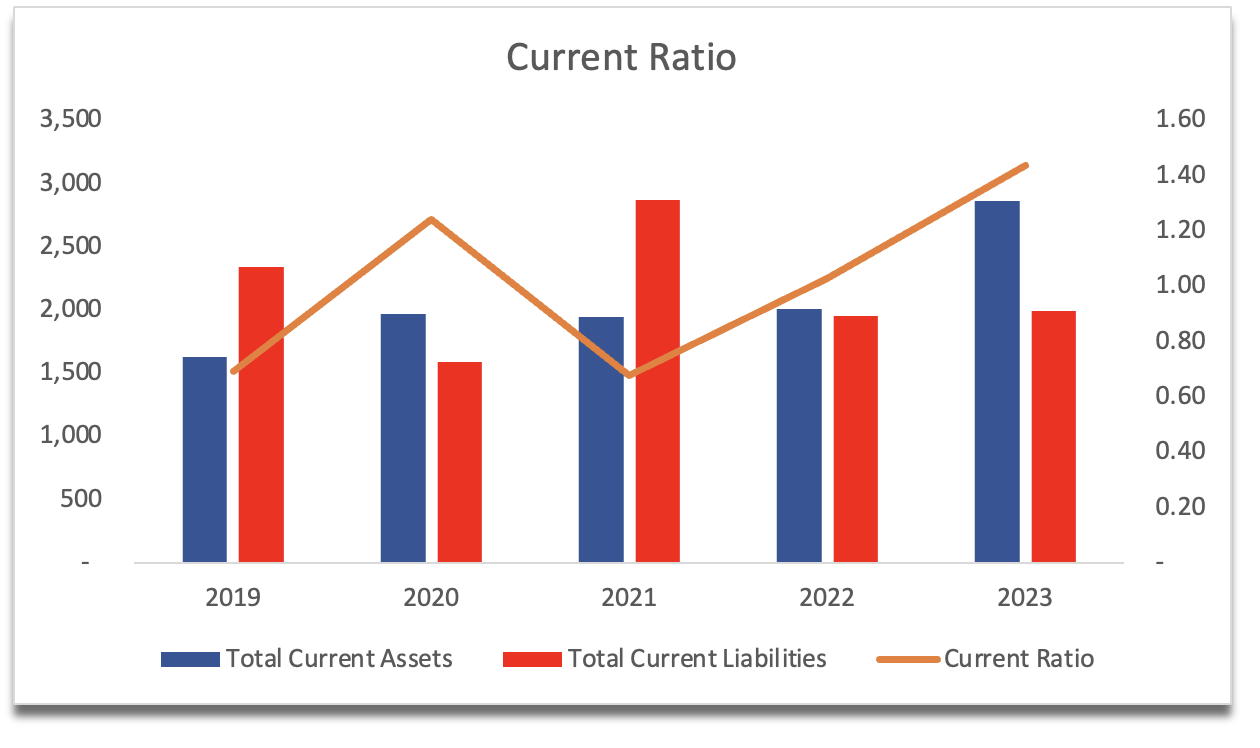

In terms of liquidity, the company's current ratio has been fluctuating quite a bit over the last while, however, in the most recent years it seems to have gotten much healthier. As of FY23, it reached 1.4 and with a cash injection of $3B in the recent quarter, the ratio is up to 4.7. The increase in the cash pile was the proceeds of long-term debt for the same amount for the acquisition of the Hostess Brand. The cash pile will come back down, so I don't expect the ratio to remain this strong, however, over 1 is good enough and even better if it's closer to 1.5. As of now, the company has no liquidity issues.

{kind=link}

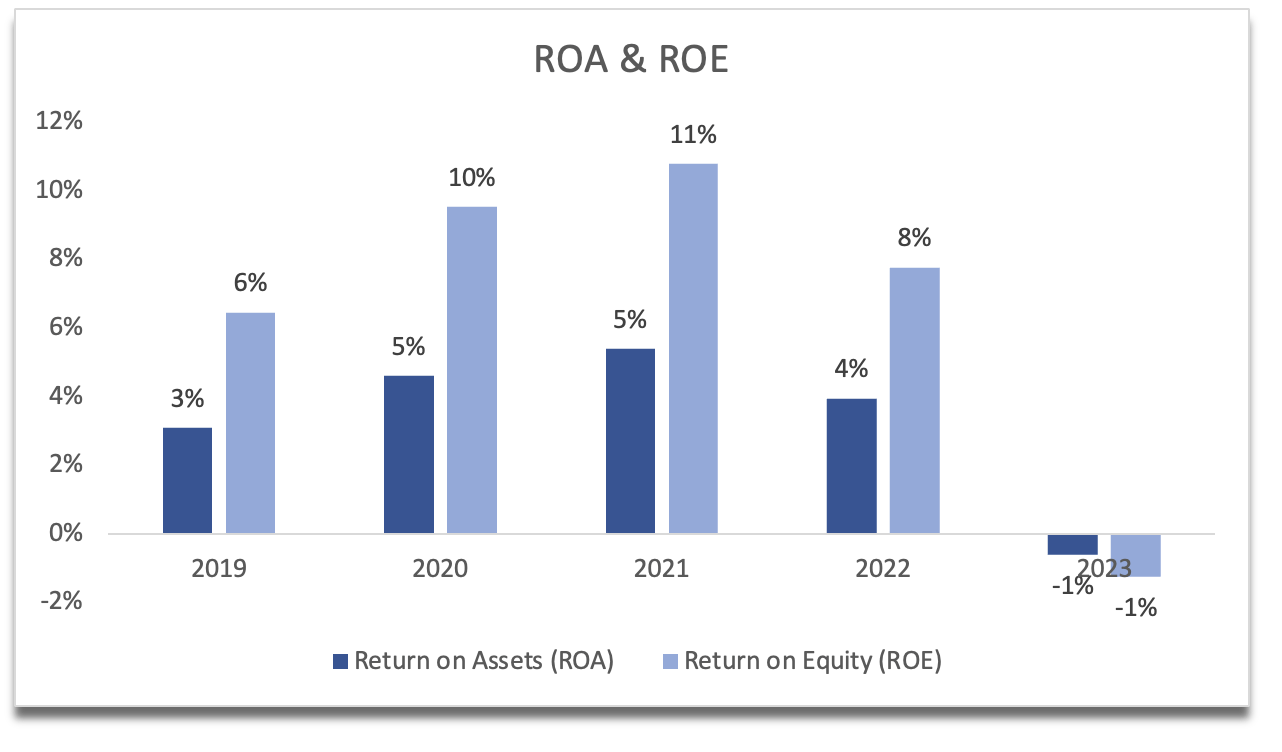

Looking at the company's efficiency and profitability, we can see that these metrics have seen better days, especially FY23, which were negative because of the pre-tax loss on divestitures of some of their brands that were sold to Post (POST), including Rachel Ray Nutrish, 9Lives, Kibbles ´n Bits, Nature's Recipe, and Gravy Train brands. The one-off loss is not going to repeat next year, so I would expect the company to make money once again and the metrics will improve. At the end of FY22, these weren’t very appealing already, so I would like to see improvements on these going forward.

{kind=link}

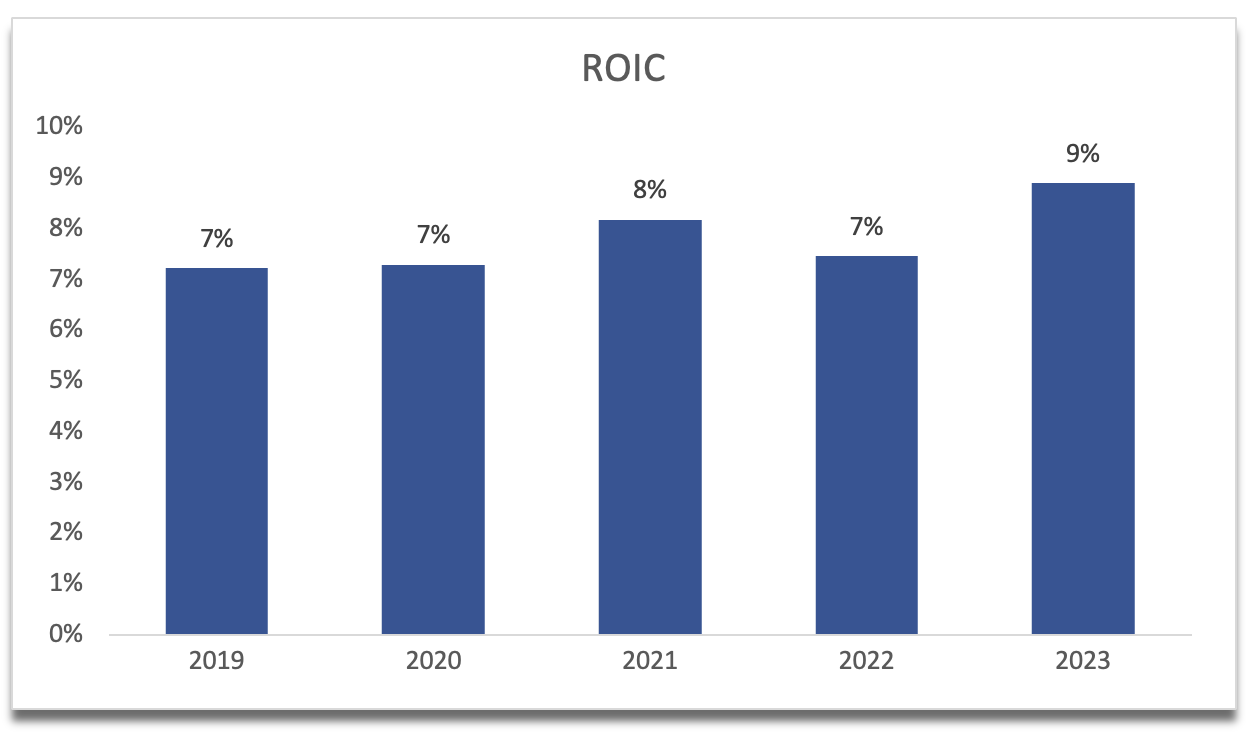

The company's ROIC has been slowly but surely increasing over the last 5 years, and I would like to see this trend continue. I would like to see the company reaching at least 10% next year if everything goes well. Anything over 10% I consider the company to have some sort of competitive advantage and a decent moat. It also tells me that the management is adept at allocating the company's capital to profitable projects.

{kind=link}

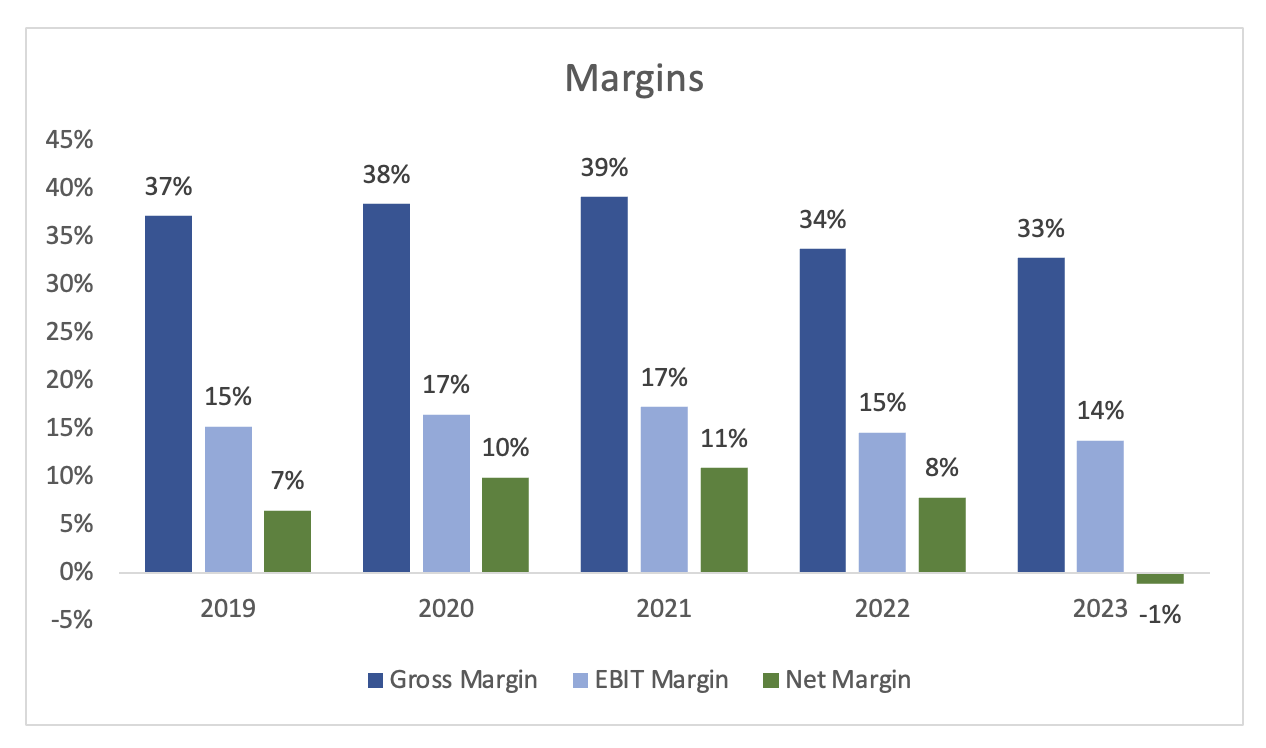

Since we're on the topic of efficiency and profitability, it would be a good time to look at the company's margins, which have deteriorated slightly since FY21 and that is not good. The company felt significant material cost inflation over the last while. With inflation coming down and stabilizing over the last while, I don’t think this deterioration will last, and the company should be able to get back to its historical profitability over the next year or two. We can already see this improvement in the latest quarter. Six months ended October 31 st , the company’s gross margins were back to around 37%, operating margins back to 16%, while net margins are back at around 10%, which the company hasn’t seen since FY21. Just to note that there are still 2 more quarters of the year, which may bring down these margins, so take these results with a grain of salt for now, until we see the full picture of the year.

{kind=link}

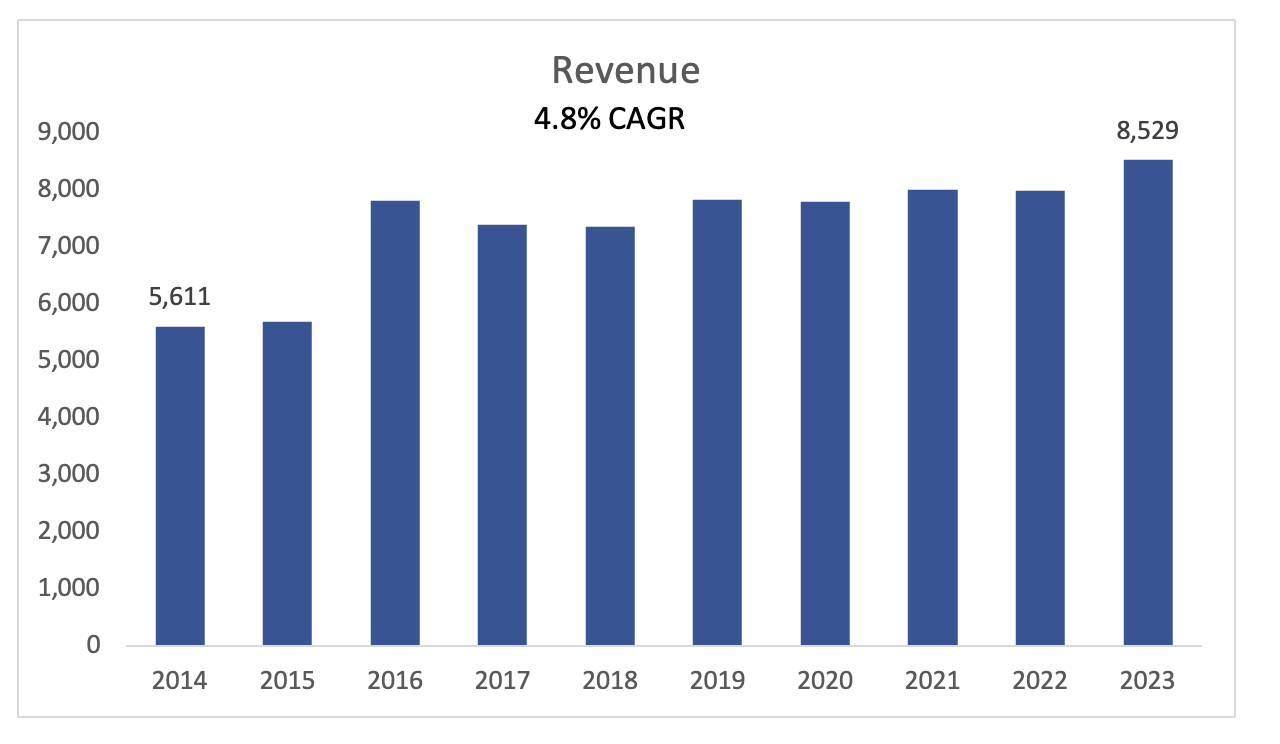

In terms of revenues, just like many companies like SJM, it has not been known for its amazing top-line growth. It managed to achieve around 5% CAGR over the last decade, which isn't bad, but also not that great. Future acquisitions may push its revenue growth higher, however, the brands the company could acquire usually also do not exhibit fast growth. A lot of investors look for top-line growth, however, I believe improvements in efficiency and profitability are the way to go for companies like SJM. As long as they don’t stay put and just chug along without any improvements.

{kind=link}

Overall, it looked like the company had hit a couple of bad years due to the macroeconomic conditions of higher interest rates and higher costs. The company seems to be getting back to its better years and I believe it'll perform well for the next two quarters.

Valuation

I always approach my valuation analysis with a conservative outlook; therefore, I don’t predict that the company will see much improvement in its sales growth, just to give myself more margin of safety. Below are my assumptions for the base, conservative, and optimistic cases with their respective CAGRs.

{kind=link}

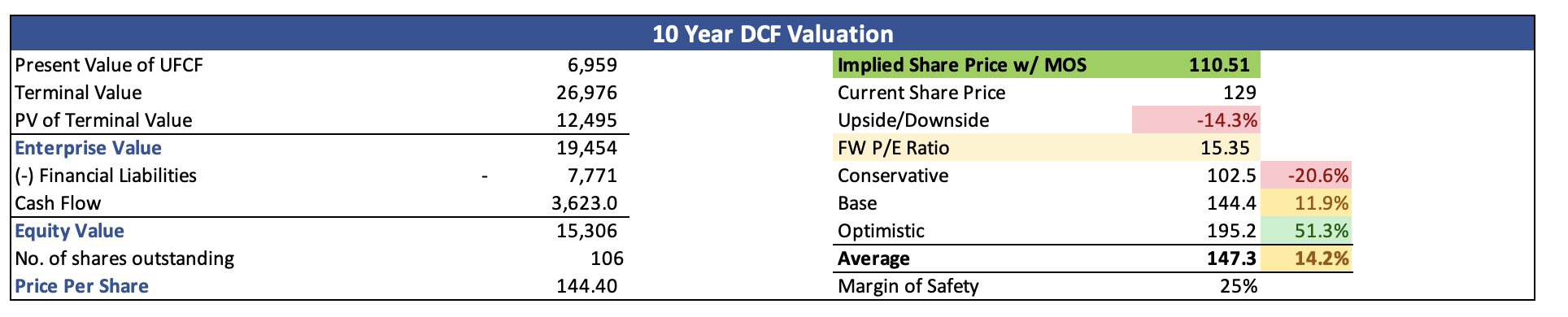

For margins and EPS, I went with slightly lower estimates than what the analysts are estimating just to give myself a little more margin of safety. Let's face it, anything predicted more than a year out is just guessing, so I would like to be on the more conservative end. Below are my assumptions. For the DCF analysis, I went with around 8% discount rate, which is slightly higher than the company's WACC of around 7%. This way I get even more defensive and add to my margin of safety. I also went with a 2.5% terminal growth rate. On top of these estimates, I added yet another 25% margin of safety just to give myself even more room for error. With that said, SJM´s intrinsic value and what I would be willing to pay for it is around $110 a share, meaning the company is trading at a 14% premium to its fair value.

{kind=link}

Comments on the Outlook

The biggest positive I see for the company is not the acquisition of Hostess Brands for $5.6B but rather the overall economic outlook in terms of inflation which, has been trending considerably down since the peak of over 9%. The company's margins saw a big hit because, as you saw in the financials above. These have started to improve quite considerably since then, and even blowing past the recent high margins of FY21. If the company can maintain this momentum of higher margins and keep improving on them, I could see the share price starting to come back up once again. With inflation easing, I can see the demand for the company's products returning as the cost of production continues to fall.

What I would like to see going forward is the management prioritizing reducing the outstanding debt after the acquisition of Hostess Brand. This will certainly start to attract more investors. Investors who are more risk-averse when it comes to leveraging. The company is getting upgraded by analysts citing the cheap valuation and a favorable risk/reward for investors.

My main concern would be the margins. I need to see a couple of more reports before concluding that these margins are here to stay.

Closing Comments

So, it looks like the company is quite close to my PT. I can see the company dropping around 10% in the next couple of months just on macro uncertainties alone. The company may not reach that number, however, and I may miss the boat, but if the company doesn’t pass my conservative estimates, then I don’t think it is such a good deal in the end. Therefore, I am initiating my coverage of the company with a hold rating and will set a price alert at around $110 a share, as I believe that is where the risk/reward is much more attractive for me.

The company will benefit from lower costs of production and efficiency will come in return; however, I believe that the volatility is not gone yet, and we will see some swings in the next couple of months that may present a good opportunity for a long-term investment.

For further details see:

J. M. Smucker: Margins Improving, However, I'd Welcome Another 10% Pullback