SJM - J. M. Smucker: Priced Attractively But Not A Buy Yet

2023-12-12 13:27:27 ET

Summary

- After the sharp pullback in recent months, shares of The J. M. Smucker Company are now trading at multi-year lows.

- The stock also appears attractive relative to its current business fundamentals, which could become a short-term tailwind.

- The big problem, however, is capital allocation which creates significant risks for long-term shareholders.

The past few years have been a real challenge for The J. M. Smucker Company ( SJM ) shareholders, with the stock appreciating by only 12.5% in more than three and a half years. During the same time period, the S&P 500 Index (SP500) returned nearly 50%, and even the Consumer Staples Select Sector SPDR® Fund ETF (XLP) delivered better returns.

The reason why this is so troubling is that up until the beginning of this year, SJM was way ahead of both the equity market and the Consumer Staples Select Sector SPDR® Fund ETF ((XLP)), but the stock experienced significant volatility in 2023 that is unusual for any large cap consumer staples business.

Yet Another Large Deal

The majority of the share price drop happened after J.M. Smucker's management announced its intentions to pursue a mega deal for Hostess Brands, Inc. ( TWNK ).

Seeking Alpha

For a company with a market capitalization of less than $13bn, a $5.6bn acquisition is hard to swallow, especially in the heavily branded space of Packed Food.

Such mega deals rarely create shareholder value and quite often backfire, as has been the case of The Kraft Heinz Company ( KHC ), Reckitt Benckiser Group plc ( RBGLY ), and even the recent fiasco with Unilever's management over the potential bid for GlaxoSmithKline's consumer unit.

Seeking Alpha

{kind=link}

About 3 years ago, I warned of the risks related to J.M. Smucker's too aggressive M&A strategy and just as the company was looking to embrace a more organic growth-oriented approach, the news of yet another mega deal came.

Seeking Alpha

Back in 2020, I showed how over the long run SJM resorts to large deals every time its free cash flow comes under pressure, and I outlined some significant risks with J.M. Smucker's management intention to move aggressively into pet food.

The Financial Implications

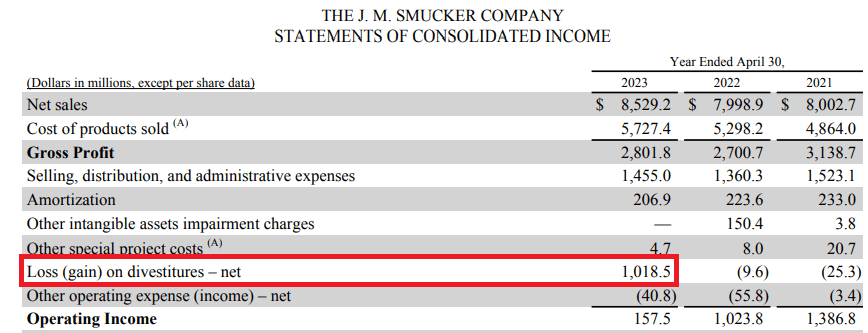

Just a couple of years after SJM did two large deals in the pet food space, in the last annual report the management announced a significant goodwill impairment related to the divestiture of some of these brands.

{kind=link}

In total, this move brought nearly $1bn worth of divestiture losses during fiscal year 2023.

{kind=link}

All that serves as a major warning against mega deals, especially when the deal is done at historically high multiples. The TWNK deal was made at a sales multiple of 3.2, which is nearly twice as high as SJM's current sales multiple.

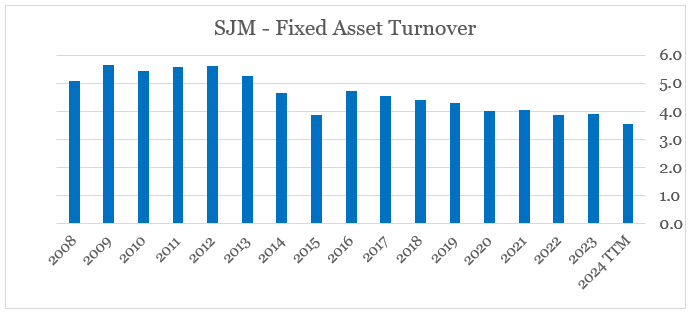

The major problem I have with the large deals that SJM pursues is that they are in areas where significant synergies are hard to realize. Instead of complementing the company's existing brand portfolio or relying on its strong brands, these deals result in a bloated brand portfolio, which is often a recipe for disaster.

J.M. Smucker Investor Presentation

{kind=link}

The company's bloated brand and product portfolio has resulted in a gradual decline for SJM's fixed asset turnover, which fell from as high as 5.6 about 10 years ago to a record low of 3.5 during the past 12-month period.

prepared by the author, using data from SEC Filings

{kind=link}

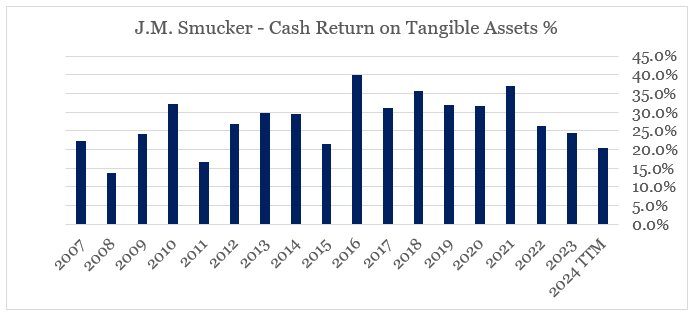

Due to this significant widening of the company's products, cash return on tangible assets has also fallen dramatically.

prepared by the author, using data from SEC Filings

{kind=link}

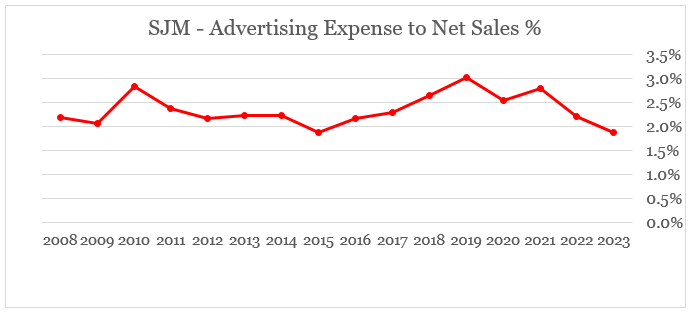

To compensate for the lower asset turnover, SJM has been spending significantly less on advertising relative to revenue during a period of time when the company's brand portfolio has been expanding. This could easily spell a disaster in a similar manner to the one we saw at Kraft Heinz, as the consequences of underinvesting in brand building activities usually take years to surface.

prepared by the author, using data from SEC Filings

{kind=link}

Having said all that, investors often look at current business fundamentals in isolation, without considering the long-term consequences of the strategy. When doing that, SJM appears as a bargain as the company trades below the long-term trend line drawn by its Enterprise Value to Tangible Assets multiple and the Cash Return on Tangible Assets.

prepared by the author, using data from SEC Filings

What that means is that SJM could experience an upward multiple repricing in the short term, if its return on tangible assets does not deteriorate further. Beyond that, however, SJM is still in a very poor position to outperform its peers as the company doubles down on its aggressive M&A approach.

Conclusion

J. M. Smucker's recent share price volatility is a major warning sign for long-term shareholders. Although I outlined the risks of the company's aggressive M&A strategy a few years ago , the market has only recently begun to catch up with the potential negative implications for shareholders. With that in mind, I can't turn bullish on SJM yet, even though the stock trades cheaply and could experience a short-lived upward momentum.

For further details see:

J. M. Smucker: Priced Attractively, But Not A Buy Yet