CLS - Jabil: Assessing Its Potential As It Nears Inclusion Into The S&P 500

2023-12-05 11:14:57 ET

Summary

- Jabil, a provider of manufacturing services, is a solid buy due to its track record, expected growth, and cheap stock price.

- The company operates in two segments: Electronics Manufacturing Services (EMS) and Diversified Manufacturing Services (DMS).

- Jabil's revenue has been growing, and it has positive cash flow and profitability metrics. It is also expected to replace Alaska Air on the S&P 500, potentially creating a short-term buying opportunity.

The best way to generate attractive returns on the market is to buy high quality companies at a discount. While this sounds easy, it is far more complicated than investors would like to admit. But one firm that has demonstrated itself as worthy of this designation is Jabil (JBL), a provider of worldwide manufacturing services and solutions. In addition to generating a solid track record in recent years and expecting that trend to continue this year, shares of the business are trading on the cheap. And for those who like to play to catalysts, there might be another interesting angle to this transaction. That is the fact that, on December 18, the firm will replace Alaska Air Group (ALK) on the S&P 500. In theory, this might create some short-term buying opportunities, since index funds and many ETFs will be forced to pick up the stock in order to remain compliant. Add on top of this how cheap shares currently are, and I would argue that the company makes for a solid 'buy' at this point in time.

A nice firm to consider buying

Some companies are very easy to describe. If you have a shoe manufacturer or a provider of tax software, that is something that can easily be described with a single sentence. Other companies are much more complicated to dissect. Case in point, we have Jabil. As I mentioned already, management describes the company as a leading provider of worldwide manufacturing services and solutions. But this doesn't really tell us much of what the firm is or what it does. It would be helpful, then, to dig into each of its operating segments.

The first of its two operating segments is called Electronics Manufacturing Services, or EMS. This particular part of the company utilizes IT, supply chain design, and engineering technologies that are mostly centered around electronics, all with the goal of producing electronic parts and components at rapid speed and often in large quantities for its customers. For the most part, this unit services customers that are in the 5G, wireless, cloud, digital print, retail, industrial, and other industries. During the company's 2023 fiscal year, this segment accounted for approximately 48.3% of the firm's revenue and 48.3% of its segment profits.

{kind=link}

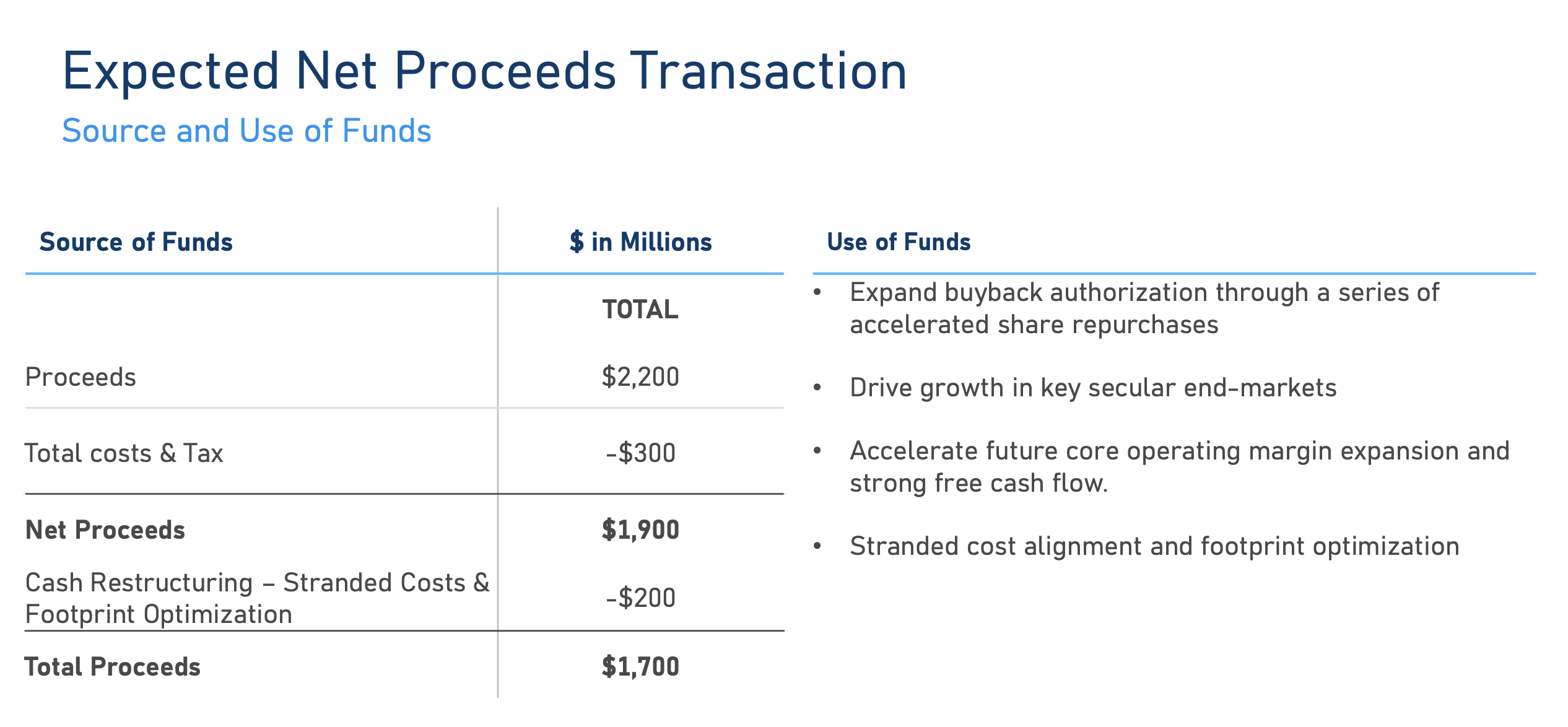

Next, we have the Diversified Manufacturing Services, or DMS, segment. This part of the company mostly focuses on customers in the automotive and transportation space, the connected devices market, healthcare and packaging, and, up until recently, mobility areas. And most of the actual activities that the company engages in here involve it providing engineering services to its customers. As the only other unit that the company has in operation, DMS accounts for the remaining 51.7% of revenue and 51.7% of segment profits, using data from the 2023 fiscal year. It is worth noting that the picture will change moving forward. That's because, on September 26, management announced that they were planning to divest the mobility unit of the company in exchange for proceeds of $2.2 billion. After taxes and fees, as well as $200 million that will be allocated toward restructuring activities, the firm will receive net proceeds of about $1.70 billion. Given the nature of the guidance that the company has given us for 2024, I've decided to incorporate this reduction in net debt when it comes to valuing the company for that year. But I have not done the same for 2023 since we don't know the full financial impact of the transaction if it had been completed at the beginning of the 2023 fiscal year.

{kind=link}

To better conceptualize the company, it might make sense to discuss some of the products it actually makes within these spaces. Examples include medical devices for the cardiovascular space, test and measurement devices, 3D printer technologies, biometric payment devices, scanners, IoT and wireless connectivity solutions, optical switches, routers of the telecommunications industry, smart home devices, and more. While the Mobility unit was responsible for $4 billion in revenue (using estimates for 2023), the largest piece of the company involves the 5G wireless and cloud technologies under its EMS segment. This year it should be responsible for $6.1 billion in revenue. This should be followed closely by the $5.6 billion in sales generated by the healthcare and packaging operations of the business under the DMS segment.

{kind=link}

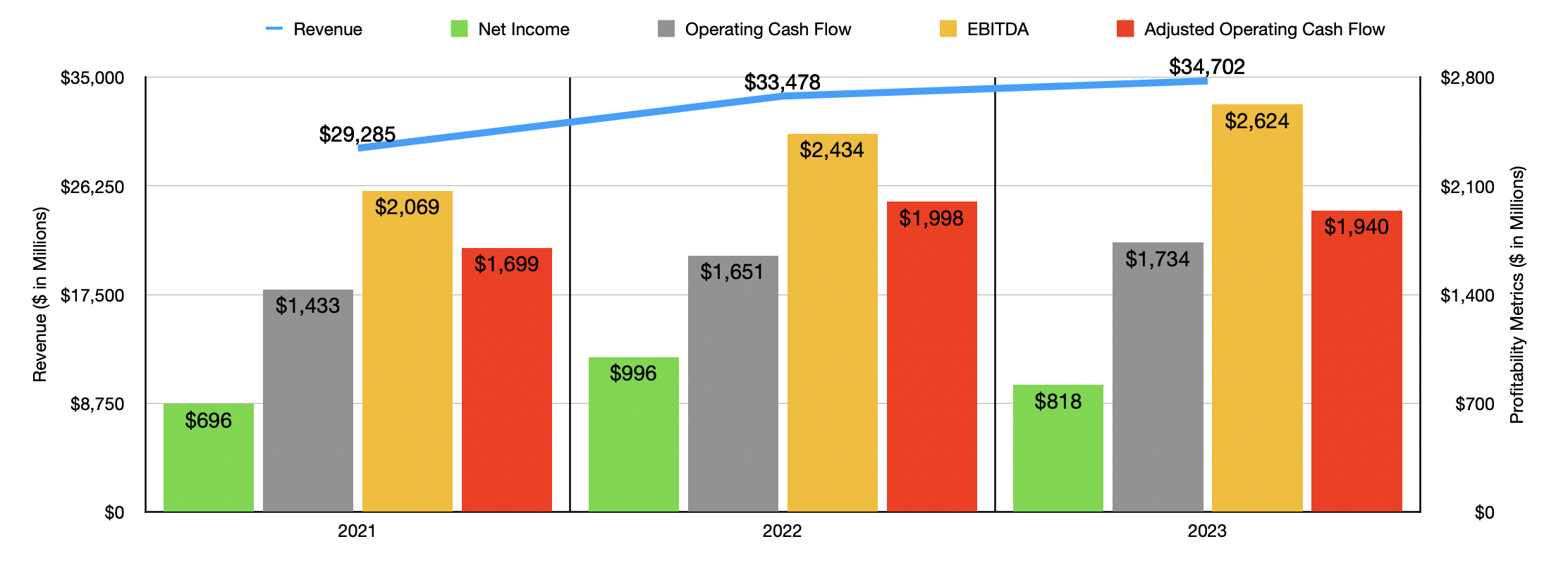

Over the past few years, management has done a good job growing the company's top line. Revenue has gone from $29.29 billion in 2021 to $34.70 billion in 2023. Much of this growth recently has come from the DMS segment. In 2023, for instance, the segment saw a nice increase in sales that totaled 8%. 7% of this rise was attributable to revenues from existing customers in the automotive and transportation businesses. The firm also benefited from a 4% increase in revenue from existing customers in the healthcare and packaging businesses. And the firm benefited from a 1% increase in sales associated with its mobility business.

On the bottom line, the picture has been mixed but generally positive. Net income rose from $696 million in 2021 to $996 million in 2022. During 2023, it pulled back some to $818 million. Other profitability metrics have bounced around, while others still have seen a general uptick. But for the most part, the trend is clear. As time goes on, Jabil becomes healthier. Operating cash flow has grown, for instance, from $1.43 billion in 2021 to $1.73 billion in 2023. If we adjust for changes in working capital, it rose from $1.70 billion to $1.94 billion. Meanwhile, EBITDA for the firm expanded from $2.07 billion to $2.62 billion.

Despite the large asset sale that management agreed to, the firm has decent expectations for the current fiscal year. Originally, management was forecasting revenue of between $33 billion and $34 billion. Because of changing industry conditions, revenue should now be around $31 billion. Earnings per share guidance, on an adjusted basis, was previously between $9.30 and $9.70. That's up from the $8.63 reported for 2023. Now, earnings have been revised lower to $9 per share or higher. If we assume $9, that should translate to adjusted profits of $1.22 billion. That would be up from the $1.17 billion in adjusted profits reported last year. We don't have estimates when it comes to other profitability figures, but good approximations would be $2.02 billion for adjusted operating cash flow and $2.74 billion for EBITDA.

{kind=link}

Using these figures, I was able to value the company as shown in the chart above. I valued the firm not only using the forward estimates, but also using the actual results generated in 2023. I then compared the 2023 numbers to the numbers of four similar firms as shown in the table below. And what I found was that, using each of the three valuation metrics, Jabil ended up being the cheapest of the group. In addition, the company has a market capitalization of $14.96 billion, and has a net debt of only $1.07 billion before the $1.70 billion in net proceeds expected to come from the aforementioned sale. Adding all of this up, we have a truly solid operator that, if anything, should be trading at a premium to similar enterprises.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Jabil |

| 12.8 |

| 7.7 |

| 6.1 |

| Flex Ltd ( FLEX ) |

| 14.7 |

| 9.9 |

| 6.9 |

| Fabrinet ( FN ) |

| 24.8 |

| 20.6 |

| 17.2 |

| IPG Photonics Corporation ( IPGP ) |

| 54.1 |

| 20.4 |

| 13.3 |

| Celestica Inc. ( CLS ) |

| 16.0 |

| 8.3 |

| 7.3 |

An interesting catalyst to consider

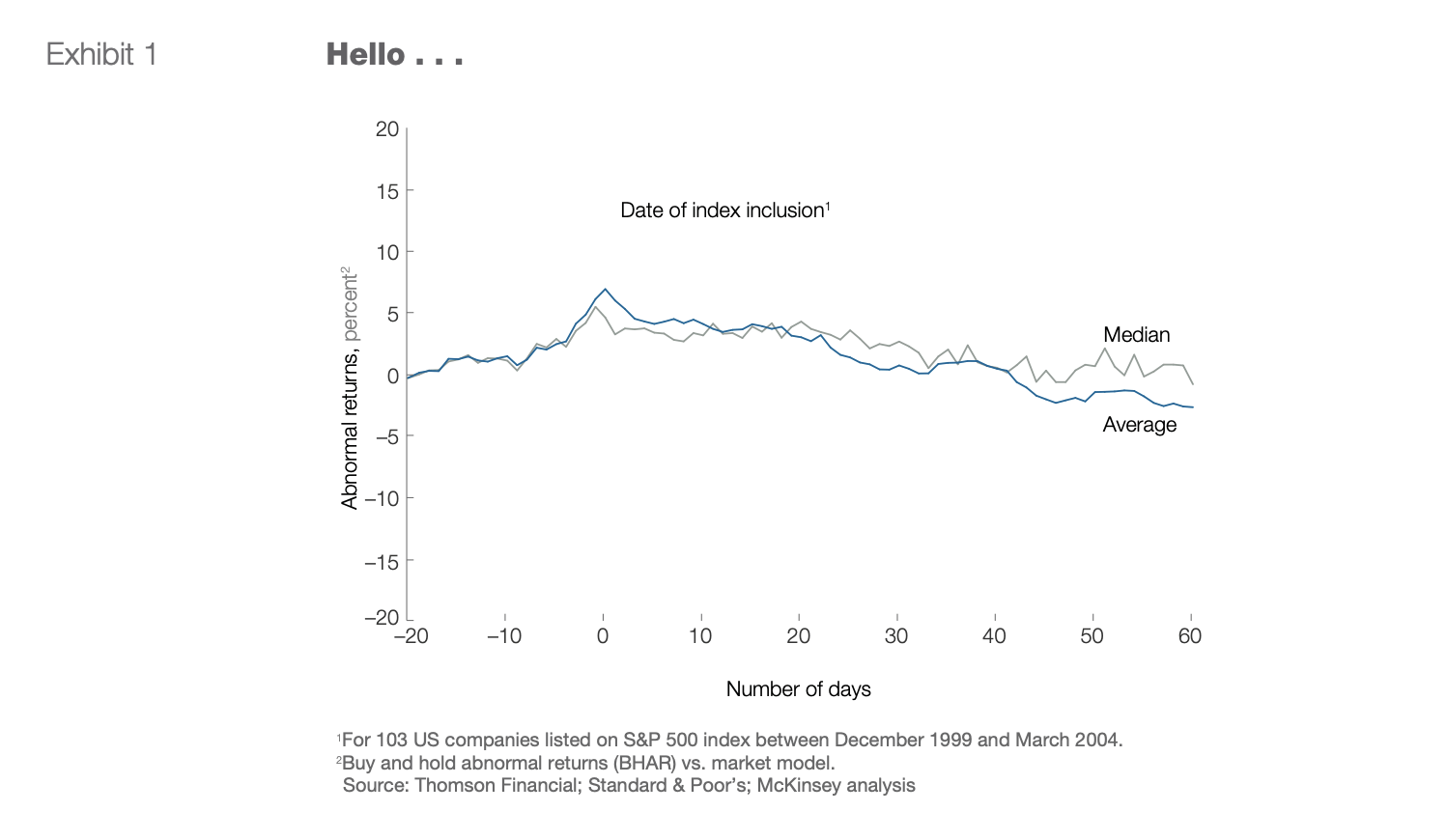

As I mentioned earlier in this article, later this month, on December 18 to be precise, Jabil is expected to replace Alaska Air on the S&P 500. There are two different angles to this. The first is that, in theory, such a maneuver would make the firm more visible and would make investors more likely to buy the stock. But there's also another component, which is that all of the index funds and ETFs that seek to emulate the S&P 500 will be forced to buy a certain quantity of shares. I did some research into this to see if there's any sort of relationship between inclusion in something like the S&P 500 and returns of shares in question.

{kind=link}

Fortunately, this is an area in which there has been a rather significant amount of research. As an example, McKinsey came out with its own report where it concluded that a few percentage points worth of returns in excess of the broader market should be anticipated. However, by looking at the picture over a somewhat longer period of time, in this case about 45 days, those excess returns vanish, which means that once the buying pressure dies down, the market pushes the stocks back to where they were. This was based on 103 instances of companies being added to the S&P 500 between December 1999 and March 2004. This could mean that a short-term buying opportunity might exist for investors. But that would be short-lived if history repeats itself.

Takeaway

As things stand right now, Jabil is most certainly an interesting prospect. The stock is cheap relative to similar firms. Management has a solid track record of growing revenue, profits, and cash flows. Yes, guidance has been reduced for the current fiscal year. But even with that, I see no reason to be pessimistic. In addition, net debt will soon be negative, and I have no reason to be anything other than bullish. In the near term, we might see a bit of a spike. If this does come to fruition, that upside will almost certainly be limited to the near term and, as such, investors would be wise to either try to game this by buying in the short run or, in my opinion, focusing only on capturing the long-term upside.

For further details see:

Jabil: Assessing Its Potential As It Nears Inclusion Into The S&P 500