JBI - Janus International: Growth Bolstered By Rising Mortgage Rates Extra Space Collaboration And AWS

2023-12-03 06:40:38 ET

Summary

- Strong margin expansion despite fluctuating historical revenue growth.

- US's high mortgage rate will bolster demand for self-storage growth.

- Collaboration with REIT Extra Space will further strengthen Nok?'s robust growth.

- With conservative assumption inputs, DCF model implies an undervalued stock.

Synopsis

Janus International Group ( JBI ) specializes in providing self-storage solutions, including new construction, smart entry systems, and technological integrations.

JBI's historical financial performance is clear to be influenced by macroeconomic factors as its revenue growth fluctuates up and down. Despite it, it manages to expand its operating and net margins through effective cost and debt management.

I believe the rising US mortgage rate, strategic collaboration with Extra Space, and integration of its back-end system with AWS will bolster and drive its future growth outlook. Despite modest growth for the next 5 years, my DCF model indicates that it is potentially undervalued. With an upside of ~39%, I recommend a buy rating for JBI.

Historical Financial Analysis

Based on the following table, it is clear that macroeconomic factors play a huge role in JBI's revenue growth. In the pre-pandemic period, it reported 16.62%, and while COVID struck, its growth declined by 2.89%. After COVID, there was rising inflation due to the central bank's monetary policy to lower the interest rate to spur economic growth. As a result, revenue growth reported strong double-digit rates.

As its revenue growth is bumpy, I believe CAGR provides a better view as it reduces the effect of volatility and provides a smoother view. Its 5-year revenue CAGR is ~16%. Although this is lower than 2021's and 2022's rates, it is still in the double-digit range. In my opinion, this is still very impressive, as most companies tend to perform worst in environments with rising interest rates, but for JBI, they thrive in such an environment.

{kind=link}

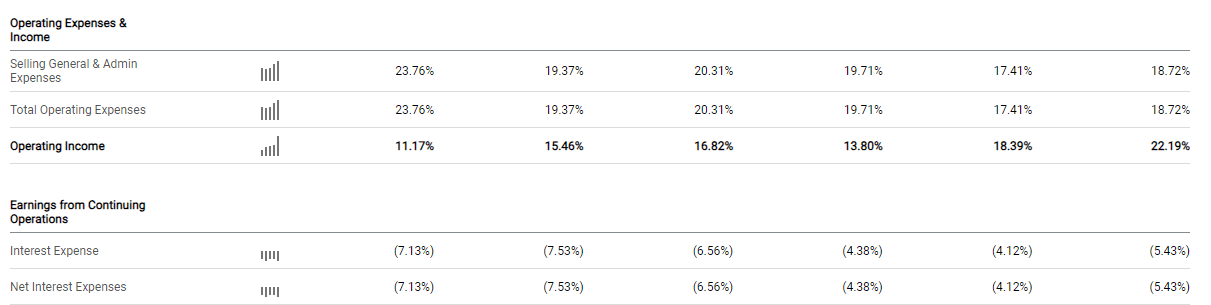

Moving onto margins, JBI has proven to be very robust over the years despite fluctuating revenue growth. In terms of gross profit margins, it is very consistent at ~35%. In terms of operating and net margin, JBI managed to grow it from 11.17% and 2.52% to 18.39% and 10.56%, respectively, from 2018 to 2022.

Author's own chart

If the gross margin remained stable, the operating and net margin expansion would be attributed to its operating costs and expense management. Based on the following table, the clear cost-saving drivers are its SG&A and interest expense. Despite high inflation, JBI showed prudent operating cost and interest expense management; it didn't let inflation erode its business.

{kind=link}

Its declining interest expense can be attributed to its prudent debt management. Over the last 4 years, it has become clear that JBI is heavily deleveraging its balance sheet. In 2018, debt/equity was ~481%, but it was reduced to ~201% in 2022, which represents a deleveraging of more than 50%. In the current high inflationary environment, I welcome this decision, as high interest expenses will erode margins and also put companies in financial distress.

Author's Own Chart

Rising US Mortgage Rate Set to Boost Demand for Self-Storage

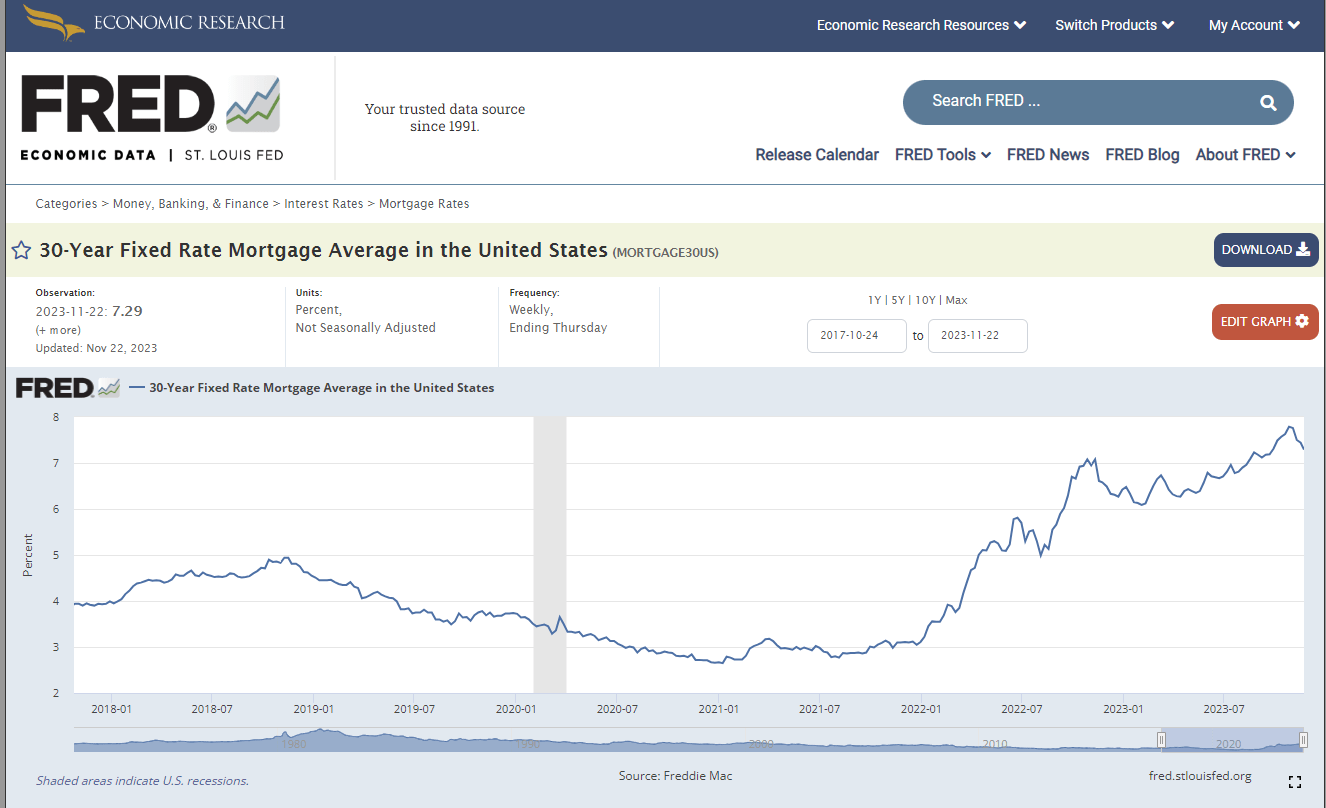

Based on the following chart from FRED , it is clear that the US mortgage rate has been rapidly rising ever since 2021. Currently, it is hitting 7.29% compared to the lowest of ~2.65%, and this represents an increase of almost 2.75x, severely affecting housing affordability, mortgage interest payments, and rental payments.

{kind=link}

Due to the high mortgage rate, many individuals are downsizing their houses, and this has been cited as the main reason why people rent storage space. Due to downsizing their house, the smaller house is unable to fit their existing furniture, which is why they opted for storage space rentals. Due to the rising mortgage rate trends I have discussed above, I believe this is the main reason pushing individuals to downsize their houses due to housing affordability issues.

The central bank's interest rate decision has a direct impact on the mortgage rate, and the central bank's interest rate decision is based on current inflation . Currently, inflation is still elevated at ~3%, which is still above the 2% target rate as well as above pre-pandemic levels. No one can predict the future of inflation, so it's anyone's guess. As long as inflation stays above the target rate, the interest rate will remain at current levels in order to cool it down, which means that the current high mortgage rate will stay as well. Hence, I anticipate that demand for self-storage will remain high, which will drive JBI's future growth.

{kind=link}

This phenomenon is not only happening in the US. In the UK , it was also reported that there was a change in the housing landscape towards smaller living spaces due to rising prices. For the same reason, smaller houses mean smaller spaces, which is driving demand for self-storage.

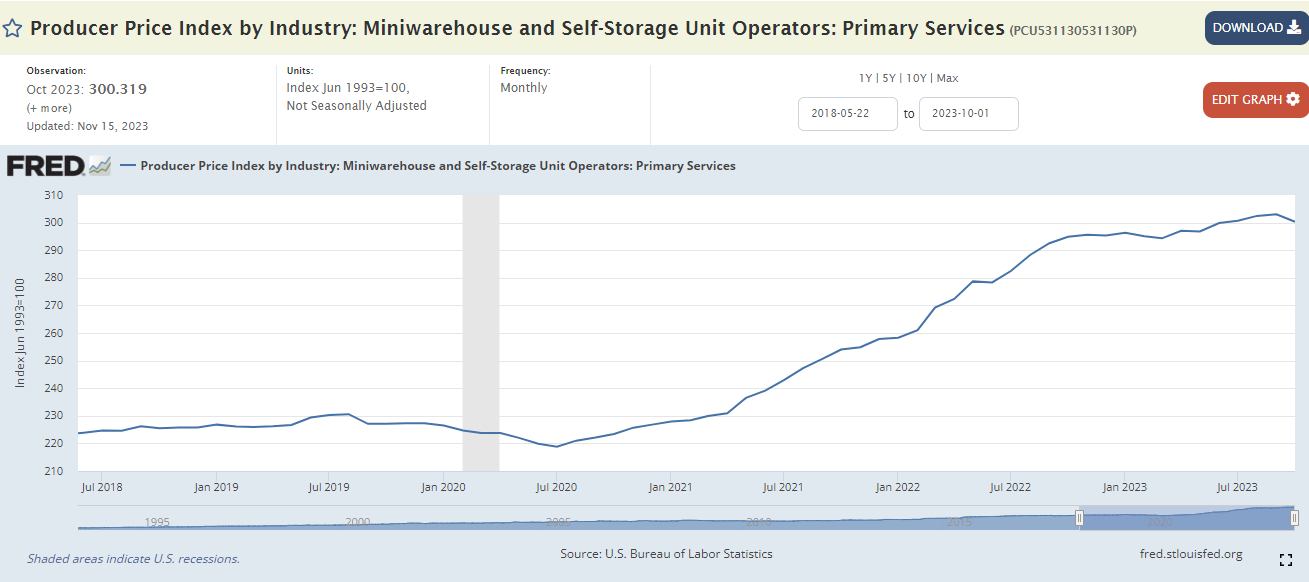

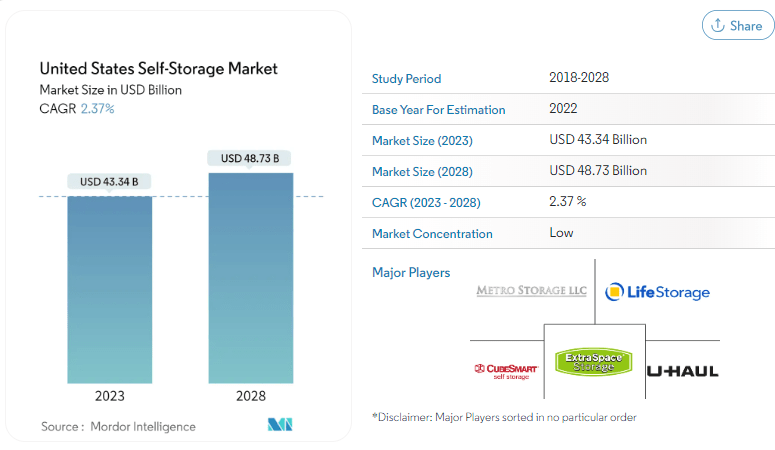

Shifting my focus back to the US, it is clear that the self-storage industry is anticipated to continue growing. For October 2023, PPI was ~300, and this means that prices have on average tripled since 1993, which was the base year set at 100. Currently, the market is valued at ~$43 billion , and it is expected to grow to ~$48 billion, which represents a 5-year CAGR of ~2.37%.

As a result of the strong demand for self-storage, JBI's new construction segment was the key driver for their revenue growth. New construction grew by 40.3%, outpacing its R3 and commercial segments. In addition to the strong growth, management also stated that self-storage occupancy rates for the quarter are still higher than what is typically expected at the midpoint of a normal or average level of activity. This signifies that demand for self-storage is still robust, and I expect this demand to drive JBL's future growth outlook.

{kind=link}

{kind=link}

JBI's Collaboration With Extra Space Poised To Accelerate Nok?'s Robust Growth

In my opinion, apart from its new construction segment, the strong market penetration of JBI's Nok? Smart Entry system is also a noteworthy key driver of its future revenue growth. The reason behind this stems from its strong order growth, where it grew 11% from the second quarter and over 50% year-over-year, signifying the product's robust demand.

On September 20, 2023, JBI announced its collaboration with Extra Space Storage . I believe this collaboration will further bolster JBI's Nok? Smart Entry system's growth, as this collaboration aims to increase the install base of Nok? digital access solutions in more than 400 more facilities.

With this collaboration, its technology will be available in around 1,110 Extra Space properties, and I believe this exposure will make JBI much more visible in the market. This collaboration not only demonstrates the value of JBI's technology but also creates opportunities for new revenue streams, thus driving up JBI's future growth outlook.

AWS Adoption Aims To Boost Customer Retention And Attraction

JBI has completed its back-end integration of Nok? to Amazon Web Services [ AWS ], taking advantage of its superior functionality and reliability from the biggest cloud provider by market share. This completion enhances the Nok? product line by utilizing AWS's superior security features, artificial intelligence [AI], and the Internet of Things [IoT].

This expands its accessibility and worldwide coverage, allowing device control based on real-time cloud technology and optimizing the user's experience with enhanced data synchronization and low latency. Management has boasted that ever since its complete integration, Nok? has experienced significant improvement in processing time as it drastically shortened by half. This could not have been done without AWS's revamp of database structure, code upgrades, and internal architecture changes.

I believe JBI's strategic decision to integrate its back-end with AWS will drive its future growth, as these enhancements will improve customer retention as well as attract new ones for JBI. If customers can enjoy better cloud connection, performance, and quality assurance as a result of this adoption, it will definitely strengthen its competitive position in the self-storage industry, which leads to a better growth outlook.

Discounted Cash Flow Model Valuation

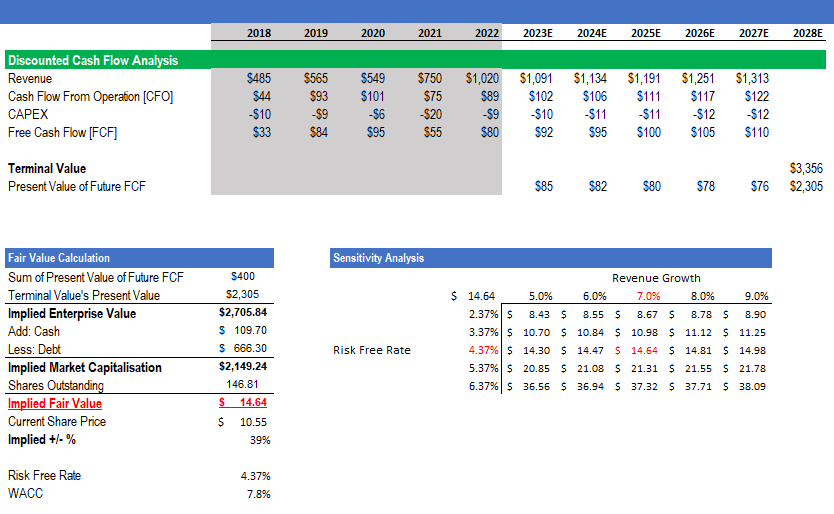

In order to determine if JBI is fairly valued, I used a simplified 5-year DCF model with a terminal value exit to determine its intrinsic value. In this section, I will walk you through the assumptions I have used in my DCF model. For 2023 and 2024, JBI's revenue growth is in line with the market consensus of ~7% and ~4% growth, respectively. Given the rising mortgage rate environment, collaboration with Extra Space, and back-end integration into AWS that I have discussed in depth above, I believe these drivers support these growth estimates, and I find them to be reasonable. For 2025-2027, I expect growth rates to be somewhat in line with 2024's growth estimates. Therefore, my model uses ~5% for these remaining years. In addition, this growth assumption ensures that my DCF model stays conservative.

JBI's 5-year median CFO as a percentage of revenue is ~13%. In my model, I utilized its most recent financial year's percentage of ~9%, and I extrapolated for the next 5 years. As it is below its median, I believe my CFO assumption is conservative.

For CAPEX, its 5-year median was 10% of revenue, and I used this rate for the next 5 years to ensure consistency. When I deduct CAPEX from CFO, it will give us FCF, and I will discount FCF back to its present value using JBI's WACC of 7.8%.

To calculate the terminal value, I require a risk-free rate. The US 10-year Treasury yield provides a good proxy for this, and it is 4.37%. Using 2027's FCF, WACC, and risk-free rate and applying them to the Gordon Growth formula, my terminal came up to $3.356 billion, or a present value of $2.305 billion.

Using JBI's WACC to discount its future FCF, the sum of the present value of its future FCF is $400 million. Hence, by adding the present value of its FCF and terminal value, its implied present enterprise value is $2.705 billion. Based on my conservative assumptions discussed above, my implied intrinsic value for JBI is ~$14.64. Compared to its current traded price, there is an implied upside of around 39%. As my DCF model indicates that JBI is undervalued, I recommend a buy rating for the stock.

{kind=link}

Downside Risk To My Buy Rating

I identified a potential downside risk to my buy recommendation. Firstly, while I discussed that US mortgage rates are currently boosting demand for self-storage due to individuals downsizing their houses, this trend might potentially invert if the mortgage rate declines due to cooling inflation. In this scenario, housing demand will adjust to the new mortgage rates. If individuals start to rent or buy larger houses, it will dampen demand for self-storage.

Secondly, while I discussed the strength of JBI's integration of AWS, this integration into third-party software creates dependency risk for JBI. When JBI uses a third-party system, it effectively loses control of the decision-making process, such as the ability to upgrade or refine the system as and when they like.

Conclusion

In conclusion, JBI's historical financial performance has shown that it is able to maintain consistent gross margins while at the same time improving its operating and net margins through effective cost management, even though it is operating in a high inflationary environment. Over the years, it also managed to bring its debt levels down effectively, which reduced its liquidity risk.

I believe the current rising US mortgage rate environment will continue to drive demand for self-storage. In addition, the self-storage market is also expected to grow until 2028. In addition, the announced collaboration with Extra Space to increase the install base of its Nok? product is intended to further strengthen this product's robust growth.

My DCF model, which uses conservative assumptions, indicates that JBI is undervalued. With a potential upside of ~39%, I recommend a buy rating for JBI stock.

For further details see:

Janus International: Growth Bolstered By Rising Mortgage Rates, Extra Space Collaboration, And AWS