JBGS - JBG SMITH: Time To Buy This Beaten Down REIT

2023-11-11 00:40:40 ET

Summary

- JBG Smith Properties shares have underperformed the S&P 500 and the real estate sector over the past 5 years.

- JBGS has been focused on shifting its business mix to be more balanced between commercial and multifamily properties.

- The company has been aggressively repurchasing shares, indicating confidence in its position and sending investors an important signal about valuation.

- I am initiating JBGS with a buy rating.

Shares of JBG Smith Properties ( JBGS ) have proved a challenging investment of late. Over the past 5 years, JBGS shares have delivered a total return of -59% compared to a total return of 69% delivered by the S&P 500 during the same period. JBGS has also faired poorly compared to the real estate sector specifically. The real estate sector can be proxied using the iShares US Real Estate ETF ( IYR ) which has delivered a total return on 12% over the past 5 years.

JGBS has performed roughly inline with office REITs Vornado Realty Trust ( VNO ) and SL Green ( SLG ).

Unlike most other REITs, JBGS has used the drop in its stock to aggressively repurchase stock and views this as the most efficient use of capital.

I believe JBGS are attractive at current levels and represent a buying opportunity.

]

Company Overview

JBGS is a REIT that owns and operates a portfolio of commercial and multifamily assets in and around the metropolitan area of Washington, D.C.

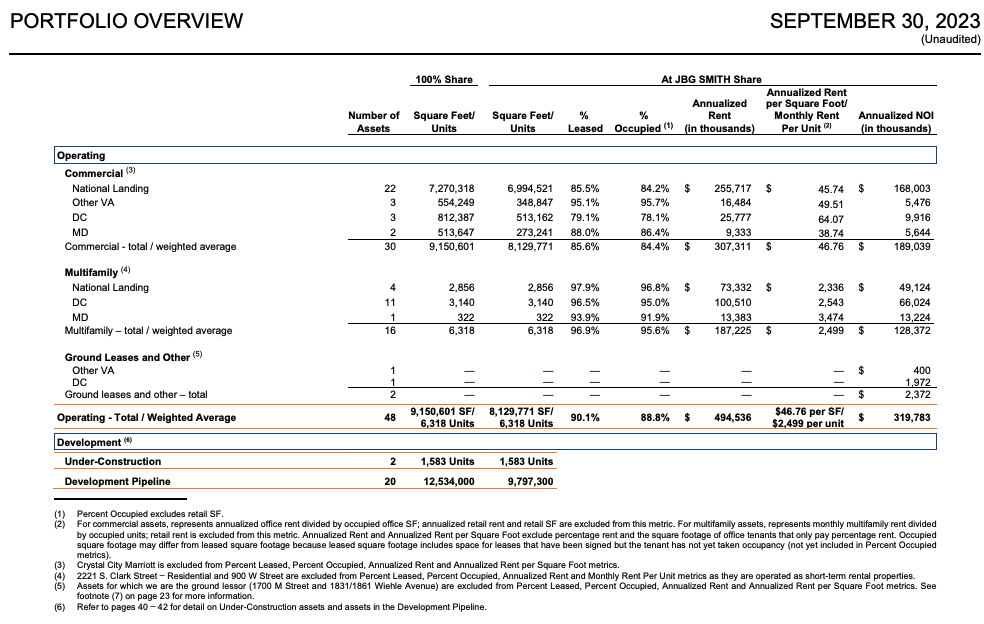

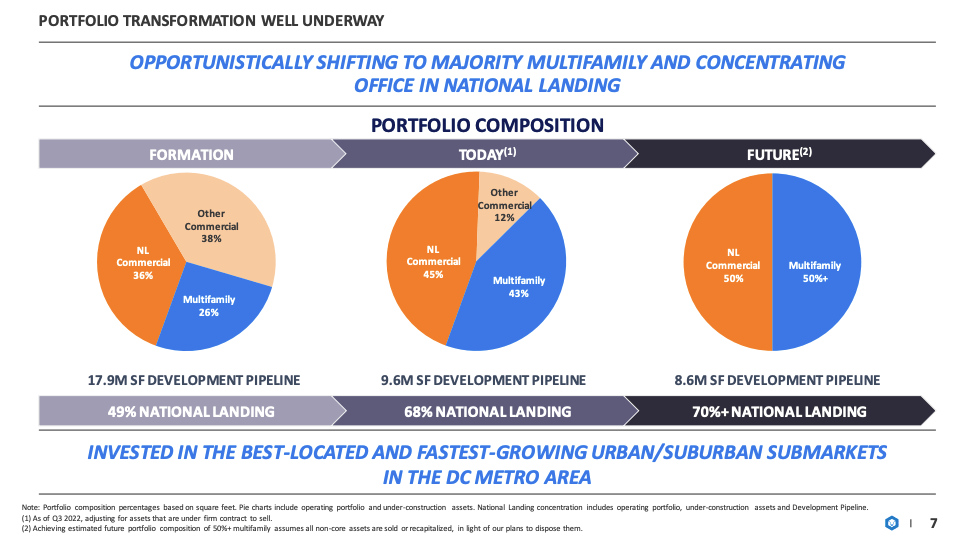

Currently, the company is weighted more heavily towards the commercial side (which is heavily focused on office) of the business which has a footprint of ~8.1 million square feet. The commercial side of the business currently accounts for ~59% of net operating income ("NOI"). The multifamily part of the business includes 6,318 units and represents ~40% of JBGS's NOI.

Over the past few years, JBGS has been focused on shifting its business mix to be more balanced between multi-family and commercial. Additionally, JBGS has been shifting exposure to focus more on the national landing, an area in Northern Virginia which has become home to Amazon's HQ2.

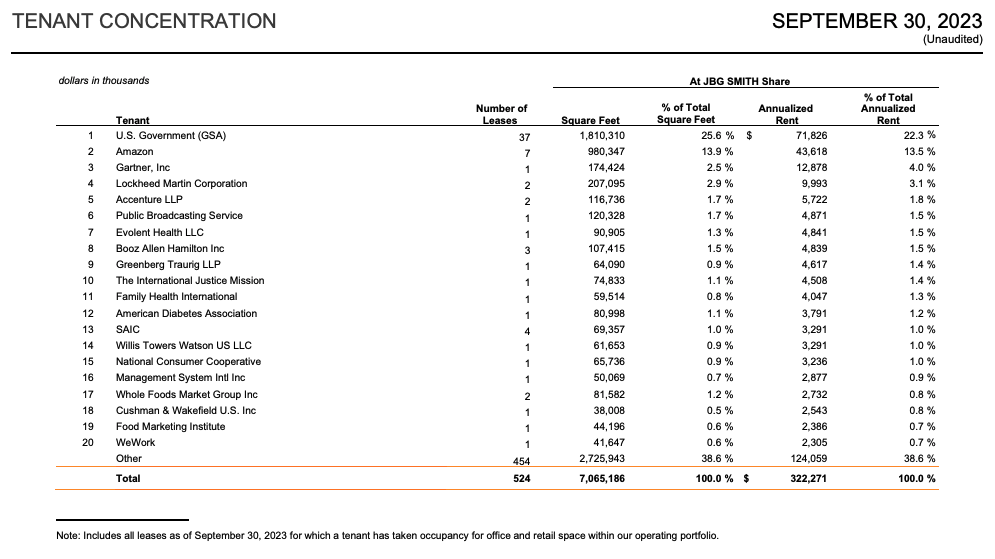

JBGS tenant base is well diversified with the two largest tenants being the U.S. Government (25.6% of total square feet) and Amazon (13.9% of total square feet). No other tenant accounts for more than 2.9% of total commercial square footage.

JBGS Investor Package JBGS Nov 2022 Investor Presentation JBGS Investor Package

{kind=link}

{kind=link}

{kind=link}

Resilient Financial Performance

Despite a very challenging office real estate market, JBGS has continued to post solid results.

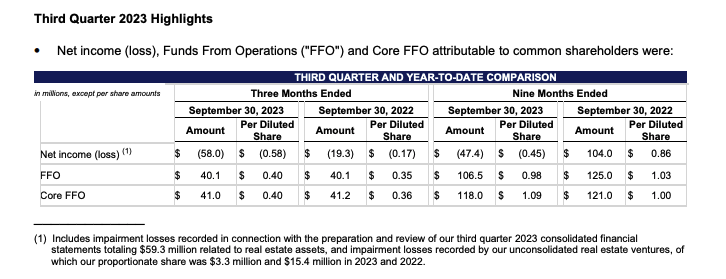

For Q3 2023, JBGS reported quarterly Core FFO per share of $0.40 vs $0.36 during the same period a year ago. Moreover, the $0.40 of Core FFO represents an 11% increase from Q2 2023.

On a year to date basis JBGS reported Core FFO of $1.09 per share up from $1.00 during the same period a year ago and $1.04 during the same period for 2021.

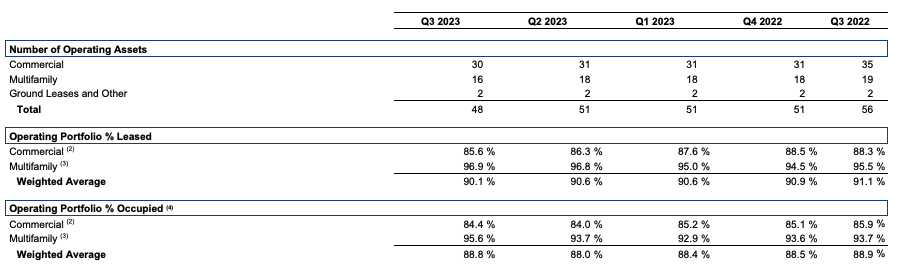

Despite a challenging operating environment in office, JBGS reported that 84.4% of its commercial operating portfolio and 95.6% of its multifamily operating portfolio was occupied as of Q3 2023. It is important to note that these occupancy levels represent an increase from the 84.0% and 93.7% commercial and multifamily operating portfolio occupancy during Q2 2023.

The increased occupancy levels and Core FFO per share vs the prior quarter suggest the company may have turned the corner and Core FFO may begin to rise from here.

JBGS Investor Package JBGS Investor Package

{kind=link}

{kind=link}

Positive Washington, D.C. Metro Trends

In its recent Q3 2023 earnings package, JBGS provided color which suggests potential near-term strength in the DC rental market:

Rent growth in the DC market was modest at 1.1%, but outpaced the other gateway markets which only grew 0.4%. DC's new supply pipeline market-wide (6%) according to CoStar is also less than some of the sunbelt markets like Austin (15%), Nashville (12%), or Jacksonville (10%) which should also help our rent growth on a relative basis. Finally, high home prices in our market, coupled with high interest rates and extremely low production, should keep renting even more in-favor than in lower cost sunbelt markets with more permissive new construction environments.

From a micro market perspective, we believe there is a positive story in the medium term resulting from limited go forward new deliveries. Markets like the Ballpark and Union Market in DC, after several years of large-scale deliveries, now have just one project under construction between them, according to CoStar data. With new supply unlikely to start in the near term, and continued strong absorption, it is likely that these markets and their mixed-use amenity-rich environments will be able to drive rent in the future. The same goes for National Landing where we control nearly the entire under-construction pipeline with just one 500-unit asset under construction in between Crystal City and Potomac Yard outside our control.

JBGS also highlighted positives relating to the national landing office market:

In National Landing, much of our leasing activity comprised two large Amazon five-year renewals: 100% of the office component, approximately 260,000 square feet, at 1770 Crystal Drive, and 88,000 square feet at 241 18th Street South. Looking ahead, we expect our demand drivers in National Landing to help us capture an outsized share of new demand within the market. This is especially evident when looking at GSA tenants and government contractor concentration in the submarket, and we expect these tenants, which account for 44% of our annualized rent, will continue to be a sticky form of office demand despite the macroeconomic environment. Mission critical GSA agencies in National Landing comprise 87% of our GSA tenancy, and 96% of our government contractor tenants are located in National Landing.

High Leverage Levels

One of the reasons why JBGS shares have performed so poorly is the fact that the companies remains highly levered. As of Q3 2023, the company reported a total of ~$2.47 billion of Net Debt, a total Net Debt/Total EV of 60.5% and Net Debt to Annualized Adjusted EBITDA of 8.1x.

The company's weighted average debt maturity stands at 4.0 years after adjusting for extension options. JBGS's exposure to rising rates is currently limited as 90.8% of the company's debt is fixed or hedged. However, the company is exposed to a potential increase in interest rates when it needs to refinance existing debt.

While the company's debt load is high, I believe it does have levers necessary to deal with any potential refinancing challenges as much of the debt is non-recourse in nature which means the company could walk away from certain uneconomic assets. JBGS also asset sales as a tool to de-lever. During Q3 2023, JBGS closed on $141.8 million of non-core asset dispositions and used the proceeds to deleverage its balance sheet.

Focus on Share Repurchases

As shown by the chart below, over the past three years JBGS has been aggressively buying back shares. The result is that JBGS has steadily reduced its shares outstanding by ~21% over the past 3 years. Comparably, other big office REITS such as SL Green ( SLG ), Vorndao ( VNO ), and Boston Properties ( BXP ) have not implemented significant buybacks.

In its Q3 2023 earnings release JBGS said that share repurchases continue to be the most accretive use of capital available given the material discount to NAV. On a YTD basis, JBGS has repurchased 20.5 million shares at a weighted average price of $14.87 per share totaling $304.7 million.

I believe the significant amount of share repurchases over the last three years suggests that JBGS is highly confident in its position. The company has a very strong understanding of its portfolio and the actual asset values compared to what the market is pricing in.

Dividend

While office focused REITs such as Vornado and SL Green have been forced to cut or suspend their dividends, JBGS has been able to maintain its dividend. JBGS shares currently yield 6.52% and receive a dividend safety rating of C- from Seeking Alpha quant scores.

While the company appears committed to the dividend, it has also noted that it could adjust its dividend to preserve cash while continuing to cover taxable income distribution requirements. Thus, I would not be surprised to see a dividend cut at some point as the company may want to find ways to reduce debt or increase its buyback.

Seeking Alpha

Valuation

As shown by the table below, JBGS trades at 11.8x 2024 consensus FFO per share. This represents a premium to office focused REITs such as VNO, SLG, and BXP. However, this multiple represents a significant discount to Elme Communities ( ELME ) which is a multifamily focused REIT with a heavy DC concentration.

Thus, based on a relative valuation JBGS appears reasonably valued vs peers given the company's split between office and multifamily.

JBGS appears attractively priced relative to its historic valuation range. Moreover, the fact that the company has been aggressively buying back shares serves an important indictor since they have the best sense of the prospects for the company moving forward.

{kind=link}

{kind=link}

Growth Expectations

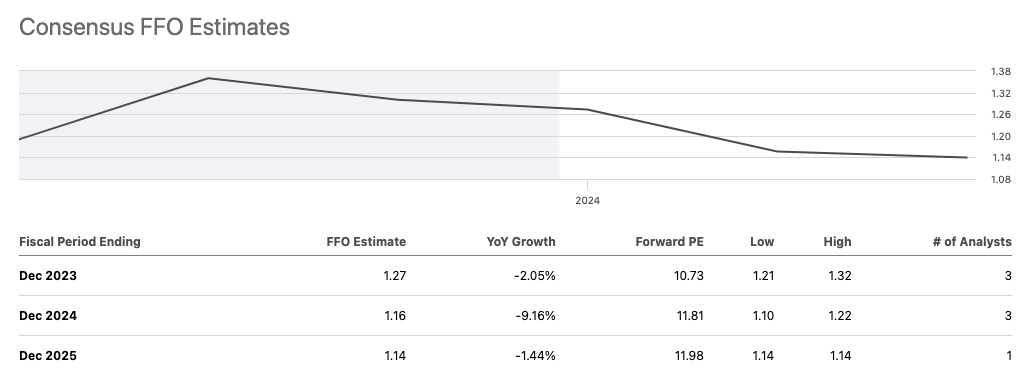

Currently, consensus estimates call for JBGS to report FFO of $1.17 for FY 2024 and FFO of $1.14 for FY 2025. This compares to FFO of $1.39 for FY 2023.

I believe the company will be able to beat these estimates and deliver at least stable FFO from FY 2023 levels for 2024 and 2025. The company expects leasing at its 1900 Crystal Drive, a two residential tower development in National Landing totaling 808 units, to commence in early 2024. Given a total multifamily footprint of 6,300 units this development marks a major increase in rentable space.

During Q3 2023, the company generated 12.2% and 10.5% same store multifamily NOI growth for the three and nine months ending September 30, 2023. I expect this growth to continue going forward on the existing portfolio.

On the commercial side, I believe we will continue to see an upswing in occupancy rates due to return to office policies which will drive improved performance from the commercial side of the business as well.

Risks To Consider & The Bear Case

JBGS is uniquely focused on the Washington, DC metro area real estate market. While the company is diversified across both the commercial and multifamily segments, it remains highly exposed to any specific downturn in the Washington, DC real estate market.

While the DC real estate market tends to be more resilient to recessions given the large government footprint it could face headwinds in the event of significant government spending reductions leading to job cuts. I view this as unlikely but it a risk investors must consider.

The bear case for JBGS, like other office focused REITs, is that work from home is here to stay and occupancy rates will continue to decline from current levels. The bears believe that JBGS will be forced to cut its dividend due to lower FFO as office occupancy rates and rents sink going forward. Under the bear case declining FFO will make it difficult for JBGS to manage its highly levered balance sheet.

A further decline in the office real estate market does not appear to be the trend given increasing return to office mandates over the past few months. Moreover, the tick up in occupancy rates that JBGS reported vs the prior quarter also serves as a positive indicator that the office market may be turning. Finally, JBGS has a strong multifamily business which is growing and will allow the company to navigate any prolonged period of office market weakness.

Conclusion

JBGS is a unique REIT in that is exclusively focused on the Washington, DC metro area. This concentration allows management to be highly focused on the opportunities at hand in that market.

Shares of JBGS have sold off over the past few years due to office market headwinds related to workplace changes following COVID-19. Additionally, REITs more generally have faced a challenging environment due to rising interest rates.

JBGS has used the drop over the past few years to implement a significant share repurchase program which has reduced the share count my more than 20%. Management has said it continues to see share repurchases as the most effective use of capital. This capital allocation strategy stands out vs other office REITs which have not focused on repurchasing shares.

JBGS has a highly levered balance sheet but has hedged most of its interest rate risk. Moreover, the company has been actively selling non-core assets in a bid to reduce leverage.

JBGS appears to be trading at a reasonable valuation relative to its peers and cheap relative to its historic norm. I believe management's focus on buying back shares despite industry headwinds is an important datapoint regarding valuation as they likely have the best insights regarding the company's prospects.

I am initiating JBGS with a buy rating and would consider downgrading the stock in the event it moved significant highly from here. Additionally, I would consider downgrading the stock in the event the Washington, DC real estate market experiences a significant headwind.

For further details see:

JBG SMITH: Time To Buy This Beaten Down REIT