PHD - JFR: Attractive Discount And Fully Covered ~12.7% Distribution Yield

2023-11-27 00:57:26 ET

Summary

- JFR merged with three of its sister funds earlier this year, which were all focused on floating rates or holding a short-duration fixed-income portfolio.

- This combination made JFR the largest floating-rate focused fund in the closed-end fund space, larger hasn't meant necessarily better though.

- The fund's discount appears attractive and the distribution rate is fully covered; however, its performance has been a bit lackluster relative to some peers.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Earlier in 2023 , Nuveen Floating Rate Income Fund ( JFR ) became significantly larger. This was through the merger of three other similar Nuveen closed-end funds with and into JFR. Those included the Nuveen Senior Income Fund, Nuveen Floating Rate Income Opportunity Fund and Nuveen Short Duration Credit Opportunities Fund.

Those funds were also focused on floating-rate investments, so there wasn't necessarily a material change. Those funds were all included on the previous consolidated semi and annual reports prior to the merge. As one of the largest floating rate-focused funds trading at a deep discount, there could be some appeal here. Investors expecting a higher for longer interest rate environment could stand to benefit from remaining invested in floating-rate securities.

The Basics

- 1-Year Z-score: -0.27

- Discount: -11.50%

- Distribution Yield: 12.69%

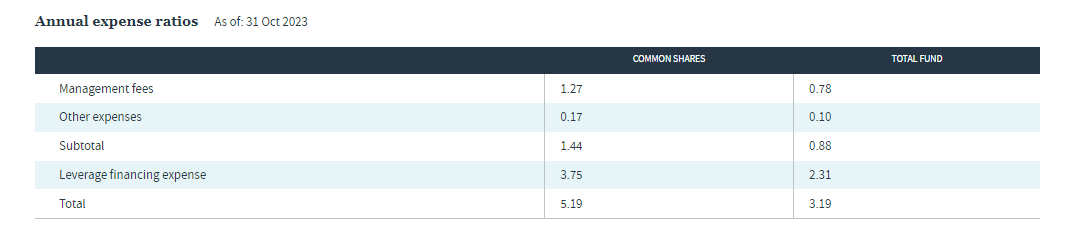

- Expense Ratio: 1.44%

- Leverage: 38.26%

- Managed Assets: $1.992 billion

- Structure: Perpetual

JFR's investment objective is to "achieve a high level of current income." To achieve this, they will "invest in a portfolio of adjustable-rate senior loans and other debt instruments." More specifically, they note that "at least 80% of its managed assets will consist of adjustable rate loans; at least 65% of these must be senior loans secured by specific collateral."

Larger Means Better?

One of the benefits that fund sponsors usually tout is that the combined fund can have a lower expense ratio. However, as noted by Stanford Chemist , this was an incredibly small benefit of around 5-6 basis points.

Sometimes, the benefit isn't even that large. In fact, JFR might not show quite the improvement that they believed it could on a pro forma basis. The reason for this is that last year, JFR's expense ratio was 1.37%, and the last annual report showed the expense ratio at 1.49%. That being said, the closing was on the last day of the fiscal year, but considering that the expense ratio rose for JFR, chances are it increased for the other funds, too.

So, investors looking forward to that next report and expecting a drop may want to temper expectations. We can also look at the fund's website, which shows that the operating expenses as of October 31, 2023, are at 1.44%. That, too, indicates that the expenses just rose post-merge rather than decreased from where they were before.

{kind=link}

The only way it would have reduced materially is if the managers took a pay cut. The fund, also being at around $1.992 billion as of the time of writing, is also suspiciously right below the final breakpoint for the reduced management fee rate. If assets can rise (preferably not from adding further leverage,) then at least a small portion could be over the breakpoint and eligible for the reduced management fee.

JFR Management Fee Breakpoint (Nuveen)

{kind=link}

When looking at the total expense ratio of the combined fund, which includes the leverage, the expense ratio has climbed to 4.77% from 2.17%. Of course, this would be driven by the higher borrowing costs that the fund is experiencing, but that's been offset by the floating rate exposure this fund carries. The management team doesn't have to hedge interest rates directly because their portfolio is a natural hedge, as they have also experienced higher yields.

Still, with a leverage ratio pushing nearly 40%, that's something to consider before jumping into this fund. It can help the fund perform better during good times and generate higher income, but it's a double-edged sword. Should things start to fall, the downside is also amplified.

Instead, a larger fund's main benefit is really more liquidity for investors. On their own, each of these funds was fairly small, and that can mean larger investors would have a harder time getting in or out of funds. The average trading volume for JFR comes to 616k shares a day, or close to about $5 million being swapped. That becomes the primary benefit, so in that regard, then yes, larger could be better.

Higher Net Investment Income Thanks to Portfolio

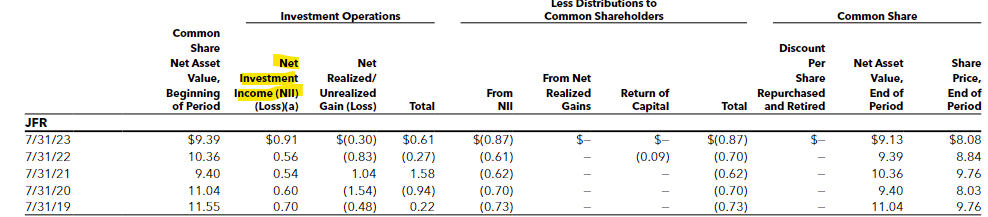

Given the mention of the higher yields of the portfolio offsetting the higher costs of the leverage, it is great to see that has taken place. In its latest report, the fund's net investment income per share climbed to $0.91 for the fiscal year 2023 from $0.56 for fiscal 2022. Looking at the per-share basis will give us a better idea going forward now that the fund has gone through this merger.

JFR Net Investment Income (Nuveen (highlight from author))

{kind=link}

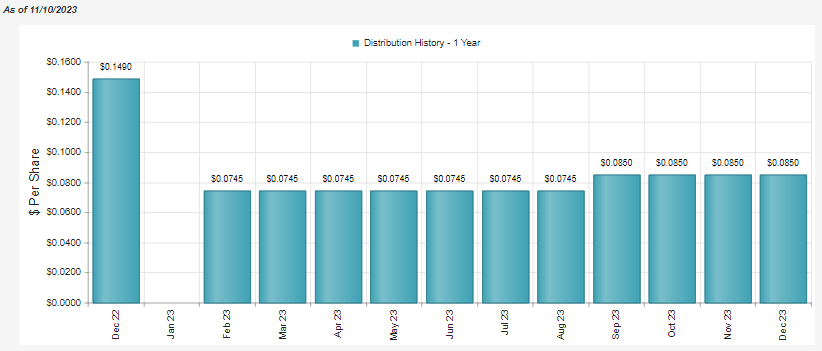

JFR, like many senior loan-focused funds, had been increasing its monthly distribution. Post-merger, the fund received an even larger bump to $0.085 per month.

JFR Distribution History (CEFConnect)

{kind=link}

Based on the latest NII and the annualized distribution amount of $1.02, it does mean coverage was on the lighter side, with NII coverage around 90%.

That being said, the fund's more recent coverage put the average earnings for the last three months at $0.0853, which would bump it back up to being covered. That provides investors with a pretty solid distribution rate of 12.62%, which is being fully covered. That's up from the 11.17% NAV rate, thanks to the fund's discount bumping it up a bit on a share price basis.

Discount Presents Opportunity, But Performance Is Looking Relatively Sour

Speaking of discounts, one of the more appealing features of JFR currently as well, as the fund is trading below its longer-term average.

Ycharts

Though it more recently is trading about in line with its 1-year average. Despite the larger fund size, it doesn't appear to have generated further interest in the fund. This is also another point that the management team mentioned could be a benefit for the fund. A narrower discount because historically, JFR's discount had traded at a reduced discount.

In comparison with some peers, JFR is one of the more discounted, along with Pioneer Floating Rate Trust ( PHD ). I've also included Invesco Senior Income Trust ( VVR ) and BlackRock Floating Rate Income Strategies Fund ( FRA ), as they are relatively comparable senior loan funds.

Ycharts

At the same time, over the last year, JFR has been the weakest of these funds. In fact, it seems it has started to perform even worse as the funds combined, and that is around when they started to diverge away from this basket.

Ycharts

If we want to look more specifically, we'll give the performance a look between JFR and this basket of peers from July 31, 2023, to today. This does highlight the weaker relative total NAV return performance.

Ycharts

This hasn't been just a short-term problem either. The fund's performance has been fairly lackluster in the last decade as well, coming up the shortest on a total NAV return basis once again.

Ycharts

That doesn't tell us what will happen in the future, and JFR's discount is relatively attractive compared to VVR, which is trading near parity with its NAV. The discount for JFR is also a bit wider than the FRA. Though going back to highlighting the leverage with JFR pushing near 40%, FRA is at around 24.3%, and VVR is also carrying a lower leverage ratio of around 33.3%. Meaning they have been able to do more with less.

With that being said, the fund's portfolio also carries some corporate bond exposure. That could explain some of the weakness as bonds are more interest rate sensitive than senior loans. FRA carries around 97.5% of bank loan exposure. However, VVR also lists around 85% in bank loans, with bonds at around 5.5% and, interestingly, nearly 8% in equities. So, each has its small quirks.

JFR Asset Allocation (Nuveen)

The average effective duration of JFR was listed at 0.45 years, whereas FRA is at 0.23 years for some context. On an absolute basis, that doesn't seem like much, but on a relative basis, it's nearly double. When the 10-Year Treasury Rate was spiking higher in October, it was really when we could see JFR start to falter, so that could explain at least some of the performance we are seeing.

Conclusion

JFR was merged with several of its sister funds earlier this year and now is the largest senior loan closed-end fund. The fund carries a fairly deep discount as it trades below the fund's long-term average discount. However, the performance of the fund has been relatively weaker than some of its peers. That could be stemming from having some exposure to corporate bonds that make the fund a bit more interest rate sensitive in a period where rates were rising rapidly. Going forward, the larger discount compared to some of its peers could be enough to see it perform better. Additionally, the fund's small sleeve to bonds could see it outperform going forward if rates fall. Of course, that assumes that they also continue to hold a small weighting to bonds.

For investors looking for income, this isn't necessarily a bad choice either, given the fact that it is running with a ~12.7% distribution rate that is now being fully covered. Similar to any other senior loan funds, should rates come down, then coverage would start to sink. That's why senior loan funds have a lot of distribution adjustments over time relative to some other CEFs that invest in other areas of the market. With that being said, JFR would be more appropriate for investors who are expecting a higher for longer rate environment.

For further details see:

JFR: Attractive Discount And Fully Covered ~12.7% Distribution Yield