JFR - JFR: The Thesis Is Holding True For This 10%-Yielding CEF

Summary

- Floating-rate fixed-income securities should hold their value better than traditional bonds during periods of rising interest rates.

- Nuveen Floating Rate Income Fund invests primarily in a portfolio of these securities, so it should be a reasonably good choice for income in today's environment.

- The closed-end fund has held up quite well over the past three months, providing support to our thesis.

- JFR raised its distribution twice in the past year, which should be pleasing to those looking to overcome inflation, as it is one of the only funds with a positive real return.

- The CEF is trading for a very attractive valuation today.

One of the biggest problems facing Americans today is the pervasive inflation that has been pushing up the cost of living all across the country. This problem has gotten so bad that it has forced many people to take on second jobs or enter the gig economy just to get the money that they need to feed themselves and cover their rising utility bills. Fortunately, as investors, we do not have to go to this extreme and have other options available to us to increase our incomes. One of the best options available to accomplish this is to invest in a closed-end fund ("CEF") that specializes in the generation of income. This is because these funds provide easy access to a professionally-managed portfolio of assets that can in most cases deliver a higher yield than pretty much anything else in the market.

Unfortunately, most income-focused closed-end funds invest in the fixed-income sector. As everyone reading this is no doubt well aware, the Federal Reserve began aggressively raising interest rates back in March 2022 in an effort to reduce the inflation rate. This has had the effect of pushing down the price of fixed-income securities, which dealt a punishing blow to some funds. Fortunately, there is a way around this. That is to invest in a fund that specializes in floating-rate fixed-income securities. As the name implies, these securities benefit from rising interest rates as the borrowing company has to pay more in interest when rates rise. Thus, floating-rate securities should hold their value reasonably well during a monetary tightening period like what we are seeing today.

In this article, we will discuss the Nuveen Floating Rate Income Fund ( JFR ), which is one fund that specializes in these securities. The fund certainly does not sacrifice any income potential either, as it yields 10.92% at the current price. When we combine this with an attractive valuation, there certainly appears to be a lot to like here.

As some readers may recall, I discussed this fund previously, but a few months have passed since that time so a few things have changed. This article will, therefore, focus specifically on those changes as well as provide an updated analysis of the fund’s finances so that we can determine if this high-yielding fund could be a good addition to your portfolio today.

About The Fund

According to the fund’s webpage , the Nuveen Floating Rate Income Fund has the stated objective of providing its investors with a high amount of current income. This is hardly surprising considering that the name of the fund alone indicates that it would be investing its assets in a way that is intended to produce an income. The fund seeks to achieve its objective by investing in floating-rate securities, which would support this objective since these securities are not going to have huge potential for capital gains. This is because they have no real link to the growth and prosperity of the issuing company. Rather, like all fixed-income securities, these securities trade based on interest rates.

In short, when interest rates increase, fixed-income securities decline in value and vice versa. This is because the yield provided by newly-issued securities will be based on the prevailing interest rate. Thus, during periods of rising interest rates, nobody would buy an already existing security since a newly-issued one that is otherwise identical would have a higher yield. The same thing happens when interest rates decline as investors attempt to buy up existing securities that have a high yield. Thus, the price of existing securities will adjust until they deliver the same yield-to-maturity as an already existing security.

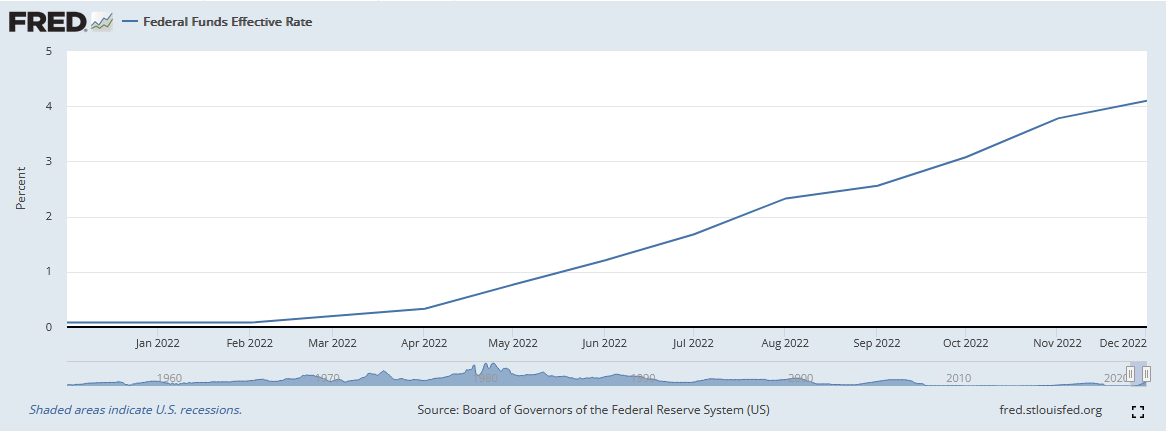

The twist that this fund provides is that it does not invest in traditional fixed-income securities. Rather, the fund buys floating-rate securities. As the name implies, these securities change their coupon payments based on some market benchmark (usually LIBOR plus a spread). Thus, they should hold their value during times of rising interest rates since they will still have a yield that is comparable to newly issued securities. This is something that is rather important today since the Federal Reserve has raised the federal funds rate since we last looked at the fund. As of the time of writing, the federal funds rate sits at 4.10%, a marked increase from the 3.08% that prevailed in October:

{kind=link}

In addition, the Federal Reserve is planning to raise rates further than was expected when we last looked at the fund. According to the latest survey , the Federal Reserve is expected to take rates to 5.25% to 5.5% in 2023. This is a marked increase from the 4.60% that was projected back in October. Thus, it could be a good idea to hold assets that increase their yield as rates increase in order to reduce our risk as investors.

This fund certainly does a good job of holding floating-rate loans per its mandate. Currently, 83.7% of the fund’s assets are invested in these securities:

Nuveen Investments

This is something that is quite nice to see, although the 13.5% allocation to corporate bonds will likely be a bit of a drag on the fund as these will go down in value when interest rates rise. The same may apply to the common stocks and the asset-backed securities that are held by the fund. However, all of these things account for less than 20% of the portfolio so it should still hold up much better than a fund that invests solely in traditional fixed-income securities.

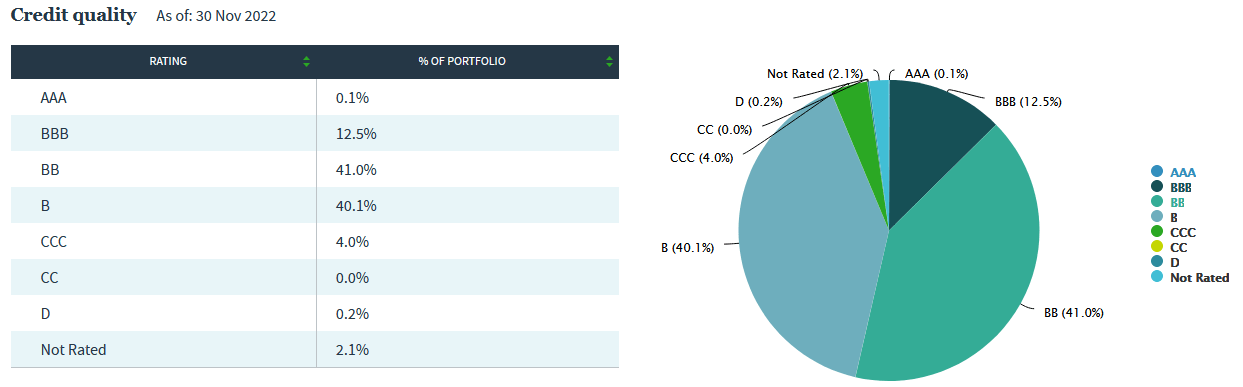

One thing that might discourage risk-averse investors, though, is that floating-rate loans are often issued by companies that already have fairly high levels of debt. Thus, these companies are generally considered to be at higher risk of default than a company issuing a traditional investment-grade bond. We can certainly see this by looking at the credit ratings of the issuers whose securities are in the portfolio:

{kind=link}

An investment-grade security is anything rated BBB or higher. As we can see, these only account for 12.6% of the fund’s portfolio. This is a much higher percentage than the last time that we looked at the fund, but it is still probably lower than many conservative investors would like to see. After all, we have all heard horror stories about junk debt being risky to hold because there is a high probability of not getting your money back. However, we can see that fully 81.1% of the fund’s assets are invested in BB or B-rated securities. These are the two highest ratings of speculative debt and according to the official bond rating scale , a company with either of these ratings has a strong enough balance sheet to cover its debt even through a short-term economic shock. They might be a bit vulnerable to a prolonged economic downturn but we have not seen one of those since the Great Depression. Thus, we should not really have to worry too much about defaults here.

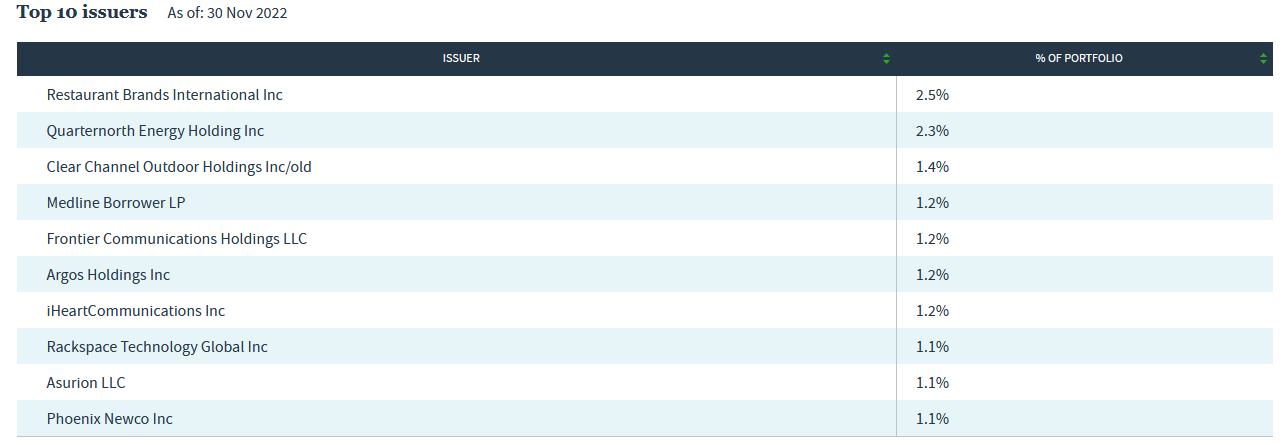

In addition to investing is reasonably highly-rated, albeit speculative-grade, companies, the Nuveen Floating Rate Income Fund lowers its risk of losses due to defaults by ensuring that no individual company accounts for too much of its portfolio. We can see this quite clearly by looking at the largest positions in the fund. Here they are:

{kind=link}

As we can see, even the largest position in the fund only accounts for 2.5% of its total assets. This is a bit higher than I may want to see, but it is still acceptable. The advantage that this provides is that any single default will only have a relatively small impact on the portfolio. While widespread defaults could still have a noticeable impact, that event would mean that the economy has far bigger problems than just a few fund investors losing money. More than likely, anyone invested in the fund will likely have more to worry about than their losses in that event.

There have been a few changes to the largest positions list since we last looked at the fund a few months ago. This is somewhat surprising, considering that this is a fixed-income fund. Here they are:

| Removed Company |

| Added Company |

| Delta 2 Lux Sari |

| Frontier Communications ( FYBR ) |

| Caesars Holdings ( CZR ) |

| iHeart Communications ( IHRT ) |

| Fertitta Entertainment |

| Rackspace Technology Global ( RXT ) |

| Jazz Pharmaceuticals ( JAZZ ) |

| Assurion |

It is quite rare to see so many changes to a portfolio over a short period of time, especially for a fixed-income fund. This may lead one to believe that the fund has a very high turnover rate. This is not actually correct, though, as the fund only has a 38.00% annual turnover. This is something that is fairly nice to see since it costs money to trade assets, which is billed to the shareholders. This creates a drag on the fund’s performance and makes management’s job somewhat more difficult. This is because management must generate sufficient returns to both cover these added expenses and still have sufficient left over to match or beat the benchmark index.

There are very few management teams that can consistently accomplish this goal, which is one reason why actively-managed funds tend to underperform comparable index funds. While there is a floating-rate security index (the Bloomberg U.S. Dollar Floating Rate Note <5 Years Index), that is very different than this fund, so it is not a useful point of comparison. Thus, we really need to evaluate the fund’s performance on its own merits.

Performance

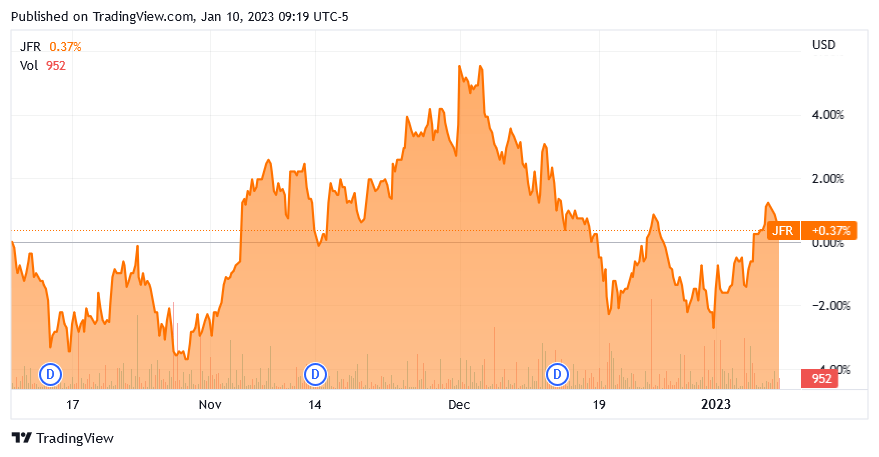

As I stated numerous times throughout this article, the Nuveen Floating Rate Income Fund should hold its value fairly well in the face of rising interest rates. That has certainly proven to be the case over the past three months. In fact, the fund is up 0.37% over the period:

{kind=link}

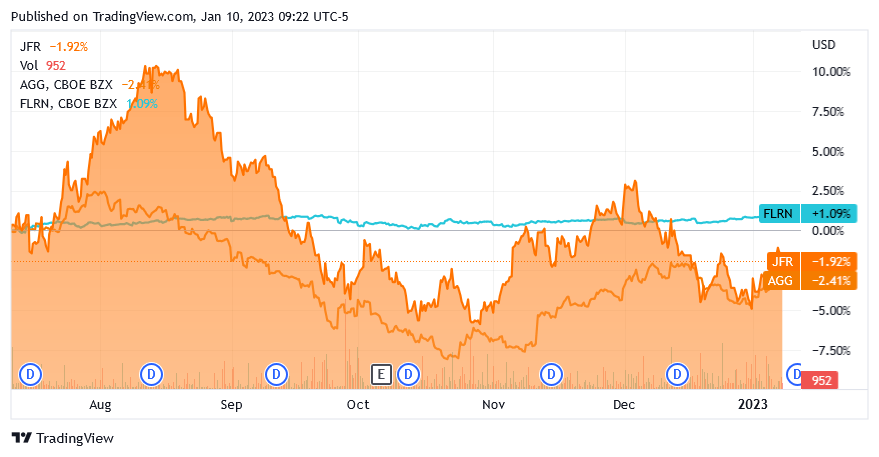

This is comparable to the floating-rate index ( FLRN ) that was mentioned earlier, although the Nuveen fund has a substantially higher yield so it delivered a much better total return. Curiously, the fund underperformed the Bloomberg U.S. Aggregate Bond Index ( AGG ) despite the latter consisting of traditional fixed-income securities dealing with rising index rates. Then again, the market has been rather irrational lately. The Nuveen closed-end fund did much better over the trailing six-month period, however:

{kind=link}

As we can see, the fund outperformed the regular bond index on any measure. While it did underperform the floating-rate securities index, the closed-end fund once again has a substantially higher yield so it actually delivered a higher total return over the period. In fact, the closed-end fund was the only one of these assets that actually delivered a positive real return since it was almost flat and has a yield that beat the 7% inflation rate that we saw over the period. Clearly then, the fund is generally meeting the requirements of our thesis. When we consider that the Federal Reserve is likely to continue to raise interest rates over the next few months, if not longer, the case for this fund becomes even more pronounced.

Leverage

As stated in the introduction, closed-end funds have the ability to use certain strategies that allow them to pay out yields that exceed that of the underlying assets as well as just about anything else in the market. One strategy that is employed by the Nuveen Floating Rate Income Fund is the use of leverage. In short, the fund borrows money and uses that borrowed money to purchase floating-rate fixed-income securities. As long as the interest rate paid on the borrowed money is less than the yield of the purchased assets, the strategy works pretty well to boost the yield of the overall portfolio. As the fund is capable of borrowing at institutional rates, which are substantially lower than retail rates, this will usually be the case.

Unfortunately, the use of debt is a double-edged sword. This is because leverage boosts both gains and losses. This could be one reason why the fund has delivered much more violent price swings than the floating-rate index fund over the past six months. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I do not typically like to see a fund’s leverage exceed a third of its assets for this reason. The Nuveen Floating Rate Income Fund does exceed this level, however. As of the time of writing, the fund has $325.4 million in leveraged assets, which constitutes 38.27% of the portfolio. The fact that the fund invests in assets that should prove reasonably safe over a long-term horizon means that it can probably get away with more leverage than a normal equity fund so this is probably okay. We do want to keep an eye on it though and make sure that it does not start increasing its leverage much more.

Distribution Analysis

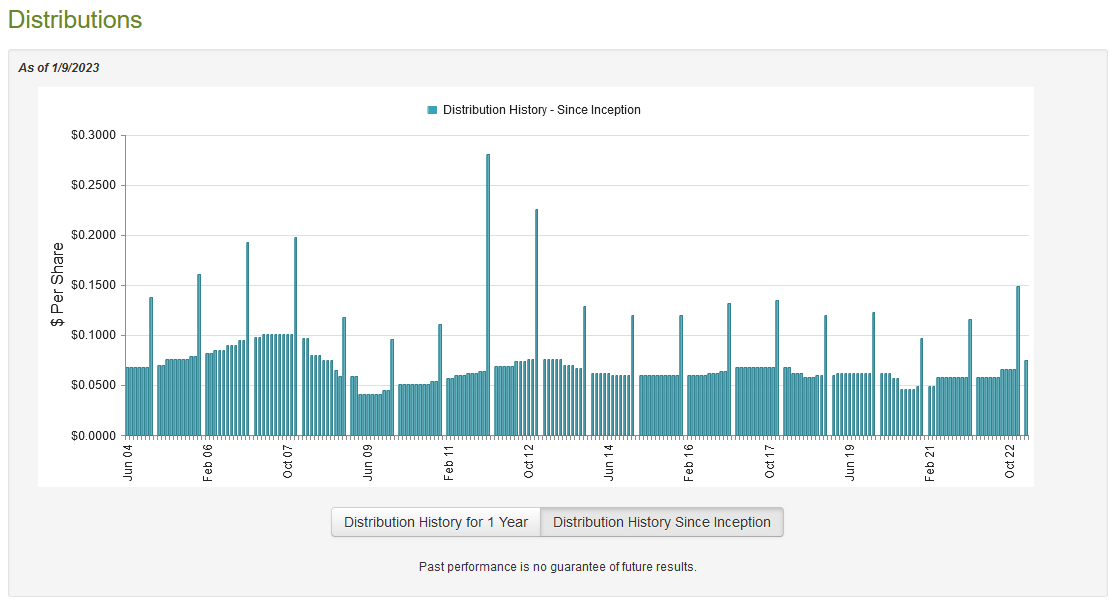

As stated earlier in this article, the primary objective of the Nuveen Floating Rate Income Fund is to provide its investors with a high level of current income. In order to accomplish this, the fund invests in a portfolio of floating-rate loans and then leverages them up in order to boost the yield. We can, therefore, safely assume that the fund boasts a very high yield itself. This is certainly the case, as the Nuveen Floating Rate Income Fund pays out a monthly distribution of $0.0745 per share ($0.894 per share annually), which gives it a 10.92% yield at the current price. The fund’s distribution has varied quite a lot over the years due to interest rates. Perhaps surprisingly, the fund is one of the few fixed-income closed-end funds that has increased its distribution twice in the past twelve months, including its most recent one last month:

{kind=link}

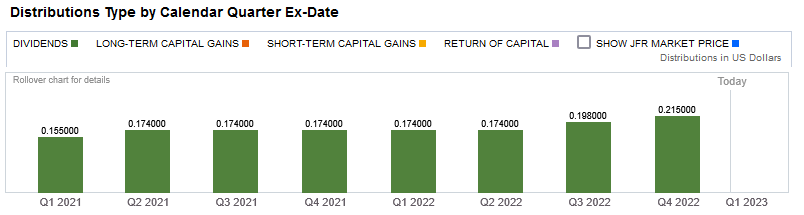

The fact that the fund’s distribution has varied so considerably over the years is likely to reduce its appeal somewhat in the eyes of those investors that are seeking a safe and secure source of income. However, the two distribution increases this year do support our thesis that this fund could be a good holding for periods of rising interest rates. Another thing that is nice is to see that the fund’s distributions are entirely classified as dividend income and contain no return of capital component:

{kind=link}

The reason why this may be somewhat comforting to see is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. In addition, a dividend distribution is typically paid for solely by the fund’s income so its sustainability is not dependent on the fund producing sufficient capital gains. As a result, these distributions tend to be the most sustainable. However, as I have pointed out before, it is possible for a distribution to be misclassified. As such, we want to investigate the fund’s finances and see exactly how sustainable the distribution is likely to be.

In my last article on this fund, the most recent document that was available to consult for this purpose was the fund’s full-year report for the period ending on July 31, 2022. That is still the most recent document available, so it is rather pointless to discuss the fund’s distribution sustainability again. In short, the fund failed to generate sufficient net investment income to cover its distribution and suffered net capital losses. Thus, it failed to cover its distribution during the first half of the year.

The fund currently has 56.918 million shares outstanding so the distribution at the new level costs the fund $4,240,391 per month or approximately $25,442,346 per half-year period. That is substantially more than the $2,645,615 net investment income that the fund had per month on average during the full-year period that ended on July 31 of last year. However, interest rates are significantly higher now so the fund is probably bringing in more money. We will want to scrutinize its semi-annual report when it comes out to see just how much the increase in net investment income has been. That report will be for the six-month period ending January 31, 2023, so it will probably be released sometime in March.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the fund’s shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. That is because such a scenario implies that we are purchasing the fund’s assets for less than they are actually worth. This is, fortunately, the case with the Nuveen Floating Rate Income Fund today. As of January 9, 2023 (the most recent date for which data is available as of the time of writing), the fund had a net asset value of $9.22 per share but the shares only trade for $8.24 per share. This gives the fund’s shares a 10.63% discount to net asset value at the current price. This is a bigger discount than the shares had the last time that we looked at the fund, although it is not as good as the 12.20% discount that the shares have traded at on average over the past month. Nevertheless, the current discount is a more than attractive price to pay for the shares today.

Conclusion

In conclusion, the Nuveen Floating Rate Income Fund could be one of the better fixed-income funds to hold today. This is because the fund’s assets should do a reasonable job of holding their value as the Federal Reserve continues its series of interest rate hikes. Nuveen Floating Rate Income Fund has performed admirably compared to index funds overall and it boasts a phenomenal 10.92% distribution yield due to its distribution being increased twice over the past year. While we do still need to ensure that the fund is properly covering its distribution, the fact that it is trading at a huge discount to net asset value provides a margin of error. Overall, Nuveen Floating Rate Income Fund looks very good right now.

For further details see:

JFR: The Thesis Is Holding True For This 10%-Yielding CEF