JPI - JPI: A Likely Alpha Opportunity For This Term Preferred CEF

2023-10-26 14:30:38 ET

Summary

- The Nuveen Preferred and Income Term Fund is a term closed-end fund that primarily invests in preferred securities.

- Investors are concerned about the fund's performance as it approaches its termination date next year, following the recent struggles of IHIT - another term fund.

- JPI has a relatively typical preferred CEF portfolio, with a focus on financials and a significant allocation to floating-rate securities and contingent capital bonds.

- Nuveen has been very good at managing funds through terminations and offering investors an exit at the NAV, making this opportunity more solid than the average term CEF.

In this article, we take a look at the Nuveen Preferred & Income Term Fund ( JPI ). JPI is a term CEF that allocates primarily to preferreds. Its attraction lies entirely in its likely discount amortization next year when it will likely offer investors an exit at the NAV - as previously happened with its sister fund JPT.

Investors who follow term CEFs were unpleasantly surprised by the recent behavior of another term fund - the Invesco High Income 2023 Target Term Fund ( IHIT ) which appears to be self-destructing on its way to termination. The key question is whether investors should expect a similar issue for JPI as we approach its own termination date in the second half of next year.

Fund Snapshot

JPI is a relatively typical preferred CEF. Around 80% of the portfolio is allocated to institutional securities, with the rest to retail (i.e. $25-"par") preferreds.

The fund carries exposure predominantly to financials - with banks and insurance companies being the largest sectors - again very typical of preferreds funds.

Nuveen

About 10% of the portfolio is in floating-rate securities and about a third is in contingent capital bonds - relatively high for preferred CEFs.

The Case for JPI

Term CEFs are an area of the market we pay a lot of attention to due to their potential to deliver a high amount of alpha for investors. Unlike most CEFs, which are perpetual funds, term CEFs have a scheduled termination date. When a CEF terminates, its discount will amortize to zero, usually providing a significant and riskless tailwind to returns.

Systematic Income

Of course, not all term CEFs terminate, unlike what many investors and analysts seem to believe. Some term CEFs have asked their shareholders to approve a conversion to a perpetual fund and have done so. Oddly enough, shareholders often vote arguably against their economic interests to approve the conversion and prevent the discount tailwind from happening.

Unlike other managers, Nuveen is unlikely to follow this path in our view, which is why we take their term CEFs much more seriously. For this reason, JPI is a fund that we have been focused on. However, the 17% drop in the IHIT NAV has put many term investors on guard, who now worry that JPI could experience a similar fate.

Our view is that this is unlikely to happen for several reasons.

One, we are unlikely to see the kind of meltdown that we saw in CMBS in preferreds as well. For that to happen, we would need to see a full-fledged banking crisis.

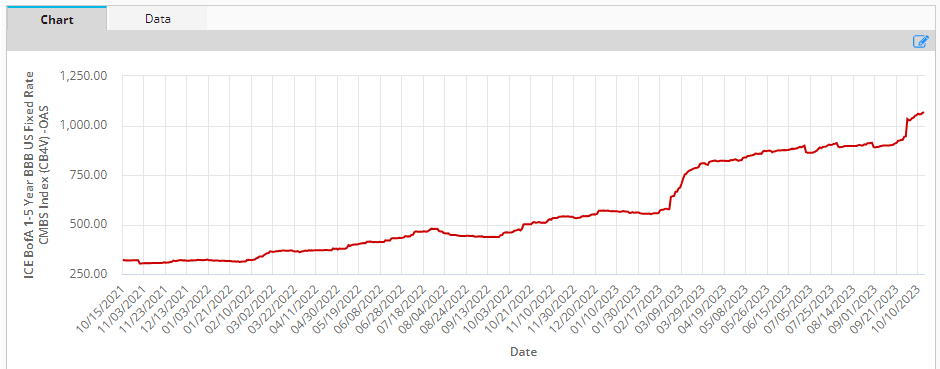

As the chart below shows, short-term BBB-rated CMBS experienced spread widening of around 5% since the start of the year - a factor responsible for a large portion of the IHIT NAV drop.

{kind=link}

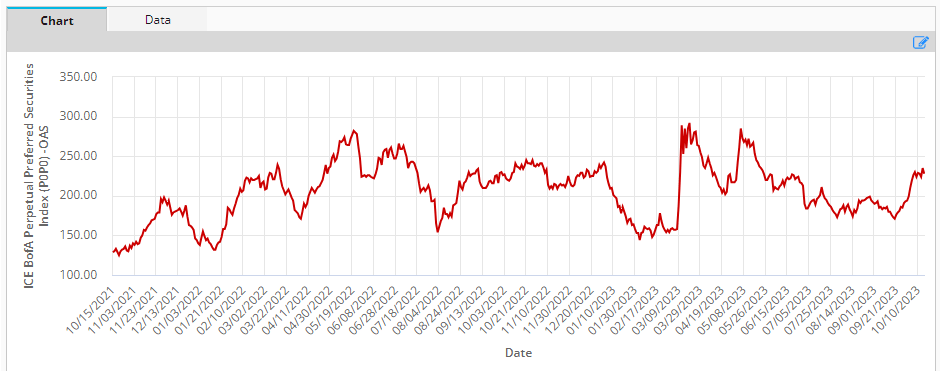

The preferreds sector has been fairly stable, on the other hand. Even in early March, when many thought that the industry would see a wave of failures, preferred credit spreads stood only 0.5% wider than their level at the start of the year. With the Bank Term Funding Program now in place, banks are much less likely to fail, even with longer-term rates now standing higher than they were during the March mini-crisis.

{kind=link}

Two, IHIT and JPI have different managers. Nuveen has gone through a number of fund terminations, including those holding less liquid securitized assets, and the NAVs of these funds have behaved very well through the termination period.

Three, unlike IHIT, JPI is unlikely to need to sell much of its portfolio. This is because most likely what will happen with JPI is what happened with JPT, which was another Nuveen term preferred CEF.

And what happened with JPT was that Nuveen offered shareholders to turn the fund into a perpetual one but also offered a tender offer for shareholders. There were enough assets left over after the tender offer for the fund to carry on, and so it does.

This scenario is better than a termination because it prevents excessive NAV damage from total portfolio turnover, and it keeps the fund outstanding. Investors still get their discount amortization by selling back to Nuveen at the NAV.

It’s possible too many shareholders tender, which would cause the fund to liquidate, however not all the fund’s assets will need to be sold to satisfy the tender offer.

JPI is trading at a 5.5% discount, which translates into an attractive level of discount amortization - what we call the pull-to-NAV yield, as shown below.

Systematic Income CEF Tool

Obviously, the NAV is going to move around through next year and so investors could still end up with a loss even if they monetize full amortization of the 5.5% discount, however, the margin of safety is attractive. And as the chart above of preferreds spreads shows, the valuation of the sector is not particularly expensive, which provides a decent entry point on a solely NAV basis.

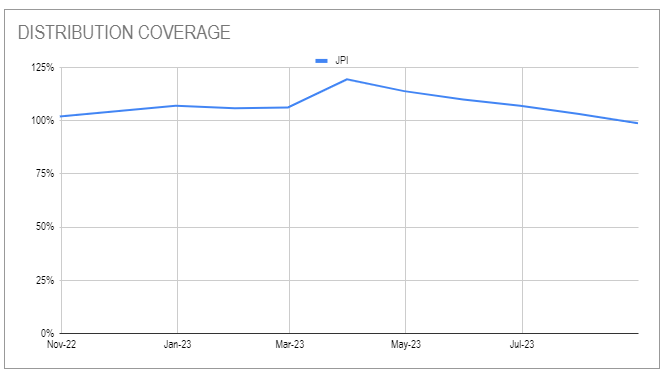

JPI has cut its distribution a couple of times over the past year - its coverage has risen as a result but is now falling steadily again.

{kind=link}

The good news on the distribution front is two-fold. One, close to 20% of its leverage is locked in till mid next year at a bit over 3% versus a standard rate of around 6%. We don't see the impact of this hedge in net income, which means net income is most likely understated.

And two, short-term rates have flatlined, so we shouldn't expect coverage to fall much more from current levels.

In any case, even if we do get another distribution cut it would be welcome as the JPI discount would likely widen from current levels, generating an even higher discount amortization tailwind for new capital.

Takeaways

We see value in JPI as an alpha opportunity through its likely tender offer in the second half of next year, which offers investors a mid-single digit opportunity in addition to its 7% current yield (which is somewhat understated relative to its underlying portfolio yield) for a low double-digit total "yield".

The broader preferreds sector remains attractive in our view, given the combination of its decent quality and high yields. It's important to stress that without this alpha term component, JPI (as a perpetual CEF) would not be an attractive fund - investors can get a higher and more efficient yield elsewhere in the preferreds CEF space or by allocating to individual preferreds.

We have tended to avoid perpetual Nuveen preferreds funds for several reasons. One, other preferreds CEFs, most notably, the Cohen & Steers suite, is more efficient from a net income perspective given their higher level of interest rate hedges. And two, Nuveen preferred CEFs have leverage caps, which makes them more vulnerable to deleveraging and serial locking in of economic losses.

Nuveen have been very good at providing investors an exit at the NAV across their term CEFs, whether through termination or tender offers. Because JPI is not a target term CEF, we expect Nuveen to run a tender offer much like it did with JPT - another Nuveen preferred term CEF - before its conversion to a perpetual fund.

Overall, this means investors are looking at a low double-digit yield opportunity for taking exposure to high-quality assets (even if it didn't feel like that in March). JPI remains in our Income Portfolios.

For further details see:

JPI: A Likely Alpha Opportunity For This Term Preferred CEF