KBE - JPI: An Interesting Opportunity For Yield And Capital Gains

2023-10-18 15:23:16 ET

Summary

- Nuveen Preferred & Income Term Fund offers a 7.07% yield, which compares respectably to most alternatives today.

- The JPI closed-end fund is set to expire next year and its shares are currently trading at a discount, providing potential for capital gains.

- The fund primarily invests in preferred stock and other income-producing securities, but its exposure to interest rate fluctuations poses risks.

- The fund failed to cover its distributions over the past two years, and net asset value has been deteriorating.

- The fund is currently trading at a big discount to NAV, which almost guarantees capital gains if its net asset value remains relatively stable for ten months.

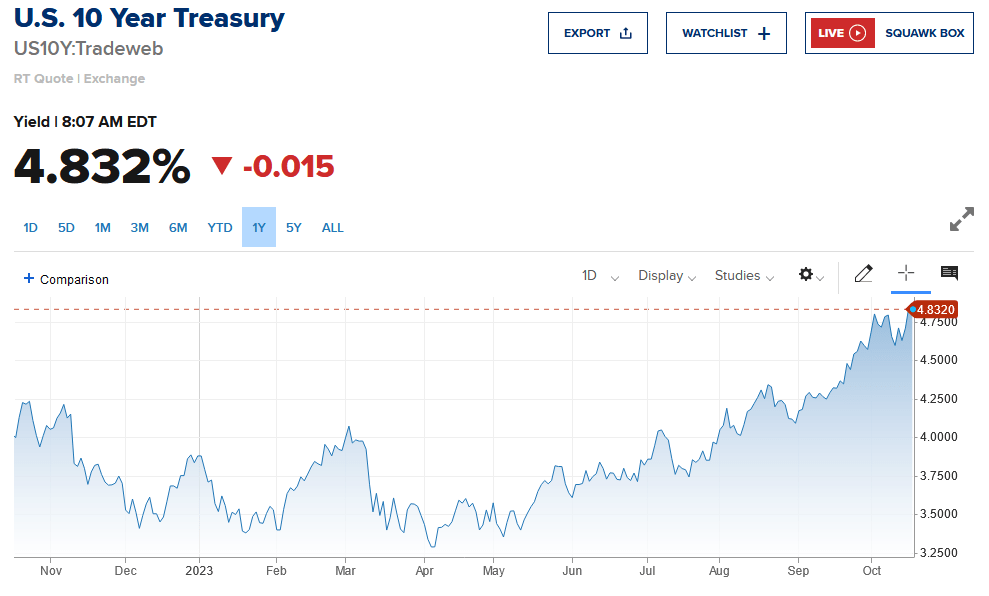

The Nuveen Preferred & Income Term Fund (JPI) is a closed-end fund, or CEF, that income-seeking investors might find attractive, as its 7.07% yield is higher than for many assets and indices in the market today. However, that yield is admittedly not as attractive as it once was, and there are numerous junk bond funds and similar things that can beat it. After all, rates have risen, and this has pushed up the yields of many risk assets. After all, the ten-year U.S. Treasury (US10Y) yields 4.832% today following a very strong run over the past year:

{kind=link}

As such, most investors are now going to be demanding a yield well above 7% from just about anything in the fixed-income space right now in order to provide compensation for taking on the additional risk of investing in a corporate issue compared to the easy option of just buying government bonds. We can see this in the fact that the iShares Preferred and Income Securities ETF ( PFF ) is yielding 7.07% as of the time of writing.

Honestly, the fact that the preferred stock index has a higher yield than the Nuveen Preferred & Income Term Fund might beg the question of why investors should bother buying this fund when they could just buy the index. While the Nuveen Preferred & Income Term Fund does have a better yield than Treasuries or just about any dividend-paying common equity, it clearly does not compare particularly well to corporate fixed-income securities in terms of yield.

The answer to this question can be found in the fact that this fund is almost guaranteed to deliver fairly solid capital gains over the next ten months unless rates increase dramatically. This comes from the fact that this is a term fund set to expire next year and its shares are currently trading at a discount. The shares are set to be redeemed at net asset value, so that should result in the discount narrowing until the shares start trading at a price that is very close to the net asset value. Thus, assuming that interest rates do not increase dramatically by then, investors purchasing the fund today should get some capital gains in addition to the distributions that the fund pays out over the period between now and its expiration.

We should still examine this fund though, as there is no guarantee that the fund's assets will have the same value at expiration as they have today.

About The Fund

According to the fund's website , the Nuveen Preferred & Income Term Fund has the primary objective of providing its investors with a high level of current income and total return. This is not surprising considering that the name of this fund implies that it will be investing primarily in preferred stock and other income-producing securities, such as corporate bonds. As is frequently the case, the website provides a much more detailed description of the fund and its strategy:

The Fund seeks to provide a high level of current income and total return by investing at least 80% of its managed assets in preferred and other income-producing securities, including hybrid securities such as contingent capital securities, with a focus on securities issued by financial and insurance firms. At least 50% of its managed assets are rated investment grade at the time of purchase or, if unrated, judged to be of comparable quality by the fund's portfolio team.

The Fund uses leverage and has a 12-year term and intends to liquidate and distribute its then-current net assets to shareholders on or before August 31, 2024.

That second paragraph is particularly important in the case of this fund. In many cases, investors might purchase a closed-end fund at a discount on net asset value, hoping that they can benefit from capital gains as the discount narrows. However, this sometimes fails to occur, and the fund winds up trading at a perpetual discount to net asset value. Many energy infrastructure funds are like this, as they have been trading at double-digit discounts for years and have never seen their valuation improve, not even during 2022 when energy prices were near their all-time inflation-adjusted highs.

This fund should not really have that problem, though, because of the forced liquidation at the end of August 2024. This event will result in the fund selling off all of its assets and then distributing the money to the shareholders. Thus, even if the market never closes the current price discount, the fund will still deliver the net asset value on the liquidation date. Thus, an investor should receive a fairly attractive capital gain on that date at the latest. This fund has been trading at a discount for quite some time:

CEF Connect

Thus, in theory, anyone buying it right now should effectively be guaranteed a capital gain over the next ten months, plus the distributions that the fund delivers in the interim.

However, that scenario is dependent on the fund's net assets remaining stable between now and the liquidation date. With many fixed-income closed-end funds, that is pretty easy to accomplish. All the fund has to do is buy bonds with a maturity date that is pretty close to the liquidation date and allow them to mature. That would result in the bonds paying out their face value at maturity, and the principal can then be delivered to the shareholders during liquidation. However, this fund's assets consist primarily of preferred stock. As we can see here, 55.90% of the portfolio's assets are invested in preferred stock:

CEF Connect

One of the defining characteristics of preferred stock is that it has no maturity date. There might occasionally be a preferred stock that becomes callable on a certain date or that has a maturity date that is set ridiculously far into the future, but for the most part preferred stock does not have a guaranteed return of principal on a certain date in the way that bonds do. A look at the fund's annual report shows that just about all of the preferred stocks in the portfolio either have no maturity date or have a maturity date that is far beyond the expected liquidation date of the fund. This is important, as it means that this fund has far more exposure to interest rate fluctuations than we would expect from a bond term fund that has its assets maturing right around the liquidation date of the fund.

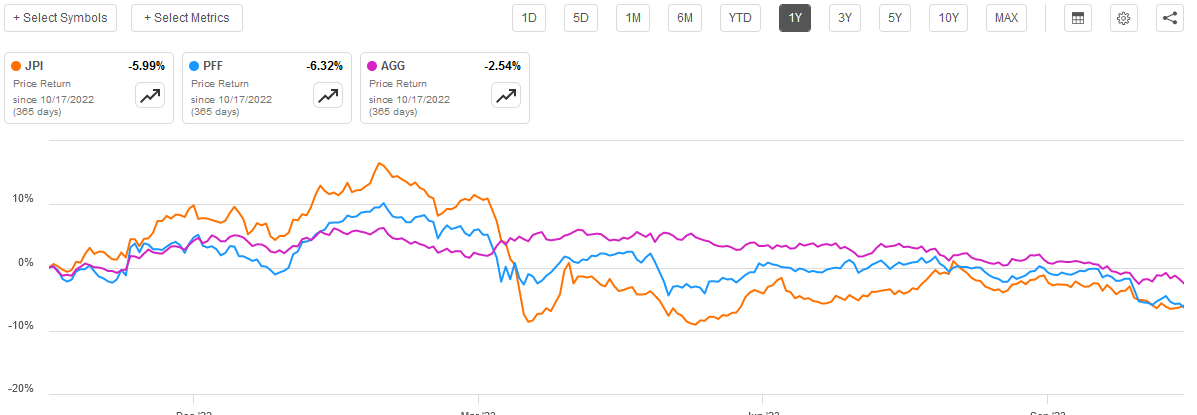

We can certainly see the impact of the fund's exposure to interest rate risk in its recent performance. Over the past year, shares of the Nuveen Preferred & Income Term Fund have declined 5.99%, which is a better performance than the American preferred stock index delivered but worse than the Bloomberg U.S. Aggregate Bond Index ( AGG ) over the period:

{kind=link}

This is not especially surprising considering that the fund has roughly a 50-50 split between preferred stocks and bonds. As such, we would expect it to deliver a performance that is somewhat between the two indices.

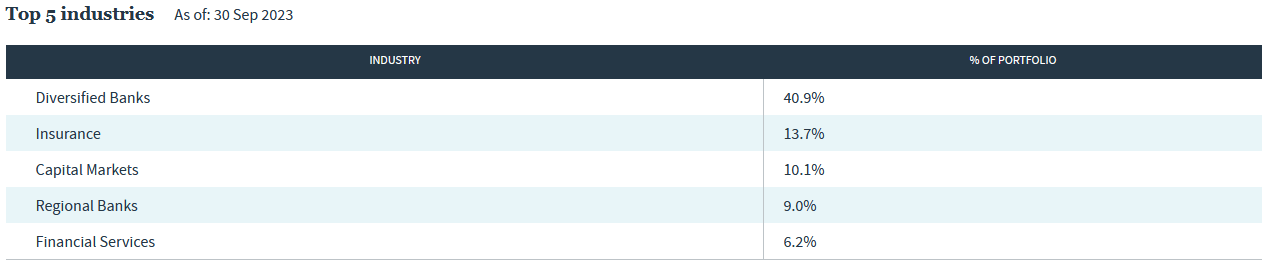

However, we can see that the fund's performance has been somewhat mixed over the period. For example, it was actually significantly outperforming both indices until about March of this year, when its share price fell to a level from which it has not really recovered. This makes sense when we consider the description of the fund's strategy from the webpage. Nuveen specifically states that this fund invests heavily in securities issued by banks and insurance companies. As of right now, 40.9% of the fund's assets are invested in securities issued by diversified banks and another 9.0% are issued by regional banks. However, just about all of its holdings are issued by companies that have some connection to the financial sector:

{kind=link}

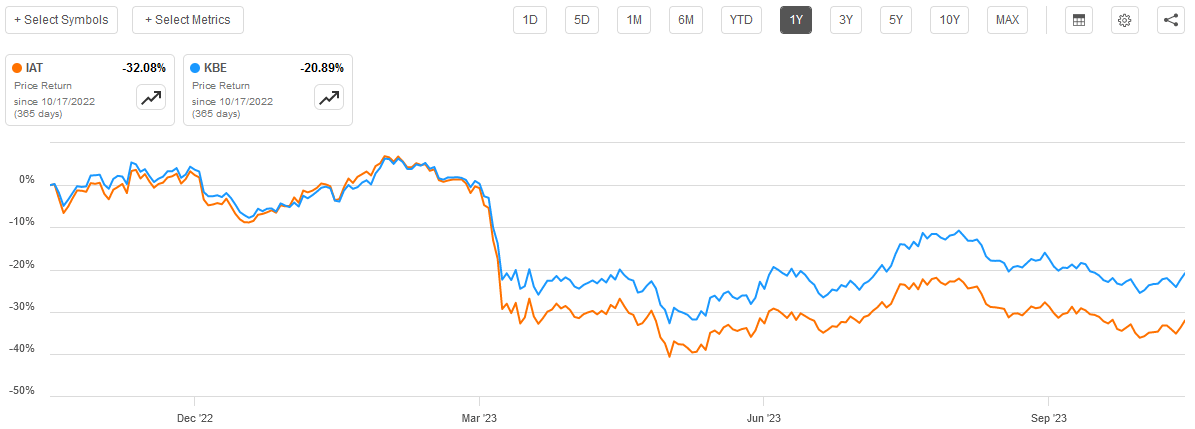

Silicon Valley Bank collapsed on March 10, 2023, which sparked a crisis of confidence among investors with respect to the financial solvency of regional banks. There was a mass sell-off of the common stock and other securities linked to these banks around that time, from which they have not yet recovered as of today. We can see this in the fact that both the SPDR® S&P Bank ETF ( KBE ) and the iShares U.S. Regional Bank ETF ( IAT ) declined substantially around that time and have been relatively flat since bottoming out:

{kind=link}

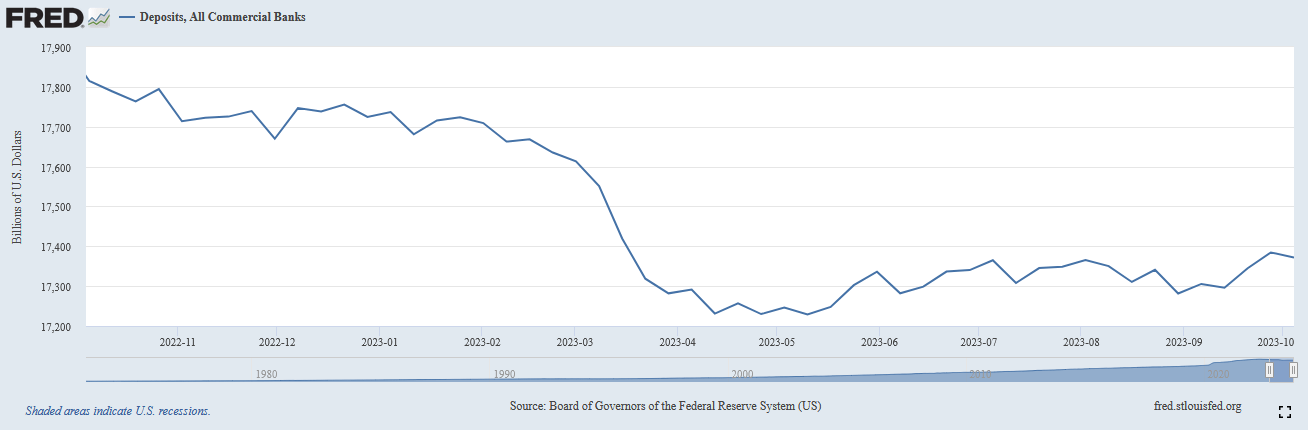

As the Nuveen Preferred & Income Term Fund invests heavily in preferred stock issued by banks, it only makes sense that the fund would have similar performance. After all, the sector is still sitting on an enormous number of unrealized losses and that is unlikely to change until either all of the long-term bonds in their portfolios mature (the "toxic securities" are U.S. Treasuries in many cases) or until interest rates drop back to the 0% range. That second scenario seems highly unlikely to happen before those assets mature. The Federal Reserve's emergency lending program has managed to stabilize the sector, but investors still have some concerns about the solvency of banks. These concerns are exacerbated by the fact that depositors continue to pull their money out of bank accounts in favor of much higher-yielding money market funds.

{kind=link}

It is curious then that the preferred stock index did not decline as much as the Nuveen Preferred & Income Term Fund in response to the regional banking crisis. After all, 73.70% of the index consists of preferred securities issued by financial institutions. The fact that the Nuveen Preferred & Income Term Fund employs leverage as a method of artificially boosting its portfolio yield likely played a role in this, as that would amplify its decline during such a scenario.

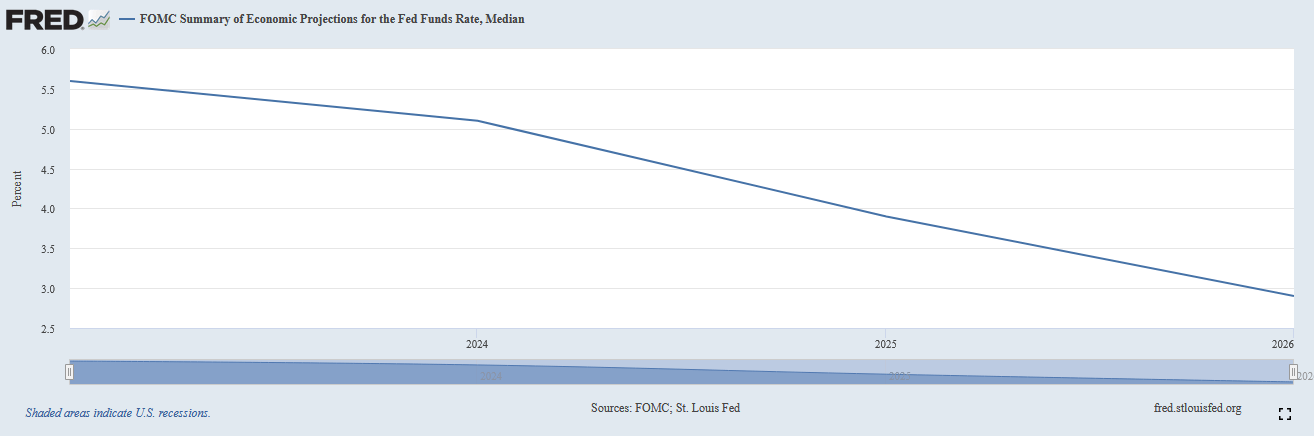

The big question at the moment for this fund is where the fund's net asset value will be on August 31, 2024, when it is liquidated. This depends on interest rates, which may prove to be higher than many people think right now. The median economic projection by the members of the Federal Open Market Committee is that rates will slowly begin to decline from here on out, with the effective federal funds rate exiting 2024 at 5.10% compared to 5.33% today:

{kind=link}

However, this could be very quickly derailed if energy prices push upward. I have seen some military commentators and analysts suggesting that the current situation in Israel might escalate into a full-blown regional war, and that would obviously cause energy prices to surge and push up the inflation rate in the United States. That may force the Federal Reserve to hike rates to try and keep the economic situation under control. Oil actually did surge this morning as Iran called for an embargo against Israel, so that gives some support for this theory.

In addition, foreign central banks became net sellers of U.S. Treasuries in July, which may have been a factor that sparked the turbulence in the market around that time. As everyone reading this may recall, that was right about the time that bonds started to sell off in the United States and long-term rates started to rise. We can actually see this in the chart showing the ten-year Treasury yield that I included in the introduction to this article. As I pointed out in a few recent articles, American commercial banks have also been reducing their U.S. Treasury holdings over the past several months. The United States Treasury has certainly not stopped its issuance of a growing number of securities to fund the Federal deficit, however. That could very easily push up interest rates regardless of what the Federal Reserve does because the government needs somebody to be willing to buy its Treasuries and the only way to attract buyers is to offer higher yields.

Any increase in rates will probably have the effect of causing the price of the securities held by the Nuveen Preferred & Income Term Trust to decline. This would not be a problem were it holding bonds that matured around the liquidation date as the fund could simply hold the bonds to maturity. However, since any liquidation would be conducted at the then-current value of the assets, investors today might wind up being forced to eat realized capital losses depending on how far the securities' values decline between now and the liquidation date.

As such, there could still be risks here, despite the liquidation being only ten months away.

Leverage

As mentioned earlier in this article, the Nuveen Preferred & Income Term Fund employs leverage as a method of boosting its effective portfolio yield. I have explained how this works in a number of previous articles. To paraphrase myself:

In short, the fund borrows money and then uses this borrowed money to purchase preferred stock or other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, it is important to note that this strategy is not as effective today as it was two years ago when the borrowing rate was essentially 0%. This is because the difference between the interest rate that the fund has to pay on the borrowed money and the yield that it receives from the purchased assets is less than it once was.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. Thus, the fund will decline much more during a market correction than it would if it were unleveraged. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like a fund's leverage to exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Nuveen Preferred & Income Term Fund has leveraged assets comprising 38.00% of its total portfolio. As such, its current leverage is well above the one-third level that we want to see. As I have pointed out in a few previous articles though, fixed-income funds like the Nuveen Preferred & Income Term Fund can get away with carrying a higher level of leverage than a common stock fund due to the comparatively low volatility of its assets. This fund is not excessively leveraged compared to what we have seen recently with other fixed-income funds, so it is okay on those grounds. However, since it seems that interest rates are more likely to trend upward from here than they are to decline in the near term, a lower level of leverage would be preferable to reduce the amount of money that the fund will lose the next time rates go up.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Nuveen Preferred & Income Term Fund is to provide its investors with a very high level of current income. In order to accomplish this objective, the fund invests primarily in preferred stocks and other income-producing securities. The U.S. preferred stock index currently has a 7.33% yield, so we can quickly see that many of the securities in which this fund invests are going to have a relatively high yield. This fund applies a layer of leverage to boost the effective yield beyond that of any of the assets that are actually held by it. The fund collects all of the money that is paid by the securities in the portfolio and then pays it out to the shareholders, net of its own expenses. As such, we might expect that this fund would have a very high yield itself.

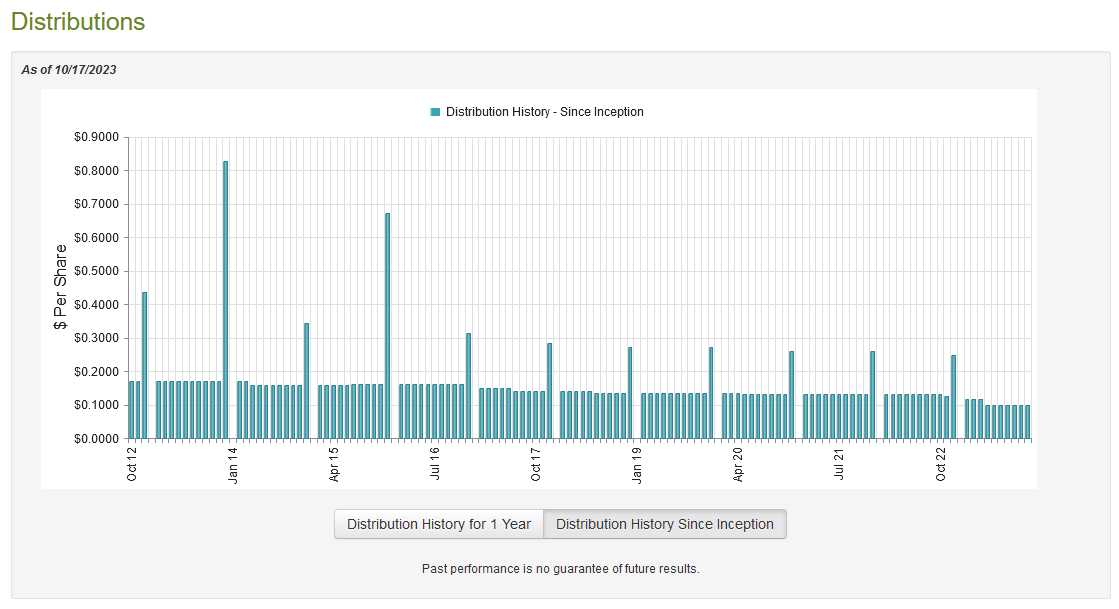

This is certainly the case, as the Nuveen Preferred & Income Term Fund pays a monthly distribution of $0.0980 per share ($1.176 per share annually), which gives it a 7.07% yield at the current price. Unfortunately, this fund has not been especially consistent with respect to its distribution over the years, as it has steadily decreased since its inception date:

{kind=link}

As such, this fund may not be appealing to anyone who is seeking a stable and secure source of income to pay their bills or finance their lifestyles. Indeed, the fact that it has a liquidation date of August 31, 2023, further reduces its appeal to those investors since they would need to find a new place to put their money after liquidation. However, the fund will continue to pay a distribution to its shareholders until its liquidation date, so we do want to examine how well it can accomplish that based on its current financial performance. After all, the situation that we want is for it to sustain a stable payout until it liquidates.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on July 31, 2023. A link to this report was provided earlier in this article. This is nice because this period includes two very divergent markets. For most of the first half of it, interest rates were rising and the market was generally reacting with concern regarding the end of the "free money" era that has dominated much of the 21st-century American economy. The second half of the period covered by this report was characterized by a great deal of optimism surrounding the possibility that the Federal Reserve will quickly pivot with respect to monetary policy and begin to cut interest rates. As such, fixed-income assets caught a bid and their prices went up, providing the fund with an opportunity to earn some capital gains by selling into a buoyant market.

During the full-year period, the Nuveen Preferred & Income Term Fund received $9,970,220 in dividends along with $35,456,169 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $45,494,531 over the period. The fund paid its expenses out of this amount, which left it with $26,244,685 available for shareholders. That was, unfortunately, not nearly enough to cover the $31,198,214 that the fund paid out to its investors as distributions during the period. At first glance, this is likely to be concerning as we usually like fixed-income funds to cover their distributions solely with net investment income. This fund clearly failed to accomplish that task.

However, there are other methods through which the fund can obtain the money that it needs to cover its distributions. For example, it might have been able to sell appreciated assets into the ebullient market in order to generate some capital gains. Unfortunately, the fund failed at this task overall. The fund reported net realized losses of $16,689,405 and had another $42,595,960 net unrealized losses. Overall, the fund's net assets declined by $64,238,894 over the period after accounting for all inflows and outflows. That is quite concerning as it indicated that the fund failed to cover its distributions for the second year in a row. Thus, the fund has consistently been paying out more than it managed to earn from its portfolio over the past twenty-four months.

This certainly explains why the fund's management thought was necessary to cut the distribution in February and again in May. It remains to be seen whether or not the fund can sustain the distribution at the new level, and we will have to wait until the fund's semi-annual report is released next year before we know for sure. While there may be some investors thinking that it is not a huge deal if the fund overdistributes right now because it will liquidate in ten months, it is important to keep in mind that if it pays out too much today, the amount of money that it can pay out at liquidation will be reduced.

Valuation

As of October 17, 2023 (the most recent date for which data is currently available), the Nuveen Preferred & Income Term Fund has a net asset value of $17.62 per share but the shares currently trade for $16.56 each. This gives the fund's shares a 6.02% discount on net asset value. This is actually quite a bit better than the 5.40% discount that the shares have had on average over the past month, so now could be a good time to enter the fund if you want to add it to your portfolio.

One thing that is important to keep in mind with this fund is that when it liquidates, it will do so at whatever the net asset value is on the date of liquidation. Thus, by buying the fund at a discount, you are essentially guaranteeing yourself a capital gain equal to the discount if the net asset value stays stable over the next ten months. While there is no guarantee that this will be the case, the larger the discount the more likely it is that you will ultimately realize a gain from the liquidation.

Conclusion

In conclusion, the Nuveen Preferred & Income Term Fund is an interesting fund that offers potential investors an opportunity to receive both income and a significant capital gain over the next ten months. The fund is set to liquidate next August, so by buying the fund's shares at a discount now, there could be an opportunity for gains. Unfortunately, a continued increase in interest rates does pose a risk to this strategy, but the larger the discount the better the chance of getting a significant capital gain.

Right now, Nuveen Preferred & Income Term Fund shares seem to be trading at a reasonable price to ensure some sort of gain. Overall, this fund could be an interesting trade for an income-focused investor who is not turned off by the fact that the fund will only provide income for a bit less than a year.

For further details see:

JPI: An Interesting Opportunity For Yield And Capital Gains